전기자동차 시장 예측(-2035년) : 차종, 추진, 차량 커넥티비티, 컴포넌트, 최종사용자, PEV 시장, HEV 시장, 지역별

Electric Vehicle Market by Vehicle Type, Propulsion, Vehicle Connectivity, Component, End Use, P-EV market, H-EV market and Region - Global Forecast 2035

상품코드:1840080

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 486 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

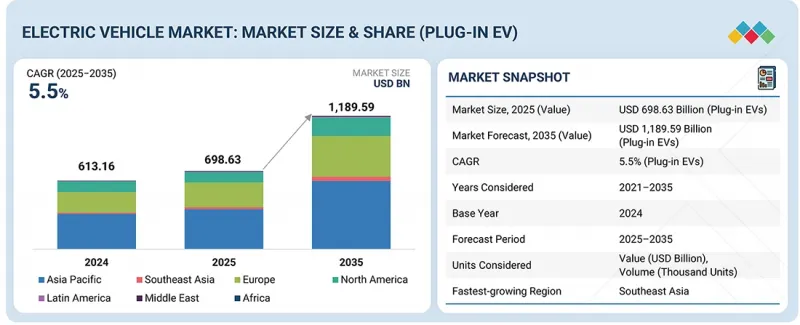

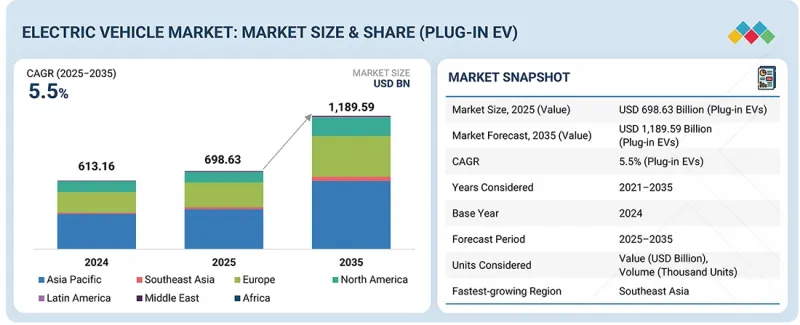

세계의 플러그인 전기자동차(PEV) 시장 규모는 2025년 6,986억 3,000만 달러에서 예측 기간 중 5.5%의 CAGR로 추이하며, 2035년에는 1조 1,895억 9,000만 달러로 성장할 것으로 예측됩니다.

또한 하이브리드 전기자동차(HEV+MHEV) 시장 규모는 2025년 4,468억 7,000만 달러에서 4.1%의 연평균 복합 성장률(CAGR)로 2035년에는 6,677억 5,000만 달러로 성장할 것으로 예측됩니다. 전반적으로 전기자동차(EV) 시장은 승용차 및 상용차 부문 모두에서 배터리 구동 모빌리티에 대한 수요가 증가함에 따라 꾸준한 성장세를 보이고 있습니다.

조사 범위

조사 대상 연도

2021-2035년

기준연도

2024년

예측 기간

2025-2035년

단위

수량(대)·금액(달러)

부문

차종, 추진, EV 아키텍처, 차량 최고속도, 차량 구동 유형, 차체 유형, 구성 유형, 토폴로지, 차량 커넥티비티, 추진 & 컴포넌트, 최종사용자, 지역

대상 지역

아시아태평양, 동남아시아, 유럽, 북미, 라틴아메리카, 중동 및 아프리카

주요 성장 요인으로는 배터리의 에너지 밀도 향상, 급속 충전 기능의 발전, 차량 안전 및 성능 향상 등이 있습니다. 유럽의 2035년 제로에미션 목표와 독일, 노르웨이 등의 지원적 규제정책으로 도입이 가속화되는 반면, 중국과 미국에서는 보조금이 단계적으로 축소되고 있는 상황입니다. 충전 인프라 확충과 파워트레인 효율에 대한 투자로 항속거리 연장과 보유 비용 절감을 실현하고 있습니다. 또한 소비자들의 전기자동차에 대한 관심이 높아짐에 따라 OEM들은 개선된 열 관리 시스템 및 소프트웨어 기반 에너지 최적화 기술과 같은 첨단 기술을 통합하는 데 주력하고 있습니다. 이를 통해 차량은 더욱 안전하고, 효율적이며, 사용자 친화적인 차량이 되었습니다. 또한 차량 설계, 소프트웨어 통합 및 에너지 관리 분야의 지속적인 혁신은 예측 기간 중 EV 시장의 지속적인 성장을 지원하고 있습니다.

"전륜구동 유형이 예측 기간 중 가장 큰 성장세를 보일 것으로 예상"

전륜구동(FWD) 부문은 비용 효율성, 실용성, 도시 및 교통량이 많은 환경에서의 높은 적합성으로 인해 EV 시장에서 가장 높은 성장이 예상됩니다. FWD 시스템은 후륜구동(RWD)이나 사륜구동(AWD)보다 구조가 간단하고 제조비용이 낮아 저렴한 가격의 EV 모델을 제공할 수 있습니다. 또한 구동계 경량화를 통한 에너지 효율 향상과 항속거리 연장, 전륜축에 무게 배분을 통한 우천 및 강설시 우수한 견인력은 다양한 기후 조건에서 매력을 더하고 있습니다. 또한 많은 제조업체들이 기존 CE 플랫폼을 FWD 구조로 EV화하여 초기 도입에 박차를 가하고 있습니다. RWD와 AWD는 여전히 고성능 및 고급 모델에 대한 수요가 있지만, 가격 경쟁력, 효율성, 일상적인 도시 이동성 측면에서 FWD가 시장을 주도할 것으로 예측됩니다.

"유럽이 예측 기간 중 괄목할 만한 성장을 보일 것으로 전망"

유럽에서는 정책적 의무화, OEM의 적극적인 투자, 소비자의 도입 확대가 시장 성장을 촉진하고 있습니다. EU의 2035년 무공해 목표(신차 및 밴 대상)와 2030년 CO2 감축 기준 강화로 인해 완전 전기자동차와 플러그인 하이브리드 차량으로의 전환이 가속화되고 있습니다. Volkswagen, BMW, Mercedes-Benz, Volvo, Stellantis 등 주요 제조업체들은 전기자동차 생산, 소프트웨어 통합, 전용 충전 네트워크 구축에 많은 투자를 하고 있으며, VW ID.4, BMW iX, Mercedes EQC 등 신모델을 출시하여 수요에 대응하고 있습니다. 수요에 대응하고 있습니다. 또한 플러그인 하이브리드(PHEV)의 보급이 듀얼 파워트레인에 대한 수요를 지원하는 한편, 배터리 전기자동차(BEV)의 확대는 고용량 배터리, 열 관리 시스템, 인버터 냉각 솔루션의 진화를 촉진하고 있습니다.

2025년 상반기 유럽 BEV 등록대수는 전년 동기 대비 34% 증가했으며, 시장 점유율은 15.6%에 달했습니다. PHEV는 8.4%를 차지했으며, 독일, 벨기에, 네덜란드가 이 성장을 주도했습니다. 또한 뮌헨에서 열린 IAA Mobility 모터쇼에서 중국의 고급 자동차 제조업체인 홍치(Hongqi)는 550km의 주행거리와 급속 충전 기능(20분 만에 10%에서 80%까지 충전)을 갖춘 소형 전기 SUV를 발표하며 도시 및 교외 운전자를 타겟으로 삼고 있습니다. 도시 및 교외 운전자를 타겟으로 합니다. 유럽은 탄탄한 자동차 제조거점에 더해 부품의 현지 생산과 충전 네트워크 확대에 대한 투자를 통해 공급망의 강인함과 경쟁력을 확보하고 있습니다. 규제 강화, OEM의 전동화 로드맵, 하이브리드 수요, 소비자의 관심 증가로 유럽은 전기자동차 시장의 지속적인 성장을 위한 가장 유력한 지역으로 부상하고 있습니다.

세계의 전기자동차 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인의 분석, 기술·특허의 동향, 법규제 환경, 사례 연구, 시장 규모 추이·예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

시장 역학

촉진요인

억제요인

기회

과제

제6장 업계 동향

규제 상황

지속가능성 구상

인증, 라벨, 환경기준

기술 분석

기술/제품 로드맵

특허 분석

향후 응용

AI/생성형 AI가 전기자동차 시장에 미치는 영향

성공 사례와 실세계에 대한 응용

EV 시장에 대한 투자 의사결정 프로세스

구입 기준에서 주요 이해관계자

채택 장벽과 내부 과제

에코시스템 분석

공급망 분석

가격 분석

고객 사업에 영향을 미치는 동향과 혼란

투자와 자금조달 시나리오

사용 사례별 자금조달

주요 컨퍼런스와 이벤트

무역 분석

사례 연구 분석

기존 및 향후 전기자동차 모델

총소유 비용

부품 표 분석

OEM 전기자동차의 진보

제7장 전기자동차 시장 : 추진별

2024년 전기자동차 베스트셀러 모델

배터리 전기자동차(BEV)

연료전지 전기자동차(FCEV)

플러그인 하이브리드 전기자동차(PHEV)

하이브리드 전기자동차(HEV)

마일드 하이브리드 전기자동차(MHEV)

주요 인사이트

제8장 전기자동차 시장 : 차종별

승용차

상용차

주요 인사이트

제9장 전기자동차 시장 : 컴포넌트별

배터리 셀과 팩

온보드 충전기

모터

전력 제어 유닛

배터리 관리 시스템

연료전지 스택

연료 처리장치

파워 컨디셔너

공기압축기

가습기

제10장 전기자동차 시장 : 최종사용자별

운영 데이터

개인

상용 플릿

제11장 전기자동차 시장 : 차량 커넥티비티별

차량·건물(V2B)/차량·인프라(V2I)

차량·전력망(V2G)

차량차통신(V2V)

제12장 하이브리드 전기자동차 시장 : 구성 유형별

시리즈 방식

패러렐 방식

시리즈·패러렐 방식

주요 인사이트

제13장 마일드 하이브리드 전기자동차 시장 : 토폴로지별

P0-벨트 통합

P1-엔진·변속기 사이

P2-변속기측 통합(벨트 접속)

P3-변속기측 통합(샤프트 접속)

P4-후륜축 통합

제14장 플러그인 전기자동차 시장 : 전기 아키텍처별

차량 모델 : 전기 아키텍처별

400V

800V

주요 인사이트

제15장 플러그인 전기자동차 시장 : 차체 유형별

SUV/MPV

세단

해치백

주요 인사이트

제16장 플러그인 전기자동차 시장 : 구동별

인기 전기자동차 모델(구동별)

전륜구동(FWD)

후륜구동(RWD)

총륜구동(AWD)

주요 인사이트

제17장 플러그인 전기자동차 시장 : 최고속도별

시속 110마일 미만

시속 110마일 이상

주요 인사이트

제18장 전기자동차 시장 : 지역별

아시아태평양

거시경제 전망

중국

인도

일본

한국

동남아시아

거시경제 전망

태국

인도네시아

말레이시아

베트남

싱가포르

필리핀

호주

북미

거시경제 전망

미국

캐나다

멕시코

유럽

거시경제 전망

독일

프랑스

네덜란드

노르웨이

스웨덴

영국

덴마크

오스트리아

스위스

스페인

러시아

이탈리아

중동

거시경제 전망

아랍에미리트

사우디아라비아

이스라엘

라틴아메리카

거시경제 전망

브라질

콜롬비아

칠레

우루과이

코스타리카

아프리카

거시경제 전망

모로코

이집트

남아프리카공화국

제19장 경쟁 구도

주요 참여 기업의 전략/강점

시장 점유율 분석

매출 분석

기업 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 스타트업/중소기업

경쟁 시나리오

제20장 기업 개요

주요 기업

BYD COMPANY LTD.

TESLA

ZHEJIANG GEELY HOLDING GROUP

VOLKSWAGEN GROUP

GENERAL MOTORS

CHANGAN

BMW GROUP

LI AUTO INC.

HYUNDAI MOTOR GROUP

GAC GROUP

STELLANTIS NV

GREAT WALL MOTOR

기타 기업

TOYOTA MOTOR CORPORATION

RENAULT-NISSAN-MITSUBISHI

HONDA MOTOR CO., LTD.

MERCEDES-BENZ GROUP AG

FORD MOTOR COMPANY

CHERY

LEAPMOTOR INTERNATIONAL B.V.

SAIC MOTOR CORPORATION LIMITED

NIO

XIAOMI

RIVIAN

LUCID

DONGFENG MOTOR CORPORATION

FAW TRUCKS CO., LTD.

XPENG INC.

KG MOBILITY CORP.

NETA

MAZDA MOTOR CORPORATION

SUBARU CORPORATION

BAIC GROUP CO., LTD.

TATA MOTORS LIMITED

XIAOMI AUTO

제21장 MARKETSANDMARKETS에 의한 제안

동남아시아가 유리한 기회를 제공

BEV가 시장 점유율의 대부분을 점유

800V 전기 아키텍처의 도입이 채택을 가속

신규 비즈니스 모델 : Battery-as-a-Service와 Charging-as-a-Service

결론

제22장 부록

KSA

영문 목차

영문목차

The plug-in electric vehicle market is predicted to grow from USD 698.63 billion in 2025 to USD 1,189.59 billion in 2035, at a CAGR of 5.5%. The hybrid electric vehicle market (HEV+MHEV) is set to grow from USD 446.87 billion in 2025 to USD 667.75 billion in 2035, at a CAGR of 4.1%. The electric vehicle market is set for steady growth, driven by rising demand for battery-powered mobility across passenger and commercial segments.

Scope of the Report

Years Considered for the Study

2021-2035

Base Year

2024

Forecast Period

2025-2035

Units Considered

Volume (Thousand Units) and Value (USD Billion)

Segments

Vehicle Type, Propulsion, EV Architecture, Vehicle Top Speed, Vehicle Drive Type, Vehicle Body Type, Configuration Type, Topology, Vehicle Connectivity, Propulsion & Component, End Use, and Region

Regions covered

Asia Pacific, Southeast Asia, Europe, North America, Latin America, the Middle East, and Africa

Key factors include improvements in battery energy density, faster charging capabilities, and enhanced vehicle safety and performance. Government policies, such as Europe's 2035 zero-emission targets and supportive regulations in countries like Germany and Norway, are accelerating adoption despite subsidies in China and the US being phased out. Expansion of charging infrastructure and investments in powertrain efficiency enable longer ranges and lower ownership costs. Consumer interest in EVs is fostering OEM focus on integrating advanced technologies such as improved thermal management systems and software-driven energy optimization, ensuring vehicles are safer, more efficient, and user-friendly. Continuous innovation in vehicle design, software integration, and energy management supports sustained growth in the EV market throughout the forecast period.

"Front-wheel drive type is expected to have the largest growth in the electric vehicle market during the forecast period."

The front-wheel drive (FWD) segment is expected to witness the largest growth in the electric vehicle market over the forecast period, driven by its cost efficiency, practicality, and suitability for urban and high-traffic conditions. FWD systems are simpler and cheaper to produce than RWD or AWD configurations, translating into more affordable EV options for budget-conscious consumers. The lower drivetrain weight improves energy efficiency and range, while the weight distribution over the front axle provides better traction in rainy or snowy conditions, making FWD vehicles appealing in diverse climates. Leading FWD EV models such as Nissan Leaf, Hyundai Kona Electric, Toyota bZ4X, and mini EVs like GW Black Cat, GW White Cat, and GW Good Cat have demonstrated strong market acceptance due to their practicality and cost-effectiveness. Manufacturers have also leveraged FWD architectures by converting existing ICE platforms to EVs, accelerating early adoption. Recent launches, including Hyundai's Kona Electric FWD variant in Thailand in February 2025 with a 450 km range, further reinforce the segment's growth potential. While RWD and AWD continue to see demand in performance and premium models, FWD is expected to dominate due to affordability, efficiency, and suitability for everyday urban mobility.

"400V architecture is expected to hold the largest share in the electric vehicle market during the forecast period."

The 400V electric architecture is expected to hold the largest share in the electric vehicle market over the forecast period, driven by its widespread adoption, cost efficiency, and compatibility with existing charging infrastructure. Most early and mid-range EVs utilize 400V systems due to their balance of performance, moderate charging speeds, and lower production costs compared with higher-voltage architectures. The voltage in these systems ranges between 300V and 500V, depending on factors such as state of charge, temperature, and battery age, offering flexibility while maintaining efficiency. Leading global EV models powered by 400V architecture include Hyundai Kona Electric, Kia Niro EV, Volkswagen ID.4, BMW i4, Mercedes EQE, Kia EV6, Tesla Model 3, and mass-market launches such as Tata Motors' planned 400V EVs on its acti.ev platform. Another example is the Kia EV4, unveiled at Kia's 2025 EV Day, built on the 400V E-GMP platform with battery options offering up to 630 km range and fast 400V charging capabilities. Nissan launched the new LEAF based on a 400V architecture in September 2025. The mature supply chain, high-volume component availability, and lower purchase prices make 400V systems attractive for both OEMs and consumers. While 800V architectures are emerging for high-performance, fast-charging EVs, the combination of cost advantages, established production processes, and broad compatibility ensures that 400V systems will continue to dominate the EV market during the forecast period.

"Europe set to witness a significant growth in the electric vehicle market during the forecast period."

Europe is set to witness notable growth in the electric vehicle market over the forecast period, driven by regulatory mandates, strong OEM commitments, and expanding consumer adoption. Policies such as the EU 2035 zero-emission target for new cars and vans, coupled with stricter CO2 reduction standards for 2030, are accelerating the shift toward fully electric passenger cars and plug-in hybrids. Leading European automakers, including Volkswagen, BMW, Mercedes-Benz, Volvo, and Stellantis, are investing heavily in EV production, software integration, and dedicated charging infrastructure, while introducing models like the VW ID.4, BMW iX, and Mercedes EQC to meet rising consumer demand. The growing adoption of plug-in hybrids supports continued demand for dual powertrain systems, while battery electric vehicles are driving expansion in high-capacity battery packs, thermal management systems, and inverter cooling solutions. In the first half of 2025, BEV registrations in Europe surged 34% year-over-year, reaching 15.6% of market share, with PHEVs accounting for 8.4% of sales. Germany, Belgium, and the Netherlands led this growth, supported by increased charging infrastructure and consumer incentives. At the IAA Mobility auto show in Munich, Chinese luxury automaker Hongqi unveiled the EHS5, a compact electric SUV with a 550 km range and fast charging capability (10% to 80% in 20 minutes), targeting urban and suburban drivers. Europe's strong automotive manufacturing base, combined with investments in localized component production and charging networks, is ensuring supply chain resilience and competitiveness. Regulatory pressure, OEM electrification roadmaps, hybrid adoption, and consumer demand are positioning Europe for sustained growth in the electric vehicle market.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

By Company Type: Tier I - 42%, Tier II - 35%, and Tier III - 23%

By Designation: Directors - 36%, Managers - 43%, and Others - 21%

By Region: Asia Pacific - 17%, Southeast Asia - 11%, Europe - 28%, North America - 31%, Latin America - 8%, Middle East - 3%, and Africa - 2%

The electric vehicle market is dominated by major players, including BYD Company Ltd. (China), Tesla (US), Zhejiang Geely Holding Group (China), Volkswagen Group (Germany), and General Motors (US). These companies are expanding their portfolios to strengthen their electric vehicle market position.

Research Coverage

The report covers the electric vehicle market in terms of vehicle type (passenger cars and commercial vehicles), propulsion (battery electric vehicle, fuel cell electric vehicle, plug-in hybrid electric vehicle, hybrid electric vehicle, and mild hybrid electric vehicle), by EV architecture (400V and 800V), vehicle top speed (<125 mph and >125 mph), vehicle drive type (front-wheel drive, rear-wheel drive, and all wheel drive), vehicle body type (SUV/MPV, sedan, and hatchback), configuration type (series, parallel, and series-parallel), topology (P0, P1, P2, P3, and P4), vehicle connectivity (V2G, V2H/V2B, and V2L), propulsion & component (BEV components, PHEV components, FCEV components, HEV components, and MHEV components), end use (private and commercial fleets), and region. It covers the competitive landscape and company profiles of the significant electric vehicle market players.

The study also includes an in-depth competitive analysis of the key market players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the electric vehicle market and its subsegments.

This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report also helps stakeholders understand the current and future pricing trends of the electric vehicle market.

The report will help market leaders/new entrants with information on various trends in the electric vehicle market based on propulsion, vehicle type, drive type, EV architecture, body type, region, and other parameters.

The report provides insight into the following pointers:

Analysis of key drivers (policy support for EV adoption, Reduced operating and maintenance costs, Next generation battery innovations, zero tailpipe and vehicle lifecycle emissions, declining costs of EV batteries), restraints (high initial purchase price, capital-intensive charging infrastructure deployment, battery durability and lifecycle management, geopolitical instability and supply chain disruptions), opportunities (accelerated investment in charging infrastructure, innovation in wireless and on-the-move charging, fleet electrification and commercial deployment, expansion of Charging-as-a-Service (CaaS) business model, integration of bidirectional charging and smart parking), and challenges (extended charging duration constraints, fragmented charging standards and infrastructure)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the electric vehicle market

Market Development: Comprehensive information about lucrative markets - the report analyses the electric vehicle market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the electric vehicle market

Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players like BYD Company Ltd. (China), Tesla (US), Zhejiang Geely Holding Group (China), Volkswagen Group (Germany), and General Motors (US), among others, in the electric vehicle market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary participants

2.1.2.2 Primary interviews from demand and supply sides

2.1.2.3 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 FACTOR ANALYSIS

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PLUG-IN ELECTRIC VEHICLE MARKET

4.2 ELECTRIC VEHICLE MARKET, BY VEHICLE TYPE

4.3 ELECTRIC VEHICLE MARKET, BY PROPULSION

4.4 PLUG-IN ELECTRIC VEHICLE MARKET, BY TOP SPEED

4.5 PLUG-IN ELECTRIC VEHICLE MARKET, BY DRIVE TYPE

4.6 PLUG-IN ELECTRIC VEHICLE MARKET, BY ELECTRIC ARCHITECTURE

4.7 PLUG-IN ELECTRIC VEHICLE MARKET, BY VEHICLE BODY TYPE

4.8 HYBRID ELECTRIC VEHICLE MARKET, BY CONFIGURATION TYPE

4.9 PLUG-IN ELECTRIC VEHICLE MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Policy support for electric vehicle adoption

5.2.1.2 Reduced operating and maintenance costs

5.2.1.3 Next-generation battery innovations

5.2.1.4 Zero tailpipe and vehicle lifecycle emissions