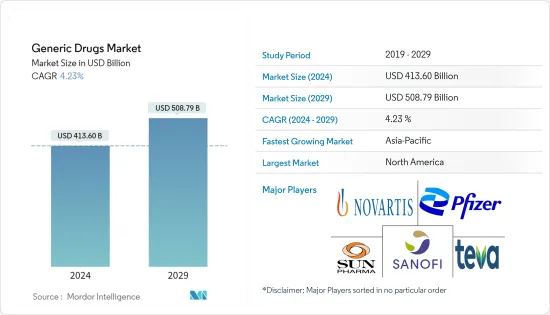

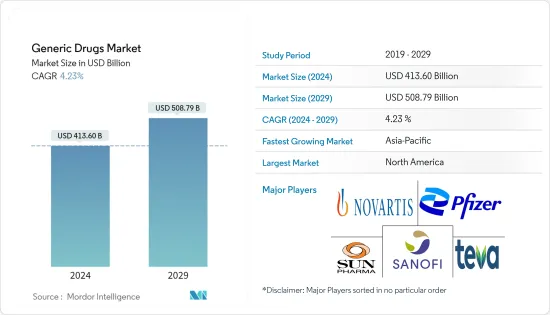

제네릭 의약품 시장 규모는 2024년 4,136억 달러에 이를 것으로 추정됩니다. 2029년까지 5,087억 9,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 4.23%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

신종 코로나바이러스 감염증인 코로나19는 봉쇄 조치와 공급망 혼란으로 인해 팬데믹 초기에 제네릭 의약품 시장에 심각한 영향을 미쳤습니다. 이후 코로나19 감염으로 인해 제네릭 의약품 제조업체가 이 감염병 치료제를 생산할 수 있는 기회가 많아지면서 제네릭 의약품에 대한 수요가 증가했습니다. 바이러스가 환자에게 미치는 영향에 대응하기 위해 인공호흡기 및 스테로이드 사용 환자를 위한 정맥주사제와 같은 제네릭 의약품이 사용되어 코로나19 감염으로 인한 사망자 수 감소에 기여했습니다. 예를 들어, 2021년 11월에 발표된 미국 식품의약국(USFDA) 보고서에 따르면 FDA는 제네릭 의약품 프로그램을 시행했습니다. 이 이니셔티브는 개발 프로세스 초기 및 신청서 검토 중에 규제 당국의 기대치를 명확히하기 위해 서면 연락을 보내고 회의를 개최하여 제네릭 의약품 개발자의 제품 개발을 지원했습니다. 2020년 FDA는 제품 개발 및 제출 전 사전 단축 NDA 회의에 대한 121건의 요청을 받았습니다. 따라서 이러한 노력은 팬데믹 이후 단계 시장 성장에 긍정적인 영향을 미쳤습니다. 따라서 분석에 따르면 조사 대상 시장은 제네릭 의약품에 대한 수요가 증가할 것으로 예상되므로 예측 기간 동안 동일한 추세를 따를 것으로 예상됩니다.

또한, 만성질환의 유병률 증가, 노인 인구의 급증, 의료비 증가 등이 시장 성장의 원인으로 꼽히고 있습니다. 국제암연구소(IARC)의 2020년 보고서에 따르면, 전 세계 185개국의 36개 암 발생률과 사망률을 추정한 결과, 2020년 전 세계적으로 약 1,930만 건의 새로운 암이 진단될 것으로 예상되며, 남성의 경우 1,010만 건 이상, 여성의 경우 930만 건 이상이 암으로 진단될 것으로 예상됩니다. 보고되고 있습니다. 또한, 세계 RA 네트워크의 2021년 보고서에 따르면 전 세계 3억 5,000만 명 이상의 사람들이 관절염을 앓고 있으며, 그 부담은 여러 요인으로 인해 증가할 것으로 예상되며, 그 중 하나는 전 세계 노인 인구의 부담 증가입니다. 따라서 만성 질환의 유병률 증가로 인해 효과적인 치료에 대한 수요가 급증하여 예측 기간 동안 제네릭 의약품 시장의 성장을 가속할 것으로 예상됩니다.

또한, 노인들은 만성 질환에 걸리기 쉽기 때문에 예방과 치료를 위한 효과적인 치료 옵션에 대한 수요가 증가하여 시장 성장을 가속할 것입니다. 2021년 세계보건기구(WHO) 자료에 따르면, 세계 인구 중 60세 이상 인구의 비율은 2015년에서 2050년 사이에 12%에서 22%로 거의 두 배로 증가할 것이며, 2050년에는 전 세계 노인의 80%가 저소득층과 중산층에 거주하게 될 것으로 예상됩니다. 인구 고령화가 이전보다 훨씬 빠르게 진행되고 있고, 만성질환을 앓고 있을 가능성이 높기 때문에 제네릭 의약품에 대한 수요가 증가하여 시장 확대가 가속화될 것으로 보입니다.

또한, 주요 시장 기업들이 채택한 다양한 유기적 및 무기적 전략이 시장 성장을 지원할 것으로 예상됩니다. 2022년 2월, 잼파마 그룹은 주의력결핍 과잉행동장애(ADHD)를 치료하는 캐나다 다케다제약의 레퍼런스 제품인 INTUNIV XR의 제네릭 버전인 Guanfasin XR을 출시했습니다. 또한 2021년 10월 중국 장강제약그룹은 간질 환자 치료에 사용되는 3등급 제네릭 의약품인 에리칼바제핀 아세테이트 아세테이트의 첫 번째 판매 신청서를 제출했습니다. 또한 2021년 7월에는 철결핍성 빈혈(IDA) 치료에 사용되는 주사제인 제네릭 페르목시톨(Ferumoxytol)이 제네릭 및 바이오시밀러 의약품의 세계 리더인 샌드(Sand)에 의해 미국에서 출시되었습니다.

따라서 앞서 언급한 요인에 따라 시장은 예측 기간 동안 크게 성장할 것으로 예상됩니다. 그러나 정부의 엄격한 규제는 예측 기간 동안 시장을 억제할 수 있습니다.

경구용 제네릭 의약품은 가장 간단하고 편리하며 가장 안전한 약물 투여 수단입니다. 반복적이고 장기간 사용하기에 편리하고, 자가 투여가 가능하며, 통증이 없습니다. 따라서 가장 많이 사용되고 생산되는 약물 형태입니다.

신제품 출시와 협업 증가는 이 부문의 성장을 가속할 것으로 예상됩니다. 출시로 인해 경구용 제네릭 제품의 판매 및 제조가 증가하여 이 부문의 성장을 가속할 것입니다.

또한 2021년 10월, 머크는 유엔이 지원하는 의약품 특허 풀(MPP)과 라이선스 계약을 체결하여 더 많은 기업이 자사의 실험용 경구용 항바이러스 코로나19 감염 치료제의 제네릭 버전을 생산할 수 있도록 했습니다. 이러한 협력은 향후 몇 년동안 이 분야의 성장을 가속할 수 있습니다.

따라서 위의 요인으로 인해 이 부문은 예측 기간 동안 성장이 확대될 것으로 예상됩니다.

아시아태평양은 의료 질환에 대한 인식이 높아지고 고령화 인구가 증가함에 따라 세계 제네릭 시장에서 가장 빠르게 성장할 것으로 예상됩니다. 인도와 중국과 같은 아시아태평양의 국가들은 다른 국가들보다 더 많은 기여를 하고 있습니다. 국제인구과학연구소(IIPS)가 2021년 1월 발표한 연구 결과에 따르면, 60세 이상 인도인 중 약 7,500만 명이 만성질환을 앓고 있는 것으로 나타났습니다. 약 4,500만 명이 심혈관 질환과 고혈압을 앓고 있으며, 약 2,000만 명이 당뇨병을 앓고 있습니다. 따라서 이 나라의 높은 만성질환 유병률은 비용 효율적인 치료제에 대한 수요를 증가시켜 이 시장을 견인할 것으로 보입니다.

IBEF가 2021년 11월 발표한 인도 제약산업 보고서에 따르면 인도는 세계 최대 제네릭 의약품 공급국입니다. 인도 제약 산업은 미국 제네릭 수요의 40%, 영국 전체 의약품의 25%를 공급하고 있습니다.

주요 시장 기업의 파트너십, 합병 및 인수와 같은 전략적 및 비전략적 노력은 시장 성장에 더욱 기여할 것으로 예상됩니다. 예를 들어, 2022년 1월Lupin은 인도 환자에게 고품질 제네릭 의약품 및 복합 제네릭 의약품을 제공하기 위해 Shenzhen Foncoo Pharmaceutical Co.

따라서 앞서 언급한 요인으로 인해 아시아태평양은 예측 기간 동안 더 빠른 속도로 성장할 것으로 예상됩니다.

세계 제네릭 의약품 시장은 경쟁이 치열하고 많은 업체들이 시장을 독점하고 있습니다. 시장 참여자들은 심화되는 시장 경쟁을 유지하기 위해 R&D 투자 증가, 합병, 인수, 제품 혁신 등의 전략을 채택하고 있습니다. 주요 시장 기업로는 Mylan NV, Eli Lilly and Company, GlaxoSmithKline PLC, Pfizer Inc, Sun Pharma, Novartis, Sanofi 등이 있습니다.

The Generic Drugs Market size is estimated at USD 413.60 billion in 2024, and is expected to reach USD 508.79 billion by 2029, growing at a CAGR of 4.23% during the forecast period (2024-2029).

COVID-19 severely impacted the generic drugs market during the early pandemic due to lockdown restrictions and supply chain disruption. Later, there was an increased demand for generic pharmaceuticals as the COVID-19 infections provided many opportunities for generic drug manufacturers to manufacture the drugs to treat this infection. As the COVID-19 public health emergency unfolded last year, the FDA shifted its focus to generic drug submissions involving potential treatments and supportive therapies for COVID-19 patients. To combat the virus's effects on patients, generic medicines such as intravenous drugs for patients on ventilators and steroids were used, which helped reduce COVID-19 fatalities. For instance, according to a report by the USFDA published in November 2021, the FDA has implemented a generic drug program. This initiative assisted generic medication developers with product development by sending written communications and holding meetings to clarify regulatory expectations early in the development process and during application review. The FDA received 121 requests for product development and pre-submission pre-abbreviated NDA meetings in 2020. Thus, such initiatives have positively impacted market growth in the post-pandemic phase. Thus, as per the analysis, the market studied is expected to follow the same trend over the forecast period as the demand for generic drugs is expected to increase.

Furthermore, the reasons attributed to the growth of the market are the increasing prevalence of chronic diseases, a surge in the geriatric population, and growing healthcare expenditure. As per the 2020 report of the International Agency for Research on Cancer (IARC), which estimated the incidence and mortality of 36 cancers in 185 countries globally, an estimated 19.3 million new cases of cancer were diagnosed in 2020 all over the world, and from the total number of diagnosed cancer cases, over 10.1 million cases were reported in males and 9.3 million cases were reported in females. Additionally, according to the 2021 report of the Global RA Network, more than 350 million people are living with arthritis around the world, and its burden is expected to increase owing to various factors, one of which is the rising burden of the geriatric population around the globe. Thus, the growing prevalence of chronic diseases is expected to surge the demand for effective treatment, thereby boosting the growth of the generic drug market over the forecast period.

Furthermore, the geriatric population is more susceptible to chronic diseases, which increases the demand for effective treatment options for prevention and treatment, thereby boosting the market's growth. According to the WHO data for 2021, the proportion of the global population aged 60 and above will nearly double from 12% to 22% between 2015 and 2050. By 2050, 80% of the world's elderly will live in low- and middle-income countries. The population is aging considerably more quickly than in the past, and this demographic is also more likely to suffer from chronic diseases, which will likely increase demand for generic drugs and accelerate market expansion.

Additionally, various organic and inorganic strategies adopted by the key market players are expected to support the growth of the market. In February 2022, Jamp Pharma Group launched Guanfacine XR, a generic version of the reference product INTUNIV XR from Takeda Canada Inc. that treats attention deficit hyperactivity disorder (ADHD). Moreover, in October 2021, The Yangtze River Pharmaceutical Group in China submitted the first marketing application for eslicarbazepine acetate, a class 3 generic medication used to treat epileptic patients. In addition, in July 2021, Generic Ferumoxytol, an injectable drug used to treat iron deficiency anemia (IDA), was launched in the United States by Sandoz, a global leader in generic and biosimilar medicines.

Hence, based on the aforementioned factors, the market is expected to grow significantly during the forecast period. However, stringent government regulation may restrain the market over the forecast period.

Oral generics are the simplest, most convenient, and safest means of drug administration. They are convenient for repeated and prolonged use and can be self-administered and pain-free; hence, they are the most used and manufactured form of drugs.

The growing launches and collaborations are expected to boost the segment's growth. In January 2022, the Medicines Patent Pool (MPP) announced that it had signed agreements with 27 generic manufacturing companies for the manufacturing of the oral COVID-19 antiviral medication molnupiravir and its supply in 105 low- and middle-income countries. In February 2022, Oakrum Pharma, LLC, in collaboration with ANI Pharmaceuticals, announced that the USFDA had approved the ANDA for a generic version of Cystadane1 (betaine anhydrous for oral solution) Powder in a 180-gram bottle and granted competitive generic therapy (CGT) 180 days of exclusivity. Such launches increase the sales and manufacture of oral generic products, boosting the segment's growth.

In addition, in October 2021, Merck & Co. signed a licensing agreement with the United Nations-backed Medicines Patent Pool (MPP) that will allow more companies to manufacture generic versions of its experimental oral antiviral COVID-19 treatment. Such collaborations are likely to boost the segment's growth over the coming years.

Thus, owing to the factors mentioned above, the segment is expected to expand its growth over the forecasted period.

Asia-Pacific is anticipated to witness the fastest-growing trend in the global generic market owing to increased awareness among people related to medical disorders and the growing aging population in the region. Countries like India and China in the Asia-Pacific region contribute more than the other nations. According to a study published by the International Institute for Population Sciences (IIPS), in January 2021, approximately 75 million Indians over the age of 60 had some form of chronic disease. About 45 million people have cardiovascular disease and hypertension, and about 20 million suffer from diabetes. Thus, the high prevalence of chronic diseases in the country will boost the demand for cost-effective therapeutics, thereby driving the studied market.

According to the Indian Pharmaceutical Industry Report published in November 2021 by IBEF, India is the world's top supplier of generic pharmaceuticals. The Indian pharmaceutical industry supplies 40% of the generic demand in the United States and 25% of all pharmaceuticals in the United Kingdom.

Strategic and non-strategic initiatives such as partnerships, mergers, and acquisitions by key market players are further expected to contribute to market growth. For instance, in January 2022, Lupin signed a partnership agreement with Shenzhen Foncoo Pharmaceutical Co. to bring high-quality generic and complex generic medicines to patients in India. Further, in October 2021, Dr. Reddy's Laboratories launched an anti-cancer drug in the Chinese market through its joint venture, Kunshan Rotam Reddy Pharmaceutical Co. Ltd. (KRRP). The drug is a therapeutic equivalent generic version of Zytiga, which is owned by Johnson & Johnson.

Therefore, owing to the aforementioned factors, the Asia-Pacific region is expected to show growth at a faster pace over the forecast period.

The global generic drugs market is highly competitive, with many players dominating the market. The market players are adopting strategies such as rising R&D investment, mergers, acquisitions, and product innovations to sustain the increasing market rivalry. The key market players include Mylan NV, Eli Lilly and Company, GlaxoSmithKline PLC, Pfizer Inc., Sun Pharma, Novartis, and Sanofi.