정밀 임업 시장 예측(-2030년) : 오퍼링별, 기술별, 용도별, 시스템 아키텍처별, 소유권 유형별, 최종사용자별, 지역별

Precision Forestry Market by Offering, by Technology, Application, End User and Region - Global Forecast to 2030

상품코드:1863602

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 278 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

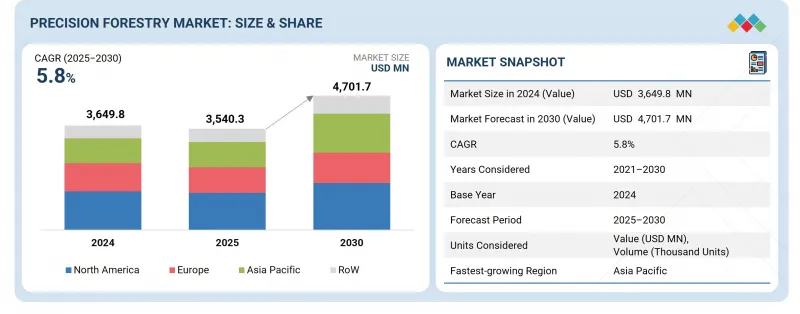

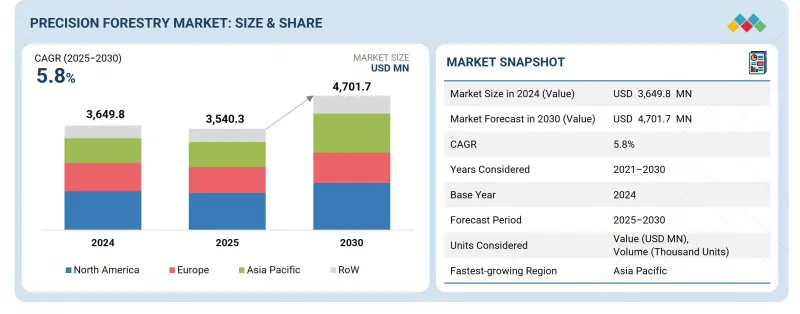

정밀 임업 시장 규모는 2025년 35억 4,030만 달러에서 2030년까지 47억 107만 달러에 달할 것으로 예측되고 있으며, CAGR은 5.8%로 전망되고 있습니다.

조사 범위

조사 대상 기간

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

대상 단위

금액(10억 달러)

부문

오퍼링별, 기술별, 용도별, 시스템 아키텍처별, 소유권 유형별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

정밀 임업 시장의 성장은 효율성, 생산성 및 탄소 관리를 향상시키는 첨단 기술, 지속가능한 임업 관행, AI를 활용한 솔루션의 도입 확대에 의해 촉진되고 있습니다.

세계 정밀 임업 시장은 산업 임업 기업, 정부 기관, 환경 및 보존 단체, 상업용 산림 소유자의 정밀 임업 기술 채택 증가에 힘입어 예측 기간 중 상당한 성장을 보일 것으로 예측됩니다. 산업 임업 기업은 실시간 데이터와 분석을 통해 벌채 활동의 효율성, 수확량 극대화, 공급망 효율성 강화를 위해 정밀 임업 솔루션의 도입을 확대하고 있습니다. 정부 기관은 디지털 매핑, 원격 감지 및 분석 플랫폼을 활용하여 산림 보전, 화재 감지 및 재조림 프로그램을 강화하고 있습니다. 환경 및 보전 분야에서는 탄소 모니터링, 생물다양성 평가, 지속가능한 토지 이용 계획을 위한 정밀 임업 툴을 도입하고 있습니다. 한편, 상업용 산림 소유주들은 생산성을 극대화하기 위해 나무 건강 모니터링, 병해충 관리, 토양 분석에 정밀 기술을 활용한 접근 방식을 채택하고 있습니다. 이러한 분야는 정밀 임업 기술이 다양한 용도로 통합되고 있음을 보여주며, 전 세계에서 지속가능하고 효율적인 데이터베이스 산림 관리를 실현하는 중요한 기반 기술로 자리매김하고 있습니다.

벌목 및 작업 부문은 GPS/GNSS, LiDAR, 차량용 센서 등 첨단 기술의 보급으로 2024년 가장 큰 시장 점유율을 차지했습니다. 이러한 기술은 벌목 및 현장 작업의 정확성, 생산성, 지속가능성을 향상시킵니다. 임업 기업은 스마트 수확기, 포워더, 텔레매틱스 지원 장비를 적극적으로 활용하여 기계 성능 최적화, 목재 폐기물 감소, 지속가능한 산림 관리 확보를 추진하고 있습니다. 또한 환경 규제 준수와 업무 효율화에 대한 관심이 높아지면서 지형 매핑, 기계 경로 계획, 실시간 모니터링을 위한 데이터베이스 툴이 통합되어 벌채 및 작업 분야는 정밀 임업에서 가장 성숙하고 광범위하게 도입이 진행되고 있는 용도입니다.

정밀 임업 시장에서 고정식/고정식 시스템 부문은 예측 기간 중 높은 CAGR을 나타낼 것으로 예측됩니다. 이는 산림 지역 전체에 영구적인 모니터링 및 센싱 데이터 수집 인프라의 도입 증가가 주요 요인으로 작용하고 있습니다. 지상 설치형 LiDAR 스캐너, 환경 센서, 고정형 카메라 네트워크 등을 포함한 이러한 시스템은 산림 건강 평가, 바이오매스 추정, 화재 감지를 위한 지속적이고 정확한 데이터 수집을 가능하게 합니다. 실시간 환경 모니터링을 위한 IoT 지원 고정형 시스템 도입 확대와 클라우드 기반 데이터 분석 및 자동화의 발전이 결합되어 이러한 시스템에 대한 수요를 견인하고 있습니다. 또한 정부 및 임업 기관이 장기적인 생태계 관리 및 삼림 벌채 추적을 위해 고정형 시스템에 투자하고 있는 것도 이동형 및 휴대용 시스템에 비해 이 부문의 성장을 가속화하고 있습니다.

북미는 첨단 산림관리 기술의 조기 도입과 Deere & Company(미국), Trimble Inc(미국), Caterpillar(미국), Tigercat International Inc(캐나다) 등 주요 정밀 임업 솔루션 프로바이더들의 강력한 입지를 바탕으로 2024년 정밀 임업 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 등 정밀 임업 솔루션을 제공하는 주요 기업의 강력한 존재감으로 2024년 정밀 임업 시장에서 가장 큰 점유율을 확보했습니다. 이 지역의 잘 구축된 디지털 인프라와 높은 투자 능력은 GPS/GNSS, GIS, 드론, LiDAR, 고급 데이터 분석과 같은 기술의 임업 업무에 대한 통합을 가속화하고 있습니다. 또한 미국과 캐나다의 정부 정책에 힘입어 지속가능한 산림 관리에 대한 관심이 높아지면서 벌채 최적화, 폐기물 감소, 산림 건강성 향상을 위한 정밀 임업 툴의 도입이 촉진되고 있습니다. 주요 임업 기계 제조업체와 기술 프로바이더의 존재는 이 시장에서 북미의 우위를 더욱 공고히 하고 있습니다.

주요 기업 분석

세계의 정밀 임업 시장에 대해 조사했으며, 오퍼링별, 기술별, 용도별, 시스템 아키텍처별, 소유권 유형별, 최종사용자별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

서론

시장 역학

고객 비즈니스에 영향을 미치는 동향/혼란

가격 분석

공급망 분석

에코시스템 분석

투자와 자금조달 시나리오

기술 분석

무역 분석

특허 분석

2025-2026년의 주요 컨퍼런스와 이벤트

사례 연구 분석

관세와 규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

AI/생성형 AI의 영향

2025년 미국 관세가 정밀 임업 시장에 미치는 영향

제6장 정밀 임업 시장(오퍼링별)

서론

하드웨어

소프트웨어

서비스

제7장 정밀 임업 시장(기술별)

서론

스마트 하베스팅/CTL

재고 및 수율 모니터링

화재 감지

지리공간

IoT

로봇 공학과 센서

기타

제8장 정밀 임업 시장(용도별)

서론

삼림 관리와 계획

수확과 작업

임업

화재 관리와 탐지

재고·물류 관리

환경과 보전

삼림 재생과 식림

해충·질병 관리

토양 검사

야생 생물 생식지 관리

유전학

기타

제9장 정밀 임업 시장(시스템 아키텍처별)

서론

고정식/고정형 시스템

모바일/핸드헬드 시스템

제10장 정밀 임업 시장(소유권 유형별)

서론

산업 임업 회사

상업림 소유주

소규모 토지 소유주/사유림 소유주

제11장 정밀 임업 시장(최종사용자별)

서론

정부기관

임업 회사

농업 협동 조합

비영리단체

기타

제12장 정밀 임업 시장(지역별)

서론

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시경제 전망

영국

독일

프랑스

이탈리아

스페인

폴란드

북유럽

러시아

기타

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

한국

인도

호주

인도네시아

말레이시아

태국

베트남

기타

기타 지역

기타 지역의 거시경제 전망

중동

아프리카

남미

제13장 경쟁 구도

서론

주요 참여 기업의 전략/강점, 2021-2025년

매출 분석, 2021-2024년

시장 점유율 분석, 2024년

기업 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 참여 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제14장 기업 개요

주요 참여 기업

DEERE & COMPANY

PONSSE OYJ

KOMATSU LTD.

TRIMBLE INC.

CATERPILLAR

TIGERCAT INTERNATIONAL INC.

ROTTNE

ECO LOG

TOPCON

SAMPO ROSENLEW OY

기타 기업

TREEMETRICS

HITACHI CONSTRUCTION MACHINERY CO., LTD.

INSIGHT ROBOTICS

KESLA

HUSQVARNA GROUP

ASTEC INDUSTRIES, INC.

NV5GLOBAL, INC.

BOBCAT COMPANY

OREGON TOOL, INC.

ARBORPRO

FIELD TRUTH INC

SATPALDA

TREEVIA FOREST TECHNOLOGIES

AB VOLVO

STORA ENSO

제15장 부록

KSA

영문 목차

영문목차

The precision forestry market is projected to reach USD 4,701.07 million by 2030 from USD 3,540.3 million in 2025, at a CAGR of 5.8%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Offering, Technology, Application, End User and Region

Regions covered

North America, Europe, APAC, RoW

The growth of the precision forestry market is driven by increasing adoption of advanced technologies, sustainable forestry practices, and AI-enabled solutions that enhance efficiency, productivity, and carbon management.

" Widespread application of precision forestry solutions across stakeholder group to drive market"

The global precision forestry market is projected to grow significantly during the forecast period, supported by the increasing adoption of precision forestry technologies by industrial forestry companies, government agencies, environmental & conservation organizations, and commercial forest owners. Industrial forestry companies are increasingly adopting precision forestry solutions to streamline harvesting activities, maximize yield, and strengthen supply chain efficiency through real-time data and analytics. Government agencies are leveraging digital mapping, remote sensing, and analytics platforms to strengthen forest conservation, fire detection, and reforestation programs. The environmental and conservation sector is deploying precision forestry tools for carbon monitoring, biodiversity assessment, and sustainable land-use planning. Meanwhile, commercial forest owners are utilizing precision-driven approaches for tree health monitoring, pest and disease management, and soil analysis to maximize productivity. Together, these segments highlight the growing integration of precision forestry technologies across diverse applications, positioning them as key enablers of sustainable, efficient, and data-driven forest management worldwide.

"Harvesting & operations segment accounted for largest market share in 2024"

The harvesting & operations segment captured the largest market share in 2024 due to the widespread adoption of advanced technologies, such as GPS/GNSS, LiDAR, and onboard sensors, which enhance precision, productivity, and sustainability in timber extraction and field operations. Forestry companies are increasingly leveraging smart harvesters, forwarders, and telematics-enabled equipment to optimize machine performance, reduce wood waste, and ensure sustainable forest management. Additionally, growing emphasis on environmental compliance and operational efficiency has led to the integration of data-driven tools for terrain mapping, machine routing, and real-time monitoring, making harvesting and operations the most mature and extensively implemented application segment in precision forestry.

"Fixed/stationary systems segment to record higher CAGR during forecast period"

The fixed/stationary systems segment is expected to register a higher CAGR during the forecast period in the precision forestry market, driven by the increasing deployment of permanent monitoring, sensing, and data collection infrastructures across forested areas. These systems, which include ground-based LiDAR scanners, environmental sensors, and fixed camera networks, enable continuous and high-accuracy data gathering for forest health assessment, biomass estimation, and fire detection. The increasing adoption of IoT-enabled fixed systems for real-time environmental monitoring, combined with advancements in cloud-based data analytics and automation, is driving demand for these systems. Furthermore, government and forestry agencies are investing in fixed systems for long-term ecosystem management and deforestation tracking, further supporting the segment's accelerated growth compared to mobile or portable systems.

"North America accounted for largest market share in 2024"

North America secured the largest share of the precision forestry market in 2024 due to the early adoption of advanced forestry management technologies and the strong presence of leading companies offering precision forestry solutions, such as Deere & Company (US), Trimble Inc. (US), Caterpillar (US), and Tigercat International Inc. (Canada). The region's well-established digital infrastructure and high investment capacity have accelerated the integration of technologies such as GPS/GNSS, GIS, drones, LiDAR, and advanced data analytics in forestry operations. Additionally, the growing emphasis on sustainable forest management, supported by government initiatives in the US and Canada, has increased the adoption of precision forestry tools for optimizing harvesting, reducing waste, and improving forest health. The presence of major forestry equipment manufacturers and technology providers further strengthens North America's dominance in this market.

Breakdown of Primaries

A variety of executives from key organizations operating in the precision forestry market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

By Company Type: Tier 1-35%, Tier 2- 40%, and Tier 3-25%

By Designation: C-level Executives-30%, Directors-40%, and Others-30%

By Region: North America-40%, Europe-32%, Asia Pacific-23%, and RoW-5%

Note: Other designations include sales, marketing, and product managers.

Tier 1 companies include market players with revenues above USD 500 million; tier 2 companies earn revenues between USD 100 million and USD 500 million; and tier 3 companies earn revenues up to USD 100 million.

The precision forestry market is dominated by globally established players such as Deere & Company (US), Ponsse Oyj (Finland), Trimble Inc. (US), Komatsu Ltd. (Japan), Caterpillar (US), Topcon (US), Rottne (Sweden), Tigercat International Inc. (Canada), and Eco Log (Sweden). The study includes an in-depth competitive analysis of these key players in the precision forestry market, with their company profiles, recent developments, and key market strategies.

Study Coverage

The report segments the precision forestry market and forecasts its size by offering, technology, application, system architecture, ownership type, end user, and region. It also discusses the market's drivers, restraints, opportunities, and challenges, and gives a detailed view of the market across four main regions: North America, Europe, Asia Pacific, and RoW. The report includes a supply chain analysis and the key players and their competitive analysis in the precision forestry ecosystem.

Key Benefits of Buying the Report

Analysis of key drivers (Growing adoption of remote sensing and GIS technologies, rising requirement for sustainable forestry practices, elevating demand for timber and wood-based products, and escalating need to adopt sustainable forest management techniques), restraints (High initial investment and operational costs, and geographical and environmental limitations), opportunities (Inclination toward AI-driven predictive analytics for forest management, integration of blockchain technology to ensure transparency in wood supply chain, and implementation of carbon credit and carbon offset programs), and challenges (Limited awareness of benefits offered by precision forestry solutions, and delayed ROI in precision forestry technologies) influencing the growth of the precision forestry market

Products/Solution/Service Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and product/solution/service launches in the precision forestry market

Market Development: Comprehensive information about lucrative markets-the report analyzes the precision forestry market across varied regions

Market Diversification: Exhaustive information about new products/solutions/services, untapped geographies, recent developments, and investments in the precision forestry market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Deere & Company (US), Ponsse Oyj (Finland), Trimble Inc. (US), Komatsu Ltd. (Japan), and Caterpillar (US), among others

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.1.2 List of key secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 List of key primary interview participants

2.1.2.3 Breakdown of primaries

2.1.2.4 Key industry insights

2.1.3 SECONDARY AND PRIMARY RESEARCH

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PRECISION FORESTRY MARKET

4.2 PRECISION FORESTRY MARKET, BY END USER

4.3 PRECISION FORESTRY MARKET, BY TECHNOLOGY

4.4 PRECISION FORESTRY MARKET, BY APPLICATION

4.5 PRECISION FORESTRY MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing adoption of remote sensing and GIS technologies

5.2.1.2 Rising requirement for sustainable forestry practices

5.2.1.3 Elevating demand for timber and wood-based products

5.2.1.4 Escalating need to adopt sustainable forest management techniques

5.2.2 RESTRAINTS

5.2.2.1 High initial investment and operational costs

5.2.2.2 Geographical and environmental limitations

5.2.3 OPPORTUNITIES

5.2.3.1 Inclination toward AI-driven predictive analytics for forest management

5.2.3.2 Integration of blockchain technology to ensure transparency in wood supply chain

5.2.3.3 Implementation of carbon credit and carbon offset programs

5.2.4 CHALLENGES

5.2.4.1 Limited awareness of benefits offered by precision forestry solutions

5.2.4.2 Delayed ROI in precision forestry technologies

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE TREND OF HARDWARE OFFERINGS, BY KEY PLAYER, 2020-2024

5.4.2 AVERAGE SELLING PRICE TREND OF HARVESTERS, BY REGION, 2020-2024

5.5 SUPPLY CHAIN ANALYSIS

5.6 ECOSYSTEM ANALYSIS

5.7 INVESTMENT AND FUNDING SCENARIO

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Forest management information systems (FMIS)