AI Orchestration Market by Offering, Deployment Model, Application and Region - Global Forecast to 2030

상품코드:1843273

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 526 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

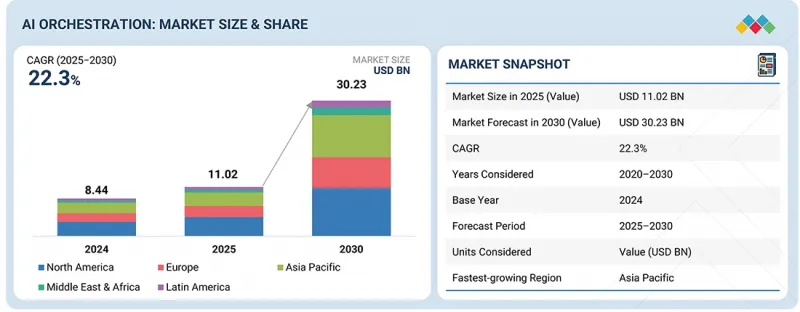

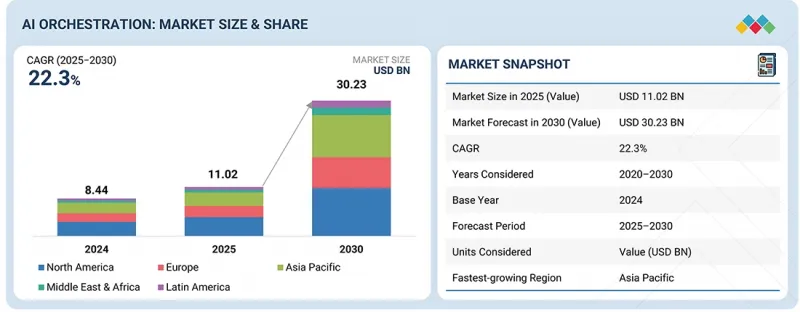

세계 AI 오케스트레이션 시장 규모는 2025년 110억 2,000만 달러에서 2030년까지 302억 3,000만 달러에 이를 것으로 예측되며, CAGR 22.3%의 성장이 예상됩니다.

조사 범위

조사 대상 연도

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

달러

부문

제공, 오케스트레이션 아키텍처, 배포 모델, 용도, 최종 사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 중동, 아프리카, 라틴아메리카

IT 및 비즈니스 워크플로우 전체에 일관되게 적용되는 중앙 집중식 승인, 계보 추적 및 정책 적용을 조직이 요구하게 되어 각 용도에서 통일된 거버넌스 레이어에 대한 요구가 높아지고 있는 것이 성장의 촉진요인이 되고 있습니다. 은행, 의료, 공공 부문의 컴플라이언스 프레임워크는 증거, 역할을 인식 한 승인, 롤백 제어를 포함한 감사 대응 오케스트레이션 레이어를 구매자가 요구하고 규제 압력도 기세를 늘리고 있습니다.

이러한 요인으로 인하여 AI 오케스트레이션은 어시스턴트, 워크플로우 및 레거시 시스템을 투명한 컨트롤로 교차하는 기업 자동화 전략의 핵심 계층이 되고 있습니다. 기업이 고객 서비스, IT 운영, 보안, 재무, 공급망 등 이용 사례로 조직적인 액션을 확대하는 가운데 신속한 TTV(Time-To-Value)와 거버넌스, 휴대용 정책, 측정 가능한 ROI를 결합할 수 있는 벤더가 채용을 선도할 것으로 예측됩니다. 복잡한 가격 체계와 기능 간의 예산 분할은 기업 수준의 헌신을 방해합니다. 게다가 의도파관 않은 폐쇄 가능성은 AI 오케스트레이션 툴의 자율성을 제한하고 시장 전체의 확대를 방해할 수 있습니다.

"기업이 어시스트에서 안전한 프로덕션 등급 액션으로 규모를 확대함에 따라 에이전트 빌더 도구 제공이 예측 기간에 갑작스러운 수요를 나타냅니다."

에이전트 빌더 도구는 AI 오케스트레이션에서 뛰어난 성장 엔진으로 부상하며 팀이 데이터 관리를 손상시키지 않고 신속하게 행동할 수 있도록 합니다. 비즈니스 사용자는 사전 빌드된 작업으로 에이전트를 구성할 수 있으며 플랫폼 팀은 입력 및 출력, 승인 및 제한을 설정하여 모든 다시 쓰기가 추적 가능하고 가역적임을 보장합니다. 책임을 분담함으로써 구축 시간을 단축하고 고객 서비스, IT 경영, 재무, 공급망 관리 등 다양한 분야에서 일관된 거버넌스를 확보할 수 있습니다. 공급업체는 사례 업데이트, 인타이틀먼트 검사, 데이터 검색, 변경 요청 등과 같은 일반적인 작업에 대해 즉시 사용할 수 있는 작업에 대한 카탈로그를 제공합니다. 또한 배포 전 테스트 계획 및 도구 선택을 지원하는 평가 키트도 제공합니다.

로우코드 및 프로코드 옵션은 병렬로 실행되므로 서비스 소유자는 플로우를 조립하고 엔지니어는 보안 커넥터 및 사용자 지정 작업을 재작업 없이 추가할 수 있습니다. 빌더 시트와 액션의 소비가 혼합된 가격 설정은 실제 사용 상황에 맞게 설정되어 있으므로 각 부서는 소규모부터 시작하여 자신있게 확장할 수 있습니다. 조직이 파일럿에서 프로덕션 정책 기반 자동화로 확장됨에 따라 이러한 도구는 새로운 에이전트의 조립 라인으로 작동하여 오케스트레이터에 일관된 원격 측정 및 증거를 제공합니다. 그 결과 처음 가치를 얻는 데 걸리는 시간이 단축되고 감사가 더욱 깨끗해지고 멀티 테넌트 SaaS, 싱글 테넌트 SaaS 또는 고객이 관리하는 클라우드 환경에서 실행되는 재사용 가능한 에이전트 라이브러리가 확장됩니다.

"규제된 워크플로우와 측정 가능한 ROI로 BFSI 최종 사용자가 2025년 AI 오케스트레이션 채택을 선도했습니다."

BFSI는 AI 오케스트레이션 시장에서 가장 큰 최종 사용자 부문을 차지합니다. 이것은 사업 규모의 크기와 규제 감독의 엄격함을 반영한 것입니다. 금융기관은 KYC 갱신, 결제조업체, 대출승인, 클레임 처리 등의 프로세스를 간소화하는 한편, 모든 단계를 감사 가능한 상태로 유지하도록 강요되고 있습니다. 오케스트레이션 플랫폼은 행동이 정책에 구속되고, 역할에 따라 승인이 이루어지고, 규제 당국 및 감사인을 위한 증거가 기록되도록 보장하는 데 필요한 거버넌스 계층을 제공합니다. 이를 통해 은행과 보험 회사는 컴플라이언스를 손상시키지 않고 예외 처리 비용을 줄이고 해결 시간을 단축 할 수 있습니다. IBM, Palantir, UiPath와 같은 공급업체는 이미 조직 워크플로우를 통해 수동 터치 포인트를 줄이고, 감사 대응 능력을 확보하고, 고객 만족도를 향상시킨 BFSI 사례 연구를 소개했습니다.

이 보고서는 세계 AI 오케스트레이션 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

AI 오케스트레이션 시장의 기업에게 매력적인 기회

AI 오케스트레이션 시장 : 주요 3 용도별

북미의 AI 오케스트레이션 시장 : 전개 모델별, 소프트웨어별

AI 오케스트레이션 시장 : 지역별

제5장 시장 개요와 산업 동향

소개

시장 역학

성장 촉진요인

억제요인

기회

과제

AI 오케스트레이션의 진화

공급망 분석

생태계 분석

에이전트 오케스트레이션 플랫폼 제공업체

에이전트 빌더 도구 제공업체

워크플로우 오케스트레이션 제공업체

모델 서빙 플랫폼 제공업체

데이터 오케스트레이션 제공업체

인프라 오케스트레이션 제공업체

서비스 제공업체

2025년 미국 관세의 영향 - AI 오케스트레이션 시장

소개

주요 관세율

가격의 영향 분석

국가/지역에 미치는 영향

최종 이용 산업에 대한 영향

투자 및 자금조달 시나리오

사례 연구 분석

기술 분석

주요 기술

보완 기술

인접 기술

규제 상황

규제기관, 정부기관, 기타 조직

규제

특허 분석

조사 방법

특허 출원 건수 : 문헌 유형별(2016-2025년)

혁신과 특허출원

가격 설정 분석

평균 판매 가격 : 주요 기업별(2025년)

용도별 평균 판매 가격(2025년)

주요 컨퍼런스 및 이벤트(2025-2026년)

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

고객사업에 영향을 주는 동향/혼란

제6장 AI 오케스트레이션 시장 : 제공별

소개

소프트웨어

AI 오케스트레이션 플랫폼

에이전트 빌더 도구

워크플로우 오케스트레이션 플랫폼

데이터 오케스트레이션 플랫폼

모델 서빙 플랫폼

인프라 오케스트레이션 플랫폼

서비스

전문 서비스

매니지드 서비스

제7장 AI 오케스트레이션 시장 : 오케스트레이션 아키텍처별

소개

집중형 오케스트레이션

비집중형 오케스트레이션

분산형 오케스트레이션

하이브리드 오케스트레이션

제8장 AI 오케스트레이션 시장 : 전개 모델별

소개

싱글 테넌트 SaaS

멀티 테넌트 SaaS

고객 매니지드 클라우드

On-Premise 및 에어 갭

제9장 AI 오케스트레이션 시장 : 용도별

소개

고객 서비스 자동화

판매 및 수익 자동화

마케팅 자동화

IT 서비스 매니지먼트

보안 업무

재무 및 조달 자동화

공급망 자동화

인사 및 종업원 서비스 데스크

엔터프라이즈 지식 검색

소프트웨어 엔지니어링 및 코딩 자동화

필드 서비스 및 자산 운용

기타 용도

제10장 AI 오케스트레이션 시장 : 최종 사용자별

소개

BFSI

소매 및 소비재

전문 서비스 제공업체

의료 및 생명과학

통신

소프트웨어 기술 공급자

미디어 및 엔터테인먼트

물류 및 운송

정부 및 방위

자동차

에너지 및 유틸리티

제조

기타 최종 사용자

제11장 AI 오케스트레이션 시장 : 지역별

소개

북미

북미의 AI 오케스트레이션 시장 성장 촉진요인

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 AI 오케스트레이션 시장 성장 촉진요인

유럽의 거시 경제 전망

영국

독일

프랑스

이탈리아

스페인

네덜란드

기타 유럽

아시아태평양

아시아태평양의 AI 오케스트레이션 시장 성장 촉진요인

아시아태평양의 거시 경제 전망

중국

인도

일본

한국

싱가포르

호주 및 뉴질랜드(ANZ)

기타 아시아태평양

중동 및 아프리카

중동 및 아프리카의 AI 오케스트레이션 시장 성장 촉진요인

중동 및 아프리카의 거시 경제 전망

사우디아라비아

아랍에미리트(UAE)

남아프리카

튀르키예

카타르

기타 중동 및 아프리카

라틴아메리카

라틴아메리카의 AI 오케스트레이션 시장 성장 촉진요인

라틴아메리카의 거시 경제 전망

브라질

멕시코

아르헨티나

기타 라틴아메리카

제12장 경쟁 구도

개요

주요 참가 기업의 전략(2020-2025년)

수익 분석(2020-2024년)

시장 점유율 분석(2024년)

브랜드/제품 비교

제품 비교 분석 : 에이전트 오케스트레이션 플랫폼별

제품 비교 분석 : 에이전트 빌더 도구별

제품 비교 분석 : 워크플로우 오케스트레이션 플랫폼별

주요 벤더 기업의 평가와 재무 지표

기업 평가 매트릭스 : 주요 기업(2024년)

기업의 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제13장 기업 프로파일

소개

주요 기업

IBM

AMAZON WEB SERVICES

SALESFORCE

ADOBE

MICROSOFT

SAP

GOOGLE

COFORGE

SERVICENOW

UIPATH

NVIDIA

LIVEPERSON

GENESYS

PALANTIR

KORE.AI

ALTAIR

YELLOW.AI

GLEAN

DIGITAL.AI

WORKATO

APPIAN

기타 기업

SOLACE

JITTERBIT

SNAPLOGIC

AISERA

ONEREACH.AI

DOMINO DATA LABS

ANYSCALE

FORETHOUGHT.AI

VUE.AI(MAD STREET DEN)

RAFAY SYSTEMS

SPACELIFT.IO

AIRIA

DAGSTER LABS

HUMANITEC

TONKEAN

AKKA.IO

SPARKBEYOND

UNION.AI

ORKES

TENEO.AI

ORBY AI(UNIPHORE)

MULTIMODAL.DEV

HOPSWORKS

제14장 인접 시장과 관련 시장

소개

에이전트 AI 시장 - 세계 예측(-2032년)

시장의 정의

시장 개요

AI 플랫폼 시장 - 세계 예측(-2030년)

시장의 정의

시장 개요

제15장 부록

JHS

영문 목차

영문목차

The global AI orchestration market size is projected to grow from USD 11.02 billion in 2025 to USD 30.23 billion by 2030, at a CAGR of 22.3%.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

USD (Million)

Segments

Offering, Orchestration Architecture, Deployment Model, Application, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, and Latin America

Growth is being driven by the increasing need for a unified governance layer across applications, as organizations seek centralized approvals, lineage tracking, and policy enforcement that apply uniformly across IT and business workflows. Regulatory pressure is also adding momentum, with compliance frameworks in banking, healthcare, and the public sector driving buyers toward audit-ready orchestration layers that incorporate evidence, role-aware approvals, and rollback controls.

These factors are turning AI orchestration into the central layer of enterprise automation strategies, bridging assistants, workflows, and legacy systems with transparent controls. Vendors that can combine fast time-to-value with governance, portable policies, and measurable ROI are expected to lead adoption as enterprises expand orchestrated actions across customer service, IT operations, security, finance, and supply chain use cases. The intricate nature of pricing structures and the division of budgets across functions are impeding enterprise-level commitments. Additionally, the potential for unintentional write-backs is constraining the autonomy of AI orchestration tools, which could hinder overall market expansion.

"Agent builder tools offering to witness breakout demand over the forecast period as enterprises scale from assist to safe, production-grade actions"

Agent builder tools are emerging as a standout growth engine within AI orchestration, enabling teams to move quickly without compromising data control. Business users can compose agents with prebuilt actions, while platform teams set typed inputs and outputs, approvals, and limits, ensuring that every write-back is traceable and reversible. Dividing responsibilities helps reduce build time and ensures consistent governance across various areas, including customer service, IT operations, finance, and supply chain management. Vendors are providing catalogs of ready-to-use actions for common tasks such as case updates, entitlement checks, data lookups, and change requests. Additionally, they offer evaluation kits to assist with testing plans and selecting tools before implementation.

Low-code and pro-code options run side by side, allowing a service owner to assemble a flow and an engineer to add secure connectors or custom actions without requiring rework. Pricing aligns with real usage, featuring a mix of builder seats and action consumption, which enables departments to start small and scale with confidence. As organizations expand from pilots to live, policy-bound automation, these tools act as the assembly line for new agents, feeding orchestrators with consistent telemetry and evidence. The result is a faster time to first value, cleaner audits, and a growing library of reusable agents that run across multi-tenant SaaS, single-tenant SaaS, or customer-managed cloud environments.

"BFSI end user leads AI orchestration adoption in 2025, driven by regulated workflows and measurable ROI"

Banking, financial services, and insurance (BFSI) represent the largest end-user segment in the AI orchestration market, reflecting the scale of operations and the intensity of regulatory oversight. Institutions are under pressure to streamline processes such as KYC updates, payment investigations, loan approvals, and claims handling while keeping every step auditable. Orchestration platforms provide the governance layer necessary to ensure that actions are bound by policy, approvals are enforced based on role, and evidence is logged for regulators and auditors. This helps banks and insurers reduce exception handling costs and expedite resolution times without compromising compliance. Vendors such as IBM, Palantir, and UiPath have already showcased BFSI case studies where orchestrated workflows reduced manual touchpoints, ensured audit readiness, and improved customer satisfaction scores.

Growth is reinforced by the high transaction volume and risk profile of BFSI operations, which makes orchestration's combination of speed and control especially attractive. For example, orchestrated agents can automatically flag anomalies, assemble evidence, and route approvals in payment flows, while ensuring that rollback is always possible. BFSI is expected to contribute the largest revenue share in 2025 and set the pace for adoption in other regulated industries, demonstrating that AI orchestration can deliver both efficiency and compliance at scale.

"North America will have the largest market share in 2025, and Asia Pacific is slated to grow at the fastest rate during the forecast period"

North America is set to capture the largest share of AI orchestration revenue in 2025, anchored by the US with additional momentum from Canada. Enterprises in the region are moving beyond pilots and are standardizing on an orchestration layer that can execute approved actions inside CRM, ERP, ITSM, and data platforms with full evidence. Demand is strongest in banking, healthcare, telecom, software, and public sector programs where audit trails, identity scopes, and clean rollback are non-negotiable. The region benefits from deep hyperscaler footprints and a dense network of global system integrators and boutique specialists that package certified connectors, industry playbooks, and managed services. Buyers also favor deployment choice.

Customer-managed and single-tenant options are commonly used for sensitive workloads, while multi-tenant SaaS supports rapid entry and departmental expansion. Procurement teams request unit economics dashboards, exportable run telemetry, and reference architectures that integrate with existing observability stacks. As organizations expand from assist use cases to governed write-backs and broaden coverage across service, operations, and finance, North America's large installed base and compliance intensity sustain leadership and drive multi-year, portfolio-level rollouts across Fortune 1000 accounts.

Meanwhile, Asia Pacific is expected to record the fastest growth through 2025-2030 as large, distributed enterprises push for efficiency and local regulators clarify rules for responsible AI. Telecom operators, manufacturers, banks, and public agencies in India, China, Japan, and South Korea are scaling programs that connect planning, tool execution, and approvals in one governed run. Growth is facilitated by rising cloud adoption, local data center build-outs, and the need to automate exception-heavy processes across shared-service hubs and field operations. Vendors are tailoring offers to regional needs with localized connectors, language support, and deployment choices that include customer-managed cloud and on-premises runtimes for data residency and key control.

Partners in the region, including global system integrators, local consulting firms, and channel providers, are creating rapid-start kits for various use cases such as customer service automation, IT incident response, and handling non-conformance issues. These kits help organizations achieve quicker returns on investment. As companies assess improvements in cycle time, accuracy, and cost-to-serve, they are likely to shift their budgets from experimentation to expansion. This trend positions the Asia Pacific region as the most dynamic growth driver for AI orchestration in the coming years.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the AI orchestration market.

By Company: Tier I - 33%, Tier II - 44%, and Tier III - 23%

By Designation: C-Level Executives - 36%, D-Level Executives - 41%, and others - 23%

By Region: North America - 39%, Europe - 18%, Asia Pacific - 32%, Middle East & Africa - 4%, and Latin America - 7%

The report includes the study and in-depth company profiles of key players offering AI orchestration software and services. The major players in the AI orchestration market include IBM (US), AWS (US), Salesforce (US), Adobe (US), Microsoft (US), SAP (Germany), Google (US), Coforge (India), ServiceNow (US), UiPath (US), NVIDIA (US), LivePerson (US), Genesys (US), Palantir (US), Kore.ai (US), Altair (US), Yellow.ai (US), Glean (US), Digital.ai (US), Workato (US), Appian (US), Solace (Canada), Jitterbit (US), SnapLogic (US), Aisera (US), OneReach.ai (US), Domino Data Labs (US), Anyscale (US), Forethought.ai (US), Vue.ai (US), Rafay Systems (US), Spacelift.io (US), Airia (US), Dagster Labs (US), Humanitec (Germany), Tonkean (US), Akka.io (US), SparkBeyond (US), Union.ai (US), Orkes (US), Teneo.ai (Sweden), Orby AI (US), Multimodal.dev (US), and Hopsworks (Sweden).

Research Coverage

This research report categorizes the AI orchestration market by offering, orchestration architecture, deployment model, application, and end user. The offering segment is split into AI orchestration software and AI orchestration services. The software segment is further split into agent orchestration platforms, agent builder tools, workflow orchestration platforms, data orchestration platforms, model serving platforms, and infrastructure orchestration platforms. The services segment comprises managed services and professional services (training and consulting, system integration and implementation, and support and maintenance). The orchestration architecture segment includes centralized orchestration, decentralized orchestration, distributed orchestration, and hybrid orchestration. The deployment model segment spans single tenant SaaS, multi-tenant SaaS, customer managed cloud, and on premises & air gapped deployment.

Application segment covers customer service automation, sales & revenue automation, marketing automation, IT service management, security operations, finance & procurement automation, supply chain automation, HR & employee service desk, enterprise knowledge search, software engineering & coding automation, field service & asset operations, and other applications (legal operations & contract lifecycle, risk & internal audit, and research & lab workflows). The end user segment is split into BFSI, retail & CPG, professional service providers, healthcare & life sciences, telecommunications, software & technology providers, media & entertainment, logistics & transportation, government & defense, automotive, energy & utilities, manufacturing, and other enterprises (education, travel & hospitality, and construction & real estate). The regional analysis of the AI orchestration market covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America.

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the AI orchestration market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, solutions, and services, as well as key strategies, contracts, partnerships, agreements, new product & service launches, mergers and acquisitions, and recent developments associated with the AI orchestration market. This report covers the competitive analysis of upcoming startups in the AI orchestration market ecosystem.

Key Benefits of Buying the Report

The report will provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall AI orchestration market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (enterprise shift from reactive chat to governed, outcome-linked automation; AI orchestration reducing cost-to-serve and time-to-resolution by executing system actions; need for a common governance layer across apps to centralize approvals, lineage, and policy enforcement; stringent focus on regulatory compliance pushing buyers toward governed AI orchestration), restraints (pricing complexity and cross-function budget splits stalling enterprise-wide commitments; risk of unintended write-backs limiting autonomy and efficiency of AI orchestration tools), opportunities (demand for sovereign and air-gapped AI orchestration in public sector and regulated industries; replacement of overlapping RPA, iPaaS, and workflow stacks with AI orchestration suites; prebuilt template libraries and certified action packs accelerating ROI cycles for mid-market), and challenges (enterprise app sprawl across multi-cloud environments causing vendor lock-in concerns; end-to-end observability across multi-agent orchestration remains complex)

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the AI orchestration market

Market Development: Comprehensive information about lucrative markets - analysis of the AI orchestration market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the AI orchestration market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of IBM (US), AWS (US), Salesforce (US), Adobe (US), Microsoft (US), SAP (Germany), Google (US), Coforge (India), ServiceNow (US), UiPath (US), NVIDIA (US), LivePerson (US), Genesys (US), Palantir (US), Kore.ai (US), Altair (US), Yellow.ai (US), Glean (US), Digital.ai (US), Workato (US), Appian (US), Solace (Canada), Jitterbit (US), SnapLogic (US), Aisera (US), OneReach.ai (US), Domino Data Labs (US), Anyscale (US), Forethought.ai (US), Vue.ai (US), Rafay Systems (US), Spacelift.io (US), Airia (US), Dagster Labs (US), Humanitec (Germany), Tonkean (US), Akka.io (US), SparkBeyond (US), Union.ai (US), Orkes (US), Teneo.ai (Sweden), Orby AI (US), Multimodal.dev (US), and Hopsworks (Sweden), among others, in the AI orchestration market. The report also helps stakeholders understand the pulse of the AI orchestration market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 INCLUSIONS AND EXCLUSIONS

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.1.2.1 Breakup of primary profiles

2.1.2.2 Key industry insights

2.2 MARKET BREAKUP AND DATA TRIANGULATION

2.3 MARKET SIZE ESTIMATION

2.3.1 TOP-DOWN APPROACH

2.3.2 BOTTOM-UP APPROACH

2.4 MARKET FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

3.1 RISE OF AI ORCHESTRATION

3.2 UNDERSTANDING AI ORCHESTRATION: SCOPE AND BOUNDARIES

3.2.1 CONTROL PLANE VS. EXECUTION PLANE VS. DATA PLANE

3.2.2 GOVERNANCE, EVALUATION, AND OBSERVABILITY LOOPS

3.2.3 BOUNDARIES VS. IPAAS, RPA, AND AI ORCHESTRATION

3.3 PACKAGING AND MONETIZATION

3.3.1 STANDALONE ORCHESTRATOR SKUS VS. SUITE COMPONENTS