ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

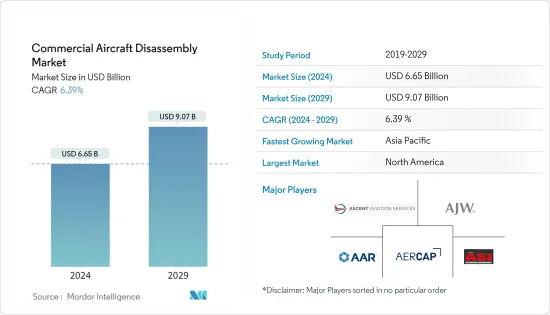

민간 항공기 해체 시장 규모는 2024년 66억 5,000만 달러로 추정 및 예측되며, 2029년에는 90억 7,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 6.39%의 CAGR로 성장할 것으로 예상됩니다.

주요 하이라이트

Oliver Wyman의 MRO 전망에 따르면, 항공사가 연비가 좋은 기종으로 교체함에 따라 민간항공기의 평균 기령은 향후 10년간 급격히 감소할 것으로 보입니다. 이에 따라 연간 평균 퇴역률은 지난 10년까지 비해 20-25% 증가할 것으로 예상됩니다.

항공 업계가 지속가능성 이니셔티브를 활용하기 위해 노력하는 가운데, 사용 후 항공기의 항공기 부품 재활용이 점점 더 널리 보급되고 있습니다. 엔진 MRO 서비스 제공업체와 리스업체들은 롤스로이스 Trent 700, 에어버스 A330 파워플랜트 등 구형 엔진에 대한 수요가 증가하고 있는 것을 목격하고 있습니다.

그러나 재활용 공정에서 고가의 합금을 사용하기 때문에 전체 공정 비용이 상승하여 시장 성장의 걸림돌로 작용하고 있습니다.

민간 항공기 해체 시장 동향

예측 기간 동안 좁은 몸체 부문이 시장 점유율을 독식

협동체 부문이 가장 큰 시장 점유율을 차지할 것으로 예상되는 주요 이유는 항공사들이 단거리 및 중거리 노선에서 협동체 항공기를 널리 사용하고 있기 때문입니다. 협동체 항공기는 단거리 노선에서 낮은 운항 비용과 높은 연료 효율성과 같은 다양한 장점과 함께 전 세계 여러 저가 항공사들이 가장 선호하는 항공기 유형으로 자리 잡았습니다.

또한 저가 항공사의 성공적인 비즈니스 모델은 그 장점으로 인해 최근 몇 년 동안 새로운 세대의 좁은 몸체 항공기에 대한 대규모 수요를 창출했습니다. 차세대 협동체 항공기의 기술 발전으로 장거리 비행이 가능해졌습니다. 보잉의 B737과 에어버스의 A320은 가장 많이 판매된 협동체 항공기 중 하나입니다.

예를 들어, 에어인디아는 2022년 12월 에어버스와 분할하는 역사적인 장비 확장의 일환으로 보잉 B737 MAX 190대를 포함한 200대 이상의 보잉 항공기를 주문하는 계약이 거의 완료되었다고 발표했습니다. 보잉 B737 MAX가 2020년 하반기부터 운항을 재개하는 것도 협동체 항공기 부문의 성장에 힘을 실어줄 것으로 보입니다.

아시아태평양이 예측 기간 동안 가장 높은 성장률을 기록할 것

아시아태평양의 견조한 경제 성장, 양호한 인구 및 개발도상국의 인구 통계가 이 지역의 항공 여객 수송을 주도하고 있습니다. 이 지역의 항공 여객 수송량은 지난 10년간 크게 증가했는데, 그 주요 이유는 이 지역의 관광지와 항공 여행에 대한 접근성 때문이며, 이는 예측 기간 동안 지속될 것으로 예상됩니다.

세계 최대 항공 시장인 중국과 인도 외에도 인도네시아, 베트남, 태국, 필리핀 등의 국가에서는 저렴한 휴양지를 찾는 관광객들의 항공 여객 수송량이 그 어느 때보다 증가하고 있습니다.

이 지역 항공사들이 항공기를 현대화함에 따라 항공기 해체, 재활용 및 서비스에 대한 수요가 증가할 것으로 예상됩니다. 예를 들어, 2022년 9월 중국항공은 보잉 B787 드림라이너를 최대 24대까지 주문하기로 결정했다고 발표했습니다.

에어버스의 전망에 따르면 중국에서는 지속적인 항공기 현대화로 인해 2023년부터 2042년까지 2320대의 항공기가 퇴역할 것으로 예상됩니다. 따라서 이러한 현대화 노력은 오래된 항공기를 재사용, 수리 및 재활용할 수 있는 시장 기회를 확대하여 순환 경제에 기여할 것입니다.

민간 항공기 해체 산업 개요

민간 항공기 해체 시장은 소수의 기업이 주요 시장 점유율을 차지하며 통합되어 있습니다. 민간 항공기 해체 및 재활용 시장에서 사업을 운영하는 주요 기업으로는 Ascent Aviation Services, A J Walter Aviation Ltd, AAR, AerCap Holdings N.V., Air Salvage International Ltd. 등이 있습니다.

이 시장에서 사업을 영위하는 주요 기업들은 인수합병, R&D 투자, 제휴, 지역 사업 확장, 신제품 출시 등 다양한 전략을 채택하고 있습니다. 항공기 제조업체, 항공사, 재활용 기업, 규제 기관 간의 협력적 파트너십은 민간 항공기 해체 및 재활용 시장 확대의 원동력으로 부상하고 있습니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인

시장 성장 억제요인

Porter's Five Forces 분석

신규 참여업체의 위협

구매자·소비자의 협상력

공급 기업의 교섭력

대체품의 위협

경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

용도별

해체·분해

재활용과 보관

사용된 서비스 가능 재료

회전 가능 부품

항공기 유형별

협동체기

광동체기

리저널 제트기

지역별

북미

미국

캐나다

유럽

독일

영국

프랑스

기타 유럽

아시아태평양

인도

중국

일본

한국

기타 아시아태평양

라틴아메리카

브라질

기타 라틴아메리카

중동 및 아프리카

아랍에미리트

사우디아라비아

이스라엘

기타 중동 및 아프리카

제6장 경쟁 상황

벤더 시장 점유율

기업 개요

Ascent Aviation Services

A J Walter Aviation Limited

AAR

AerCap Holdings N.V.

AerSale, Inc.

Air Salvage International Ltd

Aircraft End-of-Life Solutions AELS

Magellan Aerospace

CAVU Aerospace Inc.

China Aircraft Leasing Group Holdings Ltd

제7장 시장 기회와 향후 동향

ksm

영문 목차

영문목차

The Commercial Aircraft Disassembly Market size is estimated at USD 6.65 billion in 2024, and is expected to reach USD 9.07 billion by 2029, growing at a CAGR of 6.39% during the forecast period (2024-2029).

Key Highlights

According to Oliver Wyman's MRO outlook, the average age of commercial aircraft will decline dramatically over the next decade as airlines renew their fleets with more fuel-efficient models. This will drive average annual retirements to increase by 20-25% compared to the previous decade.

With the aviation industry aiming at utilizing sustainable efforts, the recycling of aircraft parts from end-of-life aircraft is becoming increasingly popular. Engine MRO service providers and leasing companies are witnessing an increasing demand for some types of older engines in their portfolios, such as the Rolls-Royce Trent 700 and the Airbus A330 Powerplant, owing to lower fuel prices that have encouraged airlines to fly their aircraft for longer durations.

However, the use of expensive alloys in the recycling process increases the overall cost of the process, which is a challenge to the market growth.

Commercial Aircraft Disassembly Market Trends

Narrow Body Segment to Dominate Market Share During the Forecast Period

Narrow body segment is expected to hold the largest market share primarily due to the airlines' widespread use of narrow-body aircraft for both short and medium-haul routes. Advanced capabilities coupled with various other advantages such as low cost of operation and fuel efficiency in short-haul routes have led to narrow-body aircraft being the most preferred type of aircraft to be used by various low-cost carrier companies worldwide.

Moreover, the success of the low-cost carrier business model has generated a massive demand for newer-generation narrow-body aircraft in recent years due to their advantages. Technological advancements in newer-generation narrow-body aircraft are making it possible to fly longer distances. Boeing's B737 and Airbus A320 are two of the most-sold aircraft narrow body aircraft.

For instance, in December 2022, Air India announced that they are close to completing a deal to order more than 200 Boeing aircraft, which includes 190 narrowbody Boeing B737 MAX aircraft, as a part of a historic fleet expansion that will be split with Airbus. The return of the Boeing B737 MAX into service in late 2020 will also help the growth of the narrow-body segment.

Asia-Pacific to Witness Highest Growth During the Forecast Period

The robust economic growth, favorable population, and demographic profiles of the populace in developing countries in the Asia-Pacific region are driving the air passenger traffic in the region. The region has seen a significant increase in air passenger traffic during the past decade, mostly due to the tourist destinations in the region and the ease of access to air travel, which is expected to continue during the forecast period.

In addition to China and India, which are two of the largest aviation markets in the world, countries like Indonesia, Vietnam, Thailand, and the Philippines are experiencing an unprecedented increase in air passenger traffic from tourists exploring cheaper holiday locations.

As airlines in this region modernize their fleets, demand for aircraft disassembly and recycling services is expected to rise. For instance, in September 2022, China Airlines announced that they had finalized an order for up to 24 Boeing B787 Dreamliners, as the carrier looks forward to continuing to upgrade its fleet with more modern and fuel-efficient airplanes.

According to the Airbus Outlook, 2320 aircraft will retire between 2023 and 2042 in China as a result of continuous fleet modernization. Thus, such modernizing efforts will create growing market opportunities to reuse, repair, and recycle older aircraft and contribute to a circular economy.

Commercial Aircraft Disassembly Industry Overview

The commercial aircraft disassembly market is consolidated with a handful of players owing the major market share. The major players operating in the commercial aircraft disassembly, dismantling & recycling market are Ascent Aviation Services, A J Walter Aviation Ltd., AAR, AerCap Holdings N.V., and Air Salvage International Ltd.

These major players operating in this market have adopted various strategies comprising mergers and acquisitions, investment in R&D, collaborations, partnerships, regional business expansion, and new product launches. Collaborative partnerships between aircraft manufacturers, airlines, recycling companies, and regulatory bodies have emerged as a driving force behind the expansion of the commercial aircraft disassembly, dismantling, and recycling market.