ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

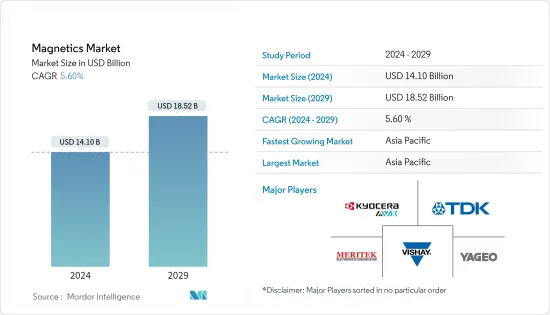

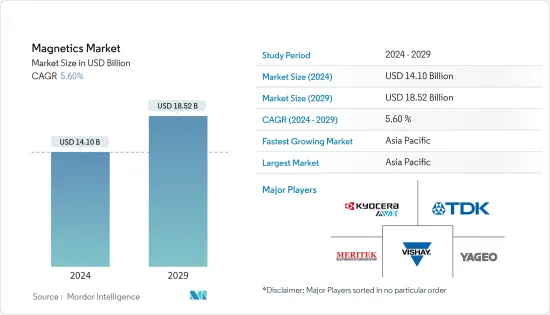

세계의 자기(Magnetics) 시장 규모는 2024년에 141억 달러에 달하고, 2024-2029년에 걸쳐 CAGR 5.60%로 추이하며 성장할 것으로 예상되며, 2029년에는 185억 2,000만 달러에 달할 것으로 예측되고 있습니다.

자기 부품은 냉장고 및 TV에서 통신 장비에 이르기까지 고급 산업 장비와 일반 가정용 전기 제품 모두에서 널리 채택됩니다. 자기 부품은 자동차에서 중요한 역할을 하며 대시보드 디스플레이, 실내외 조명, 에어컨 제어 및 기타 시스템 전원의 전압을 모니터링합니다. 이러한 부품은 휴대폰, 컴퓨터, 통신 시스템 및 기타 전자 제품에 사용됩니다.

주요 하이라이트

HPC와 AI 수요는 세계적으로 폭발적으로 성장하고 있습니다. 마찬가지로 스마트폰, PC, 인프라 수요도 안정적입니다. 스마트폰 판매량은 2024년에 크게 회복되었으며 이러한 자성 부품 수요를 견인할 것으로 예상됩니다. 고주파 인덕터는 휴대폰에 사용되며 빠르고 안정적인 넷 서핑에 유용합니다. 게다가 모바일 통신 네트워크가 발전함에 따라 스마트폰에 탑재되는 인덕터의 수가 크게 증가하고 있습니다. 인덕터는 컬러 액정과 배터리 수명 향상 등 스마트폰의 다양한 기능을 강화합니다.

스마트폰 OEM은 2024년 인공지능 대응 스마트폰을 강화하고 생성형 AI 기능과 추가 스토리지 용량을 탑재함으로써 보다 우수한 배터리 수명 수요를 창출하고 있습니다. 게다가 기술이 발전함에 따라 소비자는 기존 기기보다 선진 기술 제품을 선호하게 되어 스마트폰 판매를 밀어올리고 있습니다.

연료전지, 풍력발전, 태양광발전 등 국가간 전력망 연결(슈퍼그리드)과 직류에 근거한 신재생에너지원의 요구는 세계적으로 확대되고 있으며, 자성부품 수요도 확대되고 있습니다.

기존에 변압기는 철제였지만, 소재의 발달에 수반하여, 실리콘강, 비정질강, 페라이트·세라믹 등이, 그 높은 관통성으로부터 변압기의 코어 소재로서 사용되고 있습니다. 마찬가지로, 인덕터나 EMI 필터에도 철이나 페라이트 등 자성 소재가 코어재로서 사용되고, 코일에는 구리가 사용되는 것이 일반적입니다.

현재 자율주행 기술과 ADAS의 급속한 진화에 따라 자동차에는 레이더, 카메라, LiDAR 등 수많은 센서가 탑재되어 있으며, 그 결과 자성 부품은 비약적으로 성장하고 있습니다. 자동차 분야의 진보가 계속되고 있기 때문에 주요 벤더는 소비자 수요에 대응하기 위해 제품 개발과 진보에 지속적으로 투자하고 있습니다.

예를 들어, TDK Corporation은 2024년 1월 차량용 오디오 버스(A2B) 용도로 고내구성, 넓은 동작 범위, 고인덕턴스 공차를 실현한 새로운 인덕터 KLZ2012-A 시리즈를 출시했습니다. 2024년 1월부터 양산을 개시합니다. A2B 기술은 광범위한 통신 버스 케이블 하네스를 경량화하기 위해 개발된 것으로, 자동차의 연비 향상을 최종 목표로 하고 있습니다.

자기 시장 동향

산업용(모터/UPS)이 성장을 견인

산업용 모터는 전기 에너지를 기계 에너지로 변환하는 전기 장비입니다. 일반적으로 발전기와 송전망과 같은 교류(AC) 전원으로부터 전력이 공급됩니다. 산업용 모터는 다양한 산업에서 사용되는 다양한 장비 및 기계에 전력과 움직임을 공급하도록 특별히 설계되었습니다. 고부하를 견디고 까다로운 환경에서도 작동해야 하기 때문에 이러한 모터는 일반적으로 주택 및 상업 환경에서 사용되는 것보다 내구성이 높고 강력합니다. 산업용 모터·용도에 있어서 자기 인덕턴스에 대한 요구의 고조가 시장을 견인합니다.

Industrial Energy Accelerator의 보고서에 따르면 기업이 소비하는 세계 전기 에너지의 대부분은 가동중인 수백만 대의 전기 모터로 인한 것입니다. 이 모터는 환기, 압축 공기 생성, 물 펌핑 등 다양한 분야에서 필수적인 산업 공정 및 보조 시스템에 전력을 공급하는 데 매우 중요합니다. 또한 산업용 모터 시장에서는 최근 AC 전원과 DC 전원 모두에서 작동하도록 설계된 범용 모터가 도입되었습니다. 이러한 모터에 대한 수요 증가와 다양한 공급업체의 개발 증가는 자성 부품 적용을 증가시킬 것으로 보입니다.

산업용 모터의 설계와 기능은 토크를 발생시키는 주요 방법으로 작용하는 자기 유도에 크게 의존합니다. 엔지니어는 자기 유도의 원리를 충분히 이해하고 다양한 설계 요소를 최적화함으로써 다양한 용도에 적합한 효율적이고 고성능의 모터를 개발할 수 있습니다.

데이터센터의 무정전 전원 공급 장치(UPS) 시스템에 대한 수요는 데이터센터에 대한 투자 증가로 인해 큰 성장을 나타냅니다. 다양한 산업이 디지털 업무와 서비스를 확대함에 따라 데이터 저장, 처리 및 관리에 대한 수요가 급증하고 있습니다. 결과적으로 이러한 요구 사항을 충족하기 위해 데이터센터 인프라에 많은 투자가 이루어지고 있습니다. Cloudscene에 따르면 2023년 9월 현재 중국에는 448개의 데이터센터가 있으며, 아시아 태평양의 어느 나라 및 지역보다 더 많은 시장 기회를 크게 찾을 수 있습니다.

급성장하는 중국

중국에서 가전, 자동차, 의료기기의 생산 증가에 따라 수동전자기기 수요는 예측기간 동안에도 견조하게 추이할 것으로 예상됩니다.

Rayming PCB 및 Assembly에 따르면 중국은 지난 몇 년간 전자 제조 산업을 지배하고 있습니다. 이 국가는 미국과의 최근 무역에도 불구하고 전자 제품의 필수 제조 장소입니다. 대규모 제조 업체로서 중국은 노트북과 휴대폰의 약 50%를 세계에 수출하고 있습니다.

세계 전자 시장은 2022년 3조 5,549억 4,000만 달러에서 2023년 3조 7,393억 7,000만 달러로 성장했습니다. 세계의 전자 분야에서 중국은 수익의 큰 비율을 차지하고 있습니다. 이 나라는 전자기기 생산국의 상위에 랭크되고 있습니다. 소비자 가전에서 산업용 부품에 이르기까지 다양한 전자 제품을 생산하고 있습니다. 남부의 동관, Shenzhen 같은 도시에는 공장이 있습니다. 또한 상하이와 블루 클라우드에도 공장이 있습니다.

중국은 노트북 제조업체의 세계 생산 점유율이 돌출하고 있습니다. 중국이 수입 반도체에 의존하고 있음에도 불구하고, 이 나라는 많은 세계 최고 수준의 노트북 브랜드에 대한 좋은 선택이 되고 있습니다. Kunshan과 Chongqing는 랩톱 제조의 2대 클러스터이며 Dongguan, Shenzhen과 같은 다른 인기 있는 전자 생산 기지도 있습니다. 이 허브는 노트북, 부품 및 액세서리 생산으로 유명합니다.

100만명 이상의 인구를 가진 도시가 미국에는 9개밖에 없는 것에 비해 중국에는 약 160개의 도시가 있습니다. 이에 따라 전자기기의 제조와 소비 확대로 모든 가전 및 가정용 전자기기의 전기유량 관리에 대응하는 다양한 수동부품의 요구가 높아질 것으로 예상됩니다.

지난 15년간의 EV 산업을 목표로 한 중국의 노력은 이 나라의 최근 역사에서 산업 정책의 가장 성공적인 사례 중 하나입니다. 보조금을 포함한 정부의 대규모 개입은 국내 산업과 시장의 동시성장을 가능하게 했습니다. 정책이 실시된 타이밍은 매우 중요했고, 배터리 기술 진보나 EV의 소비자 수용의 확대와 동시기에 실시되었기 때문입니다. 중요한 것은 기존 자동차 회사의 대부분이 최근까지 EV 기술을 부인했다는 것입니다.

한편 중국의 경쟁사는 내연기관 기술로 수십년에 걸쳐 축적된 지적재산을 가진 다국적 기업을 기술적으로 도약시킬 기회를 빠르게 잡았습니다. 중국은 또한 EV의 주요 부품인 리튬 배터리의 세계 주요 생산국이기도 합니다. 국제에너지기구(IEA)에 따르면 중국은 배터리의 65%, 양극의 80%를 생산하고 있으며, 에너지부의 추정은 더욱 높습니다. 이처럼 일본의 자동차 분야에서 조사된 시장 성장 전망이 제시됩니다.

자기 산업 개요

자기 시장은 단편화되어 있으며 제품에 많은 투자를 해온 오랜 기존 기업로 구성되어 있습니다. 신규 진출기업은 고액의 투자가 필요합니다. 각 회사는 강력한 경쟁 전략을 통해 지속되고 있으며, 주요 기업는 TDK Corporation, Yageo Corporation, Meritek Electronics Corporation, AVX Corporation(Kyocera Group), Vishay Intertechnolo입니다.

2024년 1월, TDK Corporation의 자회사인 TDK Ventures Inc.는 디지털과 에너지의 변화를 목표로 하는 싱가포르의 하이테크 기업인 Silicon Box에 출자했습니다. Silicon Box를 통해 반도체 패키지의 혁신 시장을 가속시킬 계획입니다.

2023년 11월, Bourns는 높은 자기 공진 주파수, 높은 Q, 엄격한 인덕턴스 공차를 가진 에어 코일 인덕터 시리즈를 발표했습니다. 모델 AC4842 RAir Coil Inductor Series는 RF 용도 설계자에게 광범위한 high Q 솔루션 옵션을 제공하는 저손실, 고주파 솔루션을 제공합니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사 전제 조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력도-Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

자기 디바이스 카테고리의 기술 개요

시장의 거시 동향 평가

제5장 시장 역학

시장 성장 촉진요인

신재생에너지 수요 증가

전기자동차와 자율주행차 수요 증가가 자기부품 시장을 견인

시장의 과제

금속 가격 상승이 부품 제조 비용에 영향

제6장 시장 세분화

유형별

권선 인덕터

다층 인덕터

박막 인덕터

페라이트 코어·EMC 부품

EMI 필터

RF/파워 트랜스

전류 감지·기타 변압기

최종 사용자 용도별

태양광 및 풍력

EV/HEV용

산업용(모터/UPS)

철도/수송

소비자 가전

기타 최종 사용자 용도

지역별

중국

일본

미국

대만

동남아시아

한국

유럽

남미

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

TDK Corporation

Yageo Corporation

Meritek Electronics Corporation

AVX Corporation(Kyocera Group)

Vishay Intertechnology

Panasonic Corporation

Taiyo Yuden Co. Ltd

Exxelia Technology

Bourns Inc.

Wurth Elektronik Group

Coilcraft Inc.

제8장 시장 전망

LYJ

영문 목차

영문목차

The Magnetics Market size is estimated at USD 14.10 billion in 2024, and is expected to reach USD 18.52 billion by 2029, growing at a CAGR of 5.60% during the forecast period (2024-2029).

Magnetic components are widely adopted in both advanced industrial and common household appliances, ranging from refrigerators and televisions to telecommunication devices. Magnetics plays a crucial role in cars, monitoring voltage in power supplies for dashboard displays, interior and exterior lighting, climate control, and other systems. These components are used in cell phones, computers, communication systems, and other electronic products.

Key Highlights

The global demand for HPC and AI is exploding. Similarly, the demand for smartphones, PCs, and infrastructures is stabilizing. Smartphone sales are expected to recover significantly in 2024, driving the demand for these magnetic components. High-frequency inductors are used in mobile phones, which help with fast and stable internet surfing. Furthermore, with the advancement in mobile communication networks, the number of inductors in smartphones is growing significantly. Inductors enhance various smartphones' functions, including improving color LCD and battery life.

Smartphone OEMs are ramping up Artificial intelligence-enabled smartphones in 2024, with generative AI capabilities and an additional storage capacity, which creates demand for better battery life. Further, with the advancement in technology, consumers prefer advanced technology products compared to older devices, which drives the sales of smartphones.

The need for inter-country power grid connections (super grid) and renewable energy sources based on direct currents, such as fuel cells, wind power, and solar power, is expanding globally, as is the demand for magnetic components.

Traditionally, transformers were made of solid iron; however, with the development of materials, silicon steel, amorphous steel, and ferrite ceramics have been used as core materials for transformers due to their higher penetrability. Similarly, inductors and EMI filters use iron, ferrite, and other magnetic materials as core material, and coils are usually made of copper.

With the current rapid evolution of autonomous driving technologies and ADAS, automobiles are prepared with numerous sensors such as radars, cameras, and LiDAR, resulting in dramatic growth in magnetic components. Owing to ongoing advancement in automotive sector, key vendors are continuously investing on product developments and advancement to meet consumer demand.

For instance, in January 2024, TDK Corporation launched a new inductor KLZ2012-A series, designed for automotive audio bus (A2B) applications with high durability, a wide operation range, and greater inductance tolerance. The company announced that the mass production of these new product series started in January 2024. A2B technology was developed to decrease the weight of cable harnesses containing of a broad variety of telecommunication buses, pointing at its final goal of amplified fuel efficiency of automobiles.

Magnetics Market Trends

Industrial (Motors/UPS) to Witness the Growth

Industrial motors are electrical devices that convert electrical energy into mechanical energy. They are commonly powered by alternating current (AC) sources like generators and power grids. Industrial motors are specifically engineered to supply power and movement to various equipment and machinery utilized in different industries. Due to their requirement to endure heavy loads and function in challenging environments, these motors are typically more durable and potent than those employed in residential or commercial settings. The growing need for magnetic inductance in industrial motor applications will drive the market.

The Industrial Energy Accelerator reports that a significant portion of the global electrical energy consumed by companies is attributed to the millions of electrical motors in operation. These motors are crucial in powering essential industrial processes and auxiliary systems such as ventilation, compressed air generation, and water pumping across various sectors. Additionally, there has been a recent introduction of universal motors in the industrial motors market, designed to work with both AC and DC power sources. The increasing demand for these motors and growing developments by the various vendors will increase the applications of magnetic components.

The design and functioning of industrial motors heavily rely on magnetic induction, which serves as the primary method for producing torque. Engineers can develop efficient and high-performing motors suitable for various applications by thoroughly comprehending magnetic induction principles and optimizing different design elements.

The demand for data center uninterruptable power supply (UPS) systems is experiencing significant growth due to the increasing investments in data centers. As various industries expand their digital operations and services, there is a surge in demand for data storage, processing, and management. Consequently, substantial investments are being made in data center infrastructure to meet these requirements. According to Cloudscene, as of September 2023, there were 448 data centers in China, the most of any country or territory in the Asia-Pacific region, where market opportunities can be found significantly.

China to Witness Rapid Growth

The demand for passive electronics is expected to remain strong in the forecast period due to increased consumer electronics, automotive, and medical equipment production in China.

According to Rayming PCB and Assembly, China has continued dominating the electronics manufacturing industry for some years. This country is an integral manufacturing place for electronics despite its recent trade with the United States. As a large manufacturing company, China exports about 50% of laptops and cell phones globally.

The global electronics market grew from USD 3554.94 billion in 2022 to USD 3739.37 billion in 2023. In the global electronics sector, China contributes a large percentage of revenue. This country is ranked among the top producers of electronic devices. It produces various electronics products, ranging from consumer electronics to industrial components. Cities such as Dongguan and Shenzhen in the South have factories. In addition, Shanghai and Choingun are home to factories.

China produces a prominent share of laptop manufacturers globally. Despite China's dependence on imported semiconductors, this country remains a good option for many world-class laptop brands. Kunshan and Chongqing are the two biggest clusters for laptop manufacturing and other popular electronic production hubs, like Dongguan and Shenzhen. These hubs are known for producing laptops, components, and accessories.

The country also holds a significant consumer market considering the country's large population, with about 160 Chinese cities having a population crossing one million people, compared to the US, having only nine cities that incorporate more than one million people. Thus, the growing electronics manufacturing and consumption are expected to drive the need for various passive components to address electric flow management in all consumer and household electronics.

China's initiatives targeting the EV industry over the past 15 years are one of the most successful cases of industrial policy in the country's recent history. Extensive government interventions, including subsidies, enabled the domestic industry and the market to grow simultaneously. The timing of the policies was crucial because they coincided with and magnified technological advancements in battery technology and greater consumer acceptance of EVs. Importantly, many existing automotive companies dismissed EV technology until recently.

Meanwhile, their Chinese competitors quickly grasped the opportunity to technologically leapfrog multinational corporations with decades of IP accumulated in internal combustion engine technology. China is also by far the main producer of lithium batteries globally, which are the main component in EVs. According to the International Energy Agency (IEA), the country accounts for 65% of battery and 80% of cathode production, and the Department of Energy's estimate is even higher. Thus, the growing prospect of the market studied in the country's automotive sector is shown.

Magnetics Industry Overview

The magnetics market is fragmented, comprising long-standing established players who have made significant investments in the product. The new players entering the market require high investments. The companies can sustain themselves through powerful competitive strategies, and key players are TDK Corporation, Yageo Corporation, Meritek Electronics Corporation, AVX Corporation (Kyocera Group), and Vishay Intertechnolo.

* In January 2024, TDK Corporations subsidiary TDK Ventures Inc. invested in Singaporean tech company Silicon Box for digital and energy transformation. It plans to accelerate the market for semiconductor packaging innovations through Silicon Box.

* In November 2023, The Bourns introduced an air coil inductor series with high self-resonant frequency, high Q, and tight inductance tolerance. The Model AC4842R Air Coil Inductor Series offers a low-loss, high-frequency solution that gives RF application designers a wider range of high-Q solution options.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Degree of Competition

4.3 Technological overview of Magnetic Device Categories

4.4 Assessment of Macro trends in the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Demand For Renewable Energy

5.1.2 Rising Demand For Electric and Autonomous Vehicles Drives Magnetic Components Market

5.2 Market Challenges

5.2.1 Rising Metal Prices Impacting Component Production Costs