세계 HVAC 필드 디바이스 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

HVAC Field Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1431294

리서치사:Mordor Intelligence

발행일:2024년 02월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

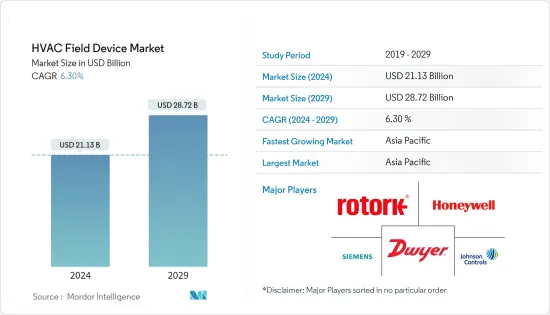

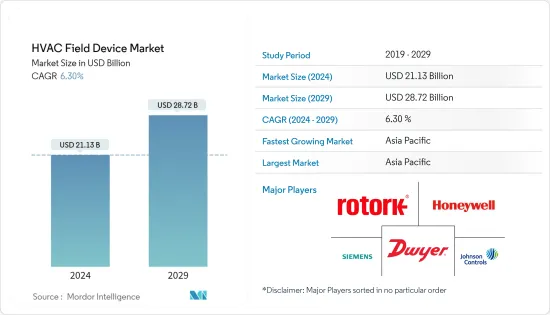

세계 HVAC 필드 디바이스 시장 규모는 2024년에 211억 3,000만 달러에 달하고, 2024-2029년의 예측 기간 동안 CAGR 6.30%로 성장하고, 2029년에는 287억 2,000만 달러에 도달할 것으로 예측됩니다.

팬데믹은 HVAC 산업에 큰 영향을 미쳤으며 초기 몇 개월 동안 폐쇄 제한과 기업이 새로운 설비 투자를 앞두고 시스템 수요가 크게 감소했습니다. 전염병 때문에 세계 많은 건설 프로젝트가 중단되었습니다. 상업, 주택 및 산업 건설 활동의 감소는 HVAC 필드 장치 수요를 일시적으로 퇴각시켰습니다.

주요 하이라이트

그 결과 미국 정부는 공공시설, 학교 및 기타 환경에서 실내 공기의 질을 개선하는 데 사용할 수 있는 연방 자금을 크게 투자했습니다. 예를 들어, American Rescue Plan은 환기 및 여과 업그레이드에 사용할 수 있는 3,500억 달러를 주 및 지방 정부에, 1,220억 달러를 학교에 제공했습니다.

최종 사용자는 실제로 문제가 발생하기 전에 유지 보수가 필요한 시기를 예측하기 위해 스마트 HVAC 장치를 사용합니다. 사물인터넷(IoT) 시스템을 활용하는 최신 HVAC 기술은 센서, 소프트웨어 및 연결성을 통합하여 HVAC 시스템이 다른 연결 장치와 데이터를 교환할 수 있도록 합니다. IoT 시스템은 공기 품질과 장치 상태에 대한 데이터를 감지하여 예방 유지보수를 강화합니다. 또한, 최신의 가장 저렴한 가격의 인터넷 HVAC 기술로 옥상 에어 핸들링 유닛, 공냉/수냉 히트 펌프, 재열 시스템이 있는 가변 풍량(VAV) 등 여러 디바이스 유형에 걸친 통찰의 열람이 대폭 용이하게 됩니다. HVAC 디바이스에서의 이러한 개척은 조사된 시장을 더욱 촉진할 것으로 예상됩니다.

특히 신흥경제국에서는 가처분소득 증가와 함께 소비자의 구매력이 상승하고 있는 것도 시장에 긍정적인 영향을 미치고 있습니다. 예를 들어 중국국가통계국에 따르면 중국 주민 1인당 평균가처분소득은 36,883위안으로 2022년 인플레이션 조정 후 명목소득은 전년대비 5.0% 증가, 절대소득은 2.9% 증가했습니다.

이 외에도 제조 부문의 상승은 HVAC 및 필드 디바이스의 범위를 더욱 강화하고 있습니다. 유엔공업개발기관의 세계제조업생산 3분기 보고서(2022년)에 따르면 아시아·오세아니아의 제조업생산은 4.4%의 성장을 보였으며 북미(3.5%)와 유럽(1.7%)을 웃돌았습니다. 했습니다. 라틴아메리카와 카리브해 국가의 제조업은 4.9% 성장했고 남미는 3.0% 성장했습니다.

또한 동유럽은 추운 기후 조건에 있으며 체코 공화국, 폴란드, 불가리아 등에서는 난방 솔루션에 대한 수요가 큽니다. 이 지역의 기타 국가들과 마찬가지로 냉난방 부문의 에너지 효율을 높이기위한 대책이 높아지고 있습니다. Stratego를 공동 설립한 EU의 Intelligent Energy Europe Programme은 2010년부터 2050년 사이에 500억 유로를 투자하면 에너지 시스템 비용을 낮출 수 있는 충분한 연료를 절약할 수 있다고 주장합니다. 이 투자의 일부로 지역 난방 점유율은 50억 유로, 개별 히트 펌프는 150억 유로입니다.

세계의 일부 정부는 주택 및 상업 공간에서 에너지 절약 시설의 사용을 촉진하기 위해 재정적인 이점을 제공합니다. 예를 들어, 미국 정부는 2005년 에너지 정책법을 도입했으며, 신축 상업용 건물에 평방 피트당 최대 1.80달러의 세금 공제를 제공합니다. American Society of Heating, Refrigerating, and Air-Conditioning Engineers, Inc.의 정부 이니셔티브와 환경 악화 및 에너지 관리에 대한 의식이 높아짐에 따라, 필드 디바이스를 포함한 에너지 효율적인 HVAC 제어 시스템 수요가 유지되면 예상됩니다.

HVAC 필드 디바이스 시장 동향

주택부문이 큰 시장 점유율을 차지할 전망

HVAC 필드 디바이스 시장을 홍보하는 주요 요인 중 하나는 주택 빌딩에서 에너지 소비의 비율이 증가하고 있는데, 이는 빌딩의 효율성을 높이기 위한 에너지 보수 시스템의 이용으로 이어지고 있습니다. 예를 들어 HomeServe는 2022년 8월에 가정용 HVAC 구독 혜택 프로그램을 도입했습니다. 이것은 가정에 고가의 HVAC(냉난방 공기 조화) 시스템의 교체 비용을 낮추어 전력 회사가 에너지 효율 목표를 달성하고 고객 만족도를 향상시키는 데 도움이 됩니다.

에어컨 수요의 확대는 이 분야 시장을 견인하는 가장 중요한 요인 중 하나입니다. 중앙 에어컨은 세계 사람들이 집을 식히는 가장 일반적인 방법이 될 것으로 예상됩니다. IEA에 따르면 에어컨과 선풍기는 세계 빌딩의 총 전력 소비량의 약 5분의 1, 즉 전 세계 전력 소비량의 10%를 차지한다고 합니다. 향후 30년간 에어컨의 사용이 급증하고 세계 전력 수요의 최고 촉진요인 중 하나가 될 것으로 예상되고 있습니다.

또한, 주거 부문에서 HVAC 필드 디바이스 시장의 확대를 뒷받침하는 주요 요인 중 하나는 실내 공기의 질에 대한 관심 증가입니다. 또한 일부 정부는 에너지 수요를 충족하는 법률을 시행하고 이러한 에어컨을 할인 가격으로 판매하는 프로그램을 구현함으로써이 고효율 장치를 구입할 것을 권장합니다. 예를 들어, 에너지 절약국(BEE)과 전력부는 에너지 효율적인 시스템을 지지하는 에너지 표시 프로그램을 일상적으로 상향 조정함으로써 주택용 에어컨의 소비 전력량에 관한 규칙을 실시했습니다.

OBERLO에 따르면 2023년에는 미국의 6,040만 가구가 스마트 홈 디바이스를 적극 활용할 것으로 예상되며, 이는 5,740만 가구가 스마트 홈 디바이스를 이용한 2022년보다 3% 증가했습니다. 2023년에는 스마트홈 기술을 이용하는 가구의 비율은 전 가구의 46.5%가 될 것으로 예상됩니다. 이 보급은 HVAC 시스템을 포함한 에너지 소비가 적은 스마트 장치에 대한 수요가 증가할 것으로 보입니다.

CO2 배출량을 줄이기 위해 벤더와 많은 정부도 주택의 탈탄소화에 주력하고 있습니다. 그 결과, 주택분야에서의 히트펌프의 채용이 촉진되어, 주택 소유자의 광열비 절감을 지원하고, 세계의 기후 변화의 원인이 되는 화석연료의 사용삭감을 촉진할 것으로 예상됩니다. Carrier, Daikin, Johnson Controls 및 Danfoss와 같은 주요 공급업체는 주거용 제품 출시에 지속적으로 투자하고 있으며, 이는 시장을 견인하는 주요 요인 중 하나입니다.

아시아태평양이 큰 시장 점유율을 차지할 전망

중국 건설산업은 지속가능한 건설정책과 지난 수년간 서비스 주도형 경제로의 전환으로 대규모 성장을 목격해 왔습니다. 대규모 인프라 프로젝트에 대한 투자는 성장을 가속하는 중국 정부의 전략의 중요한 부분이 되었습니다.

중국건설업협회에 따르면 2021년 중국의 완성된 건설물 중 주택건축이 큰 비율을 차지했습니다. 주택용 건축물은 완성층 면적의 67% 이상을 차지하고 있습니다. 이 나라의 경제 성장에 따라 사람들은 농촌에서 대도시로 이주하여 이러한 장소에서 주택 수요가 증가하고 있습니다. 또한 투자 부동산으로 이용되는 아파트가 수요를 끌어 올리고 있습니다. 이러한 대규모 주택건설은 조사시장을 견인할 것으로 예상됩니다.

국토교통성에 따르면 2022년 일본의 주택착공건수는 약 859.5천건이었습니다. 전년 대비 0.4% 증가했습니다. 2022년 일본에서 착공된 오피스 빌딩의 착공 건수는 10,200건을 넘습니다. 이러한 엄청난 수의 건설이 조사 대상 시장을 견인한다고 생각됩니다.

또한 IBEF에 따르면 인도는 작년 1년간 부동산 자산에 24억 달러를 투자했으며, 이는 매년 52% 증가했습니다. 2000년 4월부터 2022년 9월까지 건설 및 운영을 포함한 이 산업에 대한 직접 투자는 총 551억 8,000만 달러에 달했습니다. 이러한 부동산의 상당한 증가는 조사된 시장의 성장을 가능하게 하는 것으로 보입니다.

게다가 한국에서는 새로운 데이터센터 건설 프로젝트도 시장 성장을 가속하고 있습니다. 예를 들어 SK Telecom의 인터넷 인프라 부문인 SK Broadband는 최근 신흥기업 캠퍼스를 둘러싼 완전히 새로운 하이퍼스케일 데이터센터 건설에 17억 5,000만 달러를 투자할 계획을 발표했습니다. 데이터센터와 스타트업 클러스터 개발의 제1단계는 2024년까지 완성되어 4동의 데이터센터 빌딩으로 구성될 예정이며, 2029년까지 추가로 12동을 추가할 계획입니다.

HVAC 필드 디바이스 산업 개요

세계의 HVAC 필드 디바이스 시장은 매우 단편화되어 있으며 여러 선도 기업이 존재합니다. 시장 점유율 측면에서 현재 여러 회사의 대기업이 시장을 독점하고 있습니다. 시장에서 돌출한 점유율을 가진 이 대기업은 해외에서 고객 기반의 확대에 주력하고 있습니다. 이러한 기업들은 시장 점유율과 수익성을 높이기 위해 전략적 공동 이니셔티브를 활용합니다.

2023년 3월, Honeywell은 펌프, 모터, 컴프레서, 팬, 송풍기, 기어박스 등 회전 장치의 상태 기반 모니터링을 위한 Versatilis 송신기를 발표했습니다. Honeywell의 Versatilis 송신기는 회전 장치의 적절한 측정을 제공하고 산업 전반의 안전성, 가용성 및 신뢰성을 향상시키는 인텔리전스를 제공합니다.

2022년 8월 Airzone은 HVAC 인버터 시스템을 위한 독자적인 스마트 제어 솔루션으로 급성장하는 북미 시장에 진입할 것이라고 발표했습니다. Airzone의 Aidoo Pro는 인기 있는 Ecobee, Honeywell, Nest 스마트 서모스탯을 비롯한 독자적인 HVAC 인버터와 미니 스플릿 제조업체의 프로토콜과 IoT 디바이스 API의 브릿지를 제공했습니다. Aidoo Pro는 HVAC 전문가가 HVAC 인버터 시스템을 주요 스마트 서모스탯과 통합하여 모든 인버터 기능을 유지하며 타의 추종을 불허하는 효율성, 에너지 절약, 연결성 및 편안함을 제공합니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업 밸류체인 분석

산업의 매력도 - Porter's Five Forces 분석

구매자의 협상력

공급기업의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

산업에 있어서의 COVID-19의 영향 평가

제5장 시장 역학

시장 성장 촉진요인

건설시장 개척

세액공제제도에 의한 에너지절약 장려를 포함한 정부의 지원적 규제

대체를 지원하는 IoT와 제품 혁신의 출현

시장 성장 억제요인

거시 경제 상황에 대한 의존

에너지 효율이 높은 시스템의 초기 비용 높이

제6장 시장 세분화

유형별

컨트롤 밸브

밸런싱 밸브

PICV

댐퍼 HVAC

댐퍼 액추에이터 HVAC

기타 유형

센서별

환경 센서

멀티 센서

공기 품질 센서

가동률 및 조명

기타 센서

최종 사용자 산업별

상업

주택

공업

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

Siemens AG

Honeywell International Inc.

Johnson Controls International PLC

Rotork Plc

Dwyer Instruments Inc.

Belimo Holding AG

Robert Bosch GmbH

Electrolux AB

Azbil Corporation

Danfoss A/S

Daikin Industries Ltd.

제8장 투자 분석

제9장 시장 전망

JHS

영문 목차

영문목차

The HVAC Field Device Market size is estimated at USD 21.13 billion in 2024, and is expected to reach USD 28.72 billion by 2029, growing at a CAGR of 6.30% during the forecast period (2024-2029).

The pandemic significantly influenced the HVAC industry, as demand for the systems observed a significant drop during the initial months, owing to lockdown restrictions and businesses refraining from investing in new equipment. Due to the pandemic, many construction projects were halted across the world. Reduced commercial, residential, and industrial construction activities temporarily dampened the demand for HVAC field devices.

Key Highlights

Consequently, the US government has significantly invested in federal funds that can be used in public buildings, schools, and other settings to improve indoor air quality. For instance, the American Rescue Plan provided USD 350 billion for state and local governments, along with USD 122 billion for schools, that can be used for ventilation and filtration upgrades.

The end users are adopting smart HVAC equipment to predict when maintenance is needed before a real issue occurs. The latest HVAC technologies, which utilize an Internet of Things (IoT) system, are embedded with sensors, software, and connectivity, enabling the HVAC system to exchange data with other connected devices. IoT systems enhance preventative maintenance by sensing data on air quality and equipment status. Moreover, the latest and most affordable Internet of Things HVAC technology makes it significantly easier to view insights across several equipment types, such as rooftop air-handling units, air- and water-cooled heat pumps, variable air volume (VAV) with reheat systems, etc. These developments in HVAC equipment are expected to further drive the studied market.

Rising consumer purchasing power coupled with increasing disposable income, especially in developing economies, also positively impacts the market. For instance, according to the National Bureau of Statistics of China, the average disposable income per capita for residents in China was 36,883 yuan, a nominal increase of 5.0% compared to the previous year and an absolute increase of 2.9% after adjusting for inflation in 2022.

In addition to this, the rising manufacturing sector has further bolstered the scope of HVAC equipment and field devices. According to the World Manufacturing Production Quarter 3 2022 Report by the United Nations Industrial Development Organization, manufacturing production in Asia and Oceania experienced an output growth of 4.4%, ahead of North America (3.5%) and Europe (1.7%). The manufacturing sector in Latin America and the Caribbean expanded by 4.9%, and South Africa grew by 3.0%.

Furthermore, Eastern Europe has colder climatic conditions, and the demand for heating solutions is significant in these countries, such as the Czech Republic, Poland, Bulgaria, and others. Like other countries in the region, measures to increase energy efficiency in the heating and cooling sectors are rising. The Intelligent Energy Europe Programme of the EU, which co-founded Stratego, claims that an investment of EUR 50 billion between 2010 and 2050 will save enough fuel to lower the costs of the energy system. As part of this investment, district heating's share stood at EUR 5 billion and individual heat pumps at EUR 15 billion.

Several governments worldwide are offering financial benefits to promote the use of energy-saving equipment in residential and commercial spaces. For instance, the U.S. government introduced the Energy Policy Act of 2005, which provides a tax deduction of up to USD 1.80 per square foot for new commercial buildings. Buildings that reduce their regulated energy consumption by 50% in comparison to the specifications outlined in the American Society of Heating, Refrigerating, and Air-Conditioning Engineers, Inc.'s 2001 new construction standard (ASHRAE 90.1) were eligible for the tax benefit. Government initiatives and rising awareness about environmental degradation and energy management are expected to keep the demand for energy-efficient HVAC control systems, including field devices.

HVAC Field Device Market Trends

Residential Sector is Expected to Hold Significant Market Share

One of the key drivers propelling the market for HVAC field devices is the growing percentage of energy consumption in residential buildings, which has led to the usage of energy retrofit systems to increase the efficiency of buildings. For instance, HomeServe introduced its benefits program for home HVAC subscriptions in August 2022. This helps utilities accomplish energy efficiency goals and improve customer satisfaction by lowering the cost of replacing an HVAC (heating and air conditioning) system, which is expensive for households.

Growing demand for air conditioners has been one of the most critical factors driving the market in this sector. Central air conditioning is expected to become the most common way people across the globe cool their homes. According to the IEA, air conditioners and electric fans account for about a fifth of the total electricity in buildings worldwide, or 10% of all global electricity consumption. Over the next three decades, the use of ACs is set to soar, becoming one of the top drivers of global electricity demand.

Furthermore, one of the key factors propelling the expansion of the HVAC field device market in the residential sector is the rising concern for indoor air quality. Also, several governments are encouraging the purchase of this high-efficiency equipment by enforcing laws to satisfy energy demand and implementing sales programs for these air conditioners at discounted prices. By routinely making upward changes to the Energy Labeling Program in favor of energy-efficient systems, the Bureau of Energy Efficiency (BEE) and the Ministry of Electricity, for instance, have been enforcing rules on the amount of electricity consumed by residential air conditioners.

According to OBERLO, 60.4 million US homes were expected to be actively utilizing smart home devices in 2023, which was 3% more than in 2022, when 57.4 million households used smart home devices. In 2023, the proportion of households utilizing smart home technology is expected to be 46.5% of all households. This penetration is likely to lead to an increase in demand for smart devices with low energy consumption, including HVAC systems.

To reduce CO2 emissions, vendors and numerous governments are also focused on residential decarbonization. As a result, it is anticipated that the adoption of heat pumps in the residential sector will gain traction, which will aid homeowners in reducing their utility costs and promote a decrease in the use of fossil fuels, which feed global climate change. Major vendors like Carrier, Daikin, Johnson Controls, Danfoss, and others are constantly investing in residential product launches, which is one of the major factors driving the market.

Asia-Pacific is Expected to Hold Significant Market Share

The construction industry in China has witnessed massive growth due to sustainable construction policies and a shift toward a service-led economy over the past few years. Investing in large-scale infrastructure projects has been a vital part of the Chinese government's strategy to boost growth.

According to the China Construction Industry Association, in 2021, residential structures accounted for a significant share of finished construction in China. Buildings intended for housing accounted for over 67% of the completed floor space. As the country's economy grows, people migrate from rural areas to major cities, increasing demand for residential accommodation in these locations. Furthermore, apartments utilized as investment properties drive up demand. Such massive residential construction is expected to drive the study market.

According to MLIT (Japan), there were about 859.5 thousand home starts in Japan in 2022. Compared to the prior year, this represented an increase of 0.4%. Over 10,200 office building construction projects began in Japan in 2022. Such a vast number of constructions would drive the studied market.

Further, according to IBEF, India invested USD 2.4 billion in real estate assets over the last year, a 52% increase annually. From April 2000 to September 2022, FDI in the industry, comprising construction development and operations, totaled USD 55.18 billion. Such a massive rise in real estate would allow the studied market to grow.

Further, the new data center construction projects in the country are also pushing the market's growth in South Korea. For instance, SK Broadband, the internet infrastructure division of SK Telecom, recently announced plans to invest USD 1.75 billion in the creation of a brand-new hyperscale data center encircling a startup campus. The first phase of the data center and startup cluster development is expected to be completed by 2024 and comprise four data center buildings, with plans to add 12 more by 2029.

HVAC Field Device Industry Overview

The global HVAC field device market is highly fragmented and has several major players. In terms of market share, a few of the major players currently dominate the market. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

In March 2023, Honeywell introduced its Versatilis transmitters for condition-based monitoring of rotating equipment such as pumps, motors, compressors, fans, blowers, and gearboxes. Honeywell Versatilis transmitters provide relevant measurements of rotating equipment, delivering intelligence that can improve safety, availability, and reliability across industries.

In August 2022, Airzone announced it was entering the rapidly growing North American market with an exclusive smart control solution for HVAC inverter systems. Airzone's Aidoo Pro acted as the bridge between proprietary HVAC inverter and mini-split manufacturers' protocols and IoT device APIs, including for the popular Ecobee, Honeywell, and Nest smart thermostats. The Aidoo Pro enables HVAC professionals to integrate HVAC inverter systems with leading smart thermostats, preserving all inverter features and providing unparalleled efficiency, energy savings, connectivity, and comfort.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Buyers

4.3.2 Bargaining Power of Suppliers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Development of the Construction Market

5.1.2 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

5.1.3 The Emergence of IoT and Product Innovations to Aid Replacements

5.2 Market Restraints

5.2.1 Dependence on Macro-economic Conditions

5.2.2 High Initial Cost of Energy Efficient Systems