Neuromodulation Market by Technology (Internal, External), Stimulation Type (Spinal Cord, Deep Brain, Vagus Nerve Stimulation), Application (Ischemia, Depression, Epilepsy, Obesity), End User (Hospitals, ASCs, Clinics) & Region - Global Forecast to 2030

상품코드:1822290

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 367 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

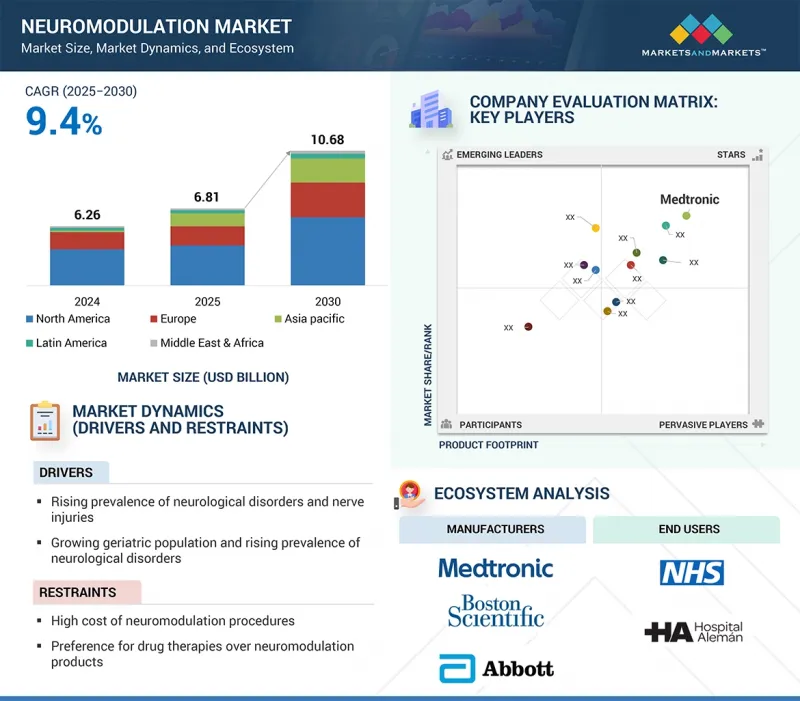

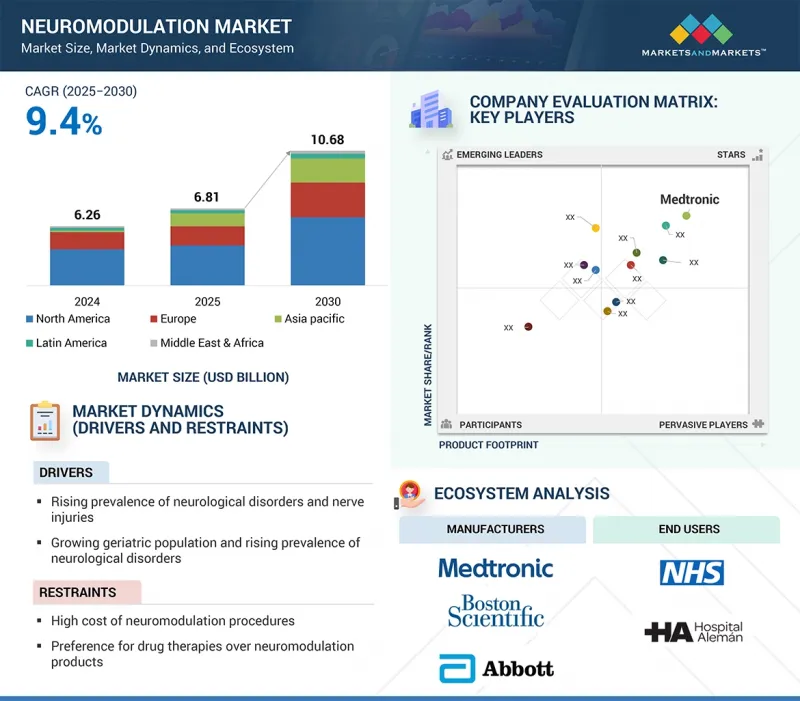

세계의 신경조절 시장 규모는 예측 기간 중에 9.4%의 연평균 복합 성장률(CAGR)로 확대되어 2025년 68억 1,000만 달러에서 2030년에는 106억 8,000만 달러에 이를 것으로 예측됩니다.

조사 범위

조사 대상 연도

2024-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

기술별, 자극 유형별, 용도별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

신경질환의 유병률 증가, 새로운 신경조절 기술 개발, 노인 인구 증가 등으로 신경조절 시장이 확대되고 있으며, 이 모든 것이 시장 성장의 요인으로 작용하고 있습니다. 또한, 신경절제술의 높은 비용이 시장 성장을 제한할 수 있습니다.

최종 사용자별로는 병원 및 외래수술센터(ASC), 클리닉 및 물리치료 센터, 기타 최종 사용자로 구분됩니다. 2024년에는 병원 및 외래수술센터(ASC)가 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 병원 및 외래 의료 부문은 종합적이고 다학제적인 치료를 제공하고 고급 신경조절요법을 이용할 수 있다는 점에서 신경조절요법 시장을 독점하고 있습니다. 이러한 환경에는 전문 수술 장비, 숙련된 임상의, 이식 가능하고 복잡한 신경절제술에 필요한 모니터링 시스템이 갖추어져 있습니다. 또한, 병원과 외래 센터는 이미 확립된 상환 제도의 혜택을 받고 있기 때문에 고가의 시술을 환자들이 더 쉽게 이용할 수 있습니다. 또한, 만성질환 관리, 수술 후 관리, 환자 추적관리에 대한 중요성이 점점 더 강조됨에 따라, 이들 기관은 시술량이 많아지고, 신경조절 제공 솔루션에 대한 리더십이 강화되고 있습니다.

신경조절 기술 시장은 내부 신경조절과 외부 신경조절으로 구분됩니다. 2024년 신경조절 시장에서 내부 신경조절 부문이 가장 큰 점유율을 차지할 것으로 예측됩니다. 내부 신경조절은 특정 신경 경로의 표적 자극을 용이하게 하는 정교한 기술로 인해 시장에서 지배적인 접근법이 되고 있습니다. 이 과정은 통각수용성 통증, 파킨슨병, 요실금, 변실금 등의 증상을 만성적으로 관리하는 데 도움이 되고 있습니다. 이식형 장치는 충전식 또는 오래 지속되는 배터리, 맞춤형 자극 프로토콜, 폐쇄 루프 피드백 메커니즘, 무선 연결 등의 특징을 가지고 있습니다. 이러한 기능을 통해 환자 결과를 개선하기 위한 실시간 모니터링과 맞춤형 치료 조정을 통해 환자 결과를 개선할 수 있습니다. 기술의 발전은 침습성을 최소화하는 컴팩트한 장치 설계를 지원하여 환자의 편안함과 치료 순응도를 향상시킵니다. 또한, 재료 과학, 전극 아키텍처, 소프트웨어 알고리즘의 지속적인 혁신을 통해 이러한 시스템의 효율성, 안전성 및 수명이 지속적으로 개선되고 있습니다. 그 결과, 임상 현장에서는 비침습적 중재보다 체내 신경조절술이 점점 더 선호되고 있습니다.

세계 신경조절 시장은 5개 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)으로 나뉩니다. 아시아태평양은 건강에 대한 인식 증가, 신경질환 및 만성통증질환 증가율, 중국, 인도, 일본 등의 국가에서 의료 인프라의 확장으로 인해 신경조절 시장에서 가장 빠르게 성장하고 있는 지역입니다. 이 지역에서는 더 나은 상환 정책 및 의료기기 접근성을 개선하기 위한 정부의 이니셔티브에 힘입어 첨단 신경조절 기술의 채택이 확대되고 있습니다. 또한, 환자 인구 증가, 가처분 소득 증가, 세계 및 현지 장비 제조업체의 투자 증가가 시장 성장을 견인하고 있습니다. 전문 치료 센터의 설립이 촉진되고 저침습적이고 이식 가능한 제품이 점차적으로 채택되고 있는 것도 이 지역에서 신경조절의 사용을 더욱 촉진하고 있습니다. 또한, 인도, 태국, 싱가포르 등의 국가에서 의료관광이 증가함에 따라 수술 건수가 증가하고 있으며, 이에 따라 수술 후 관리 및 신경치료에 대한 수요가 증가하고 있습니다.

세계의 신경조절(Neuromodulation) 시장에 대해 조사했으며, 기술별/자극 유형별/용도별/최종사용자별/지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

서론

시장 역학

고객의 비즈니스에 영향을 미치는 동향/혼란

가격 분석

밸류체인 분석

공급망 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

특허 분석

무역 데이터 분석

2025-2026년 주요 컨퍼런스 및 이벤트

사례 연구 분석

규제 분석

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

AI/생성형 AI가 신경조절 시장에 미치는 영향

2025년 미국 관세가 신경조절 시장에 미치는 영향

제6장 신경조절 시장(기술별)

서론

내부 신경조절

외적 신경조절

제7장 신경조절 시장(자극 유형별)

서론

척수 자극 치료

뇌심부 자극 치료

천골신경 자극

미주신경 자극

위신경 자극

경피적 전기 신경 자극

경두개 자기 자극

호흡 전기 자극

기타

제8장 신경조절 시장(용도별)

서론

척수 자극

심부뇌 자극

천골신경 자극

미주신경 자극

위전기 자극

경피전기 신경 자극

경두개 자기 자극

호흡 전기 자극

기타

제9장 신경조절 시장(최종사용자별)

서론

병원 및 외래수술센터(ASC)

클리닉 및 물리치료 센터

기타

제10장 신경조절 시장(지역별)

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

프랑스

영국

이탈리아

스페인

러시아

기타

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

인도

호주

기타

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타

중동 및 아프리카

헬스케어 인프라 개선과 신경학적 케어에 대한 의식의 고양이 시장 성장 촉진

중동 및 아프리카의 거시경제 전망

제11장 경쟁 구도

서론

주요 시장 진출기업의 전략/강점

매출 분석, 2020년-2024년

시장 점유율 분석, 2024년

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

기업 평가와 재무 지표

브랜드/제품 비교

경쟁 시나리오

제12장 기업 개요

주요 시장 진출기업

MEDTRONIC

BOSTON SCIENTIFIC CORPORATION

ABBOTT

LIVANOVA PLC

NEVRO CORP.

NEUROPACE, INC.

BIOVENTUS

ELECTROCORE, INC.

HELIUS MEDICAL TECHNOLOGIES, INC.

NEURONETICS

기타 기업

NEUROSIGMA, INC.

SOTERIX MEDICAL INC.

SYNAPSE BIOMEDICAL INC.

ALEVA NEUROTHERAPEUTICS

THERANICA BIO-ELECTRONICS LTD.

GIMER MEDICAL

NALU MEDICAL, INC.

MICROTRANSPONDER INC.

MAGSTIM

AMBER THERAPEUTICS

TVNS TECHNOLOGIES GMBH

BIOWAVE

BIOTRONIK

SALUDA MEDICAL PTY LTD.

SPR

제13장 부록

LSH

영문 목차

영문목차

The global neuromodulation market is projected to reach USD 10.68 billion by 2030 from USD 6.81 billion in 2025, at a CAGR of 9.4% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Technology, Stimulation Type, Application, and End User

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

The neuromodulation market is expanding due to the rising prevalence of neurological disorders, the development of new neuromodulation technologies, and the increasing geriatric population, all of which contribute to market growth. Additionally, the high cost of neuromodulation procedures may limit the market growth.

"The hospitals & ambulatory surgery centers segment of the neuromodulation end user market is expected to hold the largest position during the forecast period."

By end user, it is segmented into hospitals & ambulatory surgery centers, clinics & physiotherapy centers, and other end users. In 2024, hospitals & ambulatory surgery centers will hold the largest market share. The hospitals and ambulatory care segment dominates the neuromodulation market due to its ability to provide comprehensive, multidisciplinary care and access to advanced neuromodulation therapies. These settings are equipped with specialized surgical facilities, trained clinicians, and monitoring systems necessary for implantable and complex neuromodulation procedures. Hospitals and ambulatory centers also benefit from established reimbursement frameworks, making costly procedures more accessible to patients. Moreover, the increasing focus on chronic disease management, postoperative care, and patient follow-up is driving high procedure volumes in these settings, reinforcing their leadership in neuromodulation delivery solutions.

"The internal neuromodulation accounted for the largest market share in the neuromodulation market."

The neuromodulation technology market is segmented into internal neuromodulation and external neuromodulation. The internal neuromodulation segment accounted for the largest share in the neuromodulation market in 2024. Internal neuromodulation has become the dominant approach in the market due to its sophisticated technology that facilitates targeted stimulation of specific neural pathways. This process is instrumental in the chronic management of conditions such as nociceptive pain, Parkinson's disease, and urinary or fecal incontinence. The implantable devices are characterized by features like rechargeable or long-lasting batteries, customizable stimulation protocols, closed-loop feedback mechanisms, and wireless connectivity. These capabilities enable real-time monitoring and tailored therapeutic adjustments to enhance patient outcomes. The technological advancements support compact device designs that minimize invasiveness, thereby improving patient comfort and adherence to treatment. Furthermore, ongoing innovation in materials science, electrode architecture, and software algorithms continues to improve the efficacy, safety, and longevity of these systems. As a result, internal neuromodulation is increasingly favored over non-invasive interventions in clinical practice.

"The Asia Pacific is the fastest-growing region of the neuromodulation market by region."

The global neuromodulation market is divided into five regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific is the fastest-growing area in the neuromodulation market due to increasing health awareness, a rising rate of neurological and chronic pain disorders, and expanding healthcare infrastructure in countries like China, India, and Japan. The region is seeing greater adoption of advanced neuromodulation technologies, helped by better reimbursement policies and government efforts to improve access to medical devices. Additionally, a large patient population, higher disposable incomes, and increased investments from both global and local device manufacturers are fueling market growth. The push to establish specialized treatment centers and the gradual adoption of minimally invasive and implantable products further boost neuromodulation use in the region. Moreover, the rise in medical tourism in countries such as India, Thailand, and Singapore is increasing surgical volumes, which in turn raises the demand for post-operative care and neuromodulation.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1: 28%, Tier 2: 42%, and Tier 3: 30%

By Designation: C Level: 30%, Director Level: 34%, and Others: 36%

By Region: North America: 51%, Europe: 21%, Asia Pacific: 18%, Latin America: 6%, and Middle East & Africa: 4%

Note 1: Companies are classified into tiers based on their total revenue. As of 2023, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the neuromodulation market are Medtronic (US), Boston Scientific Corporation (US), Abbott (US), LivaNova PLC (UK), Nevro Corp (US), NeuroPace, Inc. (US), Bioventus (US), electroCore, Inc. (US), Helius Medical Technologies, Inc. (US), and Neuronetics (US).

Research Coverage

This report examines the neuromodulation market based on technology, stimulation type, application, end user, and country. It also analyzes factors such as drivers, restraints, opportunities, and challenges that influence market growth, along with details of the competitive landscape for market leaders. Additionally, the report studies micro markets according to their individual growth trends. It forecasts the revenue of market segments across five major regions and their respective countries.

Reasons to Buy the Report

The report will help both established and smaller firms to understand market trends, which, in turn, will assist them in gaining a larger market share. Companies purchasing the report can use one or a combination of the strategies listed below to strengthen their market position.

This report provides insights into the following pointers:

Analysis of key drivers (rising prevalence of neurological disorders and nerve injuries, rising geriatric population and subsequent growth in prevalence of neurological disorders, rising government support and funding for neurological disorders, increasing focus on development of advanced neuromodulation and neurostimulation technologies, increasing collaborations among device manufacturers, healthcare providers, and research institutions to develop neuromodulation devices, and availability of reimbursements for neuromodulation devices), restraints (high cost of neuromodulation procedures, preference for drug therapies over neuromodulation products, and adverse effects and complications associated with neuromodulation devices), opportunities (large population and increasing healthcare expenditure in emerging economies, and widening application scope of neuromodulation), challenges (stringent regulatory framework and time-consuming approval processes for neuromodulation and neurostimulation devices, and shortage of trained professionals)

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the neuromodulation market

Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the neuromodulation market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the neuromodulation market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key objectives of primary research

2.1.2.2 List of primary sources

2.1.2.3 Key data from primary sources

2.1.2.4 Breakdown of primary interviews

2.1.2.5 Insights from industry experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Revenue estimation of key players

2.2.1.2 Study of annual reports and investor presentations

2.2.1.3 Primary interviews

2.2.1.4 Growth forecast

2.2.1.5 CAGR projections

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 STUDY ASSUMPTIONS

2.4.1 RESEARCH-RELATED ASSUMPTIONS

2.4.2 PARAMETRIC ASSUMPTIONS

2.4.3 GROWTH-RATE ASSUMPTIONS

2.4.4 MARKET ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN NEUROMODULATION MARKET

4.2 ASIA PACIFIC: NEUROMODULATION MARKET, BY END USER AND COUNTRY, 2024

5.13.1 USE OF NEURALMODULATION TECHNOLOGIES IN RESEARCH, CLINICAL PRACTICE, AND CONSUMER APPLICATIONS

5.13.2 PAIRING TRANSLINGUAL NEUROSTIMULATION WITH INTENSIVE REHABILITATION TO ENHANCE NEUROPLASTICITY AND IMPROVE MOTOR RECOVERY IN SEVERE TRAUMATIC BRAIN INJURY PATIENTS

5.13.3 APPLICATION OF NEUROMODULATION TECHNIQUES-FROM NON-INVASIVE BRAIN STIMULATION TO DEEP BRAIN STIMULATION

5.14 REGULATORY ANALYSIS

5.14.1 REGULATORY LANDSCAPE

5.14.1.1 North America

5.14.1.1.1 US

5.14.1.1.2 Canada

5.14.1.2 Europe

5.14.1.3 Asia Pacific

5.14.1.3.1 China

5.14.1.3.2 Japan

5.14.1.3.3 India

5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15 PORTER'S FIVE FORCES ANALYSIS

5.15.1 BARGAINING POWER OF SUPPLIERS

5.15.2 BARGAINING POWER OF BUYERS

5.15.3 THREAT OF NEW ENTRANTS

5.15.4 THREAT OF SUBSTITUTES

5.15.5 INTENSITY OF COMPETITIVE RIVALRY

5.16 KEY STAKEHOLDERS & BUYING CRITERIA

5.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.16.2 KEY BUYING CRITERIA

5.17 IMPACT OF AI/GEN AI ON NEUROMODULATION MARKET

5.17.1 INTRODUCTION

5.17.2 POTENTIAL OF AI

5.17.3 IMPACT OF AI

5.17.4 KEY COMPANIES IMPLEMENTING AI

5.17.5 FUTURE OF AI

5.18 IMPACT OF 2025 US TARIFF ON NEUROMODULATION MARKET

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 PRICE IMPACT ANALYSIS

5.18.4 IMPACT ON COUNTRY/REGION

5.18.4.1 North America

5.18.4.2 Europe

5.18.4.3 Asia Pacific

5.18.5 IMPACT ON END-USE INDUSTRIES

5.18.5.1 Hospitals

6 NEUROMODULATION MARKET, BY TECHNOLOGY

6.1 INTRODUCTION

6.2 INTERNAL NEUROMODULATION

6.2.1 INTERNAL NEUROMODULATION TO RESULT IN BETTER TREATMENT RESULTS AND LOWER HEALTHCARE COSTS

6.3 EXTERNAL NEUROMODULATION

6.3.1 RISING DEMAND FOR NON-INVASIVE SOLUTIONS FOR NEUROLOGICAL AND PAIN-RELATED DISORDERS TO FUEL GROWTH

7 NEUROMODULATION MARKET, BY STIMULATION TYPE

7.1 INTRODUCTION

7.2 SPINAL CORD STIMULATION

7.2.1 GROWING INCIDENCE OF SPINAL CORD INJURIES TO FUEL MARKET GROWTH

7.3 DEEP BRAIN STIMULATION

7.3.1 MINIMALLY INVASIVE DEEP BRAIN STIMULATION TO DELIVER CONTROLLED ELECTRICAL IMPULSES AND REDUCE SIDE EFFECTS

7.4 SACRAL NERVE STIMULATION

7.4.1 INCREASING PREVALENCE OF CHRONIC URINARY INCONTINENCE AMONG ELDERLY WOMEN TO PROPEL MARKET GROWTH

7.5 VAGUS NERVE STIMULATION

7.5.1 RISING INCIDENCE OF EPILEPSY TO DRIVE ADOPTION OF NEXT-GENERATION VAGUS NERVE STIMULATION THERAPY

7.6 GASTRIC NERVE STIMULATION

7.6.1 INCREASING PREVALENCE OF GASTROESOPHAGEAL REFLUX DISEASE AND GASTROPARESIS TO FUEL MARKET GROWTH

7.7 TRANSCUTANEOUS ELECTRICAL NERVE STIMULATION

7.7.1 LOW COST AND EASE OF USE TO FUEL ADOPTION IN HEALTHCARE SECTOR

7.8 TRANSCRANIAL MAGNETIC STIMULATION

7.8.1 MINIMAL PATIENT DISCOMFORT ASSOCIATED WITH TRANSCRANIAL MAGNETIC STIMULATION TO SUPPORT DEMAND

7.9 RESPIRATORY ELECTRICAL STIMULATION

7.9.1 HIGH TREATMENT EFFICACY AND INCREASED FOCUS ON MINIMALLY INVASIVE SPINAL CORD TREATMENT TO FUEL MARKET GROWTH

7.10 OTHER STIMULATION TYPES

8 NEUROMODULATION MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 NEUROMODULATION MARKET FOR SPINAL CORD STIMULATION, BY APPLICATION

8.2.1 CHRONIC PAIN

8.2.1.1 High incidence of chronic pain among geriatric population to support market growth

8.2.2 FAILED BACK SURGERY SYNDROME

8.2.2.1 Increasing number of spinal surgeries to aid market growth

8.2.3 ISCHEMIA

8.2.3.1 High effectiveness of neuromodulation to boost effectiveness for ischemia treatment

8.3 NEUROMODULATION MARKET FOR DEEP BRAIN STIMULATION, BY APPLICATION

8.3.1 PARKINSON'S DISEASE

8.3.1.1 Development of advanced solutions and increased R&D to improve market growth

8.3.2 TREMORS

8.3.2.1 Increased prevalence of tremors and high efficacy of deep brain stimulation to drive market

8.3.3 DEPRESSION

8.3.3.1 Ongoing research and clinical studies to boost adoption of deep brain stimulation for depression treatment

8.3.4 OTHER DEEP BRAIN STIMULATION APPLICATIONS

8.4 NEUROMODULATION MARKET FOR SACRAL NERVE STIMULATION, BY APPLICATION

8.4.1 URINE INCONTINENCE

8.4.1.1 High incidence of urine incontinence to offer growth opportunities for market players

8.4.2 FECAL INCONTINENCE

8.4.2.1 Reduced symptom recurrence with sacral nerve stimulation to aid long-term management of fecal incontinence

8.5 NEUROMODULATION MARKET FOR VAGUS NERVE STIMULATION, BY APPLICATION

8.5.1 EPILEPSY

8.5.1.1 Low risk with device implantation and long-lasting battery life to aid market growth

8.5.2 OTHER VAGUS NERVE STIMULATION APPLICATIONS

8.6 NEUROMODULATION MARKET FOR GASTRIC ELECTRICAL STIMULATION, BY APPLICATION

8.6.1 GASTROPARESIS

8.6.1.1 Reduced hospitalization time associated with sastroparesis treatment to augment market growth

8.6.2 OBESITY

8.6.2.1 High prevalence of obesity and risks associated with gastric bypass to propel market growth

8.7 NEUROMODULATION MARKET FOR TRANSCUTANEOUS ELECTRICAL NERVE STIMULATION, BY APPLICATION

8.7.1 TREATMENT-RESISTANT DEPRESSION

8.7.1.1 High prevalence of chronic and recurrent depression to augment market growth

8.7.2 OTHER TRANSCUTANEOUS ELECTRICAL NERVE STIMULATION APPLICATIONS

8.8 NEUROMODULATION MARKET FOR TRANSCRANIAL MAGNETIC STIMULATION, BY APPLICATION

8.8.1 DEPRESSION

8.8.1.1 Repeated transcranial magnetic stimulation to be well-tolerated procedure with improved acceptance among patients

8.8.2 MIGRAINE

8.8.2.1 High prevalence of migraines to support market growth

8.9 NEUROMODULATION MARKET FOR RESPIRATORY ELECTRICAL STIMULATION, BY APPLICATION

8.9.1 INCREASING INCIDENCE OF SPINAL CORD INJURIES TO ENSURE CONTINUED DEMAND FOR ADVANCED TREATMENT OPTIONS

8.10 OTHER APPLICATIONS

9 NEUROMODULATION MARKET, BY END USER

9.1 INTRODUCTION

9.2 HOSPITALS & AMBULATORY SURGERY CENTERS

9.2.1 ADVANCED INFRASTRUCTURE AND ABILITY TO MANAGE COMPLEX NEUROLOGICAL CASES TO PROPEL MARKET GROWTH

9.3 CLINICS & PHYSIOTHERAPY CENTERS

9.3.1 NEED FOR FOCUSED EXPERTISE AND BETTER REHABILITATION MANAGEMENT TO ACCELERATE MARKET EXPANSION

9.4 OTHER END USERS

10 NEUROMODULATION MARKET, BY REGION

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

10.2.2 US

10.2.2.1 US to dominate North American neuromodulation market during forecast period

10.2.3 CANADA

10.2.3.1 Increasing neurological disorder rates and rising government funding to propel market growth

10.3 EUROPE

10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

10.3.2 GERMANY

10.3.2.1 Advanced surgical innovations and favorable reimbursement policies to drive market

10.3.3 FRANCE

10.3.3.1 Favorable healthcare reforms to drive adoption of advanced neuromodulation techniques

10.3.4 UK

10.3.4.1 Increased public & private sector healthcare expenditure and investments to fuel market growth

10.3.5 ITALY

10.3.5.1 Rising cases of dementia and Alzheimer's among geriatric population to spur market growth

10.3.6 SPAIN

10.3.6.1 Favorable government-led healthcare initiatives to support market growth

10.3.7 RUSSIA

10.3.7.1 Shifting demographic landscape and escalating neurological health needs to drive demand

10.3.8 REST OF EUROPE

10.4 ASIA PACIFIC

10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

10.4.2 CHINA

10.4.2.1 Government-led healthcare reforms and high prevalence of neurological disorders to fuel demand

10.4.3 JAPAN

10.4.3.1 Innovative healthcare delivery and advanced infrastructure landscape to augment market growth

10.4.4 INDIA

10.4.4.1 Booming medical tourism and rising middle class with higher disposable incomes to accelerate market growth

10.4.5 AUSTRALIA

10.4.5.1 Increasing cases of depressive and post-traumatic stress disorders to propel market demand

10.4.6 REST OF ASIA PACIFIC

10.5 LATIN AMERICA

10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

10.5.2 BRAZIL

10.5.2.1 Improvements in healthcare infrastructure to aid market growth

10.5.3 MEXICO

10.5.3.1 Expanding healthcare awareness and growing burden of neurological disorders to favor market growth

10.5.4 REST OF LATIN AMERICA

10.6 MIDDLE EAST & AFRICA

10.6.1 IMPROVEMENTS IN HEALTHCARE INFRASTRUCTURE AND INCREASED AWARENESS OF NEUROLOGICAL CARE TO DRIVE MARKET

10.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

11.1 INTRODUCTION

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

11.2.1 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN NEUROMODULATION MARKET

11.3 REVENUE ANALYSIS, 2020-2024

11.4 MARKET SHARE ANALYSIS, 2024

11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.5.1 STARS

11.5.2 EMERGING LEADERS

11.5.3 PERVASIVE PLAYERS

11.5.4 PARTICIPANTS

11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.5.5.1 Company footprint

11.5.5.2 Region footprint

11.5.5.3 Technology footprint

11.5.5.4 Stimulation type footprint

11.5.5.5 End-user footprint

11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024