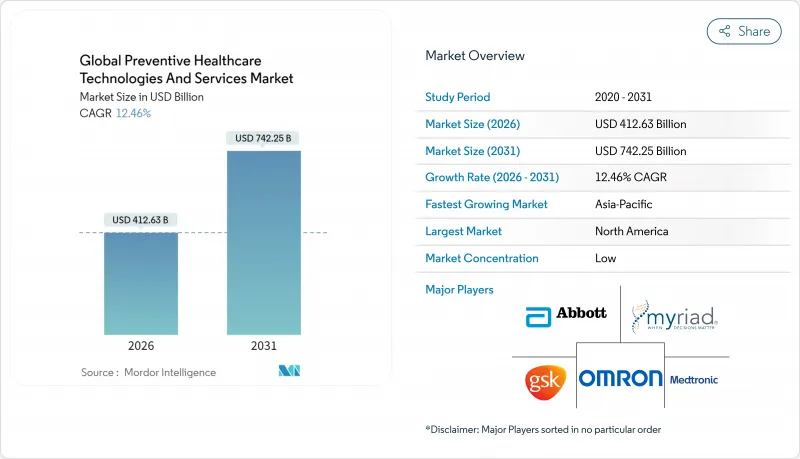

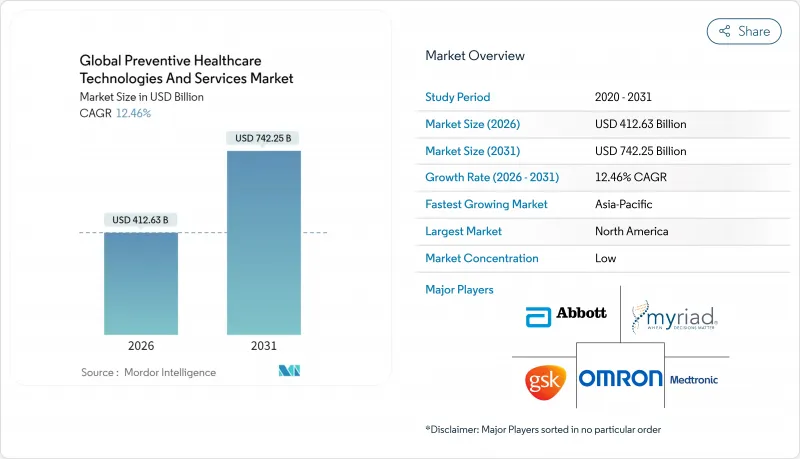

예방의료 기술 및 서비스 시장은 2025년 3,669억 1,000만 달러로 평가되었으며, 2026년 4,126억 3,000만 달러에서 2031년까지 7,422억 5,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 12.46%로 예상됩니다.

만성질환의 치료비 상승, 가치 기반 의료 계약에 대한 고용주의 지출 증가, AI 구동형 리스크 계층화의 주류화로 선별검사기기, 가상 코칭, 집단 진단의 잠재시장이 확대되고 있습니다. 북미는 성숙한 환급제도를 배경으로 2024년 42.23%의 점유율을 획득했습니다. 한편, 아시아태평양은 정부에 의한 디지털 헬스 인프라와 모바일 퍼스트 선별검사 프로그램의 확충에 의해 2030년까지 연평균 복합 성장률(CAGR) 14.19%로 확대될 것으로 전망되고 있습니다.

2024년에는 고용주의 의료 지출이 연률 7-9% 증가하였고 미국은 당뇨병 관련 비용으로만 3,270억 달러에 달했기 때문에 지불자와 제공업체는 간헐적인 치료에서 조기 발견 프로그램으로의 전환을 촉구하고 있습니다. AI를 활용한 계층화를 통해 증상 발현 수개월 전에 고위험군에 속하는 개인을 확인할 수 있기 때문에 종합적인 선별검사 복리후생을 도입한 기업 집단에서는 응급 부문 이용이 20-30% 감소하고 있습니다. 옵텀의 470만 명의 환자를 대상으로 한 가치 기반 의료 계약은 예방의 경제적 근거를 뒷받침합니다. 의료 시스템은 집단의 건강 유지에 의해 공유 절약분을 획득하는 구조입니다. 고령화와 생활 습관병으로 인한 이환율 증가는 예방의료 기술 및 서비스 시장의 모든 부문에서 선별검사 키트, 모바일 진단 및 가상 영양 상담에 대한 수요를 확대하고 있습니다. 다국적기업은 결근률 감소와 엄격한 노동 시장에서의 인재 확보를 위해 이러한 서비스를 복리후생 패키지에 통합하고 있습니다.

연속 혈당 모니터, 심전도 기능이 있는 스마트 워치, 패치형 혈압 센서는 보험자가 임상적 유용성을 인정함으로써 건강 증진 가젯에서 보험 적용 의료기기로 전환되었습니다. Apple이 2025년 2월에 확대한 'Apple Heart & Movement Study'는 이 회사의 워치 에코시스템을 대규모 연구 플랫폼으로 자리매김하고 있습니다. 반면 Google의 대화형 에이전트인 MedLM은 생체측정 데이터 스트리밍을 기반으로 실시간 안내를 제공합니다. 메디케어와 메디케이드를 통한 원격 환자 모니터링의 보험 적용 확대는 의사가 주도하는 웨어러블 처방전의 급증을 촉진하여 개인 장치를 임상 엔드포인트로 변모시켰습니다. 환자는 생체 데이터 피드를 공유하여 개별 위험 보고서를 제공받지만 GDPR(EU 개인정보보호규정) 강화로 인한 프라이버시 기대가 높아지면서 유럽인의 40%는 여전히 신중한 자세를 유지하고 있습니다. 웨어러블 스트림과 전자의무기록(EHR)의 통합은 종단적 데이터세트를 충실히 하여 진단 정확도를 높이고 AI 알고리즘 개발을 촉진합니다.

2024년 8월에 시행된 유럽의 AI법은 알고리즘의 투명성과 바이어스 모니터링을 의무화하여 예방의료 알고리즘을 전개하는 벤더의 컴플라이언스 부담을 증대시키고 있습니다. 세계적으로 알려진 정보 유출 사건이 잇따라 대중의 신뢰를 해치고 있습니다. 조사 대상 환자의 40%는 장점이 분명함에도 디지털 플랫폼에 대한 데이터 공유를 망설이고 있습니다. 웨어러블 장비 제조업체에서 전자의무기록 공급업체에 이르는 각 노드가 공격 대상이 될 수 있기 때문에 조직은 분석 개방성과 제로 트러스트 아키텍처 간의 균형을 맞추고 있습니다. 도입 지연과 사이버 보안 보험료의 상승은 중소 디지털 헬스케어 공급자의 이익률을 압박하고 있습니다.

이 제품은 정기적인 센서 판매 및 앱 구독을 지원하면서 2025년 2,382억 달러를 달성하여 예방의료 기술 및 서비스 시장에서 가장 높은 점유율을 유지했습니다. 그러나 급성기 치료보다 예방을 중시하는 정액 계약의 추진으로 서비스는 연간 13.56%의 성장이 예상되고 있습니다. 의료 리스크 평가, 생활 습관 지도, 만성질환 관리 패키지가 보급되고 있으며, 제공업체는 개선된 치료 성과를 수익화하는 공유 절약 모델에 적합합니다.

원격 예방상담은 시책상의 평등성과 하이브리드 노동력에 대한 고용주의 도입으로 가장 높은 성장률을 기록하고 있습니다. 당뇨병, 고혈압, 비만과 같은 질병 특화형 관리 프로그램은 지속적인 데이터 피드와 알고리즘을 통한 조정 프로토콜을 통해 입원 건수를 줄이고 안정적인 수익 기반을 확립하고 있습니다. 종합적인 건강 증진 프로그램 도입 후 건강 보험 부담액이 두 자릿수 감소했다고 보고하는 대기업에는 생활 습관 지도 솔루션이 제공되고 있습니다.

북미는 2025년 41.76%의 점유율로 매출을 견인했습니다. 원격 모니터링에 대한 메디케어 환급, 고용주의 건강 촉진 인센티브, 활발한 벤처 자금 조달 파이프라인이 뒷받침하고 있습니다. 웨어러블 기기와 전자의무기록(EHR)의 통합, 확립된 HIPAA 프레임워크가 데이터 상호 운용성을 촉진하여 AI 지원형 예방 플랫폼의 도입 사이클을 단축하고 있습니다. 시장의 억제요인으로는 신흥 유전체 검사의 환급 격차와 의료 제공업체의 간접비를 높이는 사이버 보안 보험료의 상승을 들 수 있습니다.

아시아태평양은 13.98%의 연평균 복합 성장률(CAGR)로 가장 높은 성장률을 기록했습니다. 스마트폰의 보급, 대규모 질병에 대한 부담 압력, 정부의 전자 의료 지원 계획이 성장을 추진하고 있습니다. 중국의 '건강 중국 2030'과 인도의 '아유슈만 바라트 디지털 미션'은 클라우드 기반 등록 시스템과 AI 트리아지 봇에 대한 투자를 가속화하여 예방의료 기술 및 서비스 시장의 도입을 촉진하고 있습니다. 모바일 퍼스트 이용자는 기존의 의료 채널을 뛰어넘어 채팅 기반 리스크 평가와 전자 약국 물류를 활용하여 지방의 접근성 격차를 메우고 있습니다.

유럽에서는 전국민 보험 모델과, 검진 및 예방 접종 목표를 국가 예산에 통합하는 시책 의무화의 강점에 의해 꾸준한 성장이 전망됩니다. 유럽의 건강 데이터 공간(EHDS)은 크로스보더 데이터 상호 운용성을 표준화하고 예측 분석 벤더의 규모의 경제를 실현합니다. EU AI 법의 준수는 초기 개발 비용을 증가시키지만 장기적인 규제 확실성을 제공하고 예방의료 솔루션에 대한 투자자의 신뢰를 높입니다. 남미, 중동, 아프리카는 현재는 점유율이 낮지만 매력적인 미개발 시장이며 브라질 UBS 디지털 등의 파일럿 사업은 인프라 제약 가운데에서도 원격 예방의료가 성공할 수 있음을 증명하고 있습니다.

The preventive health technologies and services market was valued at USD 366.91 billion in 2025 and estimated to grow from USD 412.63 billion in 2026 to reach USD 742.25 billion by 2031, at a CAGR of 12.46% during the forecast period (2026-2031).

Escalating chronic-disease treatment costs, rising employer spending on value-based care contracts, and the mainstreaming of AI-driven risk stratification widen the addressable base for screening devices, virtual coaching, and population-level diagnostics. North America captured 42.23% revenue share in 2024 on the back of mature reimbursement frameworks, whereas Asia-Pacific is set to expand at a 14.19% CAGR through 2030 as governments scale digital-health infrastructure and mobile-first screening programs.

Employer medical outlays climbed 7-9% per year in 2024, while diabetes costs alone reached USD 327 billion in the United States, prompting payers and providers to pivot from episodic care to early-detection programs. AI-enabled stratification flags high-risk individuals months before symptom onset, lowering emergency-department use by 20-30% in corporate cohorts with comprehensive screening benefits. Value-based care contracts covering 4.7 million Optum patients underscore the economic case for prevention, as health systems earn shared savings for keeping populations healthier. Aging demographics and lifestyle-driven morbidity amplify demand for screening kits, mobile diagnostics, and virtual nutrition counseling across every segment of the preventive health technologies and services market. Multinational employers are embedding these offerings into benefits packages to mitigate absenteeism and retain talent in tight labor markets.

Continuous glucose monitors, smartwatches with ECG, and patch-based blood-pressure sensors have shifted from wellness gadgets to reimbursable medical devices as payers recognize their clinical utility. Apple's February 2025 expansion of the Apple Heart & Movement Study positions its watch ecosystem as a large-scale research platform, while Google's MedLM conversational agent provides real-time coaching based on streaming biometric data. Coverage expansions by Medicare and Medicaid for remote patient monitoring drove a surge in physician-initiated wearables prescriptions, turning personal devices into clinical endpoints. Patients share biometric feeds in exchange for personalized risk reports, though 40% of Europeans remain cautious amid GDPR-heightened privacy expectations. Integration of wearable streams with EHRs enriches longitudinal datasets, enhancing diagnostic precision and fueling AI algorithm development.

Europe's AI Act, in effect since August 2024, mandates algorithmic transparency and bias monitoring, increasing compliance overhead for vendors rolling out preventive health algorithms. High-profile breaches continue to dampen public trust; 40% of surveyed patients hesitate to share data with digital platforms even when benefits are clear. Each node-from wearable OEMs to EHR vendors-presents an attack surface, compelling organizations to balance openness for analytics with zero-trust architectures. Implementation delays and higher insurance premiums for cybersecurity coverage erode margins for smaller digital-health providers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Products retained the largest slice of the preventive health technologies and services market size at USD 238.2 billion in 2025, buoyed by recurring sensor sales and app subscriptions. However, services are forecast to climb 13.56% annually, propelled by capitated contracts that reward prevention over acute interventions. Health-risk assessments, lifestyle coaching, and chronic-disease management bundles have proliferated as providers align to shared-savings models that monetize improved outcomes.

Tele-preventive consultations top the growth charts, aided by policy parity and employer adoption for hybrid workforces. Disease-specific management programs-diabetes, hypertension, obesity-anchor sticky revenue via continuous data feeds and algorithmic titration protocols that reduce hospitalization events. Lifestyle-coaching solutions appeal to large enterprises that document double-digit reductions in health-plan liabilities after rolling out comprehensive wellness schemes.

The Preventive Health Technologies and Services Market Report is Segmented by Product and Services (Products, Services), Delivery Mode (In-Person, Remote/Virtual), End User (Healthcare Providers, Employers, Payers & Insurers, Individuals, Government/Public Health Agencies), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America led spending with a 41.76% stake in 2025, fueled by Medicare reimbursement for remote monitoring, employer wellness incentives, and robust venture-funding pipelines. Integration of wearables with EHRs and established HIPAA frameworks eases data interoperability, shortening deployment cycles for AI-supported preventive platforms. Market headwinds include reimbursement gaps for emerging genomic assays and rising cybersecurity-insurance premiums that inflate provider overhead.

Asia-Pacific registers the highest growth at a 13.98% CAGR, buoyed by smartphone ubiquity, large-scale disease-burden pressures, and supportive government e-health blueprints. China's Healthy China 2030 and India's Ayushman Bharat Digital Mission accelerate investments in cloud-based registries and AI triage bots, catalyzing preventive health technologies and services market adoption. Mobile first-time users leapfrog legacy care pathways, employing chat-based risk assessments and e-pharmacy logistics to bridge rural access gaps.

Europe grows steadily on the strength of universal-coverage models and policy mandates that embed screening and vaccination targets into national budgets. The European Health Data Space standardizes cross-border data interoperability, enabling scale economics for predictive-analytics vendors. EU AI Act compliance raises upfront development costs but offers long-term regulatory certainty, improving investor confidence in preventive-health solutions. South America, the Middle East, and Africa contribute modest shares today yet represent attractive white space, with pilots such as Brazil's UBS+Digital proving tele-prevention can thrive even amid infrastructure constraints.