Sulfuric Acid Market by Raw Material (Elemental Sulfur, Base Metal Smelters, Pyrite Ore), Application (Fertilizers, Chemical Manufacturing, Metal Processing, Petroleum Refining, Textiles, and Automotive), and Region - Global Forecast to 2030

상품코드:1807084

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 258 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

세계의 황산 시장 규모는 2025년 412억 3,000만 달러에서 2030년까지 499억 4,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 3.9%의 성장이 예상됩니다.

황산은 강한 산성과 탈수 특성으로 인해 다양한 부문에서 사용되는 필수 산업용 화학제품입니다.

조사 범위

조사 대상 연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

100만 달러, 100만 톤

부문

원료, 등급, 형태, 공정, 용도

대상 지역

북미, 아시아태평양, 서유럽, 중남미, 중동, 아프리카

황산은 주로 원소 유황과 황철광과 같은 원료를 사용하여 접촉 공정에서 생산되며 비료, 금속 가공, 석유 정제, 섬유 및 화학 제조에 사용됩니다. 황산 시장은 화학 제조와 석유 정화에 대한 수요 증가로 꾸준히 성장하고 있습니다. 화학제조는 여러 산업에서 사용되는 산과 중간체의 생산에 중요한 역할을 하며, 석유 정제는 보다 깨끗한 연료의 제조에 도움이 되는 알킬화 공정을 지원합니다. 이러한 하류 제품의 요구 증가와 환경 규제 강화는 시장 성장의 주요 촉진요인이 되었습니다.

"수량에서는 비금속 제련 원재료 부문이 예측 기간에 두 번째 시장 점유율을 차지합니다."

비금속 제련 부문은 구리, 아연, 니켈과 같은 주요 비철금속 생산에 중요한 역할을 하기 때문에 예측 기간 동안 황산 시장에서 수량 기준으로 2위 점유율을 차지할 전망입니다. 이 황을 많이 포함하는 광석의 제련 중에 이산화황 가스가 부산물로 방출됩니다. 이 가스는 회수되어 접촉법과 같은 확립된 방식으로 황산으로 전환됩니다. 건설, 전기 인프라, 배터리 제조 및 신재생에너지 기술에서 광범위한 사용을 지원하는 비금속 수요 증가는 전 세계적으로 제련 활동 증가를 야기하고 있습니다. 또한, 황 배출을 줄이기 위한 엄격한 환경 규제로 제련업체는 황 회수 기술의 도입을 강요하여 황산 회수를 촉진하고 있습니다. 환경 기준을 충족시키면서 황산을 생산하는 이중 이점으로 인해 비금속 제련은 세계 황산 시장에서 점점 더 중요한 원료 공급원이 되었습니다.

"수량에서는 화학제조 분야가 예측기간에 2위 시장 점유율을 차지합니다."

화학 제조 용도 부문은 주로 황산이 광범위한 산업용 화학제품을 생산할 때 원료로서 중요한 역할을 담당하고 있기 때문에 예측 기간에 황산 시장에서 수량 기준으로 2위의 점유율을 차지할 전망입니다. 황산은 염산, 질산, 인산, 각종 황산염 등의 화합물의 제조에 널리 사용되고 있으며, 이들은 세제, 합성수지, 염료, 의약품, 안료, 화약의 제조에 있어서 중요한 중간체가 되고 있습니다. 섬유, 의료, 플라스틱, 소비재 등의 최종 이용 산업의 확대에 추진되어, 이러한 화학제품의 세계적인 수요가 계속 증가하고 있기 때문에 황산의 요구도 그에 따라 높아지고 있습니다. 게다가 신흥경제권에서 대규모 화학생산으로의 꾸준한 전환과 관리된 화학처리를 필요로 하는 환경규제의 강화가 황산시장에서의 이 용도 부문의 성장을 더욱 추진하고 있습니다.

"수량에서는 중동 및 아프리카가 예측 기간에 두 번째 시장 점유율을 차지합니다."

중동 및 아프리카는 산업기반이 확대되고 선광과 비료 생산에 대한 주력이 높아지고 있기 때문에 예측기간에 황산시장에서 수량 기준으로 2위 점유율을 차지할 전망입니다. 이 지역의 국가들은 특히 구리, 아연, 인산염과 같은 금속의 추출과 정제, 즉 대량의 황산이 필요한 공정을 위해 채광 및 야금 프로젝트에 투자하고 있습니다. 게다가 특히 아프리카 경제권에서는 식량안보와 농업생산성을 뒷받침하는 비료에 대한 수요가 높아져 황산 소비를 더욱 밀어 올리고 있습니다. 새로운 제조 및 가공 시설의 개발, 인프라의 성장, 산업의 다양화에 대한 대처가, 다양한 부문에서 황산의 왕성한 수요를 계속해서 추진하고 있습니다.

이 보고서는 세계 황산 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

황산 시장의 기업에게 매력적인 기회

황산 시장 : 지역별

황산 시장 : 용도별

황산 시장 : 원재료별

황산 시장 : 주요 국가별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

억제요인

기회

과제

제6장 산업 동향

세계의 거시경제 전망

공급망 분석

원재료 공급

황산 제조

제품 유형별

유통 네트워크

최종 이용 산업

생태계 분석

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

가격 설정 분석

황산의 평균 판매 가격의 동향 : 지역별(2022-2024년)

공업 등급의 평균 판매 가격의 동향 : 주요 기업별(2024년)

관세 및 규제 상황

관세 분석

규제기관, 정부기관, 기타 조직

기준과 규제

주요 컨퍼런스 및 이벤트(2025-2026년)

특허 분석

기술 분석

주요 기술

인접 기술

사례 연구 분석

황산 재생에 의한 지속가능성과 효율성의 향상

BASF, 새로운 고순도 황산 플랜트의 건설로 유럽의 반도체 공급망을 강화

무역 데이터

수입 시나리오(HS 코드 280700)

수출 시나리오(HS 코드 280700)

고객사업에 영향을 주는 동향/혼란

투자 및 자금조달 시나리오

황산 시장에 대한 생성형 AI의 영향

소개

황산 생산 최적화

정밀 농업의 실현

공급 체인의 합리화

환경에 미치는 영향을 최소화

황산 시장에 대한 미국 관세의 영향

시장에 영향을 미치는 주요 관세율

가격의 영향 분석

다양한 지역에 중요한 영향

황산의 최종 이용 산업에 대한 영향

제7장 황산 시장 : 형태별

소개

진한 황산

타워 및 글로버산

챔버 및 비료산

배터리산

66도 보메 황산

묽은 황산

제8장 황산 시장 : 등급별

소개

공업 등급

배터리 등급

CP급(화학적으로 순수)

제9장 황산 시장 : 프로세스별

소개

접촉 프로세스

이중 접촉(DCDA)

제10장 황산 시장 : 원재료별

소개

원소 황

황철광

비금속 제련

기타 원재료

제11장 황산 시장 : 용도별

소개

비료

금속가공

펄프 및 종이

석유 정제

섬유

자동차

화학제조

기타 용도

제12장 황산 시장 : 지역별

소개

아시아태평양

중국

일본

인도

인도네시아

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

서유럽

독일

이탈리아

프랑스

영국

스페인

기타 서유럽

중유럽 및 동유럽

러시아

튀르키예

중앙유럽과 동유럽의 다른 지역

중동 및 아프리카

GCC 국가

모로코

기타 중동 및 아프리카

남미

브라질

아르헨티나

칠레

기타 남미

제13장 경쟁 구도

소개

주요 진입기업의 전략/강점

수익 분석

시장 점유율 분석

주요 시장 기업 순위(2024년)

주요 기업 시장 점유율(2024년)

브랜드 및 제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

경쟁 시나리오

평가 및 재무지표

제14장 기업 프로파일

주요 기업

MOSAIC

JIANGXI COPPER CORPORATION

OCP

PHOSAGRO GROUP

AURUBIS AG

BASF

CHEMTRADE LOGISTICS

NOURYON

Q-ACID

LANXESS

PVS CHEMICALS

MITSUBISHI SHOJI CHEMICAL CORPORATION

WEYLCHEM INTERNATIONAL GMBH

CHINA PETROLEUM & CHEMICAL CORPORATION

KOREAZINC

TOAGOSEI CO., LTD.

OCCL LIMITED

AMAL LTD

ECOVYST INC.

BOLIDEN GROUP

기타 기업

ACIDOS Y MINERALES DE VENEZUELA CA

INDUSTRIAS BASICAS DE CALDAS SA

DEXO CHEM LABORATORIES

PCIPL

제15장 인접 시장과 관련 시장

소개

제한 사항

상호연결된 시장

고순도 황산 시장

시장의 정의

시장 개요

고순도 황산 시장 : 등급별

PPB

PPT

제16장 부록

JHS

영문 목차

영문목차

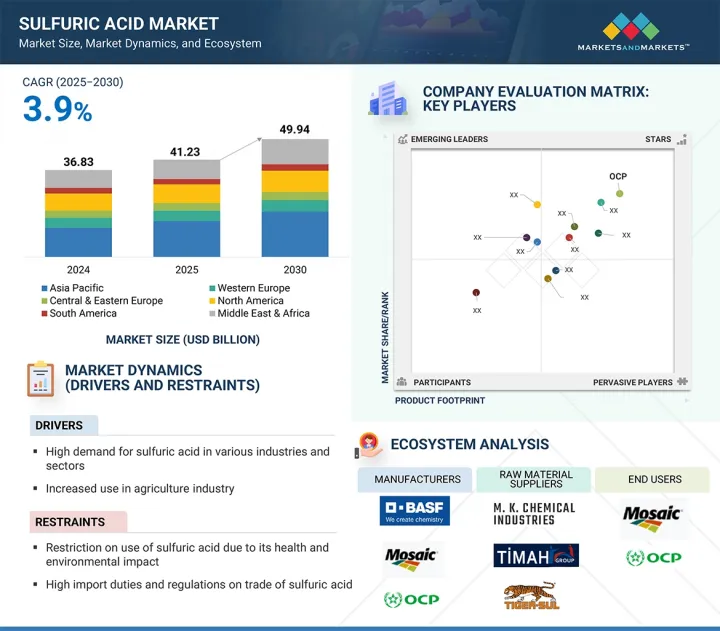

The global sulfuric acid market is projected to grow from USD 41.23 billion in 2025 to USD 49.94 billion by 2030, at a CAGR of 3.9% during the forecast period. Sulfuric acid is an essential industrial chemical used across various sectors because of its strong acidic and dehydrating properties.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Million Tons)

Segments

Raw Material, Grade, Form Type, Process, and Application

Regions covered

North America, Asia Pacific, Western Europe, Central & Eastern Europe, South America, and the Middle East & Africa

It is mainly produced through the contact process using raw materials like elemental sulfur and pyrite ore and is used in fertilizers, metal processing, petroleum refining, textiles, and chemical manufacturing. The sulfuric acid market is steadily growing, driven by increasing demand in chemical manufacturing and petroleum refining. In chemical manufacturing, it plays a crucial role in producing acids and intermediates used in multiple industries, while in petroleum refining, it supports alkylation processes that help create cleaner fuels. The rising need for these downstream products and stricter environmental regulations are key factors fueling market growth.

"In terms of volume, base metal smelters raw material segment to account for second-largest market share during the forecast period"

The base metal smelters segment is expected to hold the second-largest share in the sulfuric acid market by volume during the forecast period, driven by its crucial role in producing key non-ferrous metals such as copper, zinc, and nickel. During the smelting of these sulfur-rich ores, sulfur dioxide gas is released as a by-product. This gas is then recovered and converted into sulfuric acid using established methods like the contact process, which both reduces harmful emissions and creates a valuable industrial chemical. The increase in demand for base metals-supported by their extensive use in construction, electrical infrastructure, battery manufacturing, and renewable energy technologies-has caused a rise in smelting activities worldwide. Additionally, stringent environmental regulations to cut sulfur emissions have compelled smelters to implement sulfur capture technologies, thereby boosting sulfuric acid recovery. This dual advantage of meeting environmental standards and generating acid makes base metal smelters an increasingly important raw material source in the global sulfuric acid market.

"In terms of volume, chemical manufacturing application segment to account for second-largest market share during forecast period"

The chemical manufacturing segment is expected to hold the second-largest share in the sulfuric acid market by volume during the forecast period, mainly because of the acid's key role as a feedstock in producing a wide range of industrial chemicals. Sulfuric acid is widely used in creating compounds such as hydrochloric acid, nitric acid, phosphoric acid, and various sulfates, which are important intermediates in making detergents, synthetic resins, dyes, pharmaceuticals, pigments, and explosives. As global demand for these chemicals continues to grow-propelled by expanding end-use industries like textiles, healthcare, plastics, and consumer goods-the need for sulfuric acid has increased accordingly. Furthermore, the steady move toward large-scale chemical production in emerging economies, along with stricter environmental regulations requiring controlled chemical processing, is further boosting the growth of this application segment in the sulfuric acid market.

"In terms of volume, Middle East & Africa to account for second-largest market share during forecast period"

The Middle East & Africa is expected to hold the second-largest share by volume in the sulfuric acid market during the forecast period, due to the region's growing industrial base and increased focus on mineral processing and fertilizer production. Countries across the region are investing in mining and metallurgy projects, especially for extracting and refining metals like copper, zinc, and phosphate-processes that need large amounts of sulfuric acid. Additionally, the rising demand for fertilizers to support food security and agricultural productivity, particularly in African economies, further boosts sulfuric acid consumption. The development of new manufacturing and processing facilities, infrastructure growth, and industrial diversification efforts continue to fuel strong demand for sulfuric acid across various sectors.

Profile break-up of primary participants for the report:

By Company Type: Tier 1 - 65%, Tier 2 - 20%, and Tier 3 - 15%

By Designation: Directors- 25%, Managers- 30%, and Others - 45%

By Region: North America - 30%, Asia Pacific - 40%, Western Europe - 12%, Central & Eastern Europe - 8%, Middle East & Africa - 7%, and South America - 3%

PhosAgro Group (Russia), Aurubis AG (Germany), Mosaic (US), OCP (Morocco), and Jiangxi Copper Corporation (China) are some of the major players operating in the sulfuric acid market. These players have adopted acquisitions, agreements, joint ventures, and expansions to increase their market share and business revenue.

Research Coverage

The report defines, segments, and projects the sulfuric acid market based on raw material, grade, form type, process, application, and region. It offers detailed insights into the key factors shaping the market's growth, such as drivers, restraints, opportunities, and challenges. It strategically profiles sulfuric acid manufacturers, thoroughly analyzing their market shares and core competencies, and monitors and evaluates competitive developments like acquisitions, agreements, joint ventures, and expansions.

Reasons to Buy the Report

The report is expected to assist market leaders and new entrants by providing them with the most accurate estimates of revenue figures for the sulfuric acid market and its segments. It is also designed to help stakeholders better understand the market's competitive landscape, gather insights to enhance their business positions, and develop effective go-to-market strategies. Additionally, it enables stakeholders to grasp the market's current trends and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of critical drivers (High demand for sulfuric acid in various industries and sectors, and increased use in agriculture sector), restraints (restriction on use of sulfuric acid due to its health and environmental impact, and high import duties and regulations on trade of sulfuric acid), opportunities (increasing use of sulfuric acid in wastewater treatment), and challenges (difficulties involved in transportation of sulfuric acid) influencing the growth of the sulfuric acid market.

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities in the sulfuric acid market.

Market Development: Comprehensive information about lucrative markets - the report analyses the sulfuric acid market across varied regions.

Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the sulfuric acid market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players in the sulfuric acid market, such as PhosAgro Group (Russia), Aurubis AG (Germany), Mosaic (US), OCP (Morocco), and Jiangxi Copper Corporation (China).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 List of primary interview participants (demand and supply sides)

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of interviews with experts

2.2 MATRIX CONSIDERED FOR DEMAND-SIDE ANALYSIS

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.3.2.1 Calculations for supply-side analysis

2.4 GROWTH FORECAST

2.5 DATA TRIANGULATION

2.6 RESEARCH ASSUMPTIONS

2.7 RESEARCH LIMITATIONS

2.8 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SULFURIC ACID MARKET

4.2 SULFURIC ACID MARKET, BY REGION

4.3 SULFURIC ACID MARKET, BY APPLICATION

4.4 SULFURIC ACID MARKET, BY RAW MATERIAL

4.5 SULFURIC ACID MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Strong demand for sulfuric acid in numerous applications

5.2.1.2 Increased usage of sulfuric acid in agricultural sector

5.2.2 RESTRAINTS

5.2.2.1 Restriction on use of sulfuric acid due to health and environmental concerns

5.2.2.2 High import duties and regulations on trade of sulfuric acid

5.2.3 OPPORTUNITIES

5.2.3.1 Increasing use of sulfuric acid in wastewater treatment

5.2.4 CHALLENGES

5.2.4.1 Difficulties associated with transportation

6 INDUSTRY TRENDS

6.1 GLOBAL MACROECONOMIC OUTLOOK

6.2 SUPPLY CHAIN ANALYSIS

6.2.1 RAW MATERIAL SUPPLY

6.2.2 SULFURIC ACID PRODUCTION

6.2.3 PRODUCT TYPES

6.2.4 DISTRIBUTION NETWORK

6.2.5 END-USE INDUSTRIES

6.3 ECOSYSTEM ANALYSIS

6.4 PORTER'S FIVE FORCES ANALYSIS

6.4.1 BARGAINING POWER OF SUPPLIERS

6.4.2 BARGAINING POWER OF BUYERS

6.4.3 THREAT OF NEW ENTRANTS

6.4.4 THREAT OF SUBSTITUTES

6.4.5 INTENSITY OF COMPETITIVE RIVALRY

6.5 KEY STAKEHOLDERS AND BUYING CRITERIA

6.5.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.5.2 BUYING CRITERIA

6.6 PRICING ANALYSIS

6.6.1 AVERAGE SELLING PRICE TREND OF SULFURIC ACID, BY REGION, 2022-2024

6.6.2 AVERAGE SELLING PRICE TREND FOR TECHNICAL GRADE, BY KEY PLAYER, 2024

6.7 TARIFF AND REGULATORY LANDSCAPE

6.7.1 TARIFF ANALYSIS

6.7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.7.3 STANDARDS AND REGULATIONS

6.8 KEY CONFERENCES AND EVENTS, 2025-2026

6.9 PATENT ANALYSIS

6.9.1 METHODOLOGY

6.10 TECHNOLOGY ANALYSIS

6.10.1 KEY TECHNOLOGIES

6.10.1.1 Wet Gas Sulfuric Acid (WSA) technology

6.10.2 ADJACENT TECHNOLOGIES

6.10.2.1 GORE SO2 Control System

6.11 CASE STUDY ANALYSIS

6.11.1 ENHANCING SUSTAINABILITY AND EFFICIENCY THROUGH SULFURIC ACID REGENERATION

6.11.2 BASF STRENGTHENS EUROPE'S SEMICONDUCTOR SUPPLY CHAIN WITH NEW HIGH-PURITY SULFURIC ACID PLANT

6.12 TRADE DATA

6.12.1 IMPORT SCENARIO (HS CODE 280700)

6.12.2 EXPORT SCENARIO (HS CODE 280700)

6.13 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.14 INVESTMENT AND FUNDING SCENARIO

6.15 IMPACT OF GENERATIVE AI ON SULFURIC ACID MARKET

6.15.1 INTRODUCTION

6.15.2 OPTIMIZING SULFURIC ACID PRODUCTION

6.15.3 ENABLING PRECISION AGRICULTURE

6.15.4 STREAMLINING SUPPLY CHAIN

6.15.5 MINIMIZING ENVIRONMENTAL IMPACT

6.16 IMPACT OF US TARIFF ON SULFURIC ACID MARKET

6.16.1 KEY TARIFF RATES IMPACTING MARKET

6.16.2 PRICE IMPACT ANALYSIS

6.16.3 KEY IMPACT ON VARIOUS REGIONS

6.16.3.1 US

6.16.3.2 Europe

6.16.3.3 Asia Pacific

6.16.4 IMPACT ON END-USE INDUSTRIES OF SULFURIC ACID

6.16.4.1 Metal processing

6.16.4.2 Pulp & paper

6.16.4.3 Petroleum refining

6.16.4.4 Textiles

6.16.4.5 Automotive

6.16.4.6 Chemical manufacturing

7 SULFURIC ACID MARKET, BY FORM TYPE

7.1 INTRODUCTION

7.2 CONCENTRATED SULFURIC ACID

7.2.1 WIDE-RANGING APPLICABILITY TO ACCELERATE MARKET GROWTH

7.3 TOWER/GLOVER ACID

7.3.1 SUSTAINED USE OF TRADITIONAL ACID PRODUCTION SETUPS AND SPECIFIC INDUSTRIAL PROCESSES TO BOOST MARKET

7.4 CHAMBER/FERTILIZER ACID

7.4.1 GROWING DEMAND TO SUPPORT GLOBAL FOOD SECURITY TO PROPEL MARKET

7.5 BATTERY ACID

7.5.1 SUSTAINED DEMAND FOR LEAD-ACID BATTERIES IN CONVENTIONAL AND BACKUP POWER APPLICATIONS TO DRIVE MARKET

7.6 66 DEGREE BAUME SULFURIC ACID

7.6.1 REQUIREMENT FOR STANDARDIZED AND QUALITY-CONTROLLED ACID FORMS IN INDUSTRIAL PROCESSING TO FUEL MARKET

7.7 DILUTE SULFURIC ACID

7.7.1 RISING SAFETY AND REGULATORY CONSIDERATIONS TO PROPEL MARKET

8 SULFURIC ACID MARKET, BY GRADE

8.1 INTRODUCTION

8.2 TECHNICAL GRADE

8.2.1 RISING DEMAND IN KEY INDUSTRIAL PROCESSES SUCH AS FERTILIZER MANUFACTURING TO ACCELERATE MARKET GROWTH

8.3 BATTERY GRADE

8.3.1 GROWING PRODUCTION AND ADOPTION OF LEAD-ACID BATTERIES IN AUTOMOTIVE, INDUSTRIAL, AND BACKUP POWER APPLICATIONS TO FUEL MARKET

8.4 CP GRADE (CHEMICALLY PURE)

8.4.1 INCREASING NEED FOR ULTRA-PURE CHEMICAL INPUTS IN HIGH-PRECISION SECTORS TO DRIVE MARKET

9 SULFURIC ACID MARKET, BY PROCESS

9.1 INTRODUCTION

9.2 CONTACT PROCESS

9.2.1 WIDESPREAD INDUSTRIAL ACCEPTANCE AND OPERATIONAL RELIABILITY TO ACCELERATE MARKET GROWTH

9.3 DOUBLE CONTACT DOUBLE ABSORPTION (DCDA)

9.3.1 INCREASING EMPHASIS ON ENVIRONMENTAL COMPLIANCE AND PRODUCTION EFFICIENCY TO FUEL MARKET

10 SULFURIC ACID MARKET, BY RAW MATERIAL

10.1 INTRODUCTION

10.2 ELEMENTAL SULFUR

10.2.1 ABUNDANT SUPPLY FROM OIL AND GAS REFINING TO ACCELERATE MARKET GROWTH

10.3 PYRITE ORE

10.3.1 LOCAL AVAILABILITY IN MINING REGIONS TO FUEL MARKET

10.4 BASE METAL SMELTERS

10.4.1 INCREASING ENFORCEMENT OF ENVIRONMENTAL REGULATIONS AND INDUSTRY PUSH FOR CLEANER OPERATIONS TO DRIVE MARKET

10.5 OTHER RAW MATERIALS

11 SULFURIC ACID MARKET, BY APPLICATION

11.1 INTRODUCTION

11.2 FERTILIZERS

11.2.1 INCREASING DEMAND DRIVEN BY GLOBAL FOOD SECURITY CONCERNS AND INTENSIFIED AGRICULTURAL PRACTICES TO ACCELERATE MARKET

11.3 METAL PROCESSING

11.3.1 RISING DEMAND FOR BASE AND PRECIOUS METALS DRIVEN BY INDUSTRIAL GROWTH AND CLEAN ENERGY TRANSITION TO FUEL MARKET

11.4 PULP & PAPER

11.4.1 RISING DEMAND FOR PACKAGING AND HYGIENE PRODUCTS TO DRIVE MARKET

11.5 PETROLEUM REFINING

11.5.1 INCREASING DEMAND FOR HIGH-OCTANE, LOW-EMISSION FUELS TO BOOST MARKET

11.6 TEXTILE

11.6.1 RISING PRODUCTION IN EMERGING ECONOMIES AND INCREASING DEMAND FOR HIGH-QUALITY AND FUNCTIONAL FABRICS TO FUEL MARKET

11.7 AUTOMOTIVE

11.7.1 SUSTAINED DEMAND FOR LEAD-ACID BATTERIES IN CONVENTIONAL AND HYBRID VEHICLES TO FUEL MARKET

11.8 CHEMICAL MANUFACTURING

11.8.1 INCREASING PRODUCTION OF DIVERSE INDUSTRIAL AND SPECIALTY CHEMICALS TO PROPEL MARKET

11.9 OTHER APPLICATIONS

12 SULFURIC ACID MARKET, BY REGION

12.1 INTRODUCTION

12.2 ASIA PACIFIC

12.2.1 CHINA

12.2.1.1 Significant fertilizer production to meet vast demand from agriculture to drive market

12.2.2 JAPAN

12.2.2.1 Demand from electronics, food processing, and precision metal treatment sectors to boost market

12.2.3 INDIA

12.2.3.1 Rising fertilizer production aligned with growing agricultural sector to fuel market

12.2.4 INDONESIA

12.2.4.1 Increasing fertilizer production and mineral processing to boost market

12.2.5 SOUTH KOREA

12.2.5.1 Expanding demand in semiconductors, battery, and electronics sectors to drive market

12.2.6 REST OF ASIA PACIFIC

12.3 NORTH AMERICA

12.3.1 US

12.3.1.1 Large-scale agricultural exports increasing demand for fertilizer to fuel market growth

12.3.2 CANADA

12.3.2.1 Robust fertilizer production and large-scale agricultural exports to propel market

12.3.3 MEXICO

12.3.3.1 Strong agricultural activity and rising demand for phosphate-based fertilizers to fuel market growth

12.4 WESTERN EUROPE

12.4.1 GERMANY

12.4.1.1 Strong chemical manufacturing and automotive sectors to fuel market

12.4.2 ITALY

12.4.2.1 Growth of chemical, textile, and automotive sectors to boost market

12.4.3 FRANCE

12.4.3.1 Rising manufacture of chemicals and automotive to drive demand

12.4.4 UK

12.4.4.1 Focus on chemical manufacturing, battery production, and industrial environmental compliance to drive market

12.4.5 SPAIN

12.4.5.1 Extensive agricultural production and high demand for fertilizers to drive market

12.4.6 REST OF WESTERN EUROPE

12.5 CENTRAL & EASTERN EUROPE

12.5.1 RUSSIA

12.5.1.1 Large-scale fertilizer production and integrated chemical industry to fuel market

12.5.2 TURKIYE

12.5.2.1 Expanding agricultural base and chemical industry to propel market

12.5.3 REST OF CENTRAL & EASTERN EUROPE

12.6 MIDDLE EAST & AFRICA

12.6.1 GCC COUNTRIES

12.6.1.1 Saudi Arabia

12.6.1.1.1 Demand from chemical manufacturing and petroleum refining industries to drive market

12.6.1.2 UAE

12.6.1.2.1 Robust demand from petroleum refining and industrial chemical manufacturing to propel market growth

12.6.1.3 Rest of GCC countries

12.6.2 MOROCCO

12.6.2.1 Largest phosphate reserves to boost fertilizer production

12.6.3 REST OF MIDDLE EAST & AFRICA

12.7 SOUTH AMERICA

12.7.1 BRAZIL

12.7.1.1 Large-scale fertilizer production and agricultural output to propel market

12.7.2 ARGENTINA

12.7.2.1 Production of phosphate-based fertilizers to meet major crop nutrient requirements to fuel market

12.7.3 CHILE

12.7.3.1 Demand for petroleum refining and chemical manufacturing to drive market

12.7.4 REST OF SOUTH AMERICA

13 COMPETITIVE LANDSCAPE

13.1 INTRODUCTION

13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

13.3 REVENUE ANALYSIS

13.3.1 TOP 5 PLAYERS' REVENUE ANALYSIS, 2020-2024

13.4 MARKET SHARE ANALYSIS

13.4.1 RANKING OF KEY MARKET PLAYERS, 2024

13.4.2 MARKET SHARE OF KEY PLAYERS, 2024

13.5 BRAND/PRODUCT COMPARISON

13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.6.1 STARS

13.6.2 EMERGING LEADERS

13.6.3 PERVASIVE PLAYERS

13.6.4 PARTICIPANTS

13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.6.5.1 Company footprint

13.6.5.2 Region footprint

13.6.5.3 Application footprint

13.6.5.4 Grade footprint

13.6.5.5 Raw material footprint

13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024