Base Metals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1435804

리서치사:Mordor Intelligence

발행일:2024년 02월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

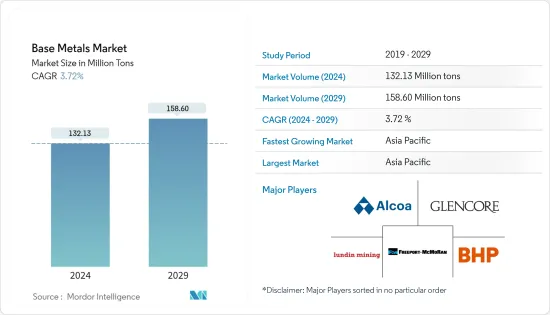

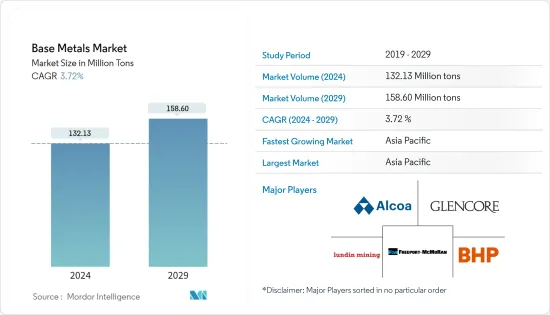

비금속 시장 규모는 2024년 1억 3,213만 톤으로 추정되며, 2029년까지 1억 5,860만 톤에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 3.72%의 CAGR로 성장할 것으로 예상됩니다.

신종 코로나바이러스 감염증(COVID-19) 팬데믹은 시장에 악영향을 끼쳤습니다. 봉쇄 및 제한 조치로 인해 제조 시설과 공장이 중단되었기 때문입니다. 공급망과 운송의 혼란으로 인해 시장에 더 많은 장애가 발생했습니다. 그러나 2021년에는 업계가 회복세를 보이며 조사 대상 시장의 수요가 회복세를 보였습니다.

주요 하이라이트

중기적으로 조사 대상 시장의 성장을 촉진하는 주요 요인은 건설 산업의 수요 증가입니다.

반대로, 비금속 가공 및 비금속을 사용한 제품 제조 과정에서 온실 가스 배출량이 증가하면 조사 대상 시장의 성장을 저해할 것으로 예상됩니다.

그러나 전기자동차(EV) 생산 부문의 수요 증가로 인해 예측 기간 동안 많은 기회가 제공될 것으로 예상됩니다.

아시아태평양이 시장을 장악하고 중국, 인도, 일본의 소비가 가장 클 것으로 예상됩니다.

비금속 시장 동향

건설 업계의 수요 확대

건설 산업에서 사용되는 비금속은 내구성과 강도로 인해 선택되며 다양한 기능을 수행합니다. 그 중 가장 일반적인 것은 알루미늄과 구리입니다.

알루미늄은 내식성, 전기 전도성, 연성이 우수하여 건설 산업에서 일반적으로 사용됩니다. 이 금속은 혹독한 날씨에 대한 저항력이 있기 때문에 창문, 문, 전선뿐만 아니라 야외 표지판과 가로등에도 사용됩니다. 금속은 시트, 튜브 및 주물로 가공됩니다. HVAC 덕트, 지붕, 벽 및 손잡이는 알루미늄으로 만들어집니다. 또한, 건설 산업에서도 흔히 볼 수 있습니다.

구리 기반 튜브는 종종 건물 내부의 파이프를 만드는 데 사용됩니다. 구리는 연성 및 가단성 금속으로 물과 토양에 의한 부식에 강합니다. 또한 재활용이 가능합니다. 구리 튜브는 납땜이 쉽고 지속적인 결합을 형성합니다. 이러한 모든 특성으로 인해이 금속은 배관 및 튜브에 이상적인 선택입니다. 경질 구리 튜브는 건물의 온수 및 냉수 수도관에 가장 적합하며 연질 구리 튜브는 HVAC 시스템 및 히트 펌프의 냉매 라인 제조에 자주 사용됩니다.

국제토목학회(ICE)의 조사에 따르면 세계 건설 산업은 주로 중국, 인도, 미국이 주도하고 있으며, 2030년까지 8조 달러에 달할 것으로 예상됩니다. 따라서 성장하는 건설 산업은 비금속 시장에 대한 수요를 증가시킬 것으로 예상됩니다.

미국 인구조사국에 따르면 2022년 미국의 민간 건설액은 1조 4,300억 달러로 2021년 1조 2,800억 달러에 비해 10.47% 증가했습니다. 2022년 주택 건설 지출은 8,991억 달러로 2021년 대비 13.3% 증가했지만, 비주택 건설 지출은 5,301억 달러로 2021년 대비 9.1% 감소했습니다. 미국의 민간 건설은 미국의 건설 산업에서 비금속 시장에 대한 수요를 증가시킬 것으로 예상됩니다.

또한 2022년 5월 미국 정부는 공항과 항만 현대화, 도로 및 교량 재건을 위한 4,300개의 특정 프로젝트 수행에 1,100억 달러 이상을 배정할 것이라고 발표했습니다. 이 프로젝트는 50개 주에 있는 약 3,200개 지역사회에 혜택을 줄 것으로 예상됩니다.

또한, 중국은 현재 건설 메가붐의 한가운데에 있습니다. 중국은 세계 최대 규모의 건축 시장을 보유하고 있으며, 전 세계 건설 투자의 20%를 차지하고 있습니다. 2030년까지 중국에서만 13조 달러에 육박하는 건축비를 지출할 것으로 예상됩니다.

또한 인도의 주택 부문은 증가 추세에 있으며 정부의 지원과 노력으로 수요가 더욱 증가하고 있습니다. 인도 브랜드 주식 재단(IBEF)에 따르면 주택 도시 개발부(MoHUA)는 주택 건설과 중단 된 프로젝트를 완료하기위한 기금 조성을 위해 2022-2023년 예산에 98억 5 천만 달러를 할당했습니다. 따라서 주택 부문에 대한 투자 증가는 비금속 시장에 대한 수요를 증가시킬 것으로 예상됩니다.

캐나다 건설협회에 따르면, 건설 부문은 캐나다 최대 고용주 중 하나이며, 캐나다의 경제적 성공에 크게 기여하고 있습니다. 이 산업은 캐나다 국내총생산(GDP)의 7%를 차지합니다. 예를 들어 캐나다 통계청에 따르면 2022년 2분기 건축 건설 총 투자액은 3.3% 증가한 623억 달러로 3분기 연속 증가세를 보였습니다. 주택 투자는 464억 달러에 달했는데, 이는 주로 공동주택 건설에 대한 지출 증가에 기인합니다. 비주거 부문은 2.6% 증가한 158억 달러에 달했습니다.

또한 캐나다 신건축계획(NBCP), 저렴한 주택 이니셔티브(AHI) 등 다양한 정부 프로젝트가 이 부문의 성장을 뒷받침하고 있습니다. 캐나다에서는 최근 몇 년 동안 주택 부문과 상업 부문이 꾸준히 성장하고 있습니다. 이 나라에서는 팬더 콘도, 하우드 콘도, 파워 앤 애들레이드 콘도, 아마존 유통센터/오타와와 같은 대규모 건설 프로젝트가 몇 차례 진행되었습니다.

모로코에서 상업시설과 호텔 개발 프로젝트가 증가함에 따라 모리타이트 시장의 수요는 상승세를 보일 것으로 예상됩니다. 예를 들어, 힐튼은 현재 모로코에서 5개의 호텔을 운영하고 있으며, 모로코 전역에 6개의 호텔이 개발 중이며, 콘래드 라바트 알자나셋이 몇 달 안에 오픈할 예정이며, 더블트리 바이 힐튼 마리나 아가디르 호텔 & 레지던스가 2023년 3분기에 오픈할 예정입니다. 오픈할 예정입니다.

위의 모든 요인으로 인해 예측 기간 동안 비금속 수요는 상승세를 보일 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 예측 기간 동안 가장 큰 비금속 시장이 될 것으로 예상됩니다. 건설 산업에 대한 투자 증가, 전기 및 전자 생산 증가, 다국적 기업의 산업 부문에 대한 투자로 인한 중장비 수요 급증은 이 지역의 비금속 수요를 촉진하는 주요 요인 중 일부입니다.

중국은 아시아태평양에서 비금속 시장에서 가장 큰 시장 점유율을 차지하고 있습니다. 국내 투자 및 건설 활동의 증가로 인해 비금속 시장 수요는 예측 기간 동안 증가할 것으로 예상됩니다. 중국은 지난 몇 년 동안 세계 인프라에 대한 주요 투자 국가 중 하나이며 상당한 기여를 하고 있습니다. 예를 들어, 중국 국가통계국(NBS)에 따르면 2022년 중국의 건설 공사 생산액은 27조 6,300억 위안(4조 1,100억 달러)에 달해 2021년 대비 6.6% 증가할 것으로 예상했습니다.

중국의 인구구조로 인해 주택건설의 성장은 앞으로도 가속화될 것으로 예상됩니다. 가계 소득 수준 상승과 농촌에서 도시로의 인구 이동이 맞물려 국내 주택 건설 부문의 수요는 계속 증가할 것으로 예상됩니다.

또한 중국은 세계 최대의 자동차 생산국이기도 합니다. 중국은 국내 승용차 시장 제품에 기여하는 다른 요인들 중에서도 물류 및 공급망 개선, 기업 활동 증가, 국내의 풍부한 소비 촉진 조치로 인해 가장 큰 승용차 생산국 중 하나가되었습니다. 따라서 이로 인해 승용차 부문의 비금속 소비에 대한 수요가 증가했습니다. 예를 들어, OICA에 따르면 2022년 중국의 승용차 생산량은 2021년 대비 11% 증가한 238만 대에 달할 것으로 예상됩니다.

인도에서는 차량 배기가스 규제 강화, 차량 안전성 향상, 차량에 운전 보조 시스템 도입, 소매 및 E-Commerce 분야의 급속한 물류 성장으로 인해 신형 및 고급 소형 상용차에 대한 수요가 크게 증가하고 있습니다. (LCV). 예를 들어, OICA에 따르면 2022년 인도의 소형 상용차 생산량은 61만 7,400대에 달해 2021년 대비 27% 증가했고 2020년 대비 60% 회복했습니다.

또한 인도의 자동차 산업에 대한 투자 증가와 발전으로 인해 비금속 소비가 증가할 것으로 예상됩니다. 예를 들어, 타타자동차는 2022년 4월 향후 5년간 승용차 사업에 30억 8,000만 달러를 투자할 계획을 발표했습니다. 따라서 자동차 생산 증가와 자동차 산업에 대한 투자 증가로 인해 국내 자동차 및 운송 산업의 비금속 시장에 대한 수요가 증가할 것으로 예상됩니다.

인도에는 12만 3,240km의 노선 길이를 가진 세계 4위의 철도망이 있으며, 여객 열차 13,450편과 화물 열차 9,141편이 있으며, 7,350개 역에서 하루 2,400만 명의 승객과 2억 3,800만 톤의 화물을 수송하고 있습니다. 최근 인도 철도의 발전과 정부의 노력으로 인해 조사 대상 시장이 확대될 가능성이 있습니다. 2022-23년 연방 예산안에 따르면 철도부에 1조 4,000억 루피(미화 184억 달러)가 배정됐습니다. 이로 인해 자동차 및 운송 산업의 비금속 시장이 확대될 것입니다.

구리, 주석, 니켈, 알루미늄 등은 전자 산업에서 자주 사용되는 금속입니다. 아시아 지역은 세계 최대의 전기 및 전자기기 생산국이며, 중국, 일본, 한국, 싱가포르, 말레이시아 등 국가들이 세계 수준에서 우위를 점하고 있습니다.

일본 전자정보기술협회(JEITA)에 따르면 2022년 12월 일본 국내 가전제품 출하액은 1,252억 엔(9억6,404만 달러)에 달했으며, 3월이 가장 호조를 보였으나 약 1,255억 엔(9억6,635만 달러)로 가장 부진한 달이었습니다. (9억 6,635만 달러)였던 반면, 5월에는 864억 엔(6억 6,528만 달러)로 가장 부진했습니다. 따라서, 중국 내 가전제품 출하량 증가는 비금속 시장에 상승 여력을 제공할 것으로 예상됩니다.

따라서 이 지역의 이러한 모든 호의적인 동향과 투자는 예측 기간 동안 비금속 수요를 촉진할 것으로 예상됩니다.

비금속 산업 개요

비금속 시장은 본질적으로 세분화되어 있습니다. 이 시장의 주요 기업으로는 Glencore, Freeport-McMoRan, Alcoa Corporation, Lundin Mining Corporation, BHP 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

건설 업계의 수요 상승

경량 차량에 대한 높은 수요

기타 촉진요인

성장 억제요인

온실가스 배출량 증가

기타 성장 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

구매자의 교섭력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

제5장 시장 세분화(시장 규모 : 수량 기준)

유형

구리

아연

납

니켈

알루미늄

주석

최종 이용 산업

건설

자동차·수송

전기·전자

소비자 제품

의료기기

기타

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 상황

M&A, 합작투자, 제휴, 협정

시장 점유율 분석/순위 분석

주요 기업의 전략

기업 개요

Alcoa Corporation

Anglo American plc

BHP

Freeport-McMoRan

Glencore

Jiangxi Copper Corporation

Lundin Mining Corporation

Rio Tinto

Vale

Vedanta Resources Limited

제7장 시장 기회와 향후 동향

ksm

영문 목차

영문목차

The Base Metals Market size is estimated at 132.13 Million tons in 2024, and is expected to reach 158.60 Million tons by 2029, growing at a CAGR of 3.72% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

Over the medium term, the major factor driving the growth of the market studied is the increasing demand from the construction industry.

On the flip side, the increasing emission of greenhouse gases during the processing of base metals and the manufacturing of products using base metals is expected to hinder the growth of the market studied.

However, increasing demand from the electric vehicle (EV) production sector is anticipated to provide numerous opportunities over the forecast period.

The Asia-Pacific region is expected to dominate the market, with the largest consumption from China, India and Japan.

Base Metals Market Trends

Growing Demand from the Construction Industry

Chosen for their durability and strength, base metals used in the construction industry serve a wide range of functions. The most common of them are aluminum and copper.

Aluminum is commonly used in the construction industry because it is resistant to corrosion, highly conductive, and ductile. Due to its resistance to harsh weather, the metal is used in windows, doors, and wire, as well as outdoor signage and street lights. The metal is processed into sheets, tubes, and castings. HVAC ducts, roofs, walling, and handles are made of aluminum. Furthermore, they are frequently found in the construction industry.

Copper-based tubing is often used to construct pipes in buildings. Copper is a ductile and malleable metal, and it is resistant to corrosion from water and soil. It is also recyclable. Copper tubing is easily soldered, forming lasting bonds. All of these properties make this metal ideal for piping and tubing. Rigid copper tubing is ideal for hot and cold tap water pipes in buildings, while soft copper tubing is frequently used to make refrigerant lines in HVAC systems and heat pumps.

According to a study by the Institution of Civil Engineers (ICE), the global construction industry is expected to reach USD 8 trillion by 2030, primarily driven by China, India, and the United States. Therefore, the growing construction industry is expected to have an upside demand for base metals market.

According to the US Census Bureau, the value of private construction in the United States in 2022 was USD 1.43 trillion, which shows an increase of 10.47% compared to 2021, which amounted to USD 1.28 trillion. Residential construction spending in 2022 amounted to USD 899.1 billion, which showed an increase of 13.3% compared to 2021, while non-residential construction spending amounted to USD 530.1 billion, which showed a decrease of 9.1% compared to 2021. Therefore, increasing in the private constructions in the United States is expected to create an upside demand for base metals market from the country's construction industry.

Additionally, in May 2022, the the United States government announced to the allocation of over USD 110 billion for carrying out 4.3 thousand specific projects for modernizing airports and ports and rebuilding roads and bridges. These projects are expected to benefit around 3.2 thousand communities across the 50 states.

Moreover, China is in the midst of a construction mega-boom. The country has the largest building market in the world, making up 20% of all construction investment globally. The country alone is expected to spend nearly USD 13 trillion on buildings by 2030.

Furthermore, the residential sector in India is on an increasing trend, with government support and initiatives further boosting the demand. According to the India Brand Equity Foundation (IBEF), the Ministry of Housing and Urban Development (MoHUA) allocated USD 9.85 billion in the 2022-2023 budget to construct houses and create funds to complete the halted projects. Therefore, the increasing investments in the residential sector are expected to create an upside demand for the base metal market.

According to the Canadian Construction Association, the construction sector is one of Canada's largest employers and a major contributor to the country's economic success. The industry contributes 7% of the country's Gross Domestic Product (GDP). For instance, according to Statistics Canada, total investment in building construction increased by 3.3% during Q2 2022, and reached USD 62.3 billion, thus increasing for the third consecutive quarter. The residential investment reached USD 46.4 billion, largely due to increased spending on building multifamily homes. The non-residential sector increased by 2.6% to USD 15.8 billion.

In addition, various government projects, such as New Building Canada Plan (NBCP) and Affordable Housing Initiative (AHI), are supporting the sector's growth. In Canada, the residential and commercial sectors have been witnessing steady growth in the recent past. The country witnessed some of the largest construction projects, such as Panda Condominium, Harwood Condominium, Power and Adelaide Condominium, and Amazon Distribution Centre/Ottawa.

Due to the growing number of commercial and hotel development projects in Morocco, the demand for base metals market is expected to have an upside demand. For instance, In Morocco, Hilton currently operates five hotels and has six hotels under development across the country, with Conrad Rabat Arzanaset to open in the coming months and the DoubleTree by Hilton Marina Agadir Hotel & Residences set to open in Q3 2023.

Owing to all above mentioned factors, the demand for base metals is expected to have an upside demand during the forecast period.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region is projected to be the largest market for base metals during the forecast period. The increasing investments in the construction industry, rising electrical and electronics production, and surging demand for heavy equipment, with multinational companies investing in the industrial sector, are some of the major factors driving the demand for base metals in the region.

China holds the largest Asia-Pacific market share for the base metals market. The demand for the base metals market is expected to rise throughout the forecast period due to rising investments and construction activity in the country. China is a huge contributor, as it has been one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to CNY 27.63 trillion (USD 4.11 trillion), an increase of 6.6% compared with 2021.

Demographics in China are expected to continue to spur growth in residential construction. Rising household income levels combined with population migrating from rural to urban areas is expected to continue to drive demand for residential construction sector in the country.

Moreover, China is also the largest manufacturer of automobiles in the world. China is one of the largest producers of passenger cars, due to the improving logistics and supply chains, increased business activity, and the country's raft of pro-consumption measures, among other factors contributing to the passenger car market products in the country. Therefore, this has increased demand for base metals consumptuon from the passenger car segment. For instance, according to OICA, in 2022, the passenger car production in China amounted to 2.38 million units, which shown an increase of 11% compared to 2021.

In India, increasing regulations on vehicle emissions, advancement in vehicle safety, the introduction of driver-assist systems in vehicles, and rapidly growing logistics in the retail and e-commerce sectors, have been significantly driving the demand for new and advanced Light commercial vehicles (LCVs). For instance, accroding to OICA, in 2022, light commercial vehicle production in India amounted to 617.4 thousand units, which showen an increase of 27% compared to 2021 and a recovery of 60% compared to 2020.

Moreover, increased investments and advancements in the automobile industry in India is expected to increase in the consumption of base metals. For instance, in April 2022, Tata Motors announced plans to invest USD 3.08 billion in its passenger vehicle business over the next five years. Therefore, increasing in the peroduction of automobiles and increasing investments in the automobile industry is expected to have an upside demand for base metals market from the country's automotive and transportaion industry..

India has the fourth largest railway network with a route length of 123.24 thousand kilometres and 13.45 thousand passenger trains and 9.141 thousand freight trains transporting 24 million passengers and 203.88 million tonnes of freight per day from 7.35 thousand stations. Recent developments and government initiatives in railways in India may boost the market studied. As per Union Budget 2022-23, Ministry of Railways have been allocated INR 1.40 trillion (USD 18.40 billion). Thus boosting the base metals market from automobile and transportation industry.

Copper, tin, nickel, and aluminum are some common metals used by the electronics industry. The Asian region is the largest producer of electrical and electronics across the globe with countries such as China, Japan, South Korea, Singapore, and Malaysia dominating at the global level.

In Japan, according to JEITA (Japan Electronics and Information Technology Association), domestic shipments of consumer electronics in Japan reached a value of JPY 125.2 billion (USD 964.04 million) in December 2022. While March was the strongest month for consumer electronics shipments during2022, with around JPY 125.5 billion (USD 966.35 million), May was the weakest, with the value falling to JPY 86.4 billion (USD 665.28 million). Therefore, increasing in the shipments of consumer electronics from the country is expected to have an upside for base metals market.

Hence, all such favorable trends and investments in the region are expected to drive the demand for base metals during the forecast period.

Base Metals Industry Overview

The Base Metals Market is fragmented in nature. The major players in this market (not in a particular order) include Glencore, Freeport-McMoRan, Alcoa Corporation, Lundin Mining Corporation, and BHP, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand from the Construction Industry

4.1.2 High Demand for Lightweight Vehicles

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Increasing Emission of Greenhouse Gases

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Type

5.1.1 Copper

5.1.2 Zinc

5.1.3 Lead

5.1.4 Nickel

5.1.5 Aluminum

5.1.6 Tin

5.2 End-user Industry

5.2.1 Construction

5.2.2 Automotive and Transportation

5.2.3 Electrical and Electronics

5.2.4 Consumer Products

5.2.5 Medical Devices

5.2.6 Others

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share Analysis**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Alcoa Corporation

6.4.2 Anglo American plc

6.4.3 BHP

6.4.4 Freeport-McMoRan

6.4.5 Glencore

6.4.6 Jiangxi Copper Corporation

6.4.7 Lundin Mining Corporation

6.4.8 Rio Tinto

6.4.9 Vale

6.4.10 Vedanta Resources Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Demand from Electric Vehicle (EV) Production Sector