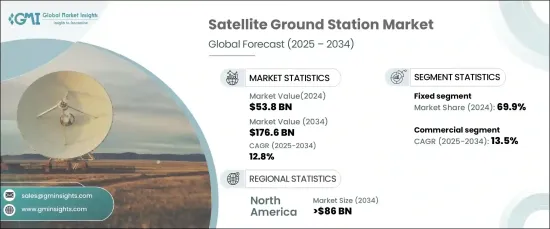

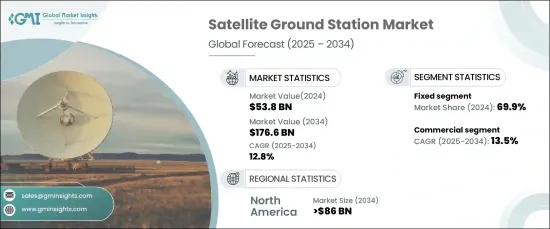

세계의 위성 지상국 시장은 2024년 538억 달러에 달했으며, 2025년부터 2034년까지 연평균 성장률(CAGR) 12.8%로 성장할 전망입니다.

이러한 성장은 특히 방송 및 통신 부문에서 위성 기반 서비스에 대한 수요가 급증한 데 힘입은 바가 큽니다. 디지털 미디어가 지속적으로 확장됨에 따라 DTH(Direct-to-Home) 서비스, 고화질 방송, OTT(Over-the-top) 플랫폼의 증가로 인해 원활한 통신과 효율적인 데이터 전송을 보장하는 강력한 지상국 인프라에 대한 필요성이 크게 대두되고 있습니다. 또한 원격 통신, 기상 모니터링, 글로벌 포지셔닝과 같은 목적으로 위성 시스템에 대한 의존도가 높아지면서 최첨단 위성 지상국에 대한 수요가 더욱 증가하고 있습니다.

기술 발전은 시장 확대의 또 다른 주요 촉진요인입니다. 고처리량 위성(HTS)의 도입으로 위성 시스템의 용량이 획기적으로 향상되어 더 빠르고 안정적인 데이터 전송이 가능해졌습니다. 이와 함께 안테나 기술 및 자동화의 혁신으로 지상국의 성능과 운영 효율성이 향상되었습니다. 소프트웨어 정의 네트워크(SDN)와 인공 지능(AI)의 통합은 예측 유지보수, 실시간 모니터링, 시스템 적응성 향상과 같은 기능을 도입하여 지상국의 운영 방식을 혁신적으로 변화시켰습니다. 이러한 기술 발전으로 위성 지상국은 진화하는 통신 수요에 더욱 신속하게 대응하여 서비스 품질을 유지하면서 대규모 데이터 트래픽을 처리할 수 있는 능력을 향상시켰습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 538억 달러 |

| 예측 금액 | 1,766억 달러 |

| CAGR | 12.8% |

시장 세분화를 플랫폼 유형별로 살펴보면 2024년에는 고정 지상국이 69.9%로 가장 큰 시장 점유율을 차지했습니다. 이러한 지상국은 통신, 방송, 지구 관측 등 다양한 용도에서 지속적이고 안정적인 위성 통신을 유지하는 데 매우 중요합니다. 고정 위성 지상국은 안전한 고대역폭 데이터 전송을 제공하므로 지속적인 운영이 필수적인 정부, 군사 및 상업용에 없어서는 안 될 필수 요소입니다.

기능적 측면에서 보면 통신 부문은 예측 기간 동안 13.5%의 연평균 성장률이 예상되는 가장 빠르게 성장하는 부문으로 두드러집니다. 통신 중심의 지상국은 위성 TV, 인터넷 연결, 군 통신 시스템과 같은 필수 서비스를 지원합니다. 이러한 지상국은 위성과 지상 네트워크 간의 고대역폭 데이터 연결을 보장하며, 이는 기존 인프라가 제한적이거나 사용할 수 없는 외딴 지역에서 특히 중요합니다.

지역별 성장세를 살펴보면, 2034년까지 860억 달러에 달할 것으로 예상되는 북미 지역이 위성 지상국 시장을 지배할 것으로 전망됩니다. 특히 미국은 우주 인프라 구축, 지속적인 기술 발전, 통신, 방송 및 지구 관측 분야의 위성 서비스에 대한 강력한 수요를 바탕으로 주요 플레이어로 부상하고 있습니다. 이 지역의 수요는 첨단 자동화 시스템의 개발과 특히 저지구궤도(LEO)에서 새로운 위성 별자리의 등장으로 더욱 증폭되어 위성 지상국 운영의 혁신과 효율성을 더욱 촉진하고 있습니다.

The Global Satellite Ground Station Market is poised for remarkable growth, reaching USD 53.8 billion in 2024, with projections indicating a strong CAGR of 12.8% from 2025 to 2034. This growth is largely driven by the surge in demand for satellite-based services, especially in the broadcasting and communication sectors. As digital media continues to expand, the rise of direct-to-home (DTH) services, high-definition broadcasting, and over-the-top (OTT) platforms has created a significant need for robust ground station infrastructure to ensure seamless communication and efficient data transmission. Additionally, the market is benefiting from the growing reliance on satellite systems for purposes such as remote communication, weather monitoring, and global positioning, further fueling the demand for cutting-edge satellite ground stations.

Technological advancements are another key driver for market expansion. The introduction of high-throughput satellites (HTS) has dramatically improved the capacity of satellite systems, enabling faster and more reliable data transfers. Alongside this, innovations in antenna technologies and automation have boosted the performance and operational efficiency of ground stations. The integration of software-defined networks (SDN) and artificial intelligence (AI) has revolutionized how these stations operate, introducing capabilities like predictive maintenance, real-time monitoring, and enhanced system adaptability. These technological strides have made satellite ground stations more responsive to evolving communication demands, increasing their ability to handle massive data traffic while maintaining service quality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $53.8 billion |

| Forecast Value | $176.6 billion |

| CAGR | 12.8% |

Market segmentation by platform type reveals that fixed ground stations held the largest market share in 2024, accounting for 69.9%. These stations are critical for maintaining constant and reliable satellite communications across various applications, including telecommunications, broadcasting, and Earth observation. Fixed satellite ground stations offer secure, high-bandwidth data transmission, making them indispensable for government, military, and commercial use, where continuous operations are a necessity.

On the functional side, the communication segment stands out as the fastest-growing, with a projected CAGR of 13.5% during the forecast period. Communication-focused ground stations support essential services such as satellite TV, internet connectivity, and military communication systems. These stations ensure high-bandwidth data connections between satellites and terrestrial networks, which is especially vital in remote areas where traditional infrastructure is limited or unavailable.

Looking at regional growth, North America is set to dominate the satellite ground station market, with expectations to reach USD 86 billion by 2034. The United States, in particular, is a key player, benefiting from its established space infrastructure, continuous technological advancements, and strong demand for satellite services in communication, broadcasting, and Earth observation. The demand in this region is further amplified by the development of advanced automated systems and the rise of new satellite constellations, particularly in Low Earth Orbit (LEO), driving further innovation and efficiency in satellite ground station operations.