빌딩 인포메이션 모델링(BIM) 시장 예측(-2030년) : 제공별, 배포 유형별, 프로젝트 수명주기별, 최종사용자별, 업계별, 지역별

Building Information Modeling Market By Offering, Deployment Type, Project Lifecycle, End User, Vertical, and Region - Global Forecast to 2030

상품코드:1869555

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 270 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

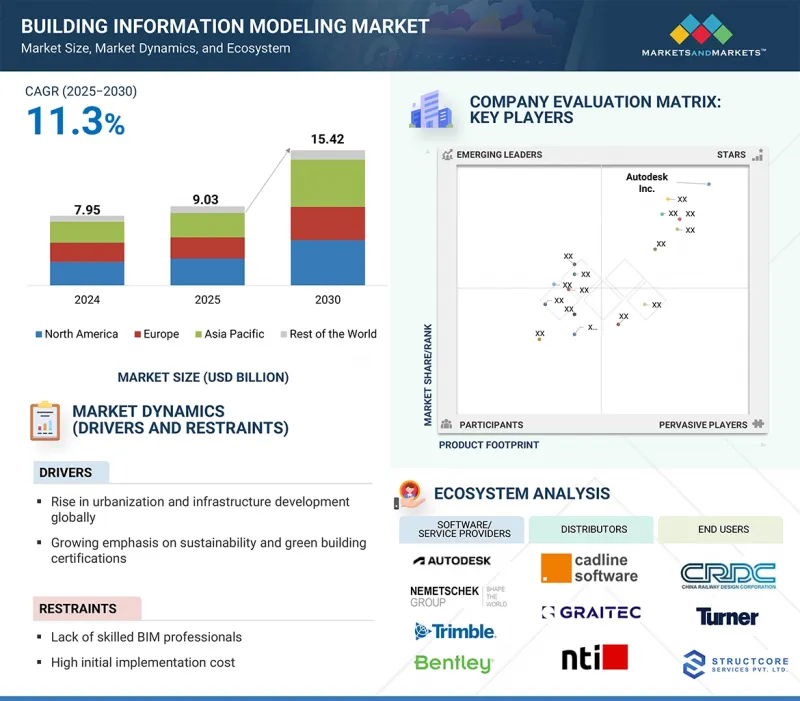

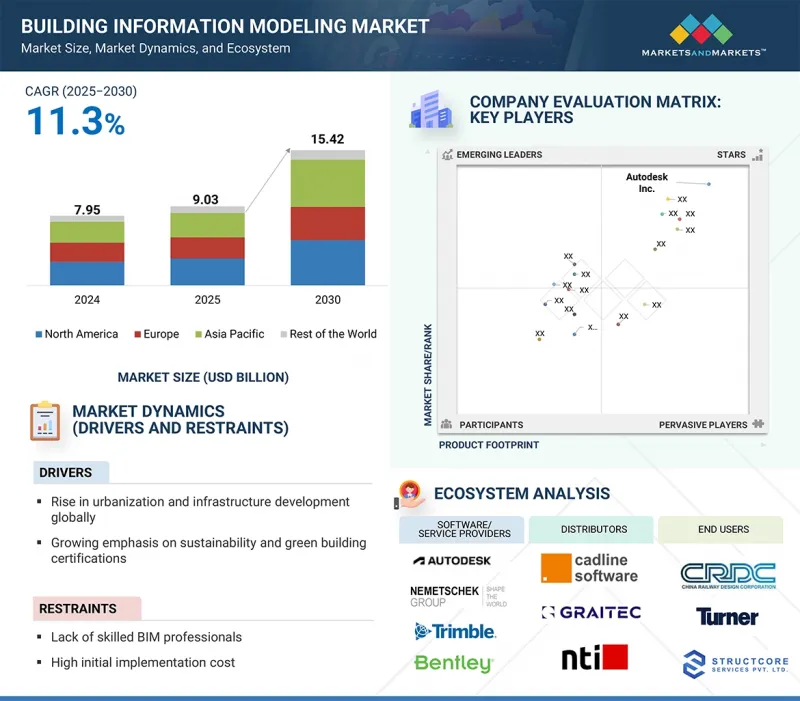

세계의 빌딩 인포메이션 모델링(BIM) 시장 규모는 2025년 90억 3,000만 달러에서 2030년까지 154억 2,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 11.3%의 성장이 전망됩니다.

조사 범위

조사 대상 기간

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

제공, 배포 유형, 프로젝트 수명주기, 최종사용자, 업계, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

BIM 시장은 건설 프로젝트의 효율적인 계획, 비용 관리, 리스크 감소에 대한 수요 증가로 인해 성장세를 보이고 있습니다. BIM의 지속가능성 목표 지원, 실시간 데이터 통합 실현, 모듈식 건설 등의 동향에 부합하는 BIM의 역량이 BIM의 채택을 촉진하고 있습니다. 정부의 의무화, IoT, 디지털 트윈, 클라우드, AI 등의 기술과의 통합이 성장을 더욱 가속화하고 있습니다. 이러한 요인들로 인해 BIM은 건설 부문의 디지털 전환의 중요한 원동력으로 자리매김하고 있습니다.

"프로젝트 수명주기 부문에서는 건설 전 단계가 2025년 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. "

건설 전 단계는 프로젝트 성공의 기반 구축에 있으며, 매우 중요한 역할을 하므로 BIM 시장을 촉진할 것으로 예측됩니다. 이 단계에서 BIM은 물리적 시공이 시작되기 전에 상세한 설계 시각화, 간섭 감지, 비용 추정, 일정 수립을 가능하게 함으로써 큰 가치를 제공합니다. 이를 통해 이해관계자들은 잠재적인 설계 모순을 식별하고, 자원 배분을 최적화하며, 재작업 및 지연 가능성을 줄일 수 있습니다. 프로젝트를 예산과 기한 내에 완료해야 할 필요성이 높아지면서 AEC 기업은 계획의 정확성 향상과 이해관계자간 협력 강화를 위해 건설 전 단계에서 BIM을 활용하는 사례가 증가하고 있습니다. 또한 건설 전 단계에서의 5D/6D BIM 통합은 비용과 지속가능성에 대한 의사결정을 더욱 강화하여 BIM 채택의 중요한 단계가 되고 있습니다.

"빌딩 정보 모델링 시장에서 가장 높은 CAGR을 나타낼 것으로 예상되는 부문은 클라우드 배포형 부문입니다. "

클라우드 배포 유형은 확장성, 비용 효율성, 원격 액세스의 용이성으로 인해 BIM 시장에서 가장 높은 CAGR을 보일 것으로 예측됩니다. 클라우드 기반 BIM 솔루션은 건설 팀이 여러 장소에서 활동하는 경우가 늘어남에 따라 실시간 협업, 원활한 데이터 공유, 중앙 집중식 프로젝트 관리를 가능하게 합니다. 이러한 플랫폼은 대규모 On-Premise 인프라의 필요성을 줄여주기 때문에 특히 중소기업에게 매력적입니다. 또한 IoT, AI, 디지털 트윈과 같은 첨단 기술과의 통합은 클라우드 환경에서 더욱 원활하게 이루어지며, 더 많은 채택을 촉진할 수 있습니다. 데이터 보안과 연결성이 향상됨에 따라 클라우드 기반 BIM으로의 전환이 크게 가속화될 것으로 예측됩니다. 또한 클라우드 배포는 자동 업데이트 및 스토리지 확장성을 지원하여 팀이 항상 최신 데이터와 모델로 작업할 수 있도록 보장합니다. AEC 산업에서 원격 근무 및 하이브리드 업무 모델 증가 추세는 클라우드 기반 BIM 플랫폼에 대한 수요를 더욱 강화시키고 있습니다.

"인도는 전 세계 빌딩 정보 모델링 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

인도는 급속한 도시화, 인프라 개발의 급증, 디지털 건설 방식을 장려하는 정부 정책 증가로 인해 세계 BIM 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. Smart Cities Mission, PM Gati Shakti와 같은 프로그램은 대규모 프로젝트의 효율적인 계획과 실행에 대한 수요를 촉진하고 있으며, BIM은 여기서 중요한 역할을 하고 있습니다. 또한 AEC 전문 업체들의 인지도 향상, 부동산 및 교통 부문의 확대, 클라우드 기반/모바일 BIM 솔루션의 보급이 시장 성장을 촉진하고 있습니다. 지속가능성, 비용 효율성, 기술 현대화 추진은 국내 공공/민간 건설 프로젝트에서 BIM 도입을 더욱 촉진하고 있습니다. 국제적인 건설사들의 진출 증가와 현지 소프트웨어 프로바이더 및 스타트업의 부상으로 경쟁력 있는 가격 및 지역 특화 솔루션을 통해 BIM의 채택이 가속화되고 있습니다. 인도의 교육 기관과 산업 협회도 BIM 교육에 중점을 두고 있으며, 기술 격차를 해소하고 주류 워크플로우로의 통합을 가속화하는 데 기여하고 있습니다. 이러한 지원적인 생태계를 통해 인도는 향후 수년간 BIM의 고성장 시장으로 자리매김할 것입니다.

세계의 빌딩 인포메이션 모델링(BIM) 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요 인사이트

빌딩 인포메이션 모델링 시장의 기업에 있어서 매력적인 성장 기회

빌딩 인포메이션 모델링 시장 : 제공 유형별(2021-2030년)

빌딩 인포메이션 모델링 시장 : 프로젝트 수명주기별

빌딩 인포메이션 모델링 시장 : 업계별

빌딩 인포메이션 모델링 시장 : 지역별

제5장 시장 개요

서론

시장 역학

촉진요인

억제요인

기회

과제

고객 비즈니스에 영향을 미치는 동향/혼란

가격결정 분석

빌딩 인포메이션 모델링 소프트웨어의 참고 가격 분석

빌딩 인포메이션 모델링 소프트웨어의 가격 분석 : 지역별(2024년)

공급망 분석

에코시스템 지도제작

투자와 자금조달 시나리오

기술 분석

주요 기술

보완 기술

인접 기술

무역 분석

수입 시나리오

수출 시나리오

특허 분석

주요 컨퍼런스와 이벤트

사례 연구

관세와 규제 상황

관세 데이터

규제기관, 정부기관, 기타 조직

표준

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

빌딩 인포메이션 모델링 시장에 대한 AI의 영향

2025년 미국 관세의 영향 - 빌딩 인포메이션 모델링 시장

서론

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

수직 방향에 대한 영향

제6장 빌딩 인포메이션 모델링 시장 : 용도별

서론

계획·모델링

건설·설계

자산관리

빌딩 시스템 분석·정비 스케줄링

제7장 빌딩 인포메이션 모델링 소프트웨어 시장 : 배포 유형별

서론

온프레미스

클라우드

제8장 빌딩 인포메이션 모델링 시장 : 최종사용자별

서론

AEC 전문 업자

컨설턴트·시설 관리자

기타 최종사용자

제9장 빌딩 인포메이션 모델링 시장 : 프로젝트 수명주기별

서론

건설전

건설

운영

제10장 빌딩 인포메이션 모델링 시장 : 업계별

서론

건축

산업

토목 인프라

석유 및 가스

유틸리티

기타 업계

제11장 빌딩 인포메이션 모델링 시장 : 제공 유형별

서론

소프트웨어

설계·모델링 소프트웨어

건설 시뮬레이션·스케줄링

비용 견적·수량 산출

시설·자산관리 소프트웨어

지속가능성·에너지 분석 소프트웨어

기타 소프트웨어 유형

서비스

실장·통합 서비스

소프트웨어 지원·정비

트레이닝·인정

모델링·문서화 서비스

컨설팅·어드바이저리 서비스

기타 서비스

제12장 빌딩 인포메이션 모델링 시장 : 지역별

서론

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시경제 전망

영국

독일

프랑스

이탈리아

스페인

폴란드

북유럽

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

인도

한국

호주

인도네시아

말레이시아

태국

베트남

기타 아시아태평양

기타 지역

기타 지역의 거시경제 전망

중동

남미

아프리카

제13장 경쟁 구도

개요

주요 참여 기업의 전략/강점

매출 분석

시장 점유율 분석

기업의 평가와 재무 지표

제품의 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 구도와 동향

제품 발매

거래

확장

제14장 기업 개요

주요 기업

AUTODESK INC.

NEMETSCHEK GROUP

BENTLEY SYSTEMS, INCORPORATED

TRIMBLE INC.

DASSAULT SYSTEMES

SCHNEIDER ELECTRIC

ASITE

HEXAGON AB

PROCORE TECHNOLOGIES, INC.

ARCHIDATA INC.

기타 기업

ACCA SOFTWARE S.P.A.

PINNACLE INFOTECH

ANGULERIS

AFRY AB

BECK TECHNOLOGY

COMPUTERS AND STRUCTURES, INC.

ASUNI SOFT

4M

SIERRASOFT

SAFE SOFTWARE INC.

FARO

GEO-PLUS

CYPE INGENIEROS S.A.

MAGICAD GROUP

REVIZTO SA

제15장 부록

KSA

영문 목차

영문목차

The global building information modeling market is projected to grow from USD 9.03 billion in 2025 to USD 15.42 billion by 2030 at a CAGR of 11.3% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Offering, Deployment Type, Project Lifecycle, End User, Vertical, and Region

Regions covered

North America, Europe, APAC, RoW

The BIM market is gaining momentum due to rising demand for efficient planning, cost control, and risk reduction in construction projects. Its ability to support sustainability goals, enable real-time data integration, and align with trends like modular construction is driving adoption. Government mandates and integration with technologies like IoT, digital twins, cloud, and AI are further accelerating growth. Together, these factors are establishing BIM as a key enabler of digital transformation in the construction sector.

"Pre-construction phase in the project lifecycle segment is expected to hold the largest market share in 2025."

The pre-construction phase is expected to lead the BIM market as it plays a critical role in setting the foundation for successful project execution. BIM offers significant value during this stage by enabling detailed design visualization, clash detection, cost estimation, and scheduling, all before physical construction begins. This helps stakeholders identify potential design conflicts, optimize resource allocation, and reduce the likelihood of rework and delays. With growing pressure to deliver projects on time and within budget, AEC firms are increasingly leveraging BIM in the pre-construction phase to improve planning accuracy and stakeholder coordination. Moreover, the integration of 5D and 6D BIM in pre-construction is further enhancing decision-making related to cost and sustainability, making it a pivotal stage for BIM adoption.

"Cloud deployment type segment is projected to witness the fastest CAGR in the building information modeling market."

The cloud deployment type is expected to exhibit the fastest CAGR in the BIM market due to its scalability, cost-efficiency, and ease of remote access. As construction teams increasingly operate across multiple locations, cloud-based BIM solutions enable real-time collaboration, seamless data sharing, and centralized project management. These platforms reduce the need for heavy on-premise infrastructure, making them especially attractive to small and mid-sized firms. Moreover, integration with advanced technologies like IoT, AI, and digital twins is more seamless in the cloud environment, driving further adoption. As data security and connectivity improve, the shift toward cloud-based BIM is likely to accelerate significantly. Additionally, cloud deployment supports automatic updates and scalable storage, ensuring that teams always work with the latest data and models. The growing trend of remote and hybrid work models in the AEC industry further reinforces the demand for cloud-based BIM platforms.

"India is expected to witness the highest CAGR in the global building information modeling market."

India is expected to witness the fastest CAGR in the global BIM market due to rapid urbanization, a surge in infrastructure development, and increasing government initiatives promoting digital construction practices. Programs like Smart Cities Mission and PM Gati Shakti are driving demand for efficient planning and execution of large-scale projects, where BIM plays a vital role. Additionally, rising awareness among AEC professionals, expanding real estate and transportation sectors, and growing adoption of cloud-based and mobile BIM solutions are fueling market growth. The push for sustainability, cost-efficiency, and technological modernization is further encouraging BIM uptake across both public and private construction projects in the country. The increasing entry of international construction firms, local software providers, and startups is boosting BIM adoption through competitive pricing and localized solutions. Educational institutions and industry bodies in India are also emphasizing BIM training, helping bridge the skill gap and accelerate its integration into mainstream workflows. This supportive ecosystem positions India as a high-growth market for BIM in the coming years.

Extensive primary interviews were conducted with key industry experts in the building information modeling market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below:

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

By Designation: C-level - 40%, Managers - 30%, and Others - 30%

By Region: North America- 40%, Europe - 30%, Asia Pacific - 20%, and RoW - 10%

Autodesk Inc. (US), Nemetschek Group (Germany), Bentley Systems, Incorporated (US), Procore Technologies, Inc. (US), Trimble Inc. (US), Dassault Systemes (France), Schneider Electric (France), Hexagon AB (Sweden), Asite (UK), and Archidata Inc. (Canada) are some of the key players in the building information modeling market.

Research Coverage:

This research report categorizes the building information modeling market based on offering (software, services), deployment type (on-premises, cloud), end user (AEC professionals, consultants & facility managers, and other end users), project lifecycle (pre-construction, construction, and operation), vertical (buildings, industrial, civil infrastructure, oil & gas, utilities, and other verticals), and region (North America, Europe, Asia Pacific, and RoW). The report describes the major drivers, restraints, challenges, and opportunities pertaining to the building information modeling market and forecasts the same till 2030. Apart from this, the report also consists of leadership mapping and analysis of all the companies included in the building information modeling ecosystem.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants in this market by providing information on the closest approximations of the revenue numbers for the overall building information modeling market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (rise in urbanization and infrastructure development globally; need for real-time collaboration, improved efficiency, and project visualization across stakeholders; rising adoption of digital twin technology to enhance lifecycle management; growing emphasis on sustainability and green building certifications; increasing need for reduction in rework and errors through model-based planning), restraints (high initial implementation cost; lack of skilled BIM professionals), opportunities (convergence of AR/VR technologies with BIM workflows; leveraging IoT to enhance BIM functionality in modern construction; global harmonization of BIM standards enabling cross-border project delivery; digital skill development programs supporting workforce readiness), and challenges (hardware and infrastructure limitations in emerging markets; lack of universal BIM standards across countries; delayed digital integration within the construction ecosystem) influencing the growth of the building information modeling market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new software & service launches in the building information modeling market.

Market Development: Comprehensive information about lucrative markets - the report analyzes the building information modeling market across varied regions

Market Diversification: Exhaustive information about new software & services, untapped geographies, recent developments, and investments in the building information modeling market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, such as Autodesk Inc. (US), Nemetschek Group (Germany), Bentley Systems, Incorporated (US), Procore Technologies, Inc. (US), Trimble Inc. (US), Dassault Systemes (France), Schneider Electric (France), Hexagon AB (Sweden), Asite (UK), and Archidata Inc. (Canada), in the building information modeling market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 Key secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 Major primary interview participants

2.1.3.2 Breakdown of primaries

2.1.3.3 Key data from primary sources

2.1.3.4 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to obtain market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to obtain market size using top-down analysis (supply side)

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RISK ASSESSMENT

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE GROWTH OPPORTUNITIES FOR PLAYERS IN BUILDING INFORMATION MODELING MARKET

4.2 BUILDING INFORMATION MODELING MARKET, BY OFFERING TYPE, 2021-2030

4.3 BUILDING INFORMATION MODELING MARKET, BY PROJECT LIFECYCLE

4.4 BUILDING INFORMATION MODELING MARKET, BY VERTICAL

4.5 BUILDING INFORMATION MODELING MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rise in global urbanization and infrastructure development

5.2.1.2 Need for real-time collaboration, improved efficiency, and project visualization across stakeholders

5.2.1.3 Increase in adoption of digital twin technology to enhance lifecycle management

5.2.1.4 Growing emphasis on sustainability and green building certifications

5.2.1.5 Reduction in rework and errors through model-based planning

5.2.2 RESTRAINTS

5.2.2.1 High initial implementation cost

5.2.2.2 Lack of skilled BIM professionals

5.2.3 OPPORTUNITIES

5.2.3.1 Convergence of AR/VR technologies with BIM workflows

5.2.3.2 Leveraging IoT to enhance BIM functionality in modern construction

5.2.3.3 Global harmonization of BIM standards enabling cross-border project delivery

5.2.3.4 Digital skill development programs supporting workforce readiness

5.2.4 CHALLENGES

5.2.4.1 Hardware and infrastructure limitations in emerging markets

5.2.4.2 Lack of universal BIM standards across countries

5.2.4.3 Delayed digital integration within construction ecosystem

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 INDICATIVE PRICING ANALYSIS FOR BUILDING INFORMATION MODELING SOFTWARE

5.4.2 INDICATIVE PRICING ANALYSIS FOR BUILDING INFORMATION MODELING SOFTWARE, BY REGION, 2024

5.5 SUPPLY CHAIN ANALYSIS

5.6 ECOSYSTEM MAPPING

5.7 INVESTMENT AND FUNDING SCENARIO

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 3D Modeling

5.8.1.2 Cloud Collaboration

5.8.1.3 Clash Detection and Coordination Tools

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Cloud Computing & Edge Processing

5.8.2.2 AR/VR in BIM

5.8.3 ADJACENT TECHNOLOGY

5.8.3.1 GIS (Geographic Information System)

5.8.3.2 Digital Twin

5.9 TRADE ANALYSIS

5.9.1 IMPORT SCENARIO

5.9.2 EXPORT SCENARIO

5.10 PATENT ANALYSIS

5.11 KEY CONFERENCES AND EVENTS

5.12 CASE STUDIES

5.12.1 J C BAMFORD EXCAVATORS LTD. ACCELERATES ON-SITE COORDINATION WITH REAL-TIME BIM INTEGRATION AT ROYALMOUNT MALL

5.12.2 POPULOUS ADOPTS BIM TO STREAMLINE FACADE DESIGN AND INDUSTRIALIZE STADIUM CONSTRUCTION AT KAI TAK SPORTS PARK

5.12.3 CHINA CONSTRUCTION FIRST DIVISION GROUP ADOPTS BIM TO PRESERVE HERITAGE AND TRANSFORM CERAMICS FACTORY INTO MIXED-USE LANDMARK IN JINGDEZHEN

5.12.4 BEIJING INSTITUTE OF ARCHITECTURAL DESIGN & BEIJING CONSTRUCTION ENGINEERING GROUP ADOPT BIM TO ORCHESTRATE CULTURAL PERFORMANCE CENTER IN SUB CENTER THEATER PROJECT

5.13 TARIFFS AND REGULATORY LANDSCAPE

5.13.1 TARIFF DATA

5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13.3 STANDARDS

5.13.3.1 BS EN ISO 19650

5.13.3.1.1 BS EN ISO 19650-1

5.13.3.1.2 BS EN ISO 19650-2

5.13.3.1.3 BS EN ISO 19650-3

5.13.3.1.4 BS EN ISO 19650-5

5.14 PORTER'S FIVE FORCES ANALYSIS

5.14.1 THREAT OF NEW ENTRANTS

5.14.2 THREAT OF SUBSTITUTES

5.14.3 BARGAINING POWER OF SUPPLIERS

5.14.4 BARGAINING POWER OF BUYERS

5.14.5 INTENSITY OF COMPETITIVE RIVALRY

5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2 BUYING CRITERIA

5.16 IMPACT OF ARTIFICIAL INTELLIGENCE ON BUILDING INFORMATION MODELING MARKET

5.16.1 INTRODUCTION

5.17 IMPACT OF 2025 US TARIFF - BUILDING INFORMATION MODELING MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRY/REGION

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON VERTICAL

6 BUILDING INFORMATION MODELING MARKET, BY APPLICATION

6.1 INTRODUCTION

6.2 PLANNING & MODELING

6.3 CONSTRUCTION & DESIGN

6.4 ASSET MANAGEMENT

6.5 BUILDING SYSTEM ANALYSIS & MAINTENANCE SCHEDULING

7 BUILDING INFORMATION MODELING SOFTWARE MARKET, BY DEPLOYMENT TYPE

7.1 INTRODUCTION

7.2 ON-PREMISES

7.2.1 PREFERENCE FOR ENHANCED DATA SECURITY AND LOCALIZED CONTROL TO DRIVE GROWTH

7.3 CLOUD

7.3.1 RISING DEMAND FOR SCALABLE, COLLABORATIVE, AND COST-EFFICIENT BIM SOLUTIONS TO DRIVE MARKET

8 BUILDING INFORMATION MODELING MARKET, BY END USER

8.1 INTRODUCTION

8.2 AEC PROFESSIONALS

8.2.1 LEVERAGING BIM FOR COLLABORATIVE DESIGN, COST CONTROL, AND PROJECT EFFICIENCY

8.3 CONSULTANTS & FACILITY MANAGERS

8.3.1 ENHANCING ASSET LIFECYCLE MANAGEMENT THROUGH DATA-DRIVEN BUILDING OPERATIONS

8.4 OTHER END USERS

9 BUILDING INFORMATION MODELING MARKET, BY PROJECT LIFECYCLE

9.1 INTRODUCTION

9.2 PRE-CONSTRUCTION

9.2.1 COMPREHENSIVE EARLY-STAGE VISUALIZATION AND CLASH-FREE PROJECT COORDINATION TO DRIVE ADOPTION

9.3 CONSTRUCTION

9.3.1 DEMAND FOR ACCURATE SEQUENCING AND EFFICIENT SITE EXECUTION TO DRIVE INTEGRATION

9.4 OPERATION

9.4.1 DATA-DRIVEN FACILITY MANAGEMENT AND LIFECYCLE EFFICIENCY TO PROMOTE USAGE

10 BUILDING INFORMATION MODELING MARKET, BY VERTICAL

10.1 INTRODUCTION

10.2 BUILDINGS

10.2.1 DIGITALIZATION AND SMART INFRASTRUCTURE INITIATIVES TO DRIVE MARKET

10.2.2 COMMERCIAL

10.2.3 RESIDENTIAL

10.3 INDUSTRIAL

10.3.1 ENHANCING MANUFACTURING EFFICIENCY THROUGH INTEGRATED BIM APPLICATIONS

10.4 CIVIL INFRASTRUCTURE

10.4.1 GOVERNMENT MANDATES AND PUBLIC SECTOR SPENDING TO DRIVE BIM ADOPTION

10.5 OIL & GAS

10.5.1 COMPREHENSIVE BIM INTEGRATION FOR SAFETY, OPTIMIZATION, AND COST CONTROL TO DRIVE DEMAND

10.6 UTILITIES

10.6.1 GROWING IMPLEMENTATION TO REDUCE REWORK AND DELAYS TO DRIVE SEGMENTAL GROWTH

10.7 OTHER VERTICALS

11 BUILDING INFORMATION MODELING MARKET, BY OFFERING TYPE

11.1 INTRODUCTION

11.2 SOFTWARE

11.2.1 DESIGN & MODELING SOFTWARE

11.2.1.1 3D visualization and early coordination to boost demand

11.2.2 CONSTRUCTION SIMULATION & SCHEDULING

11.2.2.1 Model-based sequencing and 4D simulation to drive segment growth

11.2.3 COST ESTIMATION & QUANTITY TAKEOFF

11.2.3.1 Automated quantity linking and parametric costing to fuel growth

11.2.4 FACILITY & ASSET MANAGEMENT SOFTWARE

11.2.4.1 Rising need for post-construction efficiency to drive demand

11.2.5 SUSTAINABILITY AND ENERGY ANALYSIS SOFTWARE

11.2.5.1 Sustainability goals and need for green compliance to fuel demand

11.2.6 OTHER SOFTWARE TYPES

11.3 SERVICES

11.3.1 IMPLEMENTATION AND INTEGRATION SERVICES

11.3.1.1 Growing complexity in BIM environments to drive demand

11.3.2 SOFTWARE SUPPORT AND MAINTENANCE

11.3.2.1 Continuous software upgrades and user reliance to strengthen market

11.3.3 TRAINING AND CERTIFICATION

11.3.3.1 Skill development and upskilling demand to drive market

11.3.4 MODELING AND DOCUMENTATION SERVICES

11.3.4.1 Project outsourcing trends to drive demand across AEC sectors

11.3.5 CONSULTING AND ADVISORY SERVICES

11.3.5.1 Strategic digital transformation goals to drive demand

11.3.6 OTHER SERVICES

12 BUILDING INFORMATION MODELING MARKET, BY REGION

12.1 INTRODUCTION

12.2 NORTH AMERICA

12.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

12.2.2 US

12.2.2.1 Advancing BIM adoption through technological investment and federal programs to drive market

12.2.3 CANADA

12.2.3.1 BIM implementation in most public projects to drive demand

12.2.4 MEXICO

12.2.4.1 Urbanization and policy push to lead to gradual expansion of BIM adoption

12.3 EUROPE

12.3.1 EUROPE: MACROECONOMIC OUTLOOK

12.3.2 UK

12.3.2.1 Government mandates to implement BIM to fuel growth

12.3.3 GERMANY

12.3.3.1 Government initiatives and pilot projects to drive market

12.3.4 FRANCE

12.3.4.1 Support for adoption of BIM by French Building Federation and other such organizations to drive demand

12.3.5 ITALY

12.3.5.1 Growing BIM adoption across construction projects to drive demand

12.3.6 SPAIN

12.3.6.1 Cost savings and efficiency, especially in upcoming projects, to increase deployment

12.3.7 POLAND

12.3.7.1 EU alignment and public procurement reforms to drive growth

12.3.8 NORDICS

12.3.8.1 Advanced BIM integration driven by early mandates and strong public-private collaboration

12.3.9 REST OF EUROPE

12.4 ASIA PACIFIC

12.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

12.4.2 CHINA

12.4.2.1 Growing government initiatives to address slow adoption by fragmented construction industry to drive demand

12.4.3 JAPAN

12.4.3.1 Growing adoption of BIM solutions in residential construction to drive demand

12.4.4 INDIA

12.4.4.1 Growing adoption of sustainability software within construction sector to drive demand

12.4.5 SOUTH KOREA

12.4.5.1 Government mandates for use of BIM in public domain projects

12.4.6 AUSTRALIA

12.4.6.1 Government-led frameworks and industry partnerships to drive growth

12.4.7 INDONESIA

12.4.7.1 Rising BIM integration across public works and smart city initiatives to drive market

12.4.8 MALAYSIA

12.4.8.1 Regulatory mandates and digital transformation efforts to drive demand

12.4.9 THAILAND

12.4.9.1 Governmental support and pilot initiatives to drive demand

12.4.10 VIETNAM

12.4.10.1 Government directives and international collaboration to drive BIM adoption

12.4.11 REST OF ASIA PACIFIC

12.5 REST OF THE WORLD (ROW)

12.5.1 ROW: MACROECONOMIC OUTLOOK

12.5.2 MIDDLE EAST

12.5.2.1 Bahrain

12.5.2.1.1 Bahrain leverages BIM for urban modernization

12.5.2.2 Kuwait

12.5.2.2.1 Kuwait integrates BIM in national housing and transport projects

12.5.2.3 Oman

12.5.2.3.1 Oman explores digital transformation in construction

12.5.2.4 Qatar

12.5.2.4.1 Qatar advances BIM for FIFA infrastructure legacy

12.5.2.5 Saudi Arabia

12.5.2.5.1 Saudi Arabia incorporates BIM in giga-projects

12.5.2.6 UAE

12.5.2.6.1 UAE strengthens digital construction mandates

12.5.2.7 Rest of Middle East

12.5.3 SOUTH AMERICA

12.5.3.1 Brazil

12.5.3.1.1 Brazil drives BIM standardization through government mandate

12.5.3.2 Argentina

12.5.3.2.1 Argentina sees early adoption in public infrastructure

12.5.3.3 Other South American Countries

12.5.4 AFRICA

12.5.4.1 South Africa

12.5.4.1.1 Private sector innovation and academic collaboration to drive market

12.5.4.2 Other African countries

13 COMPETITIVE LANDSCAPE

13.1 OVERVIEW

13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

13.3 REVENUE ANALYSIS

13.4 MARKET SHARE ANALYSIS

13.5 COMPANY VALUATION AND FINANCIAL METRICS

13.6 PRODUCT COMPARISON

13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.7.1 STARS

13.7.2 EMERGING LEADERS

13.7.3 PERVASIVE PLAYERS

13.7.4 PARTICIPANTS

13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024