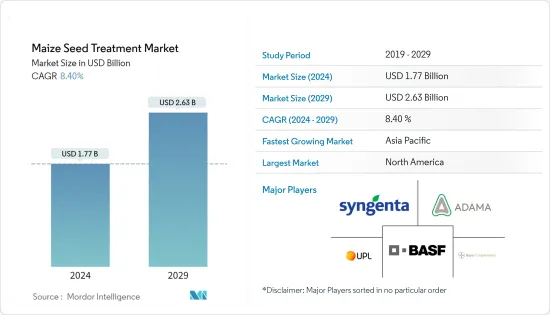

옥수수 종자 처리(Maize Seed Treatment) 시장 규모는 2024년에 17억 7,000만 달러로 추정되며, 2029년에는 26억 3,000만 달러에 이를 것으로 예측 되며, 예측 기간 중(2024-2029년) CAGR 8.40%로 추이하며 성장할 것으로 예상됩니다.

상업용 옥수수 잡종은 전 세계적으로 점점 더 인기를 얻고 있습니다. 전통적으로 북미, 유럽, 남미에서는 지난 20년 동안 상업용 옥수수 잡종을 재배해 왔습니다. 그러나 종자 교체율이 높아지고 잡종 재배가 증가하면서 아시아 태평양과 아프리카 등 개발도상국 시장이 괄목할 만한 성장을 이뤘습니다. 2018년 아시아 태평양 지역의 종자 교체율은 80%에 육박했습니다. 잡종 품종의 채택이 증가하고 유전자 변형 품종을 포함한 첨단 잡종이 보급되면서 옥수수 종자 처리 제품의 상업적 응용 시장이 호황을 누리고 있습니다. 이러한 제품은 종자 회사를 대상으로 B2B 수준으로 판매되고 있습니다. 옥수수 잡종을 판매하는 종자 회사의 수가 증가하면서 옥수수 종자 처리 제품의 상업적 응용 시장도 성장하고 있습니다. 잡종화와 종자 교체율 증가의 다음 개척지는 아프리카로, 예측 기간 동안 관련 지표가 견고한 속도로 증가할 것으로 예상됩니다.

옥수수는 북미에서 약 3,500만 헥타르에 걸쳐 재배됩니다. 옥수수는 이 지역에서 가장 중요한 곡물 작물로 곡물, 동물 사료 및 사료로 광범위하게 사용되고 있습니다. 이 지역에서 유전자 변형 및 잡종 종자의 채택이 증가함에 따라 전 세계 모든 지역 중 가장 큰 규모를 차지하고 있습니다. 이 시장은 기업들이 토양과 환경의 지속가능성을 염두에 두고 농부의 작물 보호 요구를 충족하는 제품을 출시하는 상업용 애플리케이션에 의해 주도되고 있습니다. 이 지역은 예측 기간 동안 옥수수 종자 처리 시장에서 가장 큰 지리적 부문를 유지할 것으로 예상됩니다.

옥수수 종자 처리 시장은 고도로 통합되어 있으며 상위 글로벌 플레이어가 시장 점유율의 70 % 이상을 차지하고 있습니다. 이러한 플레이어의 더 큰 시장 점유율은 고도로 다각화 된 제품 포트폴리오와 수많은 인수 및 계약에 기인 할 수 있습니다. 또한 이러한 업체들은 R&D, 제품 포트폴리오 확장, 광범위한 지리적 입지, 공격적인 인수 전략에 집중하고 있습니다. 이 시장의 주요 기업으로는 BASF SE, Syngenta AG, Adama Agricultural Solutions, UPL Limited, Bayer Crop Science 등이 있습니다.

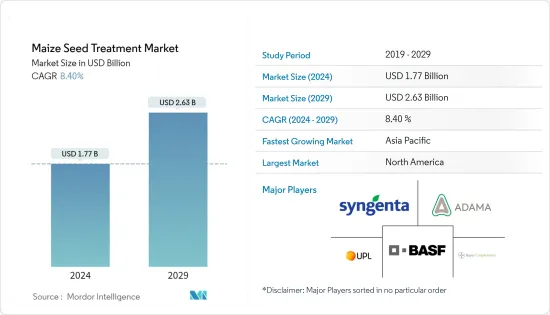

The Maize Seed Treatment Market size is estimated at USD 1.77 billion in 2024, and is expected to reach USD 2.63 billion by 2029, growing at a CAGR of 8.40% during the forecast period (2024-2029).

Commercial maize hybrids are increasingly becoming popular across the world. Traditionally, North America, Europe, and South America have been cultivating commercial maize hybrids, since last two decades. However, increasing seed replacement rates and rising adoption of hybrids led to a remarkable growth of developing markets, such as Asia-Pacific and Africa. In 2018, seed replacement rates in Asia-Pacific stood at close to 80%. Increased adoption of hybrid varieties and penetration of advanced hybrids, including genetically modified varieties, have resulted in a booming market for commercial applications of maize seed treatment products. These products are being sold at a B2B level to seed companies. An increase in the number of seed companies selling maize hybrids has also supported the market for commercial applications of maize seed treatment products. The next frontier of hybridization and increased seed replacement rates is Africa, where the metrics related to these are expected to increase at a robust pace over the forecast period.

Maize is grown over approximately 35 million hectares in North America. It is the most important grain crop in the region, with extensive application as grain, animal feed, and forage. Increased adoption of genetically modified and hybrid seeds in the region makes the geographical segment the largest among all the regions across the world. The market is driven by commercial applications, where companies are launching products that satisfy the crop protection needs of the farmer, while keeping sustainability of the soil and environment in mind. The region is expected to remain the largest geographical segment in the maize seed treatment market over the forecast period.

The maize seed treatment market is highly consolidated, with the top global players occupying more than 70% of the market share. The greater market shares of these players can be attributed to highly diversified product portfolio and numerous acquisitions and agreements. Moreover, these players are focusing on R&D, expansion of product portfolio, wide geographical presence, and aggressive acquisition strategies. Some of the key players in the market include BASF SE, Syngenta AG, Adama Agricultural Solutions, UPL Limited, and Bayer Crop Science, among others.