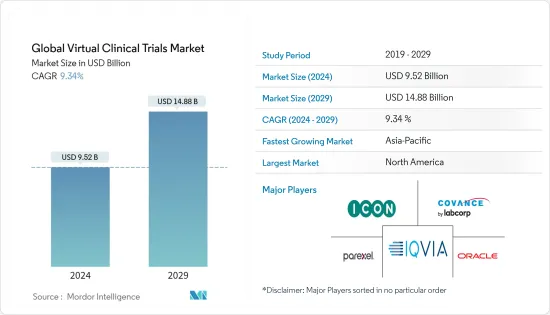

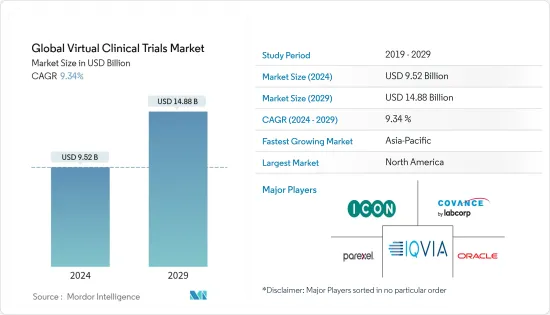

세계의 가상 임상시험 시장 규모는 2024년 95억 2,000만 달러로 추정되고, 2029년까지 148억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 9.34%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

COVID-19의 팬데믹은 세계 대부분의 인구 이동 및 운송 시스템을 차단하고, 많은 임상시험 환자가 임상시험실에 참석할 수 없게 하며, 수석 연구자(PI) 및 기타 임상 직원의 자택 대기를 제한했습니다. 그 때문에 재판의 연기나 중지가 잇따르고 있습니다. 브리스톨 마이어스 스퀴브, 화이자, 머크, 엘리 릴리는 향후 몇 주동안의 신규 침험의 시작이나 기존 연구에 대한 모집 정지를 발표하는 기업 목록에서 증가하고 있습니다. 2020년 4월에 발표된 Continuum Clinical Analysis 보고서에 의하면, 조사 대상이 된 임상시험 실시지의 약 30%는 새로운 임상시험에 환자의 등록과, 현재 등록하고 있는 환자의 시험 스케줄을 순조롭게 진행하는 것 모두에 큰 영향을 미친 것으로 평가됩니다. 의회 예산국이 발표한 보고서에 따르면 2020년 4월 약 30개 제약 회사 또는 생명 공학 회사가 시험 중단을 보고했습니다. 여기서 임상시험의 중단을 경감하기 위해 제약회사나 바이오테크놀러지 기업이 개발한 원격의료 및 디지털 기술을 활용한 가상 임상시험이 활약합니다.

가상 임상시험 시장은 의료 분야에서의 디지털화의 진전, 연구개발 활동의 성장 및 원격 의료 도입에 의해 견인되고 있습니다. 예를 들어 존슨 엔드 존슨은 2020년 2월 애플 시계와 새로운 아이폰 앱이 부정맥을 감지하여 뇌졸중 위험을 줄일 수 있는지 확인하는 하트라인 가상 테스트 설계 연구를 시작했습니다. 가상 임상시험은 채용률이 높고, 컴플라이언스가 향상되고, 탈락률이 낮고, 기존의 임상시험보다 신속하게 실시됩니다.

또한 웹 기반 임상시험 시작, 임상조사, 생명공학기업, 제약회사 간의 협업, 정부의 지원 이니셔티브 등 기술의 진보가 시장을 밀어올릴 것으로 예상됩니다. 예를 들어, 2020년 11월, 팔렉셀은 임상시험센터(CTC)와 협력했습니다. 이 협력은 초기 단계의 임상시험을 실시하는 조사 능력을 향상시킬 수 있습니다. 또한 팬데믹 하에 초기 임상연구에 대한 수요가 증가하고 지속될 수 있을 가능성이 높습니다. 마찬가지로 2020년 10월 Oracle은 FHI Clinical과 협력하여 임상시험의 효율성을 향상시키고 치료제의 보다 빠른 시장 출시를 지원했습니다.

또한, 심장병, 감염, 신경질환 등의 만성질환으로 고통받는 사람들의 발생 증가와 노인 인구 증가도 가상 임상시험 시장 성장을 가속하는 요인이 되고 있습니다. 예를 들어 질병관리 예방센터(2021)에 따르면 미국에서는 평균 10명 중 6명이 만성질환으로 고통받고 있으며 10명 중 4명이 2개 이상의 만성질환으로 고통을 받고 이 나라의 주요 사망 원인이 됩니다. WHO에 따르면, 2020년에는 세계에서 만성질환이 사망자의 거의 4분의 3을 차지하였고, 사망자의 71%가 허혈성 심질환(IHD)에 의한 것, 사망자의 75%가 뇌졸중에 의한 것, 사망자의 70%가 뇌졸중 때문이었습니다. 신흥 국가에서는 당뇨병이 원인으로 발생할 수 있습니다. 질병 부담이 증가함에 따라 신약 개발에 대한 수요가 높아질 것으로 예상됩니다. 이로 인해 의료 산업의 기술 개발이 촉진되고 시장 성장이 촉진될 것으로 예상됩니다.

그러나 수집 데이터의 양이 증가함에 따라 규제 당국에 대한 신뢰성, 기술 장애, 데이터의 정확성이 입증되고 관리되며, 이는 세계의 가상 임상시험 시장의 성장을 방해할 것으로 예상되는 과제의 일부 입니다.

종양부문은 정부가 암 계발에 대한 대처 강화, 암 이환율 상승, 항암제 개발 연구개발 활동 증가로 종양학시험 수가 증가하여 예측기간에 걸쳐 시장을 독점할 것으로 예상됩니다. Globocan 2020의 팩트 시트에 따르면 추정 19,292,789명의 암 증례가 진단되었으며, 9,958,130명이 암으로 사망하고 있습니다.

세계 암의 부담은 세계적으로 증가하고 있습니다. 가상 임상시험은 암 환자의 위험(면역억제의 위험, 이동 부담, 치료의 다양성, 규제의 복잡성)을 최소화하고 대면시험 방문에 소요되는 시간을 단축합니다. 환자의 안전을 지키기 위해 종양학의 임상시험 연구자와 스폰서는 즉시 가상 임상시험과 원격 임상시험을 도입했습니다. 2019년 10월, 조지타운 대학 의료 센터는 암 환자의 프로파일에 액세스하는 시간을 공제하기 위해 클라우드 기반 가상 상호 연결 컴퓨팅 기술을 사용했습니다. 이는 2014년부터 2017년까지 3건에서 14건으로 가상으로 평가된 사례 수가 전통적인 평가에 비해 46건에서 622건으로 증가한 것을 보여줍니다.

National Clinical Trials에 따르면, 2020년 4월에 개발의 다양한 단계에 걸쳐 종양학에 대한 약 8,306건의 임상시험이 실시되었습니다. 임상시험의 수가 증가함에 따라 가상 임상시험 수요가 증가할 가능성이 높아집니다. 따라서 위의 요인이 예측 기간 동안 이 부문을 추진할 것으로 예상됩니다.

지리적으로 북미는 의약품을 생산하는 선도 기업의 존재 외에도 신약 개발에 투자하는 데 주력하는 정부와 기업의 상승으로 세계의 가상 임상시험 시장에서 가장 큰 수익원 중 하나를 차지합니다. 2019년 11월 존슨 엔드 존슨의 제약 자회사인 얀센은 PRA 건강 과학과 협력하여 완전히 분산된 적응형 모바일 임상시험인 디지털 임상시험 셋업 CHIEF-HF를 시작했습니다. 이 회사는 웨어러블 디바이스와 스마트 기술을 활용하여 2형 당뇨병 유무를 동반한 심부전 환자에서 카나글리플로진의 효능을 평가하기 위한 증거를 효율적으로 수집하고 분석하는 것을 목표로 하고 있습니다.

게다가 이 지역은 예측 기간 동안 계속해서 우위를 유지할 것으로 예상됩니다. 이는 이 지역에서의 연구개발 증가와 임상조사 및 정부의 지원에 있어서 신기술의 채용에 기인하는 것으로 예상됩니다. 또한 시장 관계자는 디지털 기술을 이용하여 고객의 요구에 부응하고 있습니다. 예를 들어, 2020년 팔렉셀은 하이브리드 및 가상, 분산 방식을 포함한 100개 이상의 분산 평가판을 실행했습니다. 그러나 암 증례 및 기타 만성 질환 증가로 인해 가상 임상시험 시장은 예측 기간을 통해 크게 증가할 수 있습니다.

가상 임상시험 시장은 경쟁이 치열하며 여러 대형 기업으로 구성되어 있습니다. 시장에서 활동하는 기업은 제약 분야에서의 경험, 임상시험에서의 경험 및 기술에 대한 투자 등 다양한 경쟁 요인에 따라 활동하고 있습니다. 시장 진출기업이 채택하는 전략은 파트너십, 협업, 합의, 제품 출시 및 제품 확대입니다.

The Global Virtual Clinical Trials Market size is estimated at USD 9.52 billion in 2024, and is expected to reach USD 14.88 billion by 2029, growing at a CAGR of 9.34% during the forecast period (2024-2029).

The COVID-19 pandemic has shut down population movements and transport systems across large parts of the world, preventing many clinical trial patients from attending trial sites and restricting principal investigators (PIs) and other clinical staff to their homes. Hence, the flurry of trial delays and cancellations. Bristol Myers Squibb Co., Pfizer Inc., Merck & Co., and Eli-Lilly & Co. are among the growing list of companies to have announced a stop to new trial starts and pauses to recruitment into existing studies for the next several weeks. According to Continuum Clinical analysis reports published in April 2020, around 30% of the surveyed clinical trial locations are expected to have a significant impact on both enrolling patients for new trial studies and keeping patients who are currently enrolled on track with their study schedules. According to a report published by Congressional Budget Office, in April 2020, approximately 30 pharmaceutical or biotech companies had reported a trial disruption. This is where the virtual trial comes into play with telemedicine and digital technologies developed by pharmaceutical and biotech companies to reduce the clinical trials disruption.

The virtual clinical trials market is driven by the growing digitization in the healthcare sector, growth in R&D activities, and the adoption of telehealth. For example, in February 2020, Johnson & Johnson launched the Heartline virtual trial design study to see if the Apple Watch and new iPhone app may reduce the risk of stroke by detecting cardiac arrhythmia. Virtual clinical trials have higher recruitment rates, better compliance, lower drop-out rates, and are conducted faster than traditional clinical trials.

Moreover, advancements in technology, such as the launch of web-based clinical trials, collaborations between clinical research companies, biotechnology companies and pharmaceutical, and support initiatives from governments are expected to boost the market. For example, in November 2020, Parexel collaborated with the Clinical Trial Center (CTC). This collaboration may increase the research capacity of delivering early phase clinical trials. It is likely to also support the rising demand and continuation of early phase clinical studying during the pandemic. Similarly, in October 2020, Oracle collaborated with FHI Clinical for improving the efficiency of the clinical trial and helped in getting therapies to market faster.

Additionally, the increasing occurrence of people suffering from chronic diseases, such as heart diseases, infectious diseases, neurological diseases, and the rising geriatric population, are factors that propel the growth virtual clinical market. For instance, according to the Center for Disease Control and Prevention (2021), in the United States, on average, 6 out of 10 people are suffering from a chronic disease, and 4 out of 10 people are suffering from two or more, resulting in the leading cause of death in the country. According to the WHO, in 2020, chronic diseases accounted for almost three-quarters of all deaths, worldwide, and that 71% of deaths due to ischaemic heart disease (IHD), 75% of deaths due to stroke, and 70% of deaths due to diabetes may occur in developing countries. With the increasing burden of diseases, it is expected to increase the demand for the development of new drugs. This is further anticipated to fuel the technological development in the healthcare industry, thereby, augmenting the market growth.

However, a greater amount of collection data prove and manage reliability to regulators, technology failure, and data accuracy, which are some of the challenges anticipated to hamper the growth of the global virtual clinical trials market.

The oncology segment is expected to dominate the market over the forecast period due to increasing government initiatives for cancer awareness, rising in the prevalence of cancer, and increasing R&D activities on the development of cancer drugs, thus, increasing the number of oncological trials. According to Globocan 2020 fact sheet, an estimated 19,292,789 cancer cases were diagnosed with 9,958130 death due to cancer.

The worldwide cancer burden is rising, worldwide. Virtual clinical trials minimize the cancer patient's risk (risk of Immunosuppression, travel burden, therapeutic diversity, and regulatory complexity) and decrease time spent on face-to-face trial visits. To keep patients safe, oncology clinical trial investigators and sponsors have quickly incorporated virtual and remote trials. In October 2019, the Georgetown University Medical Center used cloud-based virtual interconnected computing techniques for deducting the time in accessing cancer patients' profiles, which indicates that the number of cases virtually assessed augmented from 46 to 622 as compared to the conventional assessments from 3 to 14 cases from 2014-2017.

According to the National Clinical Trials, in April 2020, around 8,306 clinical trials on oncology across the various phases of development were conducted. As the number of clinical trials increased, there are higher chances of increasing the demand for virtual clinical trials. Thus, the factors mentioned above are expected to drive the segment over the forecast period.

Geographically, North America accounts for one of the largest revenue holders in the global virtual clinical trials market due to the presence of major companies that manufacture pharmaceuticals, coupled with rising government and companies, which focus on investment in the development of new medicines. In November 2019, Janssen, a pharmaceutical subsidiary of Johnson & Johnson, in collaboration with the PRA Health Sciences, launched a digital clinical trial set-up CHIEF-HF a completely decentralized, indication-seeking, mobile clinical study. The company aims to utilize wearable devices and smart technology to efficiently gather and analyze evidence for assessing the effectiveness of Canagliflozin in the populace with heart failure with the presence or absence of Type 2 diabetes.

Moreover, the region is expected to continue its dominance over the forecast period. This can be attributed to increasing R&D in the region and the adoption of new technologies in clinical research and government support. Furthermore, market players are using digital technologies to meet client needs. For instance, in 2020, Parexel performed more than 100 decentralized trials, including hybrid and virtual/decentralized approaches. However, due to an increase in cancer cases and other chronic diseases, the virtual clinical trials market is likely to boost significantly throughout the forecast period.

The virtual clinical trials market is highly competitive and consists of several major players. The players operating in the market are operating on different competitive factors, such as experience in the pharmaceutical, experience in clinical trials, and investment in technology. The strategies adopted by the market participants are partnerships, collaborations, agreement, product launch, and product expansion. The players include Clinical Ink inc., IQVIA Holdings Inc., ICON PLC, Laboratory Corporation of America Holdings (Covance Inc.), LEO Innovation Lab., Dassault Systemes SE (Medidata Solutions Inc.), Oracle Corporation, Parexel International Corporation, Medable Inc., and Signant Health.