수술용 가운 및 드레이프 시장 : 제품 유형별, 용도별, 소재별, 멸균 상태별, 적용 분야별, 최종사용자별(-2030년)

Surgical Gowns and Drapes Market by Product Type, Usage, Material (Nonwoven, Woven ), Sterility, Application, End User - Global Forecast to 2030

상품코드:1893725

리서치사:MarketsandMarkets

발행일:2025년 12월

페이지 정보:영문 379 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

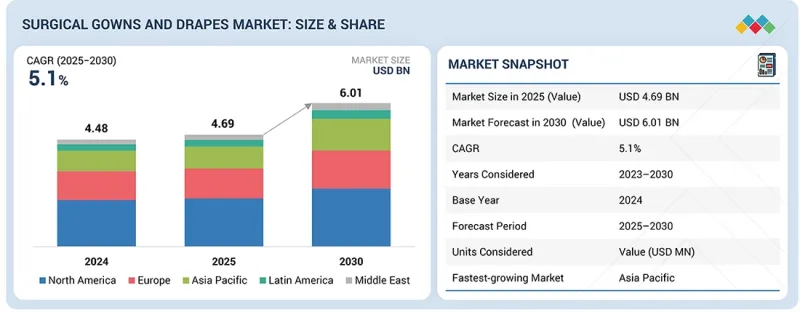

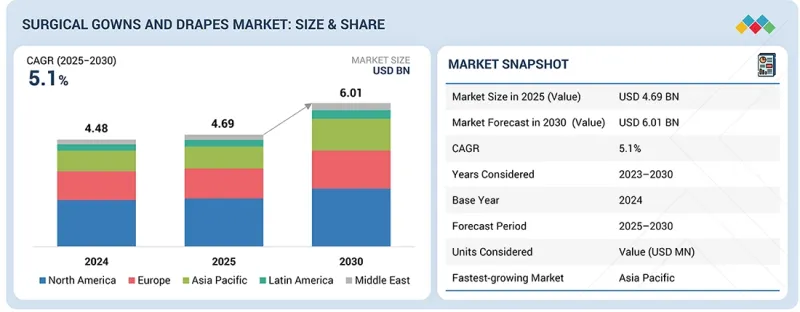

세계 수술용 가운 및 드레이프 시장 규모는 예측 기간 동안 CAGR 5.1%로 성장하여 2025년 46억 9,000만 달러, 2030년에는 60억 1,000만 달러에 이를 것으로 전망됩니다.

의료 관련 감염(HAI) 증가, 수술 수 증가, 섬유 기술의 진보로 시장은 높은 성장을 기대하고 있습니다. 감염 예방과 환자 안전에 대한 관심의 향상과 항균성 및 내액성 소재의 혁신은 고품질의 수술용 가운 및 드레이프 수요를 견인하고 있습니다.

조사 범위

조사 대상 기간

2023-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액(달러)

부문

제품 유형, 소재, 살균 상태, 용도, 최종 사용자

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

그러나 일회용 제품이 환경에 미치는 영향과 고급 수술 섬유의 고비용에 대한 우려가 시장 성장을 억제할 수 있습니다. 그럼에도 불구하고 제품 성능의 지속적인 향상과 병원 및 의료시설의 채택 증가가 시장 확대를 촉진할 것으로 예측됩니다.

"최종 사용자별로 병원 부문이 예측 기간 동안 최대 규모를 차지할 전망"

최종 사용자별로 2024년 기준에서 병원은 시장 최대 점유율을 차지했습니다. 세계 병원에서 실시되는 수술 및 의료 절차의 수가 많기 때문에 병원 부문은 수술용 가운 및 드레이프 시장에서 가장 큰 규모입니다. 병원은 수술의 주요 실시 장소이며, 감염 예방과 환자의 안전 확보에는 무균 환경의 유지가 필수적입니다. 병원에서 수술용 가운 및 드레이프에 대한 수요는 환자와 의료 종사자 모두를 보호하기 위한 고품질의 신뢰성 있는 감염 관리 제품에 대한 필요성에 의해 견인되고 있습니다. 게다가, 병원은 감염 예방을 강화하기 위해, 내액성이나 항균성이 있는 소재 등, 첨단적인 재료나 기술을 채택하는 경향이 강해지고 있습니다. 수술실, 환자 관리 지역 및 기타 임상 현장에서 수술용 가운과 드레이프가 항상 필요하기 때문에 병원 부문은 시장에서 가장 크고 가장 지배적인 최종 사용자가 되고 있습니다.

"용도별로는 일반 외과 제품 부문이 최대 시장 점유율을 차지한다"

일반 수술 분야는 세계적으로 실시되는 수술 건수가 많기 때문에 최대의 부문이 되고 있습니다. 맹장 절제술, 담낭 절제술, 탈장 수술과 같은 일반 수술은 가장 흔한 의료 절차 중 하나이며 수술 가운과 드레이프에 대한 수요를 크게 견인합니다. 이러한 수술은 환자의 안전을 보장하기 위해 엄격한 감염 관리 조치가 필요하며 고품질의 수술 섬유가 필수적입니다. 일반 수술 분야에서 일회용 가운과 드레이프의 보급은 무균 환경의 유지, 감염 위험의 감소, 수술 전체의 효율 향상에 기여하고 있습니다. 일반 수술이 계속 높은 빈도로 수행되는 동안,이 분야는 수술 가운 및 드레이프 시장의 성장을 견인하는 주요 요인으로 계속되고 있습니다.

"지역별로는 아시아태평양이 예측 기간 동안 최대 성장을 보여줄 전망"

이 지역의 급속한 도시화와 의료 인프라의 확대로 수술용 가운과 드레이프를 포함한 감염 관리 제품에 대한 수요가 크게 증가하고 있습니다. 중국, 인도, 동남아시아 등 국가에서 수술 건수가 증가함에 따라 고품질의 비용 효율적인 수술 섬유의 필요성이 커지고 있습니다. 또한, 의료 관련 감염(HAI) 증가 추세와 의료 수준 향상을 목표로 하는 정부의 이니셔티브가 이 지역에서 수술용 가운 및 드레이프의 도입을 더욱 촉진하고 있습니다. 엄청난 인구 기반과 환자 안전에 대한 관심 증가에 따라 아시아태평양은 향후 수년간 상당한 성장을 이룰 전망입니다.

본 보고서에서는 세계의 수술용 가운 및 드레이프 시장을 조사했으며, 시장 개요, 각종 시장 성장 영향요인 분석, 기술·특허의 동향, 법 규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

시장 역학

성장 촉진요인

억제요인

기회

과제

미충족 요구와 화이트 스페이스

상호 연계된 시장 및 산업 간 기회

Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

Porter's Five Forces 분석

거시경제지표

공급망 분석

밸류체인 분석

생태계 분석

가격 분석

무역 분석

2025-2026년 주요 회의 및 이벤트

고객의 사업에 영향을 주는 동향/혁신

투자 및 자금조달 시나리오

사례 연구 분석

2025년 미국 관세가 수술용 가운과 드레이프 시장에 미치는 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 장래의 응용

주요 신기술

스마트 텍스타일(E-textiles)

생분해성 및 퇴비화 가능한 소재

항균 및 항바이러스 코팅

보완적 기술

멸균 기술

재사용 가능한 수술용 섬유

기술/제품 로드맵

특허 분석

미래의 응용

AI/생성형 AI가 수술용 가운과 드레이프 시장에 미치는 영향

제7장 지속가능성과 규제상황

지역 규제 및 규정 준수

지속가능성에 대한 노력

지속가능성에 미치는 영향과 규제 정책의 노력

제8장 고객정세와 구매행동

의사결정 프로세스

구매 이해관계자 및 구매평가기준

채택 장벽과 내부 과제

다양한 최종 사용자 산업에서의 미충족 요구

시장 수익성

제9장 수술용 가운 및 드레이프 시장 : 제품 유형별

수술용 드레이프

일회용 드레이프

재사용 가능 드레이프

수술용 가운

제10장 수술용 가운 및 드레이프 시장 : 수량 분석

미국 : 수술용 드레이프 총량(용도별)

미국 : 수술용 가운 총량(용도별)

제11장 수술용 가운 및 드레이프 시장 : 소재별

부직포

폴리프로필렌(PP)

폴리에틸렌(PE)

스펀본드 멜트블로운 스펀본드(SMS)

스펀레이스 소재

기타

직물

코튼

폴리에스테르와 면의 혼방

폴리에스테르

마이크로 화이버 원단

라미네이트/코팅 재료

생분해성 소재

제12장 수술용 가운 및 드레이프 시장 : 멸균 상태별

멸균 제품

비멸균 제품

제13장 수술용 가운 및 드레이프 시장 : 용도별

심장 혈관

일반 외과

부인과

안과

절개술및 복강경 수술

기타

제14장 수술용 가운 및 드레이프 시장 : 최종 사용자별

병원

외래수술센터(ASC)

기타

제15장 수술용 가운 및 드레이프 시장 : 지역별

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

기타

아시아태평양

일본

중국

인도

호주

기타

라틴아메리카

브라질

멕시코

기타

중동 및 아프리카

제16장 경쟁 구도

개요

주요 진입기업의 전략/강점

수익 분석

시장 점유율 분석

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업

기업평가 매트릭스 : 스타트업/중소기업

기업평가와 재무지표

경쟁 시나리오

제17장 기업 프로파일

주요 기업

CARDINAL HEALTH

MEDLINE INDUSTRIES, LP

OWENS & MINOR

MCKESSON CORPORATION

MOLNLYCKE AB

SOLVENTUM

PAUL HARTMANN AG

WINNER MEDICAL, CO., LTD.

STERIS

ALPHAPROTECH

HENRY SCHEIN

B.BRAUN SE

BOSTON SCIENTIFIC CORPORATION

기타 기업

LOHMANN & RAUSCHER GMBH & CO. KG

STANDARD TEXTILE CO., INC.

PLURITEX SRL

MEDICA EUROPE BV

AMARYLLIS HEALTHCARE PVT. LTD.

STERIMED GROUP

GPC MEDICAL

ALLESET

BOEN HEALTHCARE CO., LTD.

PRIONTEX

EURONDA SPA

TIDI PRODUCTS, LLC.

제18장 조사 방법

제19장 부록

SHW

영문 목차

영문목차

The global surgical gowns and drapes market is projected to reach USD 6.01 billion by 2030 from USD 4.69 billion in 2025, at a CAGR of 5.1% during the forecast period. The market is expected to experience high growth due to the rising prevalence of healthcare-associated infections (HAIs), an increase in surgical procedures, and advancements in fabric technologies. The growing focus on infection prevention and patient safety, as well as innovations in antimicrobial and fluid-resistant materials, are driving the demand for high-quality surgical gowns and drapes.

Scope of the Report

Years Considered for the Study

2023-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product Type, Material, Sterility, Application, and End User

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

However, concerns over the environmental impact of disposable products and the high cost of premium surgical textiles may restrain market growth. Nonetheless, the continuous improvement in product performance and increasing adoption in hospitals and healthcare facilities are expected to fuel the market expansion.

The hospitals segment is expected to have the largest market during the forecast period.

Based on end user, the market is segmented into hospitals, ambulatory surgical centers, and other end users. In 2024, hospitals accounted for the largest share of the market. The hospital segment is the largest in the surgical gowns and drapes market due to the high volume of surgeries and medical procedures performed in hospitals worldwide. Hospitals are primary settings for surgeries, where maintaining a sterile environment is critical to preventing infections and ensuring patient safety. The demand for surgical gowns and drapes in hospitals is driven by the need for high-quality, reliable infection control products to protect both patients and healthcare professionals. Additionally, hospitals are more likely to adopt advanced materials and technologies, such as fluid-resistant and antimicrobial fabrics, to enhance infection prevention. With a constant need for surgical gowns and drapes in operating rooms, patient care areas, and other clinical settings, the hospital segment remains the largest and most dominant end user in the market.

The general surgery products segment accounted for the largest market share in the surgical gowns and drapes market.

The surgical gowns and drapes market is segmented into general surgery, cardiovascular, gynecology, ophthalmology, lithotomy & laparoscopy, and other applications, based on application. The general surgery segment is the largest in the surgical gowns and drapes market due to the high volume of procedures performed globally. General surgeries, such as appendectomies, gallbladder removals, and hernia repairs, are among the most common medical procedures, driving significant demand for surgical gowns and drapes. These surgeries require strict infection control measures to ensure patient safety, making high-quality surgical textiles essential. The widespread use of disposable gowns and drapes in general surgery helps maintain a sterile environment, reduce the risk of infections, and enhance overall procedural efficiency. As general surgeries continue to be performed at a high rate, this segment remains the dominant driver of growth in the surgical gowns and drapes market.

Asia Pacific is expected to be the fastest-growing market for surgical gowns and drapes during the forecast period.

The global surgical gowns and drapes market is segmented into six segments, namely, North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific is expected to be the fastest-growing market for surgical gowns and drapes during the forecast period. The region's rapid urbanization, coupled with growing healthcare infrastructure, has significantly increased the demand for infection control products, including surgical gowns and drapes. As the number of surgeries rises in countries like China, India, and Southeast Asia, the need for high-quality, cost-effective surgical textiles grows. Moreover, the increasing prevalence of healthcare-associated infections (HAIs) and government initiatives aimed at improving healthcare standards are further driving the adoption of surgical gowns and drapes in the region. With a large population base and a growing focus on patient safety, the Asia Pacific is poised to experience substantial growth in this market over the coming years.

North America leads the surgical gowns and drapes market in terms of market size, driven by its advanced healthcare systems and high number of surgical procedures performed annually. The region's well-established healthcare infrastructure, coupled with stringent infection control regulations, has made surgical gowns and drapes essential in maintaining sterile environments during surgeries. Additionally, North America's focus on patient safety and the adoption of advanced fabric technologies, such as antimicrobial and fluid-resistant materials, further boost the demand for these products. The presence of leading manufacturers and significant healthcare expenditure in countries such as the US and Canada ensures that North America remains the dominant market for surgical gowns and drapes.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1: 28%, Tier 2: 42%, and Tier 3: 30%

By Designation: C Level: 30%, Director Level: 34%, and Others: 36%

By Region: North America: 51%, Europe: 21%, Asia Pacific: 18%, Latin America: 6%, and Middle East & Africa: 4%

Note 1: Companies are classified into tiers based on their total revenue. As of 2024, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the surgical gowns and drapes market are Cardinal Health (US), Owens & Minor (US), Medline Industries, LP. (US), McKesson Corporation (US), and Molnlycke AB (Sweden).

Research Coverage

This report examines the surgical gowns and drapes market in terms of product type, material, sterility, application, end user, and regions. The report also examines key factors (including drivers, restraints, opportunities, and challenges) influencing market growth and provides an in-depth analysis of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets in terms of their individual growth trends. It forecasts the revenue of the market segments with respect to five major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms and smaller entrants to gauge the market's pulse, which in turn will help them garner a larger market share. Firms purchasing the report could use one or more strategies mentioned below to strengthen their market presence.

This report provides insights into the following pointers:

Analysis of key Drivers (Growing prevalence of HAIs, Increasing number of surgical procedures, Rising focus on infection prevention protocols, Expansion of ambulatory surgical centers)

Restraints (Reuse of surgical gowns and drapes in developing regions, High cost of premium disposable products)

Opportunities (Growth opportunities in emerging countries, Adoption of advanced fabric technologies)

Challenges (Supply chain volatility in raw materials, Quality inconsistency among low-cost suppliers)

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the surgical gowns and drapes market

Product Development/Innovation: Detailed insights into the upcoming trends, R&D activities, and product launches in the surgical gowns and drapes market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the surgical gowns and drapes market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players, such as Cardinal Health (US), Owens & Minor (US), Medline Industries, LP. (US), McKesson Corporation (US), and Molnlycke AB (Sweden)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING MARKET

2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 SURGICAL GOWNS AND DRAPES MARKET OVERVIEW

3.2 SURGICAL GOWNS AND DRAPES MARKET, BY PRODUCT TYPE, 2025 VS. 2030

3.3 SURGICAL GOWNS AND DRAPES MARKET, BY MATERIAL, 2025 VS. 2030

3.4 SURGICAL GOWNS AND DRAPES MARKET, BY STERILITY, 2025 VS. 2030

3.5 SURGICAL GOWNS AND DRAPES MARKET, BY APPLICATION, 2025 VS. 2030

3.6 SURGICAL GOWNS AND DRAPES MARKET, BY END USER, 2025 VS. 2030

3.7 SURGICAL GOWNS AND DRAPES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rising prevalence of healthcare-associated infections

4.2.1.2 Increasing number of surgical procedures

4.2.1.3 Growing focus on infection prevention protocols

4.2.1.4 Expansion of ambulatory surgical centers

4.2.2 RESTRAINTS

4.2.2.1 Reuse of surgical gowns and drapes in developing regions

4.2.2.2 High cost of premium disposable products

4.2.3 OPPORTUNITIES

4.2.3.1 Growth opportunities in emerging countries

4.2.3.2 Adoption of advanced fabric technologies

4.2.4 CHALLENGES

4.2.4.1 Supply chain volatility in raw materials

4.2.4.2 Quality inconsistency among low-cost suppliers

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 UNMET NEEDS IN SURGICAL GOWNS AND DRAPES MARKET

4.3.2 WHITE SPACE OPPORTUNITIES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 INTERCONNECTED MARKETS

4.4.2 CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF BUYERS

5.1.4 BARGAINING POWER OF SUPPLIERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC INDICATORS

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.3 SUPPLY CHAIN ANALYSIS

5.4 VALUE CHAIN ANALYSIS

5.5 ECOSYSTEM ANALYSIS

5.6 PRICING ANALYSIS

5.6.1 AVERAGE SELLING PRICE TREND, BY PRODUCT

5.6.2 AVERAGE SELLING PRICE TREND, BY KEY PLAYER

5.6.3 AVERAGE SELLING PRICE TREND, BY REGION

5.7 TRADE ANALYSIS

5.7.1 IMPORT SCENARIO (HS CODE 621010)

5.7.2 EXPORT SCENARIO (HS CODE 621010)

5.8 KEY CONFERENCES AND EVENTS, 2025-2026

5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.10 INVESTMENT AND FUNDING SCENARIO

5.11 CASE STUDY ANALYSIS

5.11.1 CASE STUDY 1: COST BENEFIT ANALYSIS OF SURGICAL GOWN AND DRAPE SELECTION

5.11.2 CASE STUDY 2: COMPARE IMPACT AND COST-EFFECTIVENESS LONG FIBER POLYESTER VS. COTTON FABRIC DRAPES

5.11.3 CASE STUDY 3: EVALUATE AND COMPARE PERFORMANCE OF DISPOSABLE VS. REUSABLE MEDICAL GOWNS

5.12 IMPACT OF 2025 US TARIFFS ON SURGICAL GOWNS AND DRAPES MARKET

5.12.1 INTRODUCTION

5.12.2 KEY TARIFF RATES

5.12.3 PRICE IMPACT ANALYSIS

5.12.4 KEY IMPACT ON COUNTRY/REGION

5.12.4.1 North America

5.12.4.2 Europe

5.12.4.3 Asia Pacific

5.12.5 IMPACT ON END-USE INDUSTRIES

5.12.5.1 Hospitals

5.12.5.2 Ambulatory Surgical Centers (ASCs)

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

6.1 KEY EMERGING TECHNOLOGIES

6.1.1 SMART TEXTILES (E-TEXTILES)

6.1.2 BIODEGRADABLE AND COMPOSTABLE MATERIALS

6.1.3 ANTIMICROBIAL AND ANTIVIRAL COATINGS

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 STERILIZATION TECHNOLOGIES

6.2.2 REUSABLE SURGICAL TEXTILES

6.3 TECHNOLOGY/PRODUCT ROADMAP

6.3.1 SHORT-TERM (2025-2027) | PROCESS IMPROVEMENT & STANDARDIZATION

6.3.2 MID-TERM (2027-2030) | MATERIAL DIVERSIFICATION & SUSTAINABILITY