자동차용 반도체 시장 예측(-2030년) : 컴포넌트별, 차종별, 추진 방식별, 재료별, 용도별, 지역별

Automotive Semiconductor Market By Component, Vehicle Type (Light Commercial Vehicle, Heavy Commercial Vehicle ), Propulusion Type (Internal Combustion Engine, Electric), Application, Material and Region - Global Forecast to 2030

상품코드:1863600

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 299 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

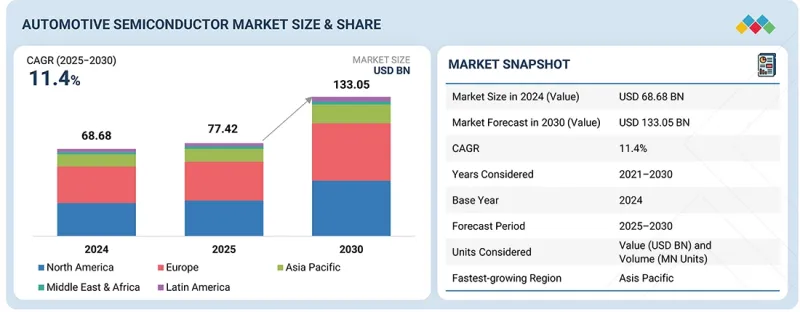

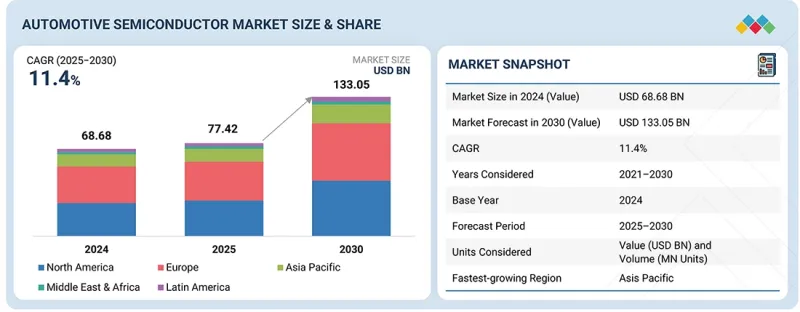

자동차용 반도체 시장 규모는 2025년 774억 2,000만 달러에서 2030년까지 1,330억 5,000만 달러로 성장하며, 2025-2030년 연평균 성장률(CAGR)은 11.4%로 예측됩니다.

자동차의 전동화 전환 가속화, 첨단운전자보조시스템(ADAS)의 통합 확대, 커넥티드카 및 소프트웨어 정의 차량의 급증에 힘입어 시장은 빠르게 성장하고 있습니다.

조사 범위

조사 대상 기간

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

대상 단위

금액(10억 달러)

부문

컴포넌트별, 차종별, 추진 방식별, 재료별, 용도별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

차량 당 반도체 탑재량 증가와 실리콘 카바이드(SiC) 및 질화갈륨(GaN) 기술의 발전으로 에너지 효율, 안전성, 성능이 향상되고 있습니다. 전기자동차(EV)의 생산 확대, 자율주행 기능의 도입, 지속가능한 모빌리티를 촉진하기 위한 정부의 구상은 시장 성장을 더욱 촉진하고 있습니다. 그러나 공급망 혼란과 높은 생산비용은 여전히 주요한 과제이며, 장기적인 경쟁력을 유지하기 위해서는 협력, 현지화, 혁신의 필요성이 강조되고 있습니다.

예측 기간 중 자동차용 반도체 시장에서 전기자동차 부문이 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이는 전 세계에서 클린 모빌리티로의 전환 가속화와 엄격한 배출가스 규제가 주요 요인으로 작용하고 있습니다. 전기자동차는 추진 시스템과 제어 시스템 전반에서 효율적인 전력 변환, 배터리 관리, 에너지 최적화를 위해 반도체에 크게 의존하고 있습니다. 우수한 스위칭 효율, 열 성능, 컴팩트한 디자인을 구현하는 실리콘 카바이드(SiC) 및 질화갈륨(GaN) 소재 기반의 파워 디바이스의 채택이 확대되고 있으며, 이는 항속거리 연장과 고속 충전의 실현을 돕고 있습니다. 첨단 센서, 마이크로컨트롤러, 통신 칩은 전기 파워트레인내 안전, 연결성, 실시간 제어를 더욱 강화합니다. 첨단운전자보조시스템(ADAS), V2X(차량간/물체간 통신), 지능형 열관리 시스템 도입 확대로 EV 1대당 반도체 탑재량이 증가하고 있습니다. 또한 정부의 보조금 정책, 인프라 투자, 아시아태평양, 유럽, 북미의 기가팩토리 확대로 EV용 반도체 공급망이 강화되고 있습니다. 자동차 제조업체들이 소프트웨어 정의 및 자율주행 전기자동차 아키텍처에 대한 투자를 늘리고 있는 가운데, 반도체 기술 혁신은 전 세계에서 지속가능하고 효율적이며 고성능의 전기 모빌리티를 구현하는 데 있으며, 핵심적인 역할을 할 것으로 보입니다.

파워트레인 분야는 차량 전동화로의 전환 가속화와 첨단 제어기술의 통합을 배경으로 2030년 자동차용 반도체 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 시장 성장은 주로 엔진 관리 시스템, 변속기 제어 장치, 배터리 관리 시스템(BMS), 전기 구동 모듈에 반도체의 채택이 확대되면서 효율성 향상, 배기가스 감소, 성능 강화를 실현하는 데 힘입어 성장하고 있습니다. 전기자동차 및 하이브리드차의 보급 확대에 따라 고전압 동작, 고속 스위칭, 우수한 열 성능을 구현하는 파워 반도체(실리콘 카바이드(SiC) 및 질화갈륨(GaN) 소자)에 대한 수요가 급증하고 있습니다. 또한 자동차 제조업체들은 실시간 모니터링, 예지보전, 에너지 최적화 기능을 통합한 스마트 파워트레인 아키텍처를 중시하고 있으며, 이로 인해 차량당 반도체 탑재량이 더욱 증가하고 있습니다. 800V 차량 플랫폼의 확대와 모듈형 파워 일렉트로닉스로의 전환도 인버터, 차량용 충전기, DC-DC 컨버터에서 반도체 솔루션의 채택 확대에 기여하고 있습니다. 그 결과, 파워트레인 분야는 계속해서 중요한 수입원이 되고 있으며, 반도체 공급업체들은 OEM의 진화하는 전동화 및 지속가능성 요구사항을 충족시키기 위해 재료 혁신, 시스템 소형화, 고효율 설계에 많은 투자를 하고 있습니다.

예측 기간 중 유럽은 자동차용 반도체 시장에서 두 번째로 높은 CAGR을 나타낼 것으로 예측됩니다. 이는 전기 모빌리티, 차량 안전 기술, 자동차 산업 전반의 디지털 전환의 강력한 발전에 힘입은 것입니다. 이 지역에는 주요 자동차 제조업체와 1차 협력업체들이 위치해 있으며, 전동화, ADAS, 커넥티비티 용도를 위한 반도체 채택을 가속화하고 있습니다. 엄격한 이산화탄소(CO2) 배출 규제와 유럽 그린딜(Green Deal)에 따른 전기자동차와 하이브리드차의 생산 증가는 전력반도체, 센서, 마이크로컨트롤러에 대한 수요를 증가시키고 있습니다. 독일, 프랑스, 네덜란드 등의 국가들은 전기자동차 인프라, 자율주행 시험, 반도체 연구개발에 대한 정부 자금 지원을 통해 혁신을 주도하고 있습니다. 또한 칩 제조업체와 자동차 OEM 업체 간의 협력 관계는 지역 기반 공급망과 차세대 E/E 아키텍처 구축을 촉진하고 있습니다. 이러한 요인들이 복합적으로 작용하여 이 지역은 세계 자동차용 반도체 환경에서 기술 혁신과 지속가능한 성장의 주요 거점으로서 입지를 구축했습니다.

자동차용 반도체 시장의 주요 참가자들의 프로파일은 다음과 같습니다.

세계의 자동차용 반도체 시장에 대해 조사했으며, 컴포넌트별, 차종별, 추진 방식별, 재료별, 용도별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

서론

시장 역학

밸류체인 분석

에코시스템 분석

투자와 자금조달 시나리오

고객 비즈니스에 영향을 미치는 동향/혼란

기술 분석

가격 분석

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

무역 분석

특허 분석

관세와 규제 상황

2025-2026년의 주요 컨퍼런스와 이벤트

AI/생성형 AI가 자동차용 반도체 시장에 미치는 영향

2025년 미국 관세가 자동차용 반도체 시장에 미치는 영향

제6장 자동차용 반도체 시장(컴포넌트별)

서론

프로세서

아날로그 IC

디스크리트 파워 디바이스

센서

메모리

기타

제7장 자동차용 반도체 시장(차종별)

서론

승용차

소형 상용차(LCVS)

대형 상용차(HCVS)

제8장 자동차용 반도체 시장(추진 방식별)

서론

내연기관(ICE)

전기

제9장 자동차용 반도체 시장(재료별)

서론

실리콘(SI)

탄화규소(SIC)

질화갈륨(GAN)

기타

제10장 자동차용 반도체 시장(용도별)

서론

파워트레인

안전성

보디 일렉트로닉스

섀시

텔레매틱스와 인포테인먼트

ADAS와 자율주행

제11장 자동차용 반도체 시장(지역별)

서론

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

폴란드

네덜란드

북유럽

기타

아시아태평양

아시아태평양의 거시경제 전망

중국

인도

일본

한국

호주

대만

동남아시아

기타

기타 지역

기타 지역의 거시경제 전망

남미

아프리카

중동

제12장 경쟁 구도

개요

주요 참여 기업의 전략/강점, 2021-2025년

시장 점유율 분석, 2024년

매출 분석, 2020-2024년

기업 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 참여 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제13장 기업 개요

서론

주요 참여 기업

INFINEON TECHNOLOGIES AG

NXP SEMICONDUCTORS

STMICROELECTRONICS

TEXAS INSTRUMENTS INCORPORATED

RENESAS ELECTRONICS CORPORATION

SEMICONDUCTOR COMPONENTS INDUSTRIES, LLC

ROBERT BOSCH GMBH

QUALCOMM TECHNOLOGIES, INC.

ANALOG DEVICES, INC.

기타 기업

TE CONNECTIVITY

ROHM CO., LTD.

APTIV

CTS CORPORATION

AUTOLIV

ZF FRIEDRICHSHAFEN AG

QUANERGY SOLUTIONS, INC.

TOSHIBA CORPORATION

MAGNA INTERNATIONAL INC.

MELEXIS

AMPHENOL CORPORATION

VALEO

CONTINENTAL AG

BROADCOM

ELMOS SEMICONDUCTOR SE

VISHAY INTERTECHNOLOGY, INC.

NUVOTON TECHNOLOGY CORPORATION

XILINX

BORGWARNER INC.

DENSO CORPORATION

SENSATA TECHNOLOGIES, INC.

제14장 부록

KSA

영문 목차

영문목차

The automotive semiconductor market is projected to grow from USD 77.42 billion in 2025 to USD 133.05 billion by 2030, at a CAGR of 11.4% between 2025 and 2030. Driven by the accelerating transition toward vehicle electrification, the rising integration of advanced driver-assistance systems (ADAS), and the surge in connected and software-defined vehicles, the market continues to expand rapidly.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Component, Vehicle Type, Material, Application and Region

Regions covered

North America, Europe, APAC, RoW

Increasing semiconductor content per vehicle and advancements in silicon carbide (SiC) and gallium nitride (GaN) technologies enhance energy efficiency, safety, and performance. Expanding EV production, adoption of autonomous features, and government initiatives promoting sustainable mobility further stimulate market growth. However, supply chain disruptions and high production costs remain key challenges, emphasizing the need for collaboration, localization, and innovation to sustain long-term competitiveness.

"By propulsion type, the electric segment is likely to register the highest CAGR between 2025 and 2030."

The electric segment is projected to record the highest CAGR in the automotive semiconductor market during the forecast period, driven by the accelerating global transition toward clean mobility and stringent emission regulations. EVs rely heavily on semiconductors for efficient power conversion, battery management, and energy optimization across propulsion and control systems. Power devices based on silicon carbide (SiC) and gallium nitride (GaN) materials are increasingly adopted for superior switching efficiency, thermal performance, and compact design, supporting higher driving ranges and faster charging. Advanced sensors, microcontrollers, and communication chips further enhance safety, connectivity, and real-time control within electric powertrains. The growing deployment of ADAS, vehicle-to-everything (V2X) communication, and intelligent thermal management systems expands semiconductor content per EV. Additionally, government incentives, infrastructure investments, and the scaling of gigafactories across Asia Pacific, Europe, and North America are strengthening the EV semiconductor supply chain. As automakers invest in software-defined and autonomous EV architectures, semiconductor innovations will remain central to achieving worldwide sustainable, efficient, high-performance electric mobility.

"Based on application, the powertrain segment is projected to account for the largest market share in 2030."

The powertrain segment is projected to hold the largest share of the automotive semiconductor market in 2030, driven by the accelerating shift toward vehicle electrification and the integration of advanced control technologies. Market growth is primarily supported by the rising deployment of semiconductors in engine management systems, transmission control units, battery management systems (BMS), and electric drive modules, enabling improved efficiency, reduced emissions, and enhanced performance. With the increasing adoption of electric and hybrid vehicles, demand for power semiconductors-silicon carbide (SiC) and gallium nitride (GaN) devices-surges due to their ability to support higher voltage operations, faster switching, and superior thermal performance. Additionally, automakers emphasize smart powertrain architectures integrating real-time monitoring, predictive maintenance, and energy optimization features, further increasing semiconductor content per vehicle. The expansion of 800 V vehicle platforms and the move toward modular power electronics also contribute to the growing use of semiconductor solutions in inverters, onboard chargers, and DC-DC converters. As a result, the powertrain segment remains a critical revenue driver, with semiconductor suppliers investing heavily in material innovation, system miniaturization, and high-efficiency designs to meet OEMs' evolving electrification and sustainability requirements.

"Europe is projected to exhibit the second-highest CAGR from 2025 to 2030."

During the forecast period, Europe is expected to register the second-highest CAGR in the automotive semiconductor market, driven by strong advancements in electric mobility, vehicle safety technologies, and digital transformation across the automotive sector. The region hosts leading automakers and Tier-1 suppliers, accelerating the adoption of semiconductors for electrification, ADAS, and connectivity applications. Increasing production of electric and hybrid vehicles, supported by stringent carbon dioxide (CO2) emission regulations and the European Green Deal, boosts the demand for power semiconductors, sensors, and microcontrollers. Countries such as Germany, France, and the Netherlands are leading in innovation, supported by government funding for EV infrastructure, autonomous driving trials, and semiconductor R&D. Moreover, collaborations between chipmakers and automotive OEMs foster localized supply chains and next-generation E/E architectures. These factors collectively position the region as a major hub for technological innovation and sustainable growth in the global automotive semiconductor landscape.

The break-up of the profile of primary participants in the automotive semiconductor market-

By Company Type: Tier 1 - 35%, Tier 2 - 45%, Tier 3 - 20%

By Region: North America - 40%, Europe - 20%, Asia Pacific - 30%, RoW - 10%

Note: Other designations include sales, marketing, and product managers.

The three tiers of the companies are based on their total revenues as of 2024: Tier 1: >USD 1 billion, Tier 2: USD 500 million-1 billion, and Tier 3: USD 500 million.

The major players in the automotive semiconductor market with a significant global presence include Infineon Technologies AG (Germany), NXP Semiconductors (Netherlands), STMicroelectronics (Switzerland), Texas Instruments Incorporated (US), and Renesas Electronics Corporation (Japan).

Research Coverage

The report segments the automotive semiconductor market and forecasts its size by component, vehicle type, propulsion type, application, and region. It also comprehensively reviews drivers, restraints, opportunities, and challenges influencing market growth. The report covers qualitative aspects in addition to quantitative aspects of the market.

Reasons to buy the report:

The report will help the market leaders/new entrants with information on the closest approximate revenues for the overall automotive semiconductor market and related segments. This report will help stakeholders understand the competitive landscape and gain more insights to strengthen their position in the market and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

Analysis of key drivers (rising vehicle electrification to curb emissions, rapid advances in ADAS and autonomous driving technologies, evolution of connected and software-defined vehicle ecosystem), restraints (high development and qualification costs, supply chain and capacity constraints), opportunities (localization and development of semiconductor ecosystem, rising development of ai-driven domain controllers and edge computing solutions, mounting demand for fast-charging and vehicle-to-grid infrastructure), and challenges (issues in scaling wide-bandgap semiconductor production for automotive applications, challenges in meeting rigorous standards related to automotive systems, complexities associated with semiconductor integration)

Product development/innovation: Detailed insights on upcoming technologies, research & development activities, and strategies, such as new product launches, collaborations, partnerships, expansions, and acquisitions, in the automotive semiconductor market

Market development: Comprehensive information about lucrative markets-the report analyses the automotive semiconductor market across varied regions

Market diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the automotive semiconductor market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, including Infineon Technologies AG (Germany), NXP Semiconductors (Netherlands), STMicroelectronics (Switzerland), Texas Instruments Incorporated (US), Renesas Electronics Corporation (Japan), Semiconductor Components Industries, LLC (US), Robert Bosch GmbH (Germany), Qualcomm Technologies, Inc. (US), Analog Devices, Inc. (US), and Microchip Technology Inc. (US)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 YEARS CONSIDERED

1.3.3 INCLUSIONS AND EXCLUSIONS

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 List of key secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 List of primary interview participants

2.1.3.2 Breakdown of primaries

2.1.3.3 Key data from primary sources

2.1.3.4 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE SEMICONDUCTOR MARKET

4.2 AUTOMOTIVE SEMICONDUCTOR MARKET, BY COMPONENT

4.3 AUTOMOTIVE SEMICONDUCTOR MARKET, BY VEHICLE TYPE

4.4 AUTOMOTIVE SEMICONDUCTOR MARKET, BY PROPULSION TYPE

4.5 AUTOMOTIVE SEMICONDUCTOR MARKET, BY APPLICATION

4.6 AUTOMOTIVE SEMICONDUCTOR MARKET, BY MATERIAL

4.7 AUTOMOTIVE SEMICONDUCTOR MARKET, BY REGION

4.8 AUTOMOTIVE SEMICONDUCTOR MARKET, BY GEOGRAPHY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising vehicle electrification to curb emissions

5.2.1.2 Rapid advances in ADAS and autonomous driving technologies

5.2.1.3 Evolution of connected and software-defined vehicle ecosystem

5.2.2 RESTRAINTS

5.2.2.1 High development and qualification costs

5.2.2.2 Supply chain and capacity constraints

5.2.3 OPPORTUNITIES

5.2.3.1 Localization and development of semiconductor ecosystem

5.2.3.2 Rising development of AI-driven domain controllers and edge computing solutions

5.2.3.3 Mounting demand for fast-charging and vehicle-to-grid infrastructure

5.2.4 CHALLENGES

5.2.4.1 Issues in scaling wide-bandgap semiconductor production for automotive applications

5.2.4.2 Challenges in meeting rigorous standards related to automotive systems

5.2.4.3 Complexities associated with semiconductor integration

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 INVESTMENT AND FUNDING SCENARIO

5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 System-on-chip (SoC) platforms

5.7.1.2 Power semiconductor devices

5.7.1.3 Automotive sensors

5.7.2 COMPLEMENTARY TECHNOLOGIES

5.7.2.1 Advanced semiconductor packaging

5.7.2.2 Automotive Ethernet and high-speed connectivity standards

5.7.2.3 Functional safety and security frameworks

5.7.2.4 In-vehicle AI accelerators and domain controllers

5.7.3 ADJACENT TECHNOLOGIES

5.7.3.1 Software-defined vehicles (SDVs) and centralized E/E architectures

5.7.3.2 Vehicle-to-Everything (V2X) communication

5.7.3.3 Digital twins and over-the-air (OTA) update ecosystems

5.8 PRICING ANALYSIS

5.8.1 AVERAGE SELLING PRICE TREND OF MEMORY, BY KEY PLAYER, 2021-2024

5.8.2 AVERAGE SELLING PRICE TREND OF MEMORY, BY REGION, 2021-2024

5.9 PORTER'S FIVE FORCES ANALYSIS

5.9.1 THREAT OF NEW ENTRANTS

5.9.2 THREAT OF SUBSTITUTES

5.9.3 BARGAINING POWER OF SUPPLIERS

5.9.4 BARGAINING POWER OF BUYERS

5.9.5 INTENSITY OF COMPETITIVE RIVALRY

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 CASE STUDY ANALYSIS

5.11.1 MOBILEYE IMPROVES AUTOMOTIVE SAFETY USING STMICROELECTRONICS' SEMICONDUCTORS

5.11.2 FLEX LEVERAGES STMICROELECTRONICS' SEMICONDUCTORS TO SUPPORT AUTOMOTIVE INNOVATION

5.11.3 GIGABYTE PILOT SERVES AS AUTONOMOUS-DRIVING CONTROL UNIT FOR TAIWAN'S FIRST SELF-DRIVING BUS

5.12 TRADE ANALYSIS

5.12.1 IMPORT SCENARIO (HS CODE 8542)

5.12.2 EXPORT SCENARIO (HS CODE 8542)

5.13 PATENT ANALYSIS

5.14 TARIFF AND REGULATORY LANDSCAPE

5.14.1 TARIFF ANALYSIS

5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15 KEY CONFERENCES AND EVENTS, 2025-2026

5.16 IMPACT OF AI/GEN AI ON AUTOMOTIVE SEMICONDUCTOR MARKET

5.16.1 INTRODUCTION

5.16.2 USE CASES OF AI/GEN AI IN AUTOMOTIVE SEMICONDUCTOR MARKET

5.17 IMPACT OF 2025 US TARIFF ON AUTOMOTIVE SEMICONDUCTOR MARKET

5.17.1 INTRODUCTION

5.17.2 PRICE IMPACT ANALYSIS

5.17.3 KEY TARIFF RATES

5.17.4 IMPACT ON COUNTRIES/REGIONS

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON APPLICATIONS

6 AUTOMOTIVE SEMICONDUCTOR MARKET, BY COMPONENT

6.1 INTRODUCTION

6.2 PROCESSORS

6.2.1 GROWING POPULARITY OF SOFTWARE-DEFINED VEHICLES AND ZONAL ARCHITECTURES TO FUEL SEGMENTAL GROWTH

6.2.2 MICROPROCESSOR UNITS (MPUS)

6.2.3 MICROCONTROLLER UNITS (MCUS)

6.2.4 DIGITAL SIGNAL PROCESSORS (DSPS)

6.2.5 GRAPHIC PROCESSING UNITS (GPUS)

6.3 ANALOG ICS

6.3.1 RISING INTEGRATION OF MULTIPLE SENSORS IN ADAS, LIDAR, RADAR, AND CAMERA SYSTEMS TO AUGMENT SEGMENTAL GROWTH