Welding Materials Market by Type (Electrodes & Filler Materials, Fluxes & Wires, Gases), Technology (Arc, Resistance, Oxy-Fuel Welding), End-use Industry (Transportation, Building & Construction, Heavy Industries), and Region - Global Forecast to 2030

상품코드:1812626

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 218 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

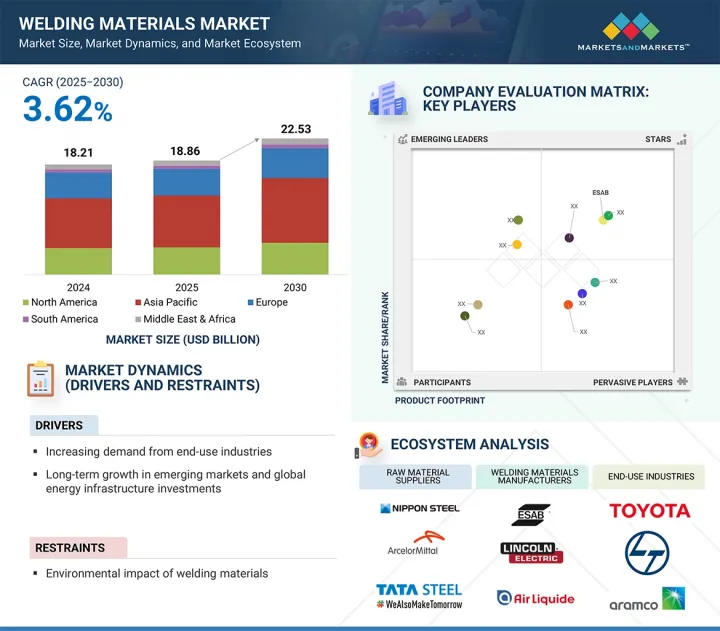

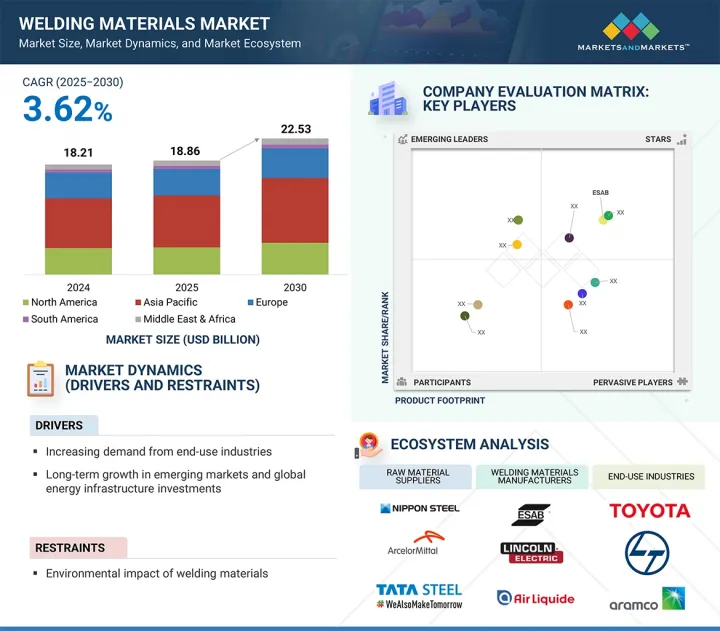

용접 재료 시장 규모는 2025년 188억 6,000만 달러에서 2030년에는 225억 3,000만 달러로 성장할 것으로 예측되며, 예측 기간 동안 CAGR 3.62%가 될 것으로 보입니다.

건축 및 건설 부문의 지출 증가, 제조업의 발전, 수리 및 유지보수 활동의 증가는 용접 재료에 대한 수요를 촉진할 것으로 예상됩니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러/10억 달러)

부문

기술별, 유형별, 최종 이용 산업별, 지역별

대상 지역

아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미

주택 건설 및 기존 인프라의 개보수 및 재구축의 증가는 용접 재료 시장을 끌어올릴 가능성이 높습니다. 그러나 이 시장은 환경에 미치는 영향에 대한 도전에 직면해 있습니다. 용접 재료의 환경 영향은 생산, 사용, 폐기가 포함되며 대기 질, 자원 소비, 폐기물 관리에 영향을 미칩니다.

아크 용접은 예측 기간 동안 용접 재료 시장에서 가장 큰 부문이 될 것으로 예상됩니다. 이 용접법은 전극과 모재 사이에 전기 아크가 형성되어 금속을 녹이는 용접 공정 중 고농도의 열에 의한 장점이 있습니다. 안정적인 금속 침전, 우수한 내식성, 높은 충격 인성도 주요 용접 기술로서의 지위에 기여하고 있습니다. 아크 용접은 저렴한 가격과 다양한 금속 표면에 대한 범용성으로 인해 용접 업계에서 선호되고 있습니다. 아크 용접이 신뢰할 수 있고 견고하며 효율적인 금속 접합을 필요로 하는 산업에서 아크 용접이 계속해서 인기 있는 용접 재료로 사용되는 이유는 바로 이러한 장점 때문입니다.

전극과 필러 재료는 주로 용접에 사용되는데, 이는 강인하고 내구성이 뛰어나며 고품질의 용접 조인트를 만드는 데 필수적이기 때문입니다. 용접 전극은 다양한 용접 방법과 용도에 사용할 수 있습니다. 용접 전극은 전극 홀더에서 접합되는 금속 표면에 전기를 통하게 하는 도관 역할을 합니다. 또한, 용접 시 필요한 용가재를 공급하는 역할도 합니다. 용가재는 용접 시 생기는 틈새를 메우기 위해 사용되는 소모품입니다. 이 틈새는 보통 두 개의 금속 조각을 접합할 때 발생하며, 이를 메우면 용접 어셈블리의 강도와 기능이 향상됩니다.

중공업은 용접 재료 시장에서 두 번째로 큰 부문이 될 것으로 예상됩니다. 중공업은 용접을 많이 사용하는데, 이는 용접이 견고하고 내구성이 뛰어나며 완전성이 높은 접합부를 필요로 하는 대형 장비 및 구조물의 제조, 조립, 유지보수에 필수적이기 때문입니다. 조선, 석유 및 가스, 광업, 철도, 중장비 제조 등의 분야에서는 두꺼운 고강도 강판과 복잡한 조립 부품을 다루기 때문에 전극, 플럭스, 필러, 와이어 등 다양한 용접 소모품이 필요합니다.

아시아태평양의 용접 재료 시장은 급속한 산업 개발, 인프라 프로젝트, 제조업의 성장으로 인해 확대되고 있습니다. 중국, 인도 등의 국가들은 교통 시스템, 도시 주택, 발전소, 항만, 산업단지에 많은 투자를 하고 있습니다. 대규모 건설 프로젝트 및 인프라 프로젝트에서는 철골 구조물, 파이프라인 및 부품의 대규모 용접이 필요하여 전극, 와이어 및 플럭스에 대한 수요가 증가하고 있습니다. 아시아태평양에는 중국, 일본, 인도, 한국, 태국에 주요 자동차 제조 기지가 있으며, 가전제품과 기계류의 주요 거점도 있습니다. 이러한 산업은 자동 용접 및 수동 용접에 의존하고 있으며, 상당한 재료를 소비하고 있습니다. 또한, 각국은 중장비 및 철도 제조의 생산능력을 높이고 있습니다.

대상 기업 : Air Liquide(프랑스), Air Products Inc.(미국), ESAB(미국), Illinois Tool Works Inc.(미국), Linde plc(독일), Lincoln Electric Holdings, Inc. Welding(인도), Tianjin Bridge Welding Materials Group(중국), Kobe Steel, Ltd.(일본), voestalpine AG(오스트리아) 등이 있습니다.

용접 재료 시장의 주요 기업들에 대한 상세한 경쟁 분석, 기업 프로파일, 최근 동향, 주요 시장 전략 등을 조사하여 전해드립니다.

조사 대상

이 보고서는 용접 재료 시장을 유형별(전극 및 필러 재료, 가스, 플럭스 및 와이어), 기술별(아크 용접, 저항 용접, 산소 연료 용접, 기타 기술), 최종사용 산업별(운송, 중공업, 건축 및 건설, 기타 최종사용 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류하고 있습니다. 이 보고서의 조사 범위에는 용접 재료 시장의 성장에 영향을 미치는 촉진요인, 시장 억제요인, 과제 및 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 기업 프로파일에 대한 철저한 분석을 통해 각 기업의 사업 개요, 제공 제품, 용접 재료 시장에서의 제휴, 계약, 제품 출시, 사업 확장, 인수 등 주요 전략에 대한 인사이트를 제공합니다. 또한, 용접 재료 생태계 내 신생기업들의 경쟁 분석도 함께 게재하고 있습니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

소개

시장 역학

업계 동향

고객 비즈니스에 영향을 미치는 동향/혼란

가격 분석

밸류체인 분석

생태계 분석

기술 분석

생성형 AI가 용접 재료 시장에 미치는 영향

특허 분석

무역 분석

2025-2026년의 주요 회의와 이벤트

규제 상황과 프레임워크

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

거시경제 분석

투자와 자금 조달 시나리오

2025년 미국 관세가 용접 재료 시장에 미치는 영향

제6장 용접 재료 시장(기술별)

소개

아크 용접

저항 용접

산소 연료 용접

기타

제7장 용접 재료 시장(유형별)

소개

전극 및 충전재

플럭스와 와이어

가스

제8장 용접 재료 시장(최종 이용 산업별)

소개

운송

중공업

건축·건설

기타

제9장 용접 재료 시장(지역별)

소개

아시아태평양

중국

일본

인도

인도네시아

기타

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

러시아

네덜란드

이탈리아

기타

중동 및 아프리카

GCC 국가

남아프리카공화국

기타

남미

브라질

아르헨티나

기타

제10장 경쟁 구도

개요

주요 진출 기업의 전략/강점

시장 점유율 분석

매출 분석

기업 평가와 재무 지표

제품/브랜드 비교

기업 평가 매트릭스 : 주요 진출 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제11장 기업 개요

주요 진출 기업

AIR LIQUIDE

AIR PRODUCTS AND CHEMICALS, INC.

ESAB

LINDE PLC

ILLINOIS TOOL WORKS INC.

THE LINCOLN ELECTRIC COMPANY

ADOR WELDING

TIANJIN BRIDGE WELDING MATERIALS GROUP CO.,LTD.

KOBE STEEL, LTD.

VOESTALPINE AG

기타 기업

PRECISION CASTPARTS CORP.

ROLLED ALLOYS

LAIWU JINCAI WELDING MATERIALS CO., LTD.

ADVANCED TECHNOLOGY & MATERIALS CO., LTD.

HYUNDAI WELDING CO.

ZULFI WELDING ELECTRODES FACTORY CO. LTD.

ATLANTIC CHINA WELDING CONSUMABLES

FORTIUS METALS

B&H GROUP

ROCKMOUNT

WELDFAST ELECTRODES PVT. LTD.

D&H SECHERON

GEDIK WELDING

SUPERON SCHWEISSTECHNIK INDIA

NEXA WELD

제12장 인접 시장

제13장 부록

KSM

영문 목차

영문목차

The welding materials market is projected to grow from USD 18.86 billion in 2025 to USD 22.53 billion by 2030, at a CAGR of 3.62% during the forecast period. The increase in spending in the building and construction sector, advancements in manufacturing industries, and the growth of repair and maintenance activities are expected to drive the demand for welding materials.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/USD Billion)

Segments

Type, Technology, End-use industry, and Region

Regions covered

Asia Pacific, North America, Europe, Middle East & Africa, and South America

The rise in residential construction and the renovation or rebuilding of existing infrastructure will likely push the welding materials market. However, the market faces challenges related to its environmental impact. The environmental effects of welding materials include their production, use, and disposal, affecting air quality, resource consumption, and waste management.

"Arc welding technology segment to lead market during forecast period"

Arc welding is expected to be the largest segment in the welding materials market during the forecast period. This method benefits from a high concentration of heat during the welding process, where an electric arc forms between the electrode and base materials, melting the metals. The consistent metal deposition, excellent corrosion resistance, and high impact toughness also contribute to its status as a leading welding technology. Arc welding is also preferred in the welding industry due to its affordability and versatility across various metal surfaces. These advantages explain why arc welding remains a popular choice in welding materials for industries that require reliable, strong, and efficient metal joining.

"Electrodes and filler materials to be largest segment during forecast period"

Electrodes and filler materials are primarily used in welding because they are essential for creating strong, durable, and high-quality welded joints. They can be employed across a wide range of welding methods and applications. Welding electrodes serve as the conduit that conducts electricity from the electrode holder to the metal surface being joined. They also supply the necessary filler material during welding. Filler materials are consumables used to fill gaps that may form during welding. These gaps typically occur when two metal pieces are joined, and filling them enhances the strength and functionality of the welded assembly.

"Heavy industries segment to hold second-largest share during forecast period"

Heavy industries are expected to be the second-largest segment of the welding materials market. Heavy industries use welding extensively because welding is critical for fabricating, assembling, and maintaining heavy-duty equipment and structures requiring strong, durable, and high-integrity joints. Sectors like shipbuilding, oil & gas, mining, railways, and heavy machinery manufacture work with thick, high-strength steel plates and complex assemblies requiring substantial welding consumables such as electrodes, fluxes, and filler wires.

"Asia Pacific welding materials market to record highest CAGR during forecast period"

The welding materials market in Asia Pacific is expanding due to rapid industrial development, infrastructure projects, and manufacturing growth. Countries like China and India are investing heavily in transportation systems, urban housing, power plants, ports, and industrial zones. Large construction and infrastructure projects require extensive welding for steel structures, pipelines, and components, boosting the demand for electrodes, wires, and fluxes. Asia Pacific also hosts major automotive manufacturing hubs in China, Japan, India, South Korea, and Thailand, along with key centers for appliances and machinery. These industries depend on automated and manual welding methods, which consume considerable materials. Furthermore, countries are ramping up their production abilities in heavy machinery and rail manufacturing.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Air Liquide (France), Air Products Inc. (US), ESAB (US), Illinois Tool Works Inc. (US), Linde plc (Germany), Lincoln Electric Holdings, Inc. (US), Ador Welding (India), Tianjin Bridge Welding Materials Group Co., Ltd. (China), Kobe Steel, Ltd. (Japan), and voestalpine AG (Austria) among others.

The study includes an in-depth competitive analysis of these key players in the welding materials market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the welding materials market by type (electrode & filler materials, gases, fluxes & wires), technology (arc welding, resistant welding, oxy fuel welding, other technologies), end-use industry (transportation, heavy industries, building & construction, and other end-use industries), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope includes detailed information on the drivers, restraints, challenges, and opportunities affecting the growth of the welding materials market. A thorough analysis of key industry players provides insights into their business profiles, products offered, and key strategies such as partnerships, agreements, product launches, expansions, and acquisitions in the welding materials market. This report also features a competitive analysis of emerging startups within the welding materials ecosystem.

Reasons to Buy Report

The report provides market leaders and new entrants with approximate revenue figures for the overall welding materials market and its subsegments. It helps stakeholders understand the competitive landscape, gain insights into positioning their businesses better, and develop appropriate go-to-market strategies. Additionally, the report offers information on key market drivers, restraints, challenges, and opportunities to help stakeholders grasp the market's pulse.

The report provides insights into the following points:

Analysis of key drivers (increasing demand from end-use industries, and long-term growth in emerging markets and investments in energy infrastructure), restraints (environmental impact of welding materials), opportunities (growth prospects in developing economies, and new and advanced applications), and challenges (shortage and high labor costs).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the welding materials market.

Market Development: Comprehensive information about profitable markets - the report analyzes the welding materials market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the welding materials market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and offerings of leading players such as Air Liquide (France), Air Products Inc. (US), ESAB (US), Illinois Tool Works Inc. (US), Linde plc (Germany), Lincoln Electric Holdings, Inc. (US), Ador Welding (India), Tianjin Bridge Welding Materials Group Co., Ltd. (China), Kobe Steel, Ltd. (Japan), and voestalpine AG (Austria).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 YEARS CONSIDERED

1.3.3 INCLUSIONS & EXCLUSIONS

1.3.4 CURRENCY CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key market insights

2.2 MARKET SIZE ESTIMATION

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RISK ASSESSMENT

2.6 GROWTH RATE ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WELDING MATERIALS MARKET

4.2 WELDING MATERIALS MARKET, BY REGION AND TYPE, 2024

4.3 WELDING MATERIALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing construction and automotive industries

5.2.1.2 Rising demand for energy and growing investments in renewable energy in emerging markets

5.2.2 RESTRAINTS

5.2.2.1 Environmental impact of welding materials

5.2.3 OPPORTUNITIES

5.2.3.1 Growth prospects in emerging economies

5.2.3.2 New and advanced applications

5.2.4 CHALLENGES

5.2.4.1 Shortage of skilled labor and high labor cost

5.3 INDUSTRY TRENDS

5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.5 PRICING ANALYSIS

5.6 VALUE CHAIN ANALYSIS

5.7 ECOSYSTEM ANALYSIS

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Advanced filler materials

5.8.1.2 Shielding gas innovations

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Welding automation & robotics

5.8.2.2 Weld imperfection detections

5.8.3 ADJACENT TECHNOLOGIES

5.8.3.1 Additive manufacturing

5.8.3.2 Surface coating technologies

5.9 IMPACT OF GEN AI ON WELDING MATERIALS MARKET

5.9.1 INTRODUCTION

5.10 PATENT ANALYSIS

5.10.1 INTRODUCTION

5.10.2 METHODOLOGY

5.11 TRADE ANALYSIS

5.11.1 EXPORT SCENARIO (HS CODE 3811)

5.11.2 IMPORT SCENARIO (HS CODE 3811)

5.12 KEY CONFERENCES AND EVENTS, 2025-2026

5.13 REGULATORY LANDSCAPE AND FRAMEWORK

5.13.1 REGULATORY LANDSCAPE

5.13.1.1 Regulatory bodies, government agencies, and other organizations

5.13.2 REGULATORY FRAMEWORK

5.13.2.1 AWS A5 series

5.13.2.2 ISO 2560:2020

5.13.2.3 ISO 14341:2020

5.14 PORTER'S FIVE FORCES ANALYSIS

5.14.1 THREAT OF NEW ENTRANTS

5.14.2 THREAT OF SUBSTITUTES

5.14.3 BARGAINING POWER OF SUPPLIERS

5.14.4 BARGAINING POWER OF BUYERS

5.14.5 INTENSITY OF COMPETITIVE RIVALRY

5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2 BUYING CRITERIA

5.16 CASE STUDY ANALYSIS

5.17 MACROECONOMIC ANALYSIS

5.17.1 INTRODUCTION

5.17.2 GDP TRENDS AND FORECASTS

5.18 INVESTMENT AND FUNDING SCENARIO

5.19 IMPACT OF 2025 US TARIFF ON WELDING MATERIALS MARKET

5.19.1 INTRODUCTION

5.19.2 KEY TARIFF RATES

5.19.3 PRICE IMPACT ANALYSIS

5.19.4 IMPACT ON COUNTRY/REGION

6 WELDING MATERIALS MARKET, BY TECHNOLOGY

6.1 INTRODUCTION

6.2 ARC WELDING

6.2.1 UNIFORMITY IN METAL DEPOSITION, GOOD CORROSION AND HIGH IMPACT RESISTANCE TO DRIVE MARKET

6.3 RESISTANCE WELDING

6.3.1 DEMAND FOR LONG PRODUCTION RUNS AND CONSISTENT CONDITIONS TO BOOST GROWTH

6.4 OXY-FUEL WELDING

6.4.1 PORTABILITY AND WELDING NON-FERROUS AND FERROUS METALS TO PROPEL MARKET

6.5 OTHER TECHNOLOGIES

7 WELDING MATERIALS MARKET, BY TYPE

7.1 INTRODUCTION

7.2 ELECTRODES & FILLER MATERIALS

7.2.1 ECONOMICAL AND WIDE APPLICABILITY TO FUEL MARKET GROWTH

7.3 FLUXES & WIRES

7.3.1 HIGH DEPOSITION RATE, FLEXIBILITY, AND USE IN EXTERNAL ENVIRONMENTS TO SUPPORT GROWTH

7.4 GASES

7.4.1 USE WITH OR WITHOUT PRESSURE AND PROTECTION OF MOLTEN METALS FROM CONTAMINATION AND OXIDATION TO DRIVE MARKET

8 WELDING MATERIALS MARKET, BY END-USE INDUSTRY

8.1 INTRODUCTION

8.2 TRANSPORTATION

8.2.1 INCREASING SALES OF ELECTRIC VEHICLES TO BOOST MARKET

8.3 HEAVY INDUSTRIES

8.3.1 DEMAND FOR REPAIRING SHIPS, PIPELINES, AND OFFSHORE OIL PLATFORMS TO DRIVE GROWTH

8.4 BUILDING & CONSTRUCTION

8.4.1 RISING CONSTRUCTION ACTIVITIES IN EMERGING ECONOMIES TO BOOST MARKET

8.5 OTHER END-USE INDUSTRIES

9 WELDING MATERIALS MARKET, BY REGION

9.1 INTRODUCTION

9.2 ASIA PACIFIC

9.2.1 CHINA

9.2.1.1 High demand from infrastructure, aerospace & defense, automobile, and marine industries to fuel market

9.2.2 JAPAN

9.2.2.1 Innovations in transportation industry to boost market

9.2.3 INDIA

9.2.3.1 Rising demand from automobile and construction sectors to drive market

9.2.4 INDONESIA

9.2.4.1 Growing population to boost demand in construction sector

9.2.5 REST OF ASIA PACIFIC

9.3 NORTH AMERICA

9.3.1 US

9.3.1.1 Significant oil & gas production to propel market

9.3.2 CANADA

9.3.2.1 Large automobile industry to offer opportunities for growth

9.3.3 MEXICO

9.3.3.1 Increasing demand from OEMs and automotive industry to boost growth

9.4 EUROPE

9.4.1 GERMANY

9.4.1.1 Rising installation of wind turbines and investments in automobile production facilities to propel growth

9.4.2 UK

9.4.2.1 Growth of automotive industry to offer lucrative opportunities

9.4.3 FRANCE

9.4.3.1 Increasing foreign investments in various end-use industries to drive market

9.4.4 RUSSIA

9.4.4.1 Rise in public and private construction projects to support growth

9.4.5 NETHERLANDS

9.4.5.1 Growth of manufacturing sector to contribute to demand

9.4.6 ITALY

9.4.6.1 Vast construction industry to favor growth

9.4.7 REST OF EUROPE

9.5 MIDDLE EAST & AFRICA

9.5.1 GCC COUNTRIES

9.5.1.1 Saudi Arabia

9.5.1.1.1 Increasing government investments in public infrastructure-related projects to support market growth

9.5.1.2 UAE

9.5.1.2.1 Operation 300bn to boost market growth

9.5.1.3 Rest of GCC countries

9.5.2 SOUTH AFRICA

9.5.2.1 Growing automotive sector to boost market

9.5.3 REST OF MIDDLE EAST & AFRICA

9.6 SOUTH AMERICA

9.6.1 BRAZIL

9.6.1.1 Economic development, industrialization, and urbanization to drive market

9.6.2 ARGENTINA

9.6.2.1 Government focus on automotive industry to propel market

9.6.3 REST OF SOUTH AMERICA

10 COMPETITIVE LANDSCAPE

10.1 OVERVIEW

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

10.3 MARKET SHARE ANALYSIS

10.4 REVENUE ANALYSIS

10.5 COMPANY VALUATION AND FINANCIAL METRICS

10.6 PRODUCT/BRAND COMPARISON

10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.7.1 STARS

10.7.2 EMERGING LEADERS

10.7.3 PERVASIVE PLAYERS

10.7.4 PARTICIPANTS

10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.7.5.1 Company footprint

10.7.5.2 Region footprint

10.7.5.3 End-use industry footprint

10.7.5.4 Type footprint

10.7.5.5 Technology footprint

10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024