ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

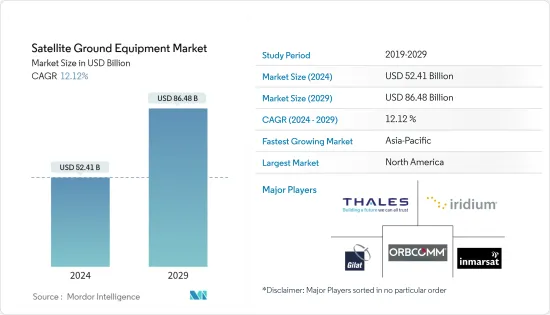

위성 지상 설비 시장 규모는 2024년 524억 1,000만 달러로 추정되고, 2029년에는 864억 8,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 12.12%로 성장할 전망입니다.

주요 하이라이트

위성 지상 설비 산업은 NOC 설비와 같은 무선 통신 솔루션의 진보, 이동 무선 통신 수요 증가, 공공 안전 용도의 대폭적인 전개에 의해 극적으로 성장하고 있습니다. 또한, 낮은 궤도(LEO) 위성 시스템, 높은 처리량 위성(HTS), Ku 밴드와 Ka 밴드 위성의 유익한 소개는 시장의 유리한 성장 기회를 늘리고 있습니다. 동시에 상용, 정부, 방위 등 각 부문의 다양한 용도에 사용되는 자율주행차와 커넥티드카의 방대한 수요는 첨단 커스터마이즈형 SATCOM 온더 무빙 안테나를 필요로 하며, 신뢰성이 높은 운용이 위성 지상 설비 시장을 견인하고 있습니다.

위성산업협회(SIA) 보고서에 따르면 GNSS 시장과 네트워크 장비가 확대됨에 따라 지상 장비의 수익이 크게 증가하고 있으며 고객 장비의 투자와 자원이 편평하거나 약간 감소하고 이동 위성 서비스가 조사한 시장 전체의 기본적인 성장 포인트가 되는 것을 밝히고 있습니다. 항공기 내에서 스마트폰이나 노트북을 사용하는 승객은 인터넷 및 비디오 스트리밍 서비스에 액세스하기 위한 기내 연결에서 혜택을 누릴 수 있습니다. 선박 관계자는 해도 업데이트, 엔진 모니터링, 기상 라우팅 방송 등 최신 해상 정보에 대한 승무원 연결을 통해 혜택을 누릴 수 있습니다. 백팩 단말기는 가혹하고 긴급한 조건에서 연결성을 지원하기 위해 신속하고 안정적으로 배치되어야 합니다.

HTS는 궤도에서 동일한 할당 주파수로 고정 위성 시스템에 비해 높은 처리량을 제공하는 위성입니다. HTS는 주파수와 여러 스폿 빔을 재사용하여 처리량을 향상시키고 전달 비트당 비용을 줄입니다. HTS는 주로 서비스가 잘 알려져 있지 않은 지역에 광대역 인터넷 액세스 서비스를 제공하기 위해 배포됩니다. 대부분의 HTS 위성은 주로 기업, 통신 및 해양 부문을 위해 설계되었습니다. 우주 및 위성 시스템 공급자는 고속 통신 서비스를 위해 HTS 위성을 발사합니다. HTS 위성 발사가 증가함에 따라 지상국 시설의 도입이 증가하고 시장을 견인하고 있습니다.

위성 방송은 멀티미디어 컨텐츠 및 방송 신호를 위성 네트워크를 통해 전달하는 것입니다. 방송 신호는 보통 TV나 라디오 방송국과 같은 방송국에서 나옵니다. 그런 다음 위성 업링크(업로드)를 통해 정지 인공위성으로 전송되고 개방 또는 보안 채널을 통해 다른 미리 정해진 지리적 위치로 재배포되거나 재전송됩니다. 직접 방송이나 위성 TV는 텔레비전 및 컨텐츠의 효과적인 전달 형태가 되고 있습니다. 광범위하고 제어 가능한 커버리지와 훨씬 더 넓은 대역폭으로 더 많은 채널을 방송할 수 있기 때문에 위성 TV는 매우 매력적입니다.

또한 현재 시장에는 다양한 위성 안테나 히터와 위성 안테나 제빙 시스템이 있으며 18인치 주거용 위성 TV 및 위성 인터넷 안테나에서 대형 상업용 및 기업용 VSAT에 이르기까지 모든 용도에 충분한 기회를 제공합니다. 위성 TV와 위성 인터넷 안테나에 눈과 얼음이 쌓이면 신호가 끊길 수 있습니다. 위성 제빙 시스템은 위성 안테나에 눈과 얼음이 쌓이는 것을 방지하는 한 가지 방법입니다.

오히려 해군이 사용하는 Advanced-EHF 위성이 장착된 멀티밴드 단말기는 꽤 비쌉니다. 게다가, 단말기의 구입이나 설치에 드는 비용은 로켓이나 우주선의 20배에서 30배가 됩니다. 위성과 단말의 개발이 별도로 이루어지는 것은 오랫동안 낭비와 비용 초과의 원인이 되어 왔습니다. 예를 들어, 공군이 우주선을 감독하는 한편, 육군이 무선을 감독할 수도 있습니다. 지상 통신 장비와 위성이 동시에 개발 사이클을 마치는 경우는 드뭅니다. 위성 지상 설비 서비스의 비용이 높아 시장 확대를 제한하고 있습니다.

위성 지상 설비 시장 동향

방위 및 관공청이 시장에서 큰 점유율을 차지할 전망

방위 부문 시장 점유율이 크게 확대될 것으로 예상. 위성 기반 이미징의 일부 애플리케이션으로는 네비게이션, 매핑 및 GIS, 긴급 상황 및 안전, 지오마케팅 및 광고, 엔터프라이즈 용도, 스포츠, 증강현실 및 게임, M-헬스, 개인 추적, 소셜 네트워킹이 포함됩니다. 이 모든 애플리케이션은 다양한 요구와 사용 조건을 충족하도록 맞춤 제작되었습니다. 컨텍스트 인식 애플리케이션 및 증강현실 애플리케이션 상승은 위치 정보 서비스 장치의 출하량이 증가함에 따라 예측 기간 동안 시장을 더욱 확대할 것으로 예상됩니다.

2023년 9월, 아랍에미리트(UAE)의 Yahsat은 아랍에미리트(UAE) 정부에 위성 서비스를 제공하는 187억 AED(51억 달러)의 중요한 계약을 획득했습니다. 17년간 ATP(Authorisation to Proceed) 계약에 따라 야사트는 2026년 이후 Al Yah 1 위성과 Al Yah 2 위성에 의한 안전하고 신뢰할 수 있는 위성 통신 용량을 정부에 기재하고 있습니다. 발표에 따르면, 이것은 2027년과 2028년에 각각 발사될 예정인 2개의 새로운 위성인 Al Yah 4와 Al Yah 5에 의해 보완됩니다. 2024년 Yahsat은 만데이트 계약에 따라 아랍에미리트(UAE) 정부로부터 10억 달러의 선불을 받았습니다. ATP 만데이트는 2026년 11월과 12월에 체결될 예정인 기존 계약, 용량 서비스 계약 및 관리형 서비스 만데이트(MSM)를 대체합니다.

2023년 11월 항공우주 및 방위 솔루션 제공업체인 Tata Advanced Systems Ltd.는 Satellogic Inc.와 제휴하여 인도 내에서 우주 기술 능력을 확립하고 개발할 것이라고 발표했습니다. 서브미터 해상도의 지구관측(EO) 데이터 수집에 참여하는 기업인 Satellogic Inc.와의 제휴는 회사의 위성 전략의 첫 단계입니다.

GOVSATCOM은 EU우주계획(2021-2027년)의 일환으로 위성통신 부문에서 우주의 능력을 이용하여 회원국 또는 EU 시민의 안보와 관련된 정책의 실시를 가능하게 하고 촉진한다 것입니다. 지상 인프라가 없는 지역(바다, 하늘, 지방, 북극권 등) 또는 현재 지상 인프라가 불안정, 손상, 파괴된 경우 GOVSATCOM에 대한 액세스는 필수적입니다(자연 재해, 위기, 분쟁 등에 따라). 또한 광대역 인디아 포럼에 따르면 고정 위성 서비스-FSS/방송 위성 서비스-BSS의 통신 및 방송 네트워크용 인터페이스 요건(필수 기술 요건)의 신규격에 따라 지상 부문의 초소구경 단말(VSAT) 참가 기업은 최신 SATCOM 기술을 활용할 수 있습니다.

IoT(사물인터넷)와 자율시스템 수요 증가, 군 및 방위 위성 통신 솔루션 수요 증가로 조사 대상 시장은 향후 성장할 것으로 예상됩니다. 그러나 이 기간 동안 위성 통신에 대한 사이버 보안 위험과 위성 데이터 전송 간섭이 시장 성장을 방해할 것으로 예상됩니다. 게다가 위성 미션의 미래 기술 진보와 위성을 통한 5G 네트워크의 배치는 업계에 수익성 높은 전망을 가져올 가능성이 높습니다. NATO에 따르면 2023년 국내총생산에서 차지하는 폴란드의 국방비는 3.9%로 NATO 회원국 중 가장 높고 미국의 3.49%가 이에 이릅니다.

예측기간 중 북미가 주요 점유율을 차지

북미 정부 기관은 첨단 통신 기술을 채택하는 선두적인 존재입니다. 관민 일체가 된 노력으로 북미, 특히 미국은 새로운 위성과 네비게이션 시스템을 도입하는 리더적 존재이며, 북미의 위성 지상 설비 산업의 성장을 뒷받침했습니다.

북미에는 지속적인 모니터링이 필요한 광대 한 해안 지역이 있습니다. 이 지역에서의 상업 활동과 무역 증가는 해상 안전과 모니터링의 필요성을 뒷받침하고 있습니다. 게다가, 탐지와 식별을 위한 적절한 시스템이 없는 경우, 불법 행위는 국가의 해상 국경을 넘어 모든 방향에서 일어날 수 있기 때문에 근본적인 위협은 해상 안전 집행에 독특하고 중대한 과제를 야기합니다. 따라서, 상기 요인은 예측 기간 동안 이 지역에서 조사된 시장에 영향을 미칠 것으로 예상됩니다.

또한 미국은 세계 최대의 군사 지출국입니다. 예를 들어, 2022년 상원 군사위원회는 대통령 제안보다 약 250억 달러 높은 방위 예산을 승인했습니다. SIPRI에 따르면 2022년 미국 국방비 총액은 2018년 6,824억 9,000만 달러에 비해 8,769억 4,000만 달러에 달할 전망입니다. 이러한 동향은 미국에서 연구 시장의 성장에 유리합니다.

통신 위성의 이점을 활용하는 데 중점을 둔 여러 정부가 주도하는 이니셔티브도 북미에서의 조사 시장 성장에 유리한 전망을 창출하고 있습니다. 예를 들어, 2022년 1월 캐나다의 혁신 및 과학기술부 장관은 지구관측 우려와 지속가능한 개발 우선순위를 다루는 새로운 솔루션을 탐구하기 위해 캐나다 전역 21개 단체에 800만 달러를 기부한다고 발표 했습니다. 이 자금은 캐나다 우주청(CSA)의 smartEarth 프로그램에서 제공됩니다. 이 프로그램은 위성 데이터를 활용하여 어려움을 해결하고 현실 세계의 문제 해결에 기여하는 캐나다 기업을 뒷받침하는 것을 목표로 합니다.

게다가 수요가 증가함에 따라 벤더에게 북미에서의 서비스 확충을 촉구하고 있으며, 이것도 조사 대상 시장의 성장에 기여하고 있습니다. 예를 들어, 2023년 4월 Rogers Communications는 Lynk Global과 제휴하여 캐나다 전역에서 위성에서 전화로의 연결 솔루션을 테스트하고 제공합니다.

위성 지상 설비 산업 개요

위성 지상 설비 시장은 Thales Group, Inmarsat Global Limited, Iridium Communications Inc., Gilat Satellite Networks Ltd., Orbcomm Inc.와 같은 대기업의 존재와 신규 진출기업 증가로 반고체화되고 있습니다. 이 시장의 벤더는 혁신, 파트너십, 합병, 인수 등의 전략을 채택하고, 제품 라인업을 강화하고, 지속 가능한 경쟁 우위를 획득하고 있습니다.

2023년 5월 저궤도 위성 회사 OneWeb은 세인트 헬레나 섬에 지상국을 설치하여 이 섬의 간선인 에쿠아이아노 해저 케이블의 능력을 획득할 예정입니다. OneWeb은 지역 전화 회사 Sure와 10년간 지상국 계약을 맺었습니다. OneWeb은 호스 포인트에 지상국을 건설하고 Sure는 시설을 관리합니다. 지상국은 루파츠 비치에 있는 섬의 케이블 독 스테이션에 광섬유로 연결됩니다.

2023년 3월 인도를 기반으로 하는 풀스택 우주공학 솔루션 기업인 Dhruva Space와 프랑스를 기반으로 하는 위성통신 사업자이자 세계의 커넥티비티 프로바이더인 Kineis는 협정각서(MoA)에 서명 그리고 두 조직이 협력하여 우주와 지상 인프라를 시작하여 위성 기반 솔루션의 다양성과 영향력을 확대하는 것을 밝혔습니다. 궤도에 9개의 위성을 가진 키네이스의 운영 서비스는 전 세계를 다룹니다.

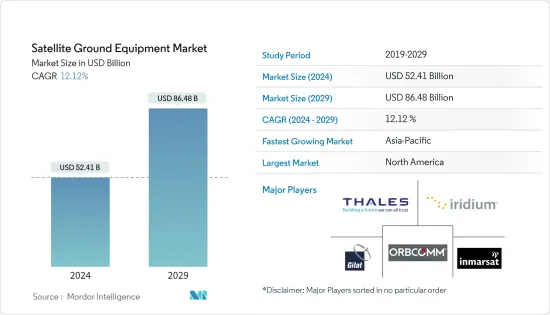

The Satellite Ground Equipment Market size is estimated at USD 52.41 billion in 2024, and is expected to reach USD 86.48 billion by 2029, growing at a CAGR of 12.12% during the forecast period (2024-2029).

Key Highlights

The satellite ground equipment industry has grown dramatically due to advancements in radio communication solutions, such as NOC equipment, the increasing demand for mobile radio communications, and the significant deployment of public safety applications. Furthermore, the profitable introduction of low earth orbit (LEO) satellite systems, high throughput satellites (HTS), and Ku- and Ka-band satellites are adding to the lucrative growth opportunities in the market. Simultaneously, the humongous demand for autonomous and connected vehicles used for various applications in the sectors, including commercial government and defense, require sophisticated customized SATCOM-on-the-move antennas for highly trusted operation, driving the Satellite Ground Equipment Market.

The Satellite Industry Association (SIA) reported that the ground equipment revenues have significantly increased, with the extension in the GNSS markets and network equipment, flat or somewhat declining customer equipment investments and resources, manifesting that mobile satellite services will become a fundamental growth point of the overall market studied. Passengers using a smartphone or laptop in the air can benefit from in-flight connectivity to access the internet or video streaming services. Ship personnel may benefit from crew connectivity with the latest maritime information, such as chart updates, engine monitoring, and weather routing broadcast. The backpack terminals must be quickly and reliably deployed to support connectivity in harsh and emergent conditions.

A High Throughput Satellite (HTS) is a satellite that provides high throughput compared with a fixed satellite system for the same amount of allocated frequency on orbit. HTS reuses the frequency and multiple spot beams to improve throughput and reduce the cost per bit delivered. HTS is primarily deployed to provide broadband Internet access service to unserved regions. Most HTS satellites are designed mainly for the enterprise, telecom, or maritime sectors. Space and satellite system providers are launching HTS satellites for high-speed communication services. The increasing HTS launches increase the adoption of ground station equipment , thereby driving the market.

Satellite broadcasting is the distribution of multimedia content or broadcast signals over or through a satellite network. The broadcast signals usually originate from a station such as a TV or radio station. Then they are sent via a satellite uplink (uploaded) to a geostationary artificial satellite for redistribution or retransmission to other predetermined geographic locations through an open or secure channel. Direct broadcasting or satellite television has become an effective form of distribution for television content. The broad and controllable coverage areas and much larger bandwidths enable more channels to be broadcast, making satellite television very attractive.

Furthermore, there is a diversity of satellite dish heaters and satellite antenna de-icing systems on the market in the present scenario, providing enough opportunities for everything from 18" residential satellite television and satellite Internet dish antennas to larger commercial and enterprise VSAT uses. Collecting snow and/or ice on a satellite television or satellite Internet dish can cause signal loss. The satellite de-icing system is one way to stop snow and ice from accumulating on satellite dishes.

On the contrary, the multi-band terminals used by the Navy, which come with Advanced-EHF satellites, are quite expensive. Furthermore, the cost of purchasing and installing the terminals can be anywhere from 20 to 30 times that of the rockets and spacecraft. The fact that satellite and terminal development initiatives are carried out separately has long been a source of waste and cost overruns. For example, the Air Force may oversee spacecraft while the Army may oversee radios. Rarely do earth-bound communication equipment and satellites reach the conclusion of their development cycles at the same time. The high cost of satellite ground equipment services is limiting the market's expansion.

Satellite Ground Equipment Market Trends

Defense and Government is Expected to Hold Significant Share of the Market

The defense segment's market share is expected to expand significantly. The growing investment in satellite technology for weapons, regional security, surveillance, and espionage intelligence is anticipated to benefit the market.Several applications of satellite-based imaging include navigation, mapping and GIS, emergency and safety, geo marketing and advertising, enterprise applications, sports, augmented reality/games, mHealth, personal tracking, and social networking. All these applications are being tailormade to satisfy different needs and usage conditions. The rise of context-aware applications and augmented reality apps, coupled with the increasing shipments of devices with location-based services, is expected to further augment the market during the forecast period.

In September 2023, United Arab Emirates (UAE) company Yahsat has been awarded a significant AED18.7 billion (USD5.1 billion) deal to provide satellite services to the UAE government. Under the 17-year Authorisation to Proceed (ATP) agreement, Yahsat will supply the government with secure and reliable satellite capacity afforded by the Al Yah 1 and Al Yah 2 satellites from 2026 onwards. The announcement said this will be supplemented by two new planned satellites - Al Yah 4 and Al Yah 5 - expected to launch in 2027 and 2028, respectively. In 2024, Yahsat will receive an advance payment of USD1 billion from the UAE government under the mandate agreement. The ATP mandate will replace existing agreements, the Capacity Services Agreement and the Managed Services Mandate (MSM), expected to conclude in November and December 2026.

In November 2023, Aerospace and defense solutions provider Tata Advanced Systems Ltd announced it has partnered with Satellogic Inc. to establish and develop local space technology capabilities in India. The partnership with Satellogic, a player in sub-metre resolution Earth Observation (EO) data collection, is a first step in the company's satellite strategy.

GOVSATCOM is part of the EU Space Programme (2021-2027), which uses space's capabilities in the field of satellite communications to enable and facilitate the implementation of Member States' or EU policies connected to citizen security. In regions with no ground infrastructure (e.g., sea, air, rural areas, the Arctic region), or if the current ground infrastructure is unstable, damaged, or destroyed, access to GOVSATCOM is essential (e.g., due to natural disasters, crises, conflicts). Further, According to the Broadband India Forum, the new standard for Interface Requirements for Communication & Broadcast Networks for fixed-satellite service-FSS/broadcasting-satellite service-BSS (mandatory technical requirements) will allow the ground segment very-small-aperture terminal (VSAT) players to take advantage of the latest SATCOM technologies (BIF).

The market studied is expected to grow in the future due to an increase in demand for the Internet of Things (IoT) and autonomous systems and a rise in demand for military and defense satellite communication solutions. During the period, however, cybersecurity risks to satellite communication and interference in satellite data transmission are expected to stifle the market growth. Furthermore, future technological advances in satellite missions and the deployment of a 5G network via satellites will likely provide profitable prospects for the industry. Accorindg to Nato, In 2023, Poland's defense spending as a share of gross domestic product was 3.9 percent, the highest of all NATO member states, followed by the United States at 3.49 percent.

North America to Hold Major Share During the Forecast Period

Government agencies in North America have been among the leaders in adopting advanced communication technologies. Owing to the combined efforts of public and private entities, the North American region, especially the United States, has been among the leaders in introducing new satellite and navigation systems that boosted the growth of the satellite ground equipment industry in North America.

North America has a large coastal area that requires continuous monitoring. The increasing commercial activities and trade in the region are also propelling the need for maritime safety and surveillance. Furthermore, the underlying threat poses unique and critical challenges in enforcing maritime safety, as illegal activities can happen from all directions across the country's maritime borders if there is no proper system for detection and identification. Hence, the factors mentioned above are anticipated to influence the market studied in the region during the forecast period.

Furthermore, the United States is the world's largest military spender. For instance, in FY 2022, the Senate Armed Services Committee approved a defense budget of about USD 25 billion higher than the President's proposal. According to SIPRI, in 2022, the total defense expenditure of the United States reached USD 876.94 billion, compared to USD 682.49 billion in 2018. Such trends favor the studied market's growth in the United States.

Several government-led initiatives focused on leveraging the benefits of communication satellites also creates a favorable outlook for the growth of the studied market in North America. For Instance, in January 2022, the Minister of Innovation, Science and Technology of Canada announced a USD 8 million commitment in 21 organizations across Canada to explore new solutions that address Earth observation concerns and sustainable development priorities. The money will come from the Canadian Space Agency's (CSA) smartEarth program, which aims to push Canadian businesses to solve difficulties utilizing satellite data and help solve real-world concerns.

Furthermore, the growing demand is encouraging the vendors to expand their offerings in the North American region which is also contributing to the growth of the studied market. For instance, in April 2023, Rogers Communications partnered with Lynk Global to test and deliver satellite-to-phone connectivity solutions across Canada.

Satellite Ground Equipment Industry Overview

The satellite ground equipment market is semi-consolidated owing to the presence of major players like Thales Group, Inmarsat Global Limited, Iridium Communications Inc., Gilat Satellite Networks Ltd, and Orbcomm Inc., as well as the growing entry of new players. Vendors in the market are adopting strategies such as innovations, partnerships, mergers, and acquisitions to enhance their product offerings and gain a sustainable competitive advantage.

In May 2023, Low Earth Orbit satellite firm OneWeb is set to establish a ground station on the island of St. Helena and take ability on the island's trunk of the Equiano subsea cable. OneWeb has inscribed a 10-year ground station agreement with regional telco Sure. OneWeb is set to construct a ground station at Horse Point, with Sure set to manage the facility. The ground station will then be connected via fiber to the island's cable dock station at Rupert's Beach.

In March 2023, India-based full-stack space-engineering solutions company Dhruva Space and France-based satellite operator and global connectivity provider Kineis have inked a Memorandum of Agreement (MoA), marking a collaboration where both organizations will collaborate to launch space and ground infrastructure to scale the variety and impact of satellite-based solutions. With nine satellites in orbit, Kineis' operational services provide global worldwide coverage.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Buyers

4.2.2 Bargaining Power of Suppliers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Assessment of the Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increase in Internet of Things (IoT) and Autonomous Systems

5.1.2 Increasing Demand for Satellite Based Services

5.2 Market Restraints

5.2.1 Interference in Transmission of Data

6 MARKET SEGMENTATION

6.1 By Type

6.1.1 Ground Equipment

6.1.2 Service

6.2 By End-user Vertical

6.2.1 Maritime

6.2.2 Defense and Government

6.2.3 Enterprises

6.2.4 Media and Entertainment

6.2.5 Other End-user Verticals

6.3 By Geography

6.3.1 North America

6.3.2 Europe

6.3.3 Asia-Pacific

6.3.4 Latin America

6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Thales Group

7.1.2 Inmarsat Global Limited

7.1.3 Iridium Communications Inc.

7.1.4 Gilat Satellite Networks Ltd

7.1.5 Orbcomm Inc.

7.1.6 Cobham SATCOM (Combham Limited)

7.1.7 Thuraya Telecommunications Company

7.1.8 ViaSat Inc.

7.1.9 ST Engineering iDirect

7.1.10 L3Harris Technologies Inc.

7.1.11 Advantech Wireless Technologies Inc. (Baylin Technologies)