플라스틱 포장은 가볍고 다루기 쉽기 때문에 소비자의 지지는 세계적으로 증가하고 있습니다. 주요 제조 업체는 주로 생산 비용 효율성에서 플라스틱 포장 솔루션에 기울고 있습니다.

주요 하이라이트

제조업체는 폴리에틸렌 테레프탈레이트, 폴리프로필렌, 폴리에틸렌 등의 재료로 만들어진 플라스틱 병을 널리 지지하고 있습니다. 이 재료는 가볍고 깨지기 어려우므로 자재관리이 쉬워집니다. 또한 제조업체는 비용 효율적인 높이에서 플라스틱 포장으로 기울입니다. 포장·가공식품이나 다양한 식음료에 대한 의존도가 높아지고 있기 때문에 플라스틱병·용기 시장은 예측기간 중에 성장할 전망입니다.

PET는 이 지역의 병 제조 업체들 사이에서 중요한 포장 재료가되었습니다. 다양한 형태와 크기를 수용할 수 있는 범용성은 기존의 유리 및 금속 용기를 대체할 수 없는 선택을 제공하며, 포장 산업에서 매우 바람직한 선택이 되었습니다.

주요 하이라이트

세계적인 포장 네트워킹 플랫폼인 PETnology의 보고서에 따르면 2023년 7월 아시아는 세계 PET 산업의 생산 능력 확대의 주도권을 잡을 전망입니다.

PET는 다른 플라스틱 제품에 비해 제조 과정에서 원료 손실이 적기 때문에 제조업체는 다른 플라스틱 포장 제품보다 PET를 선호합니다. PET는 재활용 가능하며 여러 가지 색상과 디자인을 추가할 수 있으므로 선호되는 옵션입니다. 리필 가능한 제품은 소비자 환경에 대한 의식이 높아짐에 따라 등장하여 제품 수요를 창출하는 역할을 수행해 왔습니다.

오염된 수돗물에 대한 우려와 휴대성이라는 본래의 편의성으로 인해 소비자는 점점 고품질의 음료수를 선호하게 되어 병이 들어간 음료수 수요가 급증하고 있습니다. 비알코올 음료의 인기 상승과 함께 병 음료수에 대한 이러한 욕구 증가는 음료 산업에서 플라스틱 병 시장을 추진하게 될 것으로 예상됩니다.

그러나 환경 친화적인 특성을 가진 다른 포장 재료에 대한 경사도 강해지고 있습니다. 알루미늄 캔과 유리병의 소비는 환경 친화적이고 재활용성이 높기 때문에 이 지역에서 높은 채용률을 나타냅니다. 따라서 소비자는 플라스틱에서 다른 재료로의 전환을 강화하고 있습니다.

플라스틱 병 시장 동향

음료 부문이 시장 성장을 견인할 것으로 예상

음료 부문은 병 음료수와 비알코올 음료 수요가 끊이지 않기 때문에 성장이 예상됩니다. 병 음료수 수요는 오염된 수돗물을 마시는 질병의 우려와 병 음료수가 제공하는 휴대의 용이성, 편리성 때문에 소비자가 특히 고품질의 음료수를 요구하는 경향이 있기 때문입니다.

또한, 많은 선진 경제 국가와 신흥 경제 국가에서 사람들은 병이 들어간 물을 선호합니다. 병 음료수는 다양한 음료를 판매하는 상점과 장소에서 판매됩니다. 예를 들어, 국제 병 워터 협회(IBWA)는 미국인이 다른 포장 음료보다 병이 든 물을 선호한다고 말합니다.

2023년 5월에 발표된 Beverage Marketing Corporation의 데이터에 따르면, 2022년 미국 병 음료수의 수량은 159억 갤런에 달하고, 지난 10년간 일관되게 매년 증가하고 있습니다. 최근 몇 병의 음료수가 증가함에 따라 페트병 수요가 전국적으로 급증했습니다.

PET 병은 내구성과 재활용 가능한 특성으로 인해 유리 및 플라스틱 병보다 물 포장 시장에서 널리 사용됩니다. 이 추세는 가볍고 내구성이 높고 비용 효율적인 PET가 물 포장 매체로 점점 널리 보급되고 있음을 보여줍니다.

인구 증가와 라이프스타일의 변화에 따라 중국과 인도에서는 물병의 소비량이 증가 추세에 있어 지속가능성을 요구하는 소비자 동향의 변화에 대응하기 때문에 경량으로 운반이 용이하며 보관이 가능하며 모든 규제조건을 충족하는 다양한 형식의 병에 대한 수요가 탄생하고 있습니다.

각 회사는 또한 시장에서 새로운 병 음료수의 다양한 형식을 혁신하고 자신의 전략으로 병을 홍보하여 시장 화제를 부를 수있는 기회를 제공합니다.

예를 들어 인도에서는 Wahter가 2023년 12월 ISI 인증 병 음료수를 출시했습니다. 이 식수는 광고주가 최저 비용으로 브랜딩할 수 있고, 광고주가 브랜드 계정을 설정하고, 디자인을 업로드하고, 라벨 광고주의 템플릿과 연결하여 타겟 계층에 맞는 마케팅 전략을 취할 수 있는 브랜딩 공간의 80%를 활용합니다.

아시아태평양이 가장 높은 성장을 이룰 전망

아시아태평양의 여러 국가에서 일회용 플라스틱 병과 포장 사용을 줄이는 것이 주요 이니셔티브 중 하나입니다. 중국, 인도, 일본의 의료 및 제약 분야는 세계에서 가장 큰 시장이며 주로 고령화에 의해 견인되고 있습니다.

인도 의약품 생산자 협회에 따르면, 이 나라의 의약품 시장은 2022년 490억 달러에서 2047년 4,500억 달러에 이를 것으로 예상됩니다. 그러므로 이들 기업의 페트병 수요가 증가할 수 있으며 국내 진출기업들에게는 성장 가능성이 있습니다. 인도의 플라스틱 병 시장은 플라스틱 병의 소비와 산업용도가 지속적으로 증가하고 있기 때문에 꾸준히 성장할 것으로 추정됩니다.

게다가 인도는 인구가 가장 많은 지역의 강력한 시장 중 하나이기도 하고, 신흥국 시장의 개척과 동향에 의해 병들이 음료수의 소비가 대폭 증가하고 있습니다. Indian Railway Catering and Tourism Corporation Limited는 페트병 음료수 브랜드 'Rail Neer'를 출시하여 주로 기차 및 기차역에서 판매합니다. 플라스틱병의 소비량 증가와 철도 부문의 성장에 따라 이 공사는 2021년 플라스틱병을 75.30만개에서 2023년에는 3억 5,770만개로 늘렸습니다.

PET병은 1,000갤런의 청량음료를 운송할 때 유리병보다 에너지 효율이 높고 유리나 알루미늄 용기보다 고형 폐기물의 중량이 적습니다. 따라서 이 지역의 소비자 선호도 변화로 인해 기업은 탄산 음료를 PET 병으로 옮기고 재활용 재료를 사용한 병을 개발하고 있습니다.

예를 들어, 홍콩에서는 2024년 4월에 주력 음료 '콜라'에 재생 플라스틱만을 사용한 500ml 페트병을 출시할 예정입니다. 이 세계 음료 회사는 중국에서 생산되는 코카콜라 오리지널, 코카콜라 무당, 코카콜라 플러스의 모든 500ml 병이 100% 재생 폴리에틸렌 테레프탈레이트(rPET)로 전환되었습니다고 발표했습니다.

플라스틱 병 산업 개요

플라스틱 병 시장은 부문화되어 있으며 여러 대형 기업으로 구성되어 있습니다. 시장 점유율 측면에서 현재 소수의 대기업이 시장을 독점하고 있습니다. 시장에서 압도적인 점유율을 가진 이들 기업은 해외에서 고객 기반의 확대에 주력하고 있습니다. 이러한 기업들은 시장 점유율과 수익성을 높이기 위해 전략적 공동 이니셔티브를 활용합니다. 최근 시장 개척 동향을 몇 가지 발표합니다.

2024년 5월, 플라스틱 포장의 주요 기업인 ALPLA는 폴리에틸렌 테레프탈레이트(PET)로 만든 재활용 가능한 새로운 와인 병을 발표했습니다. 이 혁신적인 포장은 이산화탄소 배출량을 50% 줄이고 최대 30%의 비용 절감을 가능하게 합니다. 현재 750ml 사이즈와 1리터 사이즈의 병이 오스트리아의 와인 생산자 Wegenstein에 채용되고 있으며, 파일럿 고객이자 공동 개발 파트너로 표시합니다.

2023년 8월 Berry Global은 새로운 지속 가능한 럭셔리 브랜드를 위한 혁신적인 rPET 병을 발표했습니다. 재생 플라스틱의 기술력과 풍부한 경험을 살려 NEUE Water의 창업자 마이클 로어즈의 독창적인 디자인 비전을 실현했습니다. 기존과 다른 납작한 모양은 페트병에 사용되는 전통적인 사출 연신 블로우 성형(ISBM) 공정에 문제를 일으켰습니다. 그러나 Berry는 이 참신한 디자인을 원활하게 통합하기 위해 기술을 능숙하게 개선했습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업 간 경쟁 관계의 강도

산업 밸류체인 분석

제5장 시장 역학

시장 성장 촉진요인

재활용 확대와 비용 효율적인 대처

음료 산업에서의 수요 증가

시장의 과제

플라스틱 사용에 관한 환경에 대한 우려

무역 시나리오

EXIM 데이터

무역 분석(수출입 주요 5개국)

산업의 규제와 시책, 규격

기술 상황

가격 동향 분석

플라스틱 수지(현재 가격과 과거 동향)

제6장 시장 세분화

수지별

폴리에틸렌(PE)

폴리에틸렌테레프탈레이트(PET)

폴리프로필렌(PP)

기타 수지(폴리스티렌, PVC, 폴리카보네이트 등)

최종 사용자 산업별

식품

음료

병이 들어간 식수

탄산음료

알코올 음료

주스와 에너지 음료

기타 음료

의약품

퍼스널케어와 세면 용품

산업용

가정용 화학제품

페인트

기타

지역별

북미

미국

캐나다

유럽

프랑스

독일

이탈리아

영국

스페인

폴란드

북유럽

아시아태평양

중국

인도

일본

태국

호주 및 뉴질랜드

인도네시아

베트남

라틴아메리카

브라질

멕시코

콜롬비아

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

이집트

남아프리카

나이지리아

모로코

제7장 경쟁 구도

기업 프로파일

Amcor Group GmbH

ALPLA Group

Silgan Holdings Inc.

Berry Global Inc.

CKS Packaging Inc.

Comar LLC

Alpack Plastic Packaging

Cospack America Corporation

Resilux NV

Greiner Packaging

Altium Packaging

Plastikpak Holding Inc.

Container Corporation of Canada

Sailor Plastics Inc.

히트맵 분석

경쟁사 분석 - 신흥기업과 기존기업

제8장 재활용과 지속가능성의 전망

제9장 장래의 전망

KTH

영문 목차

영문목차

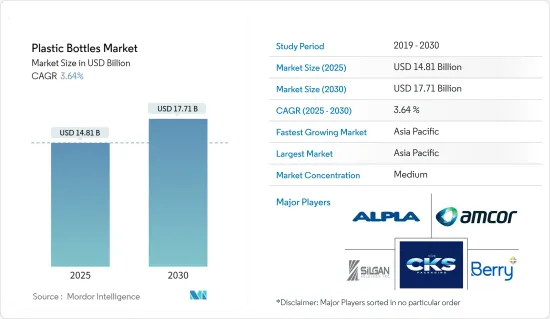

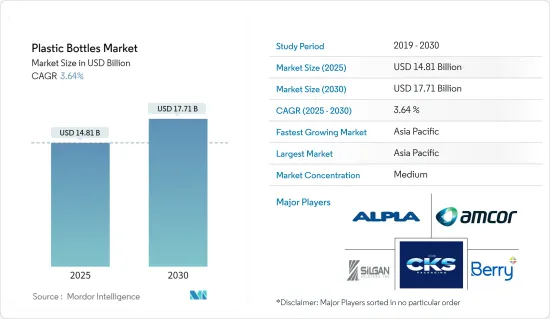

The Plastic Bottles Market size is estimated at USD 14.81 billion in 2025, and is expected to reach USD 17.71 billion by 2030, at a CAGR of 3.64% during the forecast period (2025-2030). In terms of production volume, the market is expected to grow from 15.92 billion tonnes in 2025 to 18.83 billion tonnes by 2030, at a CAGR of 3.42% during the forecast period (2025-2030).

Consumers globally increasingly favor plastic packaging due to its lightweight nature and ease of handling. Major manufacturers are gravitating toward plastic packaging solutions, primarily for their cost-effectiveness in production.

Key Highlights

Manufacturers widely favor plastic bottles crafted from materials like polyethylene terephthalate, polypropylene, and polyethylene. These materials are lightweight and unbreakable, enhancing the ease of handling. Additionally, manufacturers lean toward plastic packaging due to its cost-effectiveness. Given the rising reliance on packaged and processed foods and diverse beverages, the market for plastic bottles and containers is poised for growth during the forecast period.

PET has become a vital packaging material among bottle manufacturers across the region. Its versatility in accommodating different shapes and sizes has provided unparalleled alternatives to conventional glass and metal containers, making it a highly desirable choice in the packaging industry.

Key Highlights

According to a report by PETnology, a global packaging networking platform, in July 2023, Asia is expected to take the lead in global PET industry capacity expansions, driven by new construction and expansion initiatives set to take place after 2023.

Manufacturers prefer PET over other plastic packaging products, as it has a minimum loss of raw material during the manufacturing process compared to other plastic products. Its recyclability and the feature of adding multiple colors and designs augment it to become a preferred choice. Refillable products have emerged with rising consumer awareness of the environment and have acted to create demand for the product.

As consumers increasingly prioritize high-quality drinking water, driven by concerns over tainted tap water and the inherent convenience of portability, the demand for bottled water surges. This growing appetite for bottled water, alongside the rising popularity of non-alcoholic beverages, is set to propel the plastic bottle market within the beverage industry.

However, there is a growing inclination toward other packaging materials that offer environment-friendly properties. The consumption of aluminum cans and glass bottles has been witnessing high adoption rates in the region owing to its eco-friendly nature and high recyclability. Thus, consumers have been increasingly moving toward other materials from plastic.

Plastic Bottles Market Trends

The Beverages Segment is Expected to Drive the Market's Growth

The beverage segment is anticipated to witness growth, owing to the never-ending demand for bottled water and non-alcoholic beverages. The demand for bottled water is credited to consumers' propensity for specifically demanding high-quality drinking water, owing to the fear of diseases as an aftermath of drinking polluted tap water and the ease of portability and convenience provided by bottled water.

Further, in many developed and developing economies, people favor bottled water. Bottled water is sold in stores and places selling various drinks. For instance, the International Bottled Water Association (IBWA) stated that Americans favor bottled water over other packaged beverages.

According to Beverage Marketing Corporation data published in May 2023, in 2022, the United States bottled water sales reached 15.9 billion gallons, marking a consistent annual increase over the past decade. With the rise in bottled water volume sales in recent years, the demand for plastic bottles surged nationwide.

PET bottles are more prevalent in the water packaging market than glass and plastic bottles due to their durability and recyclability characteristics. The trend shows that lightweight, durable, and cost-effective PET is increasingly becoming the packaging medium of water.

The consumption of water bottles is an increasing trend across China and India with the growing population and changing lifestyle, creating demand for different formats of bottles that are lightweight, easy to carry, and can be stored and fulfill all the regulation terms to cater to changing consumer trends toward sustainability.

Companies also innovate different formats of bottled water, which are new in the market, and provide opportunities for the companies to promote the bottle with unique strategies to create market buzz.

For instance, in India, Wahter introduced ISI-certified bottled water in December 2023, which can be branded by advertisers at the lowest cost, leveraging 80% of branding space where advertisers can set up an account for their brand, upload their design, and link it to the template of the label advertisers to tailor their marketing strategies to their target audience.

Asia-Pacific is Expected to Witness the Highest Growth

One of the main initiatives across multiple countries in Asia-Pacific has generally been to cut down the usage of single-use plastic bottles and packaging. Companies might likely resort to plastic packaging to combat the pandemic's spread, putting the sustainability aspect away at this time.The healthcare and pharmaceutical sectors in China, India, and Japan are the world's largest markets, primarily driven by the aging population.

According to the Organisation of Pharmaceutical Producers of India, the country's pharmaceutical market is expected to reach USD 450 billion by 2047, which is up from USD 49 billion in 2022. Hence, there is a possibility for growth for domestic players as they might experience an increase in demand for plastic bottles from these companies. The Indian plastic bottle market is estimated to grow steadily, owing to the continually increasing consumption and industrial applications of plastic-made bottles.

Further, India is also one of the strong markets in the region with the highest population, and with a developing and trending outlook, there is a significant increase in the consumption of bottled water. Indian Railway Catering and Tourism Corporation Limited has launched a pet bottled water brand, "Rail Neer," which is majorly sold on trains and railway stations; with the rising consumption of water bottles and the growing railway sector, the corporation increased the production of the bottles in 2021 with 75.30 bottles produced which increased to 357.70 million bottles in 2023.

PET bottles are more energy efficient than glass bottles while delivering 1000 gallons of soft drinks and contribute less solid waste by weight than glass and aluminum containers. Thus, companies are shifting to PET format for carbonated beverages and innovating bottles with recycled materials due to changing consumer preferences in the region.

For instance, in Hong Kong, as part of its efforts to reduce its environmental footprint, the Coca-Cola Company announced the launch of 500 ml bottles made entirely from recycled plastic for its flagship drink, Coke, in April 2024. The global beverage company announced

that all 500 ml bottles of Coca-Cola Original, Coca-Cola No Sugar, and Coca-Cola Plus in production in China have shifted to 100% recycled polyethylene terephthalate (rPET).

Plastic Bottles Industry Overview

The plastic bottles market is fragmented and consists of several major players. In terms of market share, few of the major players currently dominate the market. These players, with a prominent share of the market, are focusing on expanding their customer base across foreign countries. These companies are leveraging strategic collaborative initiatives to increase their market share and profitability. Some of the recent developments in the market are:

May 2024: ALPLA, a key firm in plastic packaging, unveiled a new recyclable wine bottle crafted from polyethylene terephthalate (PET). This innovative packaging slashes carbon footprints by as much as 50% and offers potential cost savings of up to 30%. Currently, bottles offered in 750 ml and one-liter sizes are being used by Austrian wine producer Wegenstein, marking them as both a pilot customer and a collaborative development partner.

August 2023: Berry Global unveiled an innovative rPET bottle for a new sustainable luxury brand. Leveraging its technical prowess and extensive experience with recycled plastics, Berry brought to life the original design vision of NEUE Water's founder, Michael Lowers. The unconventional flat shape posed challenges to the traditional injection stretch blow molding (ISBM) process used for PET bottles. However, Berry adeptly modified the technology to integrate the novel design seamlessly.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Recycling and Oher Cost-effective Initiatives are Bolstering the Demand

5.1.2 Increasing Demand from the Beverage Industry aids the Market

5.2 Market Challenges

5.2.1 Environmental Concerns Regarding the Use of Plastics