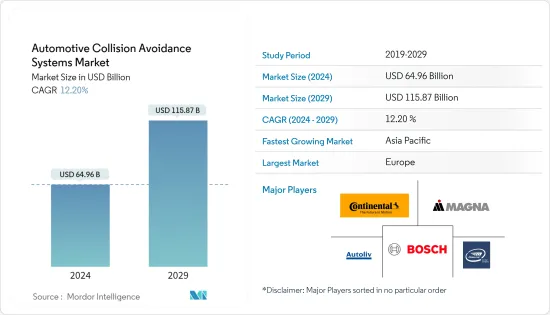

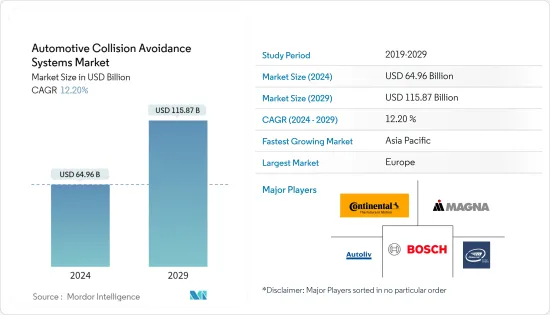

자동차 충돌 회피 시스템 시장 규모는 2024년에 649억 6,000만 달러로 추정되며, 2029년에는 1,158억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 12.20%로 성장할 전망입니다.

자동차 충돌 회피 시스템은 환경 입력을 수신하고 그에 따라 적응함으로써 임박한 충돌을 방지합니다. 복잡한 상황에서는 드라이버를 제어하고 복잡한 기능을 수행합니다. 또한 센서와 카메라를 사용하여 데이터를 수집하고 컨트롤러 유닛에서 처리합니다. 이 장치는 운전자에게 신호를 보내고 운전과 다른 운전자 모두에 대해 충돌이나 부상 위험을 증가시킬 우려 사항을 경고합니다.

자동차에 탑재되는 안전시스템을 개선하기 위한 각국 정부의 다양한 대처가 큰 성장요인으로 여겨지고 있습니다. 예를 들어 미국의 국가운송안전위원회(NTSB)는 가장 바람직한 10가지 운송안전 개선 목록을 발표했습니다. 이 목록은 승객의 안전을 위해 자동차에 장착 할 수있는 기술을 도입하는 것을 제안합니다.

자율주행차에 대한 수요 증가가 자동차 충돌 회피 시스템 수요를 견인하고 있습니다. 그러나 높은 설치 비용은 시장 성장을 방해합니다. 한편, 자동차 안전기준에 대한 우려 증가와 자동차에 대한 전자통합 증가는 충돌회피 시스템 시장의 추가 확대 기회를 창출할 것으로 예상됩니다.

ADAS(첨단운전지원시스템) 시장은 예측기간 중에 큰 성장이 예상됩니다. 다양한 단체와 대규모 OEM에 의한 안전 캠페인이 증가하고 있는 것이, 자동차의 안전성에 대한 일반 시민의 의식을 높이는 큰 요인이 되고 있습니다.

고객의 의식이 높아짐에 따라 자율 주행 기능과 고급 안전 기능을 갖춘 자동차에 대한 수요가 증가하고 있습니다. LiDAR은 레이저 광을 타겟에 조사하고 센서를 사용하여 반사를 측정하여 거리를 측정하는 데 사용됩니다. 자동차용 LiDAR 시스템은 주로 충돌 경고 및 회피 시스템, 블라인드 스팟 모니터, 레인 유지 어시스트, 레인 이탈 경고, 적응형 크루즈 컨트롤 등의 반자율 주행 또는 완전 자율 주행 지원 기능에 사용됩니다. 또한 자동 운전 차량의 모든 운전 모드에서 완벽한 자동화를 제공합니다.

자율주행차와 반자율주행차 업계 전체에서의 신흥국 시장의 발전, ADAS 탑재차에 대한 각국 정부의 중시의 높아짐, LiDAR 신흥기업에 대한 투자나 자금 조달의 급증은 시장 성장을 가속할 것으로 예상되는 핵심의 일부입니다.

예를 들어, 2023년 11월, AEye Inc.는 4Sight(TM) Flex, In-cabin Lidar system의 출시를 발표했습니다. 이것은 수평(H) 120°×수직(V) 30°의 시야, 최대 0.05°×0.05°의 초고해상도, 반사율 10%에서 최대 275m의 장거리 검출을 자랑하며, AEye의 1세대 설계 에 비해 모두 약 절반 크기와 최대 40%의 저전력입니다.

차량 제조업체와 장비 공급업체 모두의 이러한 개척에 더해, 거대한 크기와 기존 차량에 대한 확장성의 가능성도 함께, 이 시장 부문은 예측 기간 동안 큰 성장률을 나타낼 것으로 예상됩니다.

ADAS 탑재 차량에 대한 수요 증가와 건설적인 정부 지원은 예측 기간 동안 대상 시장의 성장을 뒷받침할 것으로 예상됩니다. 고객 수요가 증가함에 따라 자동차 제조업체는 R&D에 더 많은 투자를 하고 있습니다. 센서와 기술의 조합은 자동차 산업을 근본적으로 변화시켰습니다. 또한 혁신적인 기술이 새로운 고객을 유치하고 있으며 예측 기간 동안 시장이 크게 성장할 가능성이 높습니다.

중국은 아시아태평양의 자동차 제조 측면에서 유명한 국가 중 하나입니다. 중국에는 자동차 제조업체가 많이 존재하고 예측 기간 동안 시장에 유리한 기회를 만들 가능성이 높습니다. 중국 자동차공업협회(CAAM)에 따르면 2022년 7월 중국 자동차 판매량은 전년 대비 29.7% 증가한 242만대로 급증했습니다. 순전기자동차, 플러그인하이브리드차, 수소연료전지차 등 신에너지차 판매량은 2022년 7월 전년 대비 120% 증가했습니다.

중국은 세계 최대의 EV 시장 중 하나일 뿐만 아니라 급성장하는 EV 제조업체 중 하나입니다. 또한 많은 기업들이 중국 자동차 산업과 함께 확대되고 있으며 혁신적인 신제품을 통해 윈윈 솔루션을 실현하기 위해 파트너와 함께 개혁을 받아들이고 있습니다.

2023년 2월, Geely 는 신형 초소형 전기자동차 「Panda Mini」의 발매를 정식으로 발표했습니다. 표준 구성은 9.2인치 컬러 계기 패널, ABS(안티록 브레이크 시스템), EBD(전자 제동력 분배 시스템)를 갖추고 있습니다. 일부 모델에는 8인치 중앙 디스플레이와 백업 카메라가 장착되어 다양한 운전 장면에서 드라이버를 지원합니다.

Continental, Delphi, Denso, Autoliv, Mobileye, Panasonic, Hella 등 여러 회사가 자동차 충돌 회피 시스템 시장을 독점하고 있습니다. 그러나 이 시장은 여전히 여러 신규 진출기업을 유치하고 있으며, 이는 시장이 큰 잠재력을 지니고 있음을 보여줍니다. 이 회사들은 파트너십을 맺고 최신 ADAS 기능에 대한 투자를 계획하고 있습니다. 예를 들어, 2023년 11월, Hesai Technology는 Great Wall Motors와 자동차용 LIDAR 설계 파트너십을 발표했습니다. GWM의 복수의 승용차 모델이 헤사이의 초고해상도 장거리 라이더 AT128을 탑재해, 2024년부터 양산·납입할 계획입니다.

게다가 Nissan Motors는 2023년 6월 교차로에서의 충돌 회피를 특징으로 하는 LIDAR 기반의 새로운 선진 운전 지원 기술의 개발을 발표했습니다. 이 기술은 차세대 LIDAR를 활용한 Ground-Truth 지각 기술을 기반으로 하는 교차점 충돌 회피를 위한 새로운 제어 로직을 특징으로 합니다. 측면에서 물체의 속도, 위치 및 충돌의 잠재적 위험을 감지할 수 있습니다.

The Automotive Collision Avoidance Systems Market size is estimated at USD 64.96 billion in 2024, and is expected to reach USD 115.87 billion by 2029, growing at a CAGR of 12.20% during the forecast period (2024-2029).

Automotive collision avoidance systems prevent imminent crashes by receiving environmental inputs and adapting accordingly. It takes control and performs complicated functions for drivers in complex situations. It also uses sensors and cameras to collect data and process it through controller units. These units send signals to drivers to alert them about concerns that increase the risk of collision and injury, both regarding their driving and other's driving.

Various initiatives by governments of different countries to improve the safety systems onboard a car are considered significant growth factors. For instance, the National Transportation Safety Board (NTSB) of the United States released a list of the 10 most wanted transportation safety improvements. This list suggests incorporating technologies that can be used to equip vehicles for passenger safety.

Growing demand for autonomous vehicles drives the demand for automobile collision avoidance systems. However, market growth is hindered by a high installation cost. On the other hand, rising concerns about automotive safety norms and increased electronic integration in vehicles are anticipated to generate further opportunities for expansion in the collision avoidance systems market.

The advanced driver assistance system (ADAS) market is expected to grow significantly during the forecast period. Increasing safety campaigns by different organizations and large-scale OEMs are significant factors for the increased public awareness of vehicle safety.

Rising awareness among customers is leading to a growth in the demand for vehicles with autonomous and advanced safety features. LiDAR is used to measure distances by illuminating the target with laser light and measuring the reflection with a sensor. The automotive LiDAR system is used mainly in Semi or fully autonomous vehicle assistance features such as collision warning & avoidance systems, blind-spot monitors, lane-keep assistance, lane-departure warning, and adaptive cruise control. They also offer complete automation under all driving modes for self-driving cars.

Increasing developments across the autonomous and semi-autonomous vehicle industry, rising emphasis from the governments for ADAS-incorporated vehicles, and a surge in investments and funding in LiDAR startups are some of the keys that are expected to drive the market growth.

For instance, in November 2023, AEye Inc. announced the launch of 4Sight(TM) Flex, In-cabin Lidar system. It boasts a 120o horizontal (H) x 30o vertical (V) field of view, with ultra-high resolution of up to 0.05° x 0.05° and long-range detection of up to 275 meters at 10% reflectivity, all at approximately half the size and up to 40% lower power consumption compared to AEye's first-generation design.

Due to such developments from both vehicle manufacturers and equipment suppliers, combined with the immense size and potential for scalability to existing vehicles, this segment of the market is anticipated to witness a significant growth rate during the forecast period.

Growing demand for ADAS-equipped vehicles and constructive government support are expected to boost the target market growth over the forecast period. With increased customer demand, automakers invest more in research and development. The combination of sensors and technology has fundamentally transformed the automotive industry. Furthermore, innovative technologies attract new customers, which is likely to witness major growth for the market during the forecast period.

China is one of the prominent countries in terms of vehicle manufacturing in Asia-Pacific. China has a major presence of automotive manufacturers, which is likely to create lucrative opportunities for the market during the forecast period. According to the China Association of Automobile Manufacturers (CAAM), China's auto sales surged 29.7% in July 2022, standing at 2.42 million units, compared to the previous year. The sales of new energy vehicles, including pure electric vehicles, plug-in hybrids, and hydrogen fuel-cell vehicles, increased by 120% in July 2022 from the previous year.

China is not only one of the world's largest EV markets, but it is also one of the fastest-growing EV manufacturers. Many players are also expanding alongside the Chinese automobile industry, embracing reforms alongside its partners in order to achieve win-win solutions through innovative new products.

In February 2023, Geely officially announced the launch of the new Panda Mini micro-electric vehicle. In standard configuration, the vehicle features a 9.2-inch color instrument panel, ABS (Anti-lock Braking System), and EBD (Electronic Brakeforce Distribution). Some models feature an 8-inch central display and a backup camera, assisting drivers in various driving scenarios.

A few players, such as Continental, Delphi, Denso, Autoliv, Mobileye, Panasonic, and Hella, dominate the automotive collision avoidance systems market. However, the market still attracts several new players, which indicates the great potential this market exhibits. They are entering partnerships and planning to invest in the latest ADAS features. For instance, in November 2023, Hesai Technology announced an automotive LIDAR design partnership with Great Wall Motors. Multiple passenger vehicle models from GWM will equip Hesai's ultra-high resolution long-range lidar AT128, with plans for mass production and delivery starting in 2024.

Additionally, in June 2023, Nissan Motors announced the development of new LIDAR-based advanced driver-assistance technology, which features intersection collision avoidance. The technology features a new control logic for intersection collision avoidance based on ground-truth perception technology utilizing next-generation LIDAR. It can detect an object's speed, location, and potential risk of a collision from a lateral direction.