클라우드 FinOps 시장 : 제공 제품별, 용도/능력별, 전개 형태별, 서비스 모델별, 조직 규모별, 업계별, 지역별 - (-2030년)

Cloud FinOps Market Size by Application (Cost Management & Optimization, Budgeting & Forecasting, Cost Allocation & Chargeback, Reporting & Analytics, Workload Management & Optimization), Deployment (Single Cloud, Multi Cloud) - Global Forecast to 2030

상품코드:1906299

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 376 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

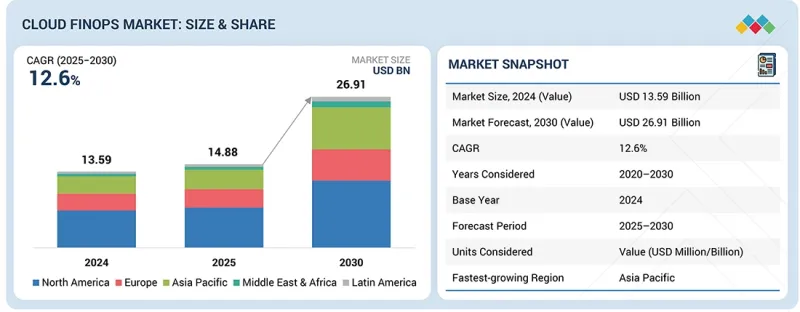

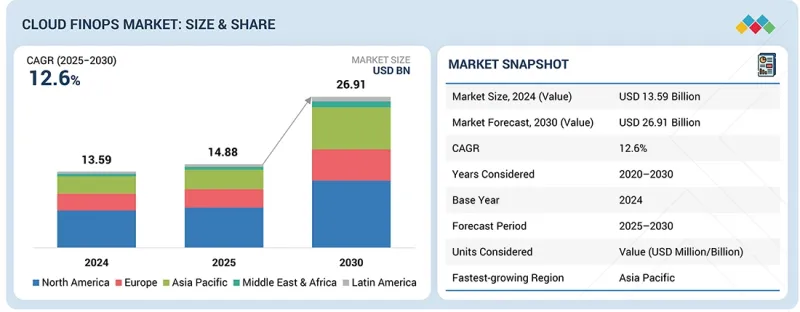

세계의 클라우드 FinOps 시장 규모는 급속히 확대되고 있습니다. 2025년 약 148억 8,000만 달러에서 2030년까지 269억 1,000만 달러로 성장하여 CAGR은 12.6%를 보일 것으로 예측됩니다.

이 시장은 기업이 클라우드 환경 전반에 걸쳐 강력한 재무 관리 메커니즘을 도입하고 컴플라이언스에 대응하는 비용 거버넌스 확보를 의무화하는 규제 감사 증가를 배경으로 꾸준히 성장하고 있습니다.

조사 범위

조사 대상 기간

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

가치(100만/10억 달러)

부문

제공 제품별, 용도/능력별, 전개 형태별, 서비스 모델별, 조직 규모별, 업계별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카

클라우드 FinOps는 지출, 사용량, 할당 지표를 통합하여 데이터 가시성을 높이고, 재무, 엔지니어링, 비즈니스 팀 전체에 대한 책임을 명확히 하고 지속적인 최적화를 가능하게 합니다. 기존 조직 구조에 클라우드 전담 FinOps 팀을 통합함으로써 클라우드 재무 관리를 더욱 공식화하고, 소비에 대한 의사결정을 예산 소유권 및 비즈니스 우선순위에 맞게 조정할 수 있게 되었습니다.

동시에 클라우드 FinOps는 클라우드 지출을 용도 성능, 단위 경제, 측정 가능한 비즈니스 성과에 직접 연결하여 투자 가치 실현을 크게 개선하고 기업을 가치 기반 소비 모델로 전환하고 있습니다. 그러나 멀티 클라우드 환경 전반에 걸친 집중적인 클라우드 비용 인텔리전스를 방해하는 단편적인 재무 및 사용 데이터 시스템이 시장 성장을 저해하고 있습니다. 유휴 자원, 과잉 프로비저닝, 비효율적인 조달 모델로 인한 지속적인 불필요한 클라우드 지출은 최적화 노력을 계속 약화시키고 있습니다. 또한, 문화적 관성 및 부서 간 수직적 구조로 인한 클라우드 FinOps 솔루션으로의 전환 저항이 도입과 성숙도를 지연시키고 있습니다. 이러한 도전에도 불구하고, 컴플라이언스에 대한 압박과 클라우드의 복잡성 증가는 클라우드 FinOps를 지속 가능한 재무 거버넌스의 핵심 분야로 부각시키고 있습니다.

의료 및 생명과학 분야의 조직들은 엄격한 규제와 비용 제약 하에서 임상 시스템, 연구 분석, 영상 진단, 유전체학, AI 기반 진단을 지원하기 위해 클라우드 도입을 가속화하고 있습니다. 이 분야의 클라우드 지출은 데이터 집약적인 워크로드, 장시간 실행되는 분석 처리, 성능과 컴플라이언스가 타협할 수 없는 미션 크리티컬한 용도에 의해 주도되고 있습니다. 그 결과, 클라우드 FinOps 도입은 비용 투명성, 워크로드 계층화, 그리고 진료과, 연구 프로그램, 치료 영역에 부합하는 리소스 배분 모델에 초점을 맞추었습니다.

FinOps의 기능은 클라우드 사용이 예측 가능하고 감사 가능하며, 임상 및 연구 우선순위에 부합하도록 보장함으로써 조직이 혁신과 재정적 규율의 균형을 맞출 수 있도록 지원합니다. 2025년 4월, Health Catalyst는 Microsoft Azure와의 협업을 확대하여 대규모 데이터 처리에 있어 비용 가시성과 거버넌스가 필수적인 클라우드 기반 분석 플랫폼을 통해 의료 서비스 제공업체의 업무 및 재무 성과 향상을 지원했습니다. 2024년 7월, GE헬스케어와 AWS는 클라우드에서 확장 가능한 영상진단, 진단 및 AI 워크로드를 지원하기 위해 전략적 제휴를 강화했습니다. 이는 대용량 및 계산 집약적인 의료 용도에서 체계적인 비용 관리의 중요성을 강조합니다. 이러한 노력은 의료 클라우드의 현대화가 혁신과 구조화된 재무 거버넌스와 연결되는 사례가 증가하고 있음을 보여줍니다. 의료 및 생명과학 조직에게 FinOps는 책임감 있는 클라우드 기반 혁신을 지속하는 데 필수적입니다. 이를 통해 비용에 대한 책임성을 실현하고, 컴플라이언스 대응을 지원하며, 클라우드 투자가 환자 치료 결과 개선, 연구 효율성 향상, 업무 탄력성 강화에 직접적으로 기여할 수 있도록 보장합니다.

대규모 기업은 클라우드 환경의 규모, 복잡성, 재무적 영향 때문에 클라우드 FinOps 시장에서 중요한 도입 부문을 형성하고 있습니다. 이들 조직은 지역, 사업부, 제품 팀에 걸쳐 광범위한 멀티 클라우드 및 하이브리드 환경을 운영하고 있으며, 중앙 집중식 가시성과 일관된 거버넌스가 필수적입니다. 대기업을 위한 FinOps 기능은 고급 비용 배분, 전사적 보고, 예측 예산 편성, 엔지니어링 소비를 기업의 재무 관리와 일치시키는 정책 기반 거버넌스에 중점을 둡니다. ERP, DevOps, IT 운영 플랫폼과의 통합은 FinOps를 기업 워크플로우에 통합하고 팀 전체에 대한 책임성을 유지하는 데 매우 중요합니다.

전략적 파트너십은 구조화된 FinOps 실행에 대한 기업 수요를 뒷받침하고 있습니다. 2025년 3월, 액센츄어는 AWS와의 협업을 확대하여 세계 클라우드 환경과 복잡한 비용 구조 전반에서 지속적인 최적화 및 거버넌스를 원하는 대기업을 위한 FinOps 자문 및 관리 서비스를 확대했습니다. 또한, 2024년 10월, IBM은 하이브리드 및 멀티 클라우드 환경에서의 엔터프라이즈 통합을 확대하고, 복잡한 배분 및 컴플라이언스 요건을 가진 대기업을 위해 보다 심층적인 비용 투명성과 거버넌스를 제공함으로써 클라우드 재무 관리 포트폴리오를 강화했습니다. 신생 벤더와 솔루션 제공업체는 하이퍼스케일러의 툴을 보완하면서 규모, 통합성, 거버넌스 깊이의 격차를 해소할 수 있는 차별화된 FinOps 기능을 제공할 수 있는 기회를 얻게 됩니다. 자동화, 크로스 클라우드 표준화, 기업용 ERP, ITSM, DevOps 에코시스템과의 원활한 통합을 제공하는 솔루션이 가장 유리한 입지를 차지할 것입니다. 측정 가능한 비용 성과를 입증하고, 복잡한 배분 모델을 지원하며, 전 세계 환경으로 확장할 수 있는 공급자는 대기업들이 FinOps를 핵심 재무 및 운영 규율로 공식화함에 따라 장기적인 전략적 중요성을 확립할 수 있습니다.

"북미는 하이퍼스케일 클라우드의 조기 성숙, 엄격한 규제 및 감사 요건, 대규모 멀티 계정 클라우드 지출 관리를 위한 네이티브 및 타사 FinOps 플랫폼의 광범위한 기업 채택으로 클라우드 FinOps 시장을 선도하고 있다"고 말했습니다. "

북미 클라우드 FinOps 시장은 높은 클라우드 성숙도, 엄격한 규제 감독, 기업의 멀티 클라우드 운영 모델의 대규모 도입으로 형성되고 있습니다. 미국과 캐나다의 조직들은 재무 감사, 데이터 거버넌스 요건, 내부 컴플라이언스 프레임워크를 통한 모니터링 강화에 직면해 있으며, 이는 구조화된 클라우드 재무 관리에 대한 강력한 수요를 주도하고 있습니다. 기업들은 컴퓨팅, 데이터 플랫폼, AI 워크로드에 걸친 복잡한 지출 패턴을 관리하기 위해 점점 더 많은 기업들이 FinOps 관행을 핵심 업무에 통합하고 있습니다.

북미에는 하이퍼스케일 클라우드 제공업체, FinOps 툴 벤더, 전문 서비스 기업으로 구성된 성숙한 생태계가 구축되어 있어 FinOps 프레임워크의 신속한 도입과 운영을 지원하고 있습니다. 대기업, 디지털 네이티브 기업, 공공기관의 클라우드 지출이 집중화되면서 실시간 비용 귀속, 차지백, 정책 중심의 예산 집행에 대한 필요성이 커지고 있습니다. 또한, 종량제 모델의 확산으로 지속적인 최적화 및 가치 실현의 중요성이 커지고 있습니다. 이러한 요인들로 인해 북미는 고도로 정교한 클라우드 FinOps 시장으로 자리매김하고 있으며, 재무 거버넌스는 클라우드 엔지니어링 및 비즈니스 의사결정과 긴밀하게 통합되어 있습니다.

본 보고서에는 클라우드 FinOps 제품을 제공하는 주요 벤더에 대한 조사가 포함되어 있습니다. 클라우드 FinOps 시장의 주요 벤더들프로파일을 소개합니다. 주요 시장 진출기업으로는 AWS(미국), Microsoft(미국), Google(미국), Oracle(미국), IBM(미국), Hitachi(일본), VMware(미국), ServiceNow(미국), Datadog(미국), Flexera(미국), Lumen Technologies(미국), DoiT(미국), Nutanix(미국), Amdocs(미국), BMC Software(미국), HCL(인도), Virtasant(미국), OpenText(캐나다), Accenture(아일랜드), ManageEngine(미국), IBM(미국), Datadog(미국), Flexera(미국), Lumen ManageEngine(미국), SoftwareOne(미국), CoreStack(미국), Virtana(미국), Cast AI(미국), Anodot(미국), Harness(미국), CloudZero(미국), PepperData(미국), Spot(미국), Unravel Data(미국)), Unravel Data(미국), KubeCost(미국) 등이 있습니다.

본 보고서 구매 이유

이 보고서는 시장 리더와 신규 시장 진출기업에게 전체 클라우드 FinOps 시장과 그 하위 부문의 수익 규모에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁상황을 이해하고, 자신의 비즈니스를 더 잘 포지셔닝하고, 적절한 시장 진출 전략을 수립할 수 있는 통찰력을 얻을 수 있습니다. 또한, 시장 동향을 파악하고 주요 시장 성장 촉진요인, 억제요인, 과제, 기회에 대한 정보를 제공합니다.

시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 클라우드 FinOps 시장을 분석합니다.

시장 다각화 : 클라우드 FinOps 시장의 신제품 및 서비스, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보 제공

경쟁사 평가: AWS(미국), Microsoft(미국), Google(미국), Oracle(미국), IBM(미국), Hitachi(일본), VMware(미국), ServiceNow(미국), Datadog(미국), Flexera(미국), Lumen Technologies(미국), DoiT(미국), Nutanix(미국), Amdocs(미국), BMC Software(미국), HCL(인도), Virtasant(미국), OpenText(캐나다), Accenture(아일랜드), ManageEngine(미국), IBM(미국) ManageEngine(미국), SoftwareOne(미국), CoreStack(미국), Nutanix(미국), Amdocs(미국), BMC Software(미국), HCL(인도), Virtasant(미국), OpenText(캐나다), Accenture(아일랜드), Accenture(아일랜드), ManageEngine(미국), SoftwareOne(미국), CoreStack(미국), Nutanix(미국), Amdocs(미국), BMC Software(미국), HCL(인도), Virtasant(미국), OpenText(캐나다) Accenture(아일랜드), ManageEngine(미국), SoftwareOne(미국), CoreStack(미국), Virtana(미국), Cast AI(미국), Cast AI(미국), Anodot(미국), Harness(미국), CloudZero(미국), CloudZero(미국), HCL(인도), Virtasant(미국), OpenText(캐나다) CloudZero(미국), PepperData(미국), Spot(미국), Unravel Data(미국), KubeCost(미국) 등 주요 시장 진출 기업의 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가. 이 보고서는 클라우드 FinOps 시장 동향에 대한 이해관계자의 이해를 돕고, 주요 시장 성장 촉진요인, 제약 조건, 과제 및 기회에 대한 정보를 제공합니다.

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

시장 역학

미충족 요구와 공백

연결된 시장과 분야간 기회

새로운 비즈니스 모델과 에코시스템 변화

Tier1/2/3참여 기업 전략적 움직임

제5장 업계 동향

Porter의 Five Forces 분석

거시경제 지표

공급망 분석

생태계 분석

가격 분석

2025년-2026년 주요 컨퍼런스 및 이벤트

고객의 비즈니스에 영향을 미치는 동향/혼란

투자 및 자금조달 시나리오

사례 연구 분석

2025년 미국 관세의 영향-클라우드 FinOps 시장

제6장 기술, 특허, 디지털, AI 도입 별 전략적 파괴

기술 분석

기술/제품 로드맵

특허 분석

향후 응용

AI/생성형 AI가 클라우드 FinOps 시장에 미치는 영향

성공 사례와 실세계에의 응용

제7장 규제 상황

규제 상황

규제기관, 정부기관 및 기타 조직

지역별 업계표준

제8장 고객 상황과 구매 행동

의사결정 프로세스

구입자 이해관계자와 구입 평가 기준

채택 장벽과 내부 과제

다양한 최종사용자 산업 미충족 요구

시장 수익성

제9장 클라우드 FinOps 시장(제공 제품별)

솔루션

서비스

제10장 클라우드 FinOps 시장(용도/능력별)

비용 관리 및 최적화

예산 편성 및 예측

비용 배분 및 요금 백

보고서 및 분석

워크로드 최적화 및 관리

기타

제11장 클라우드 FinOps 시장(전개 형태별)

전개 환경

전개 모드

제12장 클라우드 FinOps 시장(서비스 모델별)

IAAS

PAAS

SAAS

제13장 클라우드 FinOps 시장(조직 규모별)

대기업

중소기업

제14장 클라우드 FinOps 시장(업계별)

IT/ITES

은행, 금융서비스 및 보험(BFSI)

소매 및 소비재

헬스케어 및 생명과학

미디어 및 엔터테인먼트

제조

통신

정부 및 공공 부문

기타

제15장 클라우드 FinOps 시장(지역별)

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

기타

아시아태평양

중국

인도

일본

호주 및 뉴질랜드

기타

중동 및 아프리카

GCC 국가

남아프리카공화국

기타

라틴아메리카

브라질

멕시코

기타

제16장 경쟁 구도

주요 시장 진출기업의 전략/강점

매출 분석, 2020년-2024년

시장 점유율 분석, 2024년

브랜드/제품 비교

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

기업 평가와 재무 지표

경쟁 시나리오

제17장 기업 개요

주요 시장 진출기업

AWS

MICROSOFT

GOOGLE

ORACLE

IBM

HITACHI

VMWARE

SERVICENOW

DATADOG

FLEXERA

ZESTY

기타 기업

NUTANIX

AMDOCS

BMC SOFTWARE

HCL

VIRTASANT

OPENTEXT

ACCENTURE

MANAGEENGINE

SOFTWAREONE

CORESTACK

VIRTANA

CAST AI

ANODOT

HARNESS

CLOUDZERO

PEPPERDATA

SPOT

UNRAVEL DATA

CENTILYTICS

KUBECOST

FINOUT

HYPERGLANCE

DELOITTE

ALIBABA CLOUD

ZESTY

NOPS

CLOUDAVOCADO

HASHICORP

제18장 조사 방법

제19장 부록

LSH

영문 목차

영문목차

The global cloud FinOps market is expanding rapidly, with a projected market size anticipated to rise from about USD 14.88 billion in 2025 to USD 26.91 billion by 2030, featuring a CAGR of 12.6%. The global cloud FinOps market is expanding steadily, driven by rising regulatory audits that compel enterprises to implement robust financial control mechanisms across cloud environments and ensure compliance-ready cost governance.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion)

Segments

Offering, Application/Capability, Deployment, Service Model, Organization Size, Vertical

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, Latin America

As cloud usage scales, cloud FinOps is enhancing data visibility by consolidating spend, usage, and allocation metrics, enabling stronger accountability and continuous optimization across finance, engineering, and business teams. The integration of dedicated cloud FinOps teams into existing organizational structures is further formalizing cloud financial management, aligning consumption decisions with budget ownership and operational priorities.

At the same time, cloud FinOps is significantly improving investment value realization by directly linking cloud spend to application performance, unit economics, and measurable business outcomes, thereby shifting enterprises toward value-based consumption models. However, market growth is restrained by fragmented financial and usage data systems that obstruct centralized cloud cost intelligence across multi-cloud estates. Persistent unnecessary cloud expense, driven by idle resources, overprovisioning, and inefficient purchasing models, continues to dilute optimization efforts. In addition, resistance to switching to cloud FinOps solutions, often due to cultural inertia and siloed ownership, slows adoption and maturity. Despite these challenges, increasing compliance pressure and cloud complexity reinforce cloud FinOps as a critical discipline for sustained financial governance.

"By vertical, healthcare & life sciences are estimated to account for the fastest growth rate during the forecast period."

Healthcare and life sciences organizations are accelerating their cloud adoption to support clinical systems, research analytics, imaging, genomics, and AI-driven diagnostics, while operating under strict regulatory and cost constraints. Cloud expenditure in this vertical is driven by data-intensive workloads, long-running analytics, and mission-critical applications where performance and compliance cannot be compromised. As a result, cloud FinOps adoption focuses on cost transparency, workload tiering, and allocation models aligned to care units, research programs, and therapeutic areas.

FinOps capabilities help organizations strike a balance between innovation and financial discipline by ensuring cloud usage remains predictable, auditable, and aligned with clinical and research priorities. In April 2025, Health Catalyst expanded its collaboration with Microsoft Azure to help healthcare providers improve operational and financial performance through cloud-based analytics platforms, where cost visibility and governance are integral to large-scale data processing. In July 2024, GE HealthCare and AWS deepened their strategic collaboration to support scalable imaging, diagnostics, and AI workloads in the cloud, underscoring the importance of disciplined cost management for high-volume and compute-intensive healthcare applications. These initiatives demonstrate that healthcare cloud modernization is increasingly paired with innovation and structured financial governance. For healthcare and life sciences organizations, FinOps is essential for sustaining a responsible cloud-driven transformation. It enables cost accountability, supports compliance readiness, and ensures that cloud investments directly contribute to improved patient outcomes, enhanced research efficiency, and increased operational resilience.

"Large enterprises are estimated to account for the largest market share during the forecast period."

Large enterprises represent a significant adoption segment within the cloud FinOps market due to the scale, complexity, and financial impact of their cloud environments. These organizations operate extensive multi-cloud and hybrid estates that span regions, business units, and product teams, making centralized visibility and consistent governance essential. FinOps capabilities for large enterprises emphasize advanced cost allocation, enterprise-wide reporting, predictive budgeting, and policy-driven governance that aligns engineering consumption with corporate financial controls. Integration with ERP, DevOps, and IT operations platforms is crucial for embedding FinOps into enterprise workflows and maintaining accountability across teams.

Strategic partnerships underscore enterprise demand for structured FinOps execution. In March 2025, Accenture expanded its collaboration with AWS to scale FinOps advisory and managed services for large enterprises seeking continuous optimization and governance across global cloud estates and complex cost structures. Additionally, in October 2024, IBM strengthened its cloud financial management portfolio by expanding enterprise integrations across hybrid and multi-cloud environments, bringing deeper cost transparency and governance to large organizations with complex allocation and compliance requirements. For emerging vendors and solution providers, large enterprises present an opportunity to deliver differentiated FinOps capabilities that complement hyperscaler tooling while addressing gaps in scale, integration, and governance depth. Solutions that offer automation, cross-cloud normalization, and seamless integration with enterprise ERP, ITSM, and DevOps ecosystems will be best positioned for adoption. Providers that can demonstrate measurable cost outcomes, support complex allocation models, and scale across global environments can establish long-term strategic relevance as large enterprises continue to formalize FinOps as a core financial and operational discipline.

"North America leads the cloud FinOps market due to early hyperscale cloud maturity, strict regulatory and audit requirements, and widespread enterprise adoption of native and third-party FinOps platforms to manage large-scale, multi-account cloud spend."

The cloud FinOps market in North America is shaped by advanced cloud maturity, stringent regulatory oversight, and the large-scale adoption of multi-cloud operating models by enterprises. Organizations across the US and Canada face heightened scrutiny from financial audits, data governance mandates, and internal compliance frameworks, driving strong demand for structured cloud financial control. Enterprises are increasingly embedding FinOps practices into core operations to manage complex spending patterns across compute, data platforms, and AI workloads.

North America also benefits from a mature ecosystem of hyperscale cloud providers, FinOps tooling vendors, and professional services firms that support rapid implementation and operationalization of FinOps frameworks. The increasing concentration of cloud spending among large enterprises, digital-native companies, and public sector agencies has intensified the need for real-time cost attribution, chargeback, and policy-driven budget enforcement. Additionally, widespread adoption of consumption-based pricing models has elevated the importance of continuous optimization and value realization. These factors position North America as a highly sophisticated cloud FinOps market, where financial governance is tightly integrated with cloud engineering and business decision-making.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the cloud FinOps market.

By Company: Tier 1 - 33%, Tier 2 - 27%, and Tier 3 - 40%

By Designation: C-level Executives - 46%, D-level Executives - 22%, and others - 32%

By Region: North America - 40%, Europe - 28%, Asia Pacific - 27%, and Rest of the World - 5%

The report includes a study of key players offering cloud FinOps products. It profiles major vendors in the cloud FinOps market. The major market players include AWS (US), Microsoft (US), Google (US), Oracle (US), IBM (US), Hitachi (Japan), VMware (US), ServiceNow (US), Datadog (US), Flexera (US), Lumen Technologies (US), DoiT (US), Nutanix (US), Amdocs (US), BMC Software (US), HCL (India), Virtasant (US), OpenText (Canada), Accenture (Ireland), ManageEngine (US), SoftwareOne (US), CoreStack (US), Virtana (US), Cast AI (US), Anodot (US), Harness (US), CloudZero (US), PepperData (US), Spot (US), Unravel Data (US), and KubeCost (US).

Research Coverage

This research report categorizes the cloud FinOps market based on offering (solutions [native solutions, third party solutions], services [managed cloud FinOps services, professional services {FinOps advisory & strategy services, implementation & integration services, support & maintenance}]), application/capability (cost management & optimization, budgeting & forecasting, cost allocation & chargeback, reporting & analytics, workload optimization & management, other applications), deployment (deployment environment [single cloud, multi-cloud], deployment mode [public, private, hybrid]), service model (IaaS, PaaS, SaaS), organization size (large enterprises, SMEs), and vertical (IT & ITeS, BFSI, retail & consumer goods, healthcare & life sciences, media & entertainment, manufacturing, telecommunications, government & public sector, other verticals [energy & utilities, education]) and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers and acquisitions; and recent developments associated with the cloud FinOps market. This report also covers the competitive analysis of upcoming startups in the market ecosystem.

Reason to buy this report

The report would provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall cloud FinOps market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (rising regulatory audits compel enterprises to implement financial control mechanisms, cloud FinOps enhances data visibility for accountability and optimization, Integrating cloud FinOps team into existing organizational structure, cloud FinOps significantly improves investment value realization), restraints (fragmented financial data systems obstruct centralized cloud cost intelligence deployment, unnecessary cloud expense (cloud waste), resistance to switch to cloud FinOps solutions), opportunities (embedding FinOps into SaaS offerings enables differentiated value propositions, opportunity to maximize Cloud ROI using cloud FinOps strategies, Leveraging automation tools to streamline FinOps implementation), and challenges (scaling FinOps maturity across global business units strains operating consistency, effective management of relationships and negotiations with several cloud service providers)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the cloud FinOps market

Market Development: Comprehensive information about lucrative markets - the report analyses the cloud FinOps market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the cloud FinOps market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such as AWS (US), Microsoft (US), Google (US), Oracle (US), IBM (US), Hitachi (Japan), VMware (US), ServiceNow (US), Datadog (US), Flexera (US), Lumen Technologies (US), DoiT (US), Nutanix (US), Amdocs (US), BMC Software (US), HCL (India), Virtasant (US), OpenText (Canada), Accenture (Ireland), ManageEngine (US), SoftwareOne (US), CoreStack (US), Virtana (US), Cast AI (US), Anodot (US), Harness (US), CloudZero (US), PepperData (US), Spot (US), Unravel Data (US), KubeCost (US); the report also helps stakeholders understand the cloud FinOps market's pulse and provides information on key market drivers, restraints, challenges, and opportunities

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING MARKET

2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

2.5 SNAPSHOT: GLOBAL MARKET SIZE AND GROWTH RATE

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CLOUD FINOPS MARKET

3.2 CLOUD FINOPS MARKET, BY OFFERING

3.3 CLOUD FINOPS MARKET, BY APPLICATION/CAPABILITY

3.4 CLOUD FINOPS MARKET, BY DEPLOYMENT ENVIRONMENT

3.5 CLOUD FINOPS MARKET, BY DEPLOYMENT MODE

3.6 CLOUD FINOPS MARKET, BY ORGANIZATION SIZE

3.7 CLOUD FINOPS MARKET, BY SERVICE MODEL

3.8 CLOUD FINOPS MARKET, BY VERTICAL

3.9 CLOUD FINOPS MARKET, BY REGION

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rising regulatory audits compel enterprises to implement financial control mechanisms

4.2.1.2 Cloud FinOps enhances data visibility for accountability and optimization

4.2.1.3 Integrating cloud FinOps team into existing organizational structure

4.2.1.4 Cloud FinOps culture significantly improves investment value realization

4.2.2 RESTRAINTS

4.2.2.1 Fragmented financial data systems obstruct centralized cloud cost intelligence deployment

4.2.2.2 Unnecessary cloud expenses (cloud waste)

4.2.2.3 Resistance to switching to cloud FinOps solutions

4.2.3 OPPORTUNITIES

4.2.3.1 Embedding FinOps into SaaS offerings enables differentiated value propositions

4.2.3.2 Opportunity to maximize cloud ROI using cloud FinOps strategies

4.2.3.3 Leveraging automation tools to streamline FinOps implementation

4.2.4 CHALLENGES

4.2.4.1 Scaling FinOps maturity across global business units strains operating consistency

4.2.4.2 Effective management of relationships and negotiations with several cloud service providers

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 UNMET NEEDS IN CLOUD FINOPS MARKET

4.3.2 WHITE SPACE OPPORTUNITIES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 INTERCONNECTED MARKETS

4.4.2 CROSS-SECTOR OPPORTUNITIES

4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

4.5.1 EMERGING BUSINESS MODELS

4.5.1.1 Cloud FinOps business models

4.5.2 ECOSYSTEM SHIFTS

4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF BUYERS

5.1.4 BARGAINING POWER OF SUPPLIERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC INDICATORS

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS & FORECASTS

5.2.3 TRENDS IN GLOBAL CLOUD PERFORMANCE MANAGEMENT INDUSTRY

5.2.4 TRENDS IN GLOBAL INTEGRATED CLOUD MANAGEMENT PLATFORM INDUSTRY

5.3 SUPPLY CHAIN ANALYSIS

5.3.1 CLOUD SERVICE PROVIDERS

5.3.2 CLOUD FINOPS PLATFORMS AND TOOLS

5.3.3 MANAGED SERVICE PROVIDERS AND CONSULTING FIRMS

5.3.4 ENTERPRISE IT AND FINANCE DEPARTMENTS

5.3.5 SOFTWARE AND SOLUTION INTEGRATORS

5.3.6 REGULATORY AND COMPLIANCE BODIES

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 INDICATIVE PRICING ANALYSIS

5.5.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY SOLUTION

5.5.3 AVERAGE SELLING PRICE TREND

5.6 KEY CONFERENCES AND EVENTS, 2025-2026

5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.8 INVESTMENT AND FUNDING SCENARIO

5.9 CASE STUDY ANALYSIS

5.9.1 OPENTEXT OPTIMIZES CLOUD SPEND WITH HCMX FINOPS EXPRESS

5.9.2 ARKANSAS DEPARTMENT OF FINANCE AND ADMINISTRATION ENHANCES IT SECURITY AND COMPLIANCE WITH MANAGEENGINE ADAUDIT PLUS

5.9.3 ZORGSPECTRUM OPTIMIZES CLOUD SPENDING AND EFFICIENCY WITH SOFTWAREONE'S FINOPS

5.9.4 CORESTACK HELPS LOGICALIS TRANSFORM FINOPS INTO NEW BUSINESS OPPORTUNITIES

5.9.5 AWS OFFERED ENHANCED ACCOUNTABILITY AND GOVERNANCE ACROSS MEDIBANK'S BUSINESS UNITS

5.9.6 ABN AMRO REFINED COST OPTIMIZATION EFFORTS WITH MICROSOFT AZURE

5.9.7 ADOPTION OF APPTIO HELPED TUI GROUP ACHIEVE INFORMED CLOUD INVESTMENT DECISION-MAKING AND BETTER BUDGET TRACKING

5.10 IMPACT OF 2025 US TARIFF - CLOUD FINOPS MARKET

5.10.1 INTRODUCTION

5.10.2 KEY TARIFF RATES

5.10.3 PRICE IMPACT ANALYSIS

5.10.4 IMPACT ON COUNTRY/REGION

5.10.4.1 US

5.10.4.2 Europe

5.10.4.3 Asia Pacific

5.10.5 IMPACT ON VERTICALS

5.10.5.1 IT & ITeS

5.10.5.2 BFSI

5.10.5.3 Retail & Consumer Goods

5.10.5.4 Healthcare & Life Sciences

5.10.5.5 Media & Entertainment

5.10.5.6 Manufacturing

5.10.5.7 Telecommunications

5.10.5.8 Government & Public Sector

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

6.1 TECHNOLOGY ANALYSIS

6.1.1 KEY EMERGING TECHNOLOGIES

6.1.1.1 Real-Time cloud cost visibility platforms

6.1.1.2 Automated cost optimization engines

6.1.1.3 Cloud financial governance and policy management systems

6.1.2 COMPLEMENTARY TECHNOLOGIES

6.1.2.1 Cloud metering and usage analytics infrastructure

6.1.2.2 Tagging automation and metadata governance platforms

6.1.2.3 Cost allocation and chargeback systems

6.1.3 ADJACENT TECHNOLOGIES

6.1.3.1 Multi-cloud management platforms

6.1.3.2 Cloud billing exchange and marketplace systems

6.2 TECHNOLOGY/PRODUCT ROADMAP

6.2.1 SHORT-TERM (2025-2027) | BILLING STANDARDIZATION AND AUTOMATION OF WASTE REDUCTION

6.2.1.1 Material development

6.2.1.2 Product innovations

6.2.1.3 Market adoption

6.2.2 MID-TERM (2027-2030) | ENGINEERING INTEGRATED AND BUSINESS ALIGNED FINOPS

6.2.2.1 Material development

6.2.2.2 Product innovations

6.2.2.3 Market adoption

6.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS AND FINANCIALLY GOVERNED CLOUD OPERATIONS

6.2.3.1 Material development

6.2.3.2 Product innovations

6.2.3.3 Market adoption

6.3 PATENT ANALYSIS

6.4 FUTURE APPLICATIONS

6.4.1 AUTONOMOUS SERVICE ORCHESTRATION AND SELF-HEALING CLOUD OPERATIONS

6.4.2 GREEN FINOPS AND SUSTAINABILITY-LINKED COST OPTIMIZATION

6.4.3 KUBERNETES-NATIVE FINOPS AND MICRO-SERVICE COST INTELLIGENCE

6.4.4 FINSECOPS-DRIVEN POLICY-AS-CODE FINOPS

6.4.5 UNIT-ECONOMICS-CENTRIC FINOPS AND SAAS PROFITABILITY ENGINEERING

6.5 IMPACT OF AI/GENERATIVE AI ON CLOUD FINOPS MARKET

6.5.1 TOP USE CASES AND MARKET POTENTIAL

6.5.2 BEST PRACTICES IN CLOUD FINOPS

6.5.3 CASE STUDY OF AI IMPLEMENTATION IN CLOUD FINOPS MARKET

6.5.4 INTERCONNECTED ADJACENCY ECOSYSTEM AND IMPACT ON MARKET PLAYERS

6.5.5 CLIENT READINESS TO ADOPT GENERATIVE AI IN CLOUD FINOPS MARKET

6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

6.6.1 NOPS: INFORM

6.6.2 CORESTACK: FINOPS+

7 REGULATORY LANDSCAPE

7.1 REGULATORY LANDSCAPE

7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

7.1.2 INDUSTRY STANDARDS, BY REGION

7.1.2.1 North America

7.1.2.2 Europe

7.1.2.3 Asia Pacific

7.1.2.4 Middle East & South Africa

7.1.2.5 Latin America

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

8.1 DECISION-MAKING PROCESS

8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

8.2.2 BUYING CRITERIA

8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

8.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

8.5 MARKET PROFITABILITY

8.5.1 REVENUE POTENTIAL

8.5.2 COST DYNAMICS

8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 CLOUD FINOPS MARKET, BY OFFERING

9.1 INTRODUCTION

9.1.1 OFFERING: CLOUD FINOPS MARKET DRIVERS

9.2 SOLUTIONS

9.2.1 ESSENTIAL FOR ENFORCING FINANCIAL DISCIPLINE AND VALUE ACCOUNTABILITY ACROSS CLOUD ENVIRONMENTS

9.2.2 NATIVE SOLUTIONS

9.2.2.1 Cloud financial governance driven by embedding cost controls directly into cloud operations

9.2.3 THIRD-PARTY SOLUTIONS

9.2.3.1 Unified cost governance and accountability enabled across complex multi-cloud environments

9.3 SERVICES

9.3.1 ENTERPRISES ENABLED TO OPERATIONALIZE COST GOVERNANCE AND SUSTAIN FINANCIAL ACCOUNTABILITY AT SCALE

9.3.2 MANAGED CLOUD FINOPS SERVICES

9.3.2.1 Operationalizing continuous cost optimization and governance for complex cloud environments

9.3.3 PROFESSIONAL SERVICES

9.3.3.1 Organizations enabled to operationalize cloud FinOps with sustained governance and measurable cost control