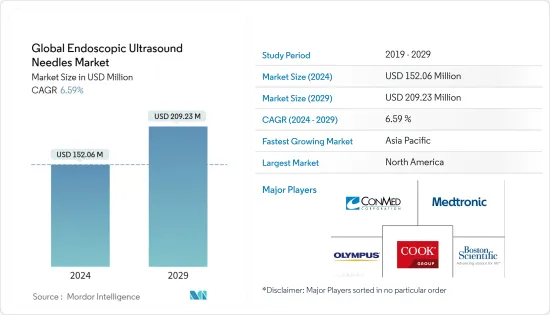

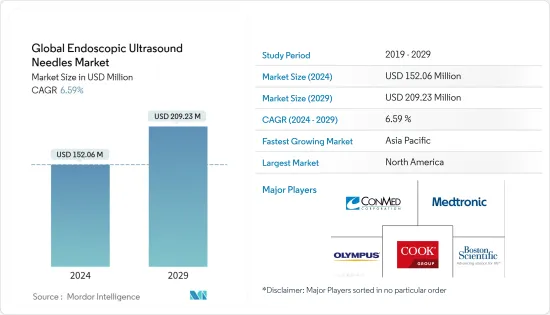

세계 초음파 내시경 천자침 시장 규모는 2024년에 1억 5,206만 달러로 추정되며, 2029년에는 2억 923만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 6.59%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19 감염병의 대유행은 시장에 큰 영향을 미쳤고, 대유행 초기에 시장은 막대한 손실에 직면했습니다. 장기간의 봉쇄와 바이러스 확산 억제를 위한 규제가 시장 성장을 저해했습니다. 예를 들어, 2021년 1월 Journal of Clinical Pathology에 게재된 기사에 따르면, 북아일랜드의 COVID-19 감염병 유행은 소규모 생검 시술 제공에 큰 영향을 미쳤다고 합니다. 그러나 현재 전염병이 진정되고 있기 때문에 정상적인 생검 절차는 정상적으로 수행되고 있습니다. 따라서 조사 대상 시장은 예측 기간 동안 안정적인 성장세를 보일 것으로 예상됩니다.

초음파 내시경 천자침은 치료 목적과 진단 목적 모두에 사용됩니다. 초음파 내시경 천자침 시장의 주요 성장 동력은 노인 인구의 증가와 소화기암 발병률의 증가입니다. 췌장암, 간암, 간 담도암, 폐암, 위장암과 같은 만성 질환의 발병률이 증가함에 따라 환자들은 최소 침습적 수술을 선호하고 있습니다. 초음파 내시경 천자침과 관련된 기술 발전의 증가는 향후 몇 년 동안 초음파 내시경 천자침 시장의 성장을 촉진할 수 있습니다.

PubMed가 2021년 6월에 발표한 논문에 따르면, 18개월 동안 800명의 환자를 무작위로 배정하고 771명을 분석하여 내시경 초음파 유도하 세침 생검(EUS-FNB)의 진단 정확도에 대한 신속한 현장 평가(ROSE)의 이점을 확인했습니다. 385건의 신속한 현장 평가(ROSE) 분석에서 96.4%의 정확도를 보였습니다. ROSE가 없는 나머지 386명은 97.4%, 절대 위험도 차이는 1.0%였습니다. 이 연구는 내시경 초음파 유도하 미세침 생검(EUS-FNB)이 충만성 췌장 병변(SPL)에서 높은 정확도를 보였다고 결론지었습니다. 고형 췌장 병변에는 주로 선암, 신경내분비 종양, 고형 성분을 포함한 낭성 췌장 신생물, 고형 가성유두상 종양, 췌장아세포종, 췌장림프종, 췌장 전이 등이 포함됩니다. 따라서 암 분야의 새로운 연구 개발로 이어지는 진행 중인 조사 및 연구는 주요 시장 참여자들에게 조사 대상 시장의 성장을 촉진할 수 있는 전략적 조치를 취하도록 촉구하고 있습니다.

암 유병률의 증가는 시장 성장을 촉진하는 주요 요인입니다. 예를 들어, ICMR 국립질병정보연구센터가 2021년 발표한 데이터에 따르면 인도의 0-14세 남녀 소아암의 거의 절반이 백혈병이었습니다. 2021년 유병률은 남자아이 46.4%, 여자아이 44.3%였습니다. 남자아이에게 흔한 또 다른 소아암은 림프종(16.4%), 여자아이에게 흔한 소아암은 악성골종양(8.9%)으로 나타났습니다.

또한, 이 지역 시장 기업들의 제품 출시가 증가하면서 시장 성장을 촉진할 것으로 예상됩니다. 예를 들어, Micro-Tech Endoscopy는 2021년 10월에 자사의 초음파 내시경 천자침인 Areus FNA Needle과 Trident FNB Needle의 향상된 버전을 출시했습니다.

따라서 암 유병률 증가, 암 진단 및 치료에 대한 연구 연구 증가, 주요 시장 기업의 제품 출시 증가와 같은 앞서 언급 한 요인으로 인해 연구 대상 시장은 연구 예측 기간 동안 성장할 것으로 예상됩니다. 그러나 초음파 내시경 천자침 조작에 대한 전문 지식을 갖춘 전문가가 부족하여 시장 성장을 억제하고 있습니다.

생검침(EUS-FNB) 부문은 점막하 병변, 림프종, 자가면역성 췌장염 등 다양한 비췌장 병변에 대한 초음파 내시경 제품의 사용량이 증가함에 따라 향후 몇 년 동안 시장을 장악할 가능성이 있습니다.

모든 암에 대한 연구와 조사 중에서도 췌장암에 대한 조사는 췌장암 발병률의 증가로 인해 적응적으로 이루어지고 있습니다. 2022년 1월 미국암협회의 데이터 검토에 따르면 췌장암의 약 25%는 흡연으로 인해, 20%는 과체중으로 인해, 전체 췌장암 사례의 10%는 유전적 유전 증후군으로 인해 발생하는 것으로 추정됩니다. 당뇨병 환자는 췌장암에 걸리기 쉽습니다. 2021년 미국임상종양학회(ASCO)의 또 다른 데이터에 따르면 미국 성인 60,430명(남성 31,950명, 여성 28,480명)이 췌장암 진단을 받은 것으로 추정됩니다. 췌장암 환자 수가 증가함에 따라 생검 바늘에 대한 수요가 증가하고 있습니다.

2021년 11월 PubMed에 발표된 논문에 따르면, 최근 초음파 내시경(EUS) 유도 미세침 생검(FNB)의 발전으로 조직 구조 보존에 기반한 진단 정확도를 향상시킬 수 있게 되었다고 합니다.

또한, 주요 시장 기업들의 제품 출시도 이 부문의 성장을 촉진하고 있습니다. 예를 들어, NeoDynamics AB는 NeoNavia FlexiPulse 프로브에 사용되는 생검 바늘 디자인에 대한 미국 특허를 취득했다고 발표했습니다. 프론트 로딩 오픈 팁 샘플링 바늘은 환자의 외상을 최소화하면서 조직 수율을 최대화할 수 있도록 설계됐습니다.

따라서 점막하 병변, 림프종, 자가면역성 췌장염과 같은 다양한 비췌장 병변에 대한 내시경 초음파 검사에 대한 제품 사용 증가 및 주요 시장 기업의 제품 출시와 같은 요인으로 인해이 부문은 예측 기간 동안 성장할 것으로 예상됩니다. 연구의.

북미 초음파 내시경 천자침 시장은 전 세계적으로 북미가 지배적입니다. 이는 캐나다와 미국에서 호흡기, 종양학, 소화기학 분야에서 첨단 진단 기법의 사용이 증가하고 있으며, 이 지역에 주요 시장 기업이 존재하기 때문입니다.

2022년 미국암협회가 발표한 자료에 따르면, 2022년에는 미국에서 약 343,040명의 소화기암 환자가 새로 발생할 것으로 추정됩니다. 또한 생식기암의 신규 환자 수는 395,600명에 달할 것으로 추정됩니다. 이러한 높은 발병률로 인해 이러한 질병을 진단하고 치료하는 절차에 대한 수요가 발생합니다. 따라서 이는 초음파 내시경 천자침 시장의 성장에 도움이 되었습니다. 또한, 캐나다, 미국 등 북미 국가에서는 호흡기, 종양학, 소화기학 분야에서 첨단 진단 방법의 사용이 증가하고 있습니다.

또한 2022년 11월 캐나다 암협회 자료에 따르면 2022년에는 233,900명이 암 진단을 받을 것으로 예상되며, 이러한 발병률 증가는 주로 캐나다의 인구 증가와 고령화에 따른 것으로 암 예방의 중요성을 강조하고 있습니다.

초음파 내시경 천자침 시장에서 대부분의 세계 기업의 존재는 또한 많은 제품에 대한 접근성으로 인해 이 지역의 조사 대상 시장의 성장에 기여하고 있습니다. 예를 들어, 미국 식품의약국(FDA)이 제공한 데이터에 따르면, 2021년 5월 Cook Ireland Ltd는 미국 FDA로부터 EchoTip 초음파 내시경 천자침, EchoTip ProCore HD 초음파 생검침에 대한 판매 승인을 받았다고 합니다.

암 유병률 증가, 제품 출시 증가 등 위의 요인들은 북미 초음파 내시경 천자침 시장의 성장에 영향을 미칠 것으로 예상됩니다.

초음파 내시경 천자침 시장은 본질적으로 적당히 통합되어 있습니다. 세계 주요 기업들은 내시경 초음파 바늘의 대부분을 생산하고 있습니다. 더 많은 연구 자금과 더 나은 유통 시스템을 갖춘 시장 리더는 확고한 입지를 구축하고 있습니다. 또한, 아시아태평양에서는 인식이 높아짐에 따라 여러 소규모 플레이어가 등장하여 시장 성장을 촉진하고 있습니다. 시장 주요 기업으로는 ACE Medical Devices Pvt. Ltd, Boston Scientific Corporation, CONMED Corporation, Cook Group Incorporated, ENDO-FLEX GmbH, Medi-Globe Corporation, Medtronic PLC, Micro- Tech Endoscopy 및 Olympus Medical Devices Pvt. Tech Endoscopy, Olympus Corporation 등이 있습니다.

The Global Endoscopic Ultrasound Needles Market size is estimated at USD 152.06 million in 2024, and is expected to reach USD 209.23 million by 2029, growing at a CAGR of 6.59% during the forecast period (2024-2029).

The COVID-19 pandemic impacted the market significantly, and the market faced considerable losses during the early pandemic. Long lockdown restrictions and restrictions to control the spread of the virus hampered the market's growth. For instance, according to an article published by the Journal of Clinical Pathology in January 2021, there has been a significant impact on the provision of small biopsy procedures due to the COVID-19 pandemic in Northern Ireland. However, as the pandemic has subsided currently, normal biopsy procedures are being carried out as usual; hence the studied market is expected to have stable growth during the forecast period of the study.

Endoscopic ultrasound needles are used for both therapeutic and diagnostic purposes. The major growth driver in the endoscopic ultrasound needles market is the increasing geriatric population and the growing prevalence of gastrointestinal cancers. There has been a rising prevalence of chronic diseases, like pancreatic, liver, hepatobiliary, lung, and gastrointestinal cancers, with patients increasingly preferring minimally invasive surgical procedures. Growing technological advancements related to endoscopic ultrasound needles are likely to fuel the expansion of the endoscopic ultrasound needles market in the coming years.

According to an article published by PubMed in June 2021, when 800 patients were randomized for 18 months, 771 were analyzed to check the benefit of rapid on-site evaluation (ROSE) on the diagnostic accuracy of endoscopic ultrasound-guided fine-needle biopsy (EUS-FNB). Among the 385 with rapid on-site evaluation (ROSE) analysis, a 96.4% accuracy result was obtained. The remaining 386 without ROSE was 97.4%, with an absolute risk difference of 1.0%. The study concluded that endoscopic ultrasound-guided fine-needle biopsy (EUS-FNB) demonstrated high accuracy in solid pancreatic lesions (SPLs). Solid Pancreatic Lesions primarily include adenocarcinoma, neuroendocrine tumors, cystic pancreatic neoplasms with solid components, solid pseudopapillary tumor, pancreatoblastoma, pancreatic lymphoma, and pancreatic metastasis. Hence, ongoing research and studies leading to new research and developments in the cancer segment inspire key market players to take strategic steps that can propel the growth of the studied market.

The rising prevalence of cancer is a major factor driving the growth of the market. For instance, according to the data published by ICMR-National Centre for Disease Informatics and Research in 2021, Leukemia accounted for nearly half of all childhood cancers in both genders in the 0-14 years age group in India; it had a prevalence of 46.4% in boys and 44.3% in girls in 2021. The other common childhood cancer in boys was found to be lymphoma (16.4%), while in girls, it was a malignant bone tumor (8.9%).

Furthermore, increasing product launches by market players in the region are also expected to enhance market growth. For instance, in October 2021, Micro-Tech Endoscopy launched an enhanced version of the company's endoscopic ultrasound needles named Areus FNA Needle and Trident FNB Needle.

Thus, due to the aforementioned factors, such as the rising prevalence of cancer, growing research studies for cancer diagnosis and treatment, and increasing product launches by key market players, the studied market is expected to experience growth during the forecast period of the study. However, the lack of professionals with expertise in operating with endoscopic ultrasound needles is restraining the market's growth.

The biopsy needles (EUS-FNB) segment is likely to dominate the market in the upcoming years due to increased product usage for the endoscopic ultrasound of different non-pancreatic lesions, such as submucosal lesions, lymphoma, autoimmune pancreatitis, etc.

Among all the cancer studies and research, pancreatic cancer research has been adaptive due to the increasing incidence of pancreatic cancer cases. As per the American Cancer Society's data review in January 2022, nearly 25% of pancreatic cancers are estimated to be caused by cigarette smoking, 20% due to overweight, and inherited genetic syndromes contributing to 10% of the total pancreatic cancer cases, where people with diabetes are more prone to have pancreatic cancer. Another data from the American Society of Clinical Oncology (ASCO) in 2021 estimated that 60,430 adults (31,950 men and 28,480 women) in the United States were diagnosed with pancreatic cancer. The growing number of cases of pancreatic cancers has been increasing the demand for biopsy needles.

As per the article published by PubMed in November 2021, the recent developments in Endoscopic Ultrasound (EUS)-Guided fine-needle biopsy (FNB) allow to associate with improved diagnostic accuracy based on preserving the tissue architecture, which is necessary to detect the typical histological features of Autoimmune Pancreatitis, which, if kept untreated, can become chronic and cause pancreatic cancer.

Furthermore, product launches by key market players are also enhancing segment growth. For instance, NeoDynamics AB announced that the Company had been granted a United States patent for its biopsy needle design employed in the NeoNavia FlexiPulse probe. The front-loaded, open-tip sampling needle has been designed to enable maximum tissue yield with minimal patient trauma.

Hence, due to factors such as increased product usage for the endoscopic ultrasound of different non-pancreatic lesions, such as submucosal lesions, lymphoma, autoimmune pancreatitis, and product launches by key market players, the segment is expected to experience growth during the forecast period of the study.

The North American endoscopic ultrasound needles market has dominated globally. This is due to the growing use of advanced diagnostic procedures in pulmonology, oncology, and gastroenterology in Canada and the United States and the presence of major market players in the region.

According to the data published by the American Cancer Society in 2022, it is estimated that there will be around 343,040 new cases of digestive system cancer in the United States in 2022; it is also estimated that there will be 395,600 new cases of genital system cancer. The presence of such a high incidence rate creates a demand for procedures to diagnose and treat such diseases. This has thus helped the endoscopic ultrasound needles market grow. Moreover, there is a growing use of advanced diagnostic procedures in pulmonology, oncology, and gastroenterology in North American countries of Canada and the United States.

Furthermore, according to the data from the Canadian Cancer Society in November 2022, it is estimated that 233,900 people will be diagnosed with cancer in 2022, and this growth in incidence is largely due to Canada's growing and aging population and emphasizes the importance of cancer prevention.

The presence of most of the global players in the endoscopic ultrasound needles market is also contributing to the growth of the studied market in this region with access to a number of products. For instance, in May 2021, Cook Ireland Ltd received marketing authorization from the United States FDA for its EchoTip Ultra Endoscopic Ultrasound Needle, EchoTip ProCore HD Ultrasound Biopsy Needle, according to data provided by the Department of Health and Human Sciences (US FDA).

These factors mentioned above, such as the rising prevalence of cancer, and increasing product launches, are expected to influence the growth of the endoscopic ultrasound needles market in North America.

The endoscopic ultrasound needles market is moderately consolidated in nature. The global key players are manufacturing the majority of endoscopic ultrasound needles. Market leaders with more funds for research and a better distribution system have an established position. Moreover, Asia-Pacific is witnessing the emergence of some small players due to a rise in awareness, helping the market grow. Some of the major players in the market include ACE Medical Devices Pvt. Ltd, Boston Scientific Corporation, CONMED Corporation, Cook Group Incorporated, ENDO-FLEX GmbH, Medi-Globe Corporation, Medtronic PLC, Micro-Tech Endoscopy, and Olympus Corporation, among others.