방사선 AI 시장 예측(-2030년) : 제공 형태(온 디바이스, SaaS), 기능(트리아지, 워크플로우, 임상의사결정지원시스템, 영상 취득, 영상 처리, 리포트 작성), 모달리티(CT, MRI, X선), 적응증(종양, 심장혈관, 신경), 최종사용자(병원, 영상 진단 센터), 지역별

Radiology AI Market by Offering (On-Device, SaaS), Function (Triage, Workflow, CDSS, Acquisition, Processing, Reporting), Modality (CT, MRI, X-ray), Indication (Onco, Cardio, Neuro), End User (Hospital, Imaging Center), Region - Global Forecast to 2030

상품코드:1942448

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 347 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

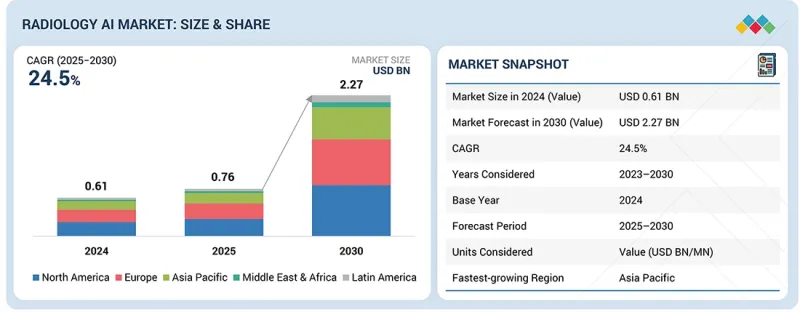

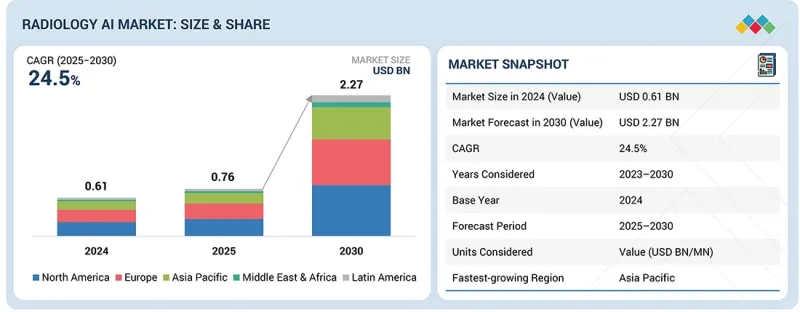

방사선 AI 시장 규모는 2025년 7억 6,000만 달러에서 2030년까지 22억 7,000만 달러에 달할 것으로 예측되고 있으며, CAGR은 24.5%로 전망되고 있습니다.

이러한 성장은 암의 조기 발견, 병변 세분화, 예측 치료 계획 수립을 위한 AI 기반 진단 툴의 도입 확대에 힘입어 진단 정확도를 높이고 영상의학과 의사의 업무 부담을 줄여주는 역할을 하고 있습니다.

조사 범위

조사 대상 기간

2024-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

금액(달러)

부문

제공 형태, 기능, 모달리티, 적응증, 최종사용자

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

종양, 신경영상, 심혈관 영상 진단 분야로의 확대 적용으로 실시간 인사이트, 개인화된 진단, 워크플로우 최적화를 실현할 수 있는 지능형 AI 플랫폼에 대한 수요가 크게 증가하면서 의료 기술 분야에서 고부가가치 기회를 창출하고 있습니다. 고부가가치 기회가 창출되고 있습니다.

"예측 기간 중 워크플로우 최적화 부문이 큰 시장 점유율을 차지할 것으로 예측됩니다. "

기능별로는 스크리닝&트리아지, 진단영상/판독(영상 획득, 재구성/강조, 영상처리, 분석/감지, 임상 의사결정 지원, 기타), 치료계획/중재지원(용량계획/최적화, 수술계획/지도, 영상기반 세분화/해부학적 모델링, 기타), 모니터링&추적, 보고서 작성&문서화, 워크플로우 최적화, 연구/개발, 기타로 구분됩니다. 모니터링&추적, 보고서 작성&문서화, 워크플로우 최적화, 연구개발, 기타로 분류됩니다. 워크플로우 최적화는 영상 부문 전반에 걸쳐 강력한 경제적, 운영적 영향력을 바탕으로 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 전 세계에서 영상의학과 전문의가 부족하고 영상 검사량이 증가함에 따라 의료기관에서는 지능형 작업 리스트 조정 및 자동화된 케이스 라우팅, 실시간 모달리티 활용, 처리 시간 단축을 통해 생산성을 향상시키는 AI를 우선적으로 도입하고 있습니다. 이러한 솔루션은 기술자와 영상의학과 의사 간의 커뮤니케이션을 효율화하고, 재검사의 필요성을 줄이며, 프로토콜의 표준화를 촉진하고, 수작업으로 인한 관리 업무를 제거할 수 있도록 지원합니다. 병원이 가치 기반 의료로 전환하는 과정에서 워크플로우 AI는 비용 절감, 환자 처리 속도 향상, 환자 경험 개선에 직접적인 도움을 주기 때문에 예측 기간 중 중요한 투자 영역이 될 것입니다.

"소프트웨어/SaaS 부문이 2025년 기준 가장 큰 점유율을 차지할 것으로 전망"

제공 형태별로는 소프트웨어/SaaS 솔루션 부문이 2025년 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 주요한 이유는 여러 영상 진단 양식에 걸쳐 도입, 업데이트 및 확장이 용이하다는 점입니다. 이 플랫폼은 기존 영상정보관리시스템(PACS), 방사선정보시스템(RIS), 전자건강기록(EHR) 시스템과 원활하게 연동되어 방사선과 전문의가 주요인프라 변경 없이도 일상적인 업무 흐름 내에서 직접 AI 지식에 접근할 수 있도록 지원합니다. 클라우드 기반 아키텍처는 접근성을 향상시키고, 모델의 지속적인 개선을 지원하며, 초기 자본 지출을 줄입니다.

또한 소프트웨어 벤더들은 구독 및 사용량 기반 가격 정책을 활용하여 도입 비용을 낮추면서 안정적이고 지속적인 매출을 창출하고 있습니다. 진단용 AI 툴에 대한 규제 당국의 승인 확대와 더불어 종양, 신경, 심장 분야에서의 강력한 이용 사례는 이 기술 시장 지배력을 더욱 가속화시키고 있습니다.

"북미가 2025년 큰 점유율을 보일 것"

북미는 의료 인프라에 대한 대규모 투자, 첨단 기술 도입, 영상 진단 서비스에 대한 높은 수요에 힘입어 2025년 시장에서 큰 비중을 차지할 것으로 예측됩니다. 특히 미국에서는 디지털 헬스 도입에 대한 연방 정부의 인센티브와 AI 진단 툴에 대한 규제 승인을 배경으로 영상의학과 워크플로우에 AI 통합이 광범위하게 진행되고 있습니다. 또한 암, 심혈관질환, 신경질환 등 만성질환 증가와 함께 고급 영상 진단 솔루션에 대한 수요가 증가하고 있으며, 영상 분석, 분류, 워크플로우 최적화를 위한 AI 알고리즘 도입이 촉진되고 있습니다.

또한 민간 및 공공 부문의 견고한 투자와 더불어 AI 스타트업 및 기존 기술 기업의 높은 집중도는 북미 시장에서의 리더십을 더욱 강화하고 있습니다.

그러나 HIPAA에 따른 데이터 프라이버시 우려와 임상의들이 AI 툴의 완전한 도입에 대한 망설임 등의 과제는 여전히 남아있습니다. 이러한 장벽에도 불구하고 첨단 의료 인프라, 유리한 의료비 상환 정책, 높은 R&D 투자, 혁신적인 AI 기술의 조기 도입 등의 요소가 결합되어 이 지역은 세계 방사선 AI 시장을 선도하고 있습니다.

세계의 방사선 AI 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 방사선 AI 시장 : 제공 형태별

제10장 방사선 AI 시장 : 기능별

제11장 방사선 AI 시장 : 모달리티별

제12장 방사선 AI 시장 : 적응증별

제13장 방사선 AI 시장 : 최종사용자별

제14장 방사선 AI 시장 : 지역별

제15장 경쟁 구도

제16장 조사 방법

제17장 부록

KSA

영문 목차

영문목차

The radiology AI market is projected to reach USD 2.27 billion by 2030 from USD 0.76 billion in 2025, at a CAGR of 24.5%. The growth is fueled by the increasing adoption of AI-driven diagnostic tools for early cancer detection, lesion segmentation, and predictive treatment planning, which enhance diagnostic accuracy and reduce radiologist workload.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Offering, Function, Modality, Indication, and End User

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

The expanding application of these solutions in oncology, neuroimaging, and cardiovascular imaging is significantly boosting demand for intelligent AI platforms capable of delivering real-time insights, personalized diagnostics, and workflow optimization, creating a high-value opportunity in the healthcare technology landscape.

The workflow optimization segment is expected to witness significant market share during the forecast period.

Based on the function, the radiology AI market is segmented into screening & triage, diagnostic imaging & interpretation (image acquisition, reconstruction & enhancement, image processing, analysis & detection, clinical decision support, others), treatment planning & intervention support (dose planning & optimization, surgical planning & guidance, image-based segmentation & anatomical modeling, others), monitoring & follow-up, reporting & documentation, workflow optimization, research & clinical development, and others. Workflow optimization is projected to record the fastest CAGR in the radiology AI market, driven by its strong economic and operational impact across imaging departments. With global radiologist shortages and rising imaging volumes, health systems are prioritizing AI that enhances productivity through intelligent worklist orchestration and automated case routing, as well as real-time modality utilization and turnaround-time reduction. These solutions streamline communication between technologists and radiologists, reduce the need for repeat scans, facilitate protocol standardization, and help eliminate manual administrative tasks. As hospitals increasingly shift toward value-based care, workflow AI directly supports cost containment, faster patient throughput, and an improved patient experience, making it a key investment area over the forecast period.

The software/SaaS segment is expected to have the largest share in 2025 in the radiology AI market.

By offering, the software/SaaS solutions segment is expected to hold the largest market share in 2025, primarily because they are easier to deploy, update, and scale across multiple imaging modalities. These platforms seamlessly integrate with existing Picture Archiving and Communication Systems (PACS), Radiology Information Systems (RIS), and Electronic Health Record (EHR) systems, enabling radiologists to access AI insights directly within their routine workflows without requiring major infrastructure changes. Cloud-based architectures enhance accessibility, support continuous model improvement, and lower upfront capital expenditure.

Additionally, software vendors leverage subscription and usage-based pricing, making adoption budget-friendly while driving strong recurring revenue. Growing regulatory approvals for diagnostic AI tools, along with strong use cases in oncology, neurology, and cardiology, further accelerate the dominance of this technology in the market.

The North America region accounted for a substantial share of the radiology AI market in 2025.

The North American region accounted for a substantial share of the radiology AI market in 2025, driven by significant investments in healthcare infrastructure, the adoption of advanced technology, and high demand for imaging services. The US, in particular, has seen widespread integration of AI into radiology workflows, supported by federal incentives for digital health adoption and regulatory approvals for AI-powered diagnostic tools. In addition, the growing prevalence of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions has increased the demand for advanced imaging solutions, fueling the adoption of AI algorithms for image analysis, triage, and workflow optimization. For instance, in April 2025, according to the NIHCM Foundation, chronic diseases continue to pose a major burden on the US healthcare system, accounting for approximately 90% of the USD 4.5 trillion spent on healthcare in 2022, affecting around 60% of people in the US with multiple chronic conditions, thus driving high costs and complex care needs.

Robust investment from both private and public sectors, along with a high concentration of AI startups and established technology companies, further reinforced North American market leadership. Companies such as Aidoc (US), Enlitic, Inc. (US), and GE HealthCare (US) are actively developing AI-enabled platforms for CT, MRI, X-ray, and PET imaging, enhancing diagnostic accuracy and operational efficiency.

However, challenges such as data privacy concerns under HIPAA and clinician hesitancy to fully adopt AI tools remain. Despite these hurdles, the region continues to lead the global radiology AI market due to a combination of advanced healthcare infrastructure, favorable reimbursement policies, high R&D investment, and early adoption of innovative AI technologies.

These factors collectively reinforce North America's leadership in the radiology AI market.

The breakdown of primary participants is as mentioned below:

By Company Type - Tier 1: 45%, Tier 2: 30%, and Tier 3: 25%

By Designation - C Level: 40%, Director Level: 30%, and Others: 30%

By Region - North America: 40%, Europe: 30%, Asia Pacific: 25%, Latin America: 3%, Middle East & Africa: 2%

Key Players in the Radiology AI Market

The key players functioning in the radiology AI market include Siemens Healthineers AG (Germany), Microsoft (US), Koninklijke Philips N.V. (Netherlands), GE HealthCare (US), Fujifilm Holdings Corporation (Japan), Canon Medical Systems Corporation (Japan), Merative (US), DeepHealth (RadNet, Inc.) (US), Shanghai United Imaging Healthcare Co., LTD (China), Hologic, Inc. (US), and Enlitic, Inc. (US).

Research Coverage:

The report analyses the radiology AI market. It aims to estimate the market size and future growth potential of various market segments based on offering, function, modality, indication, end user, and region. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will help established firms and new entrants/smaller firms gauge the market's pulse, which, in turn, will help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

Analysis of key drivers: Drivers (increasing medical imaging volumes, rising demand for AI solutions to alleviate radiologist workload, increase in regulatory clarity, accelerated approvals and government support, growing demand for AI-driven radiological image processing, growing funding for AI-focused startups, and rising collaborations with AI, tech, and analytics solution providers, Restraints (high implementation costs and ROI uncertainty, regulatory fragmentation across regions, and data quality and label scarcity for rarer indications), Opportunities (Growing demand for platform, multi-modal data, and OEM integration [PACS/EHR/marketplaces]), untapped growth potential in emerging healthcare markets, expansion of preventive care and population health management, and expansion of portable or handheld devices with AI integration), Challenges (integration challenges with legacy radiology systems, limited clinician trust and explainability demands, and concerns over data privacy and security) influencing the growth of the radiology AI market.

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product launches in the radiology AI market

Market Development: Comprehensive information on the lucrative emerging markets, by offering, function, modality, indication, end user, and region.

Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the radiology AI market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the radiology AI market such as Siemens Healthineers AG (Germany), Microsoft (US), Koninklijke Philips N.V. (Netherlands), GE HealthCare (US), Fujifilm Holdings Corporation (Japan), Canon Medical Systems Corporation (Japan), Merative (US), DeepHealth (RadNet, Inc.) (US), Shanghai United Imaging Healthcare Co., LTD (China), Hologic, Inc. (US), and Enlitic, Inc. (US).