와이어 및 케이블 관리 시장 : 제품별, 케이블 유형별, 재료별, 설치별, 최종 사용자별, 지역별 예측(-2030년)

Wire and Cable Management Market by Cable Type, Material, Installation, End User, Product, and Region - Global Forecast to 2030

상품코드:1810318

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 332 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

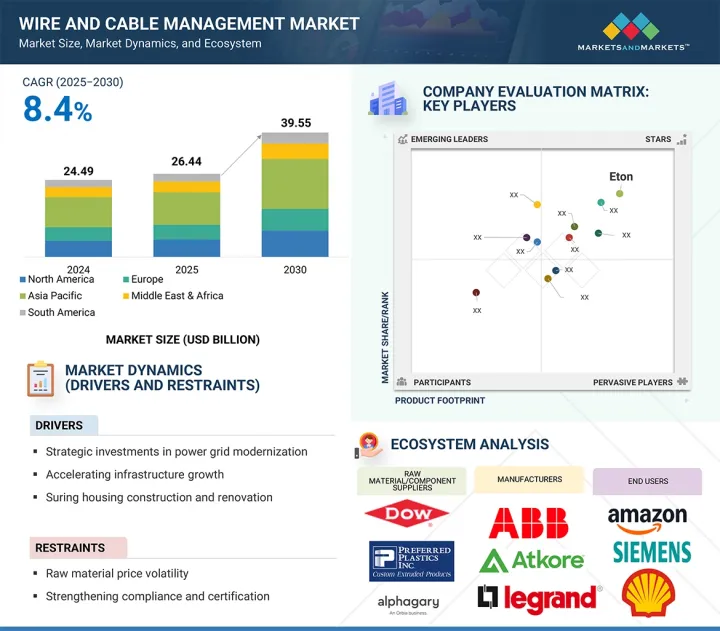

세계의 와이어 및 케이블 관리 시장 규모는 2025년 264억 4,000만 달러에서 2030년에는 395억 5,000만 달러로 성장할 것으로 예측되며, 예측 기간 중 CAGR 8.4%로 성장할 것으로 보입니다.

세계의 주요 시장에서 인프라 개척을 가속화할 필요성이 선진적인 와이어 및 케이블 관리 솔루션 수요에 박차를 가하고 있는 주요 요인입니다. 인도에서는 국가 인프라 파이프라인 및 자본 지출 증가를 통해 국가 주도의 인프라 투자가 부활하고 있으며, 전력 및 운송 등 성숙한 자산에 대한 재투자와 새로운 디지털 관련 인프라의 성장을 볼 수 있습니다. 이러한 시도는 전기 및 통신 시스템의 대규모 오버홀을 수반하며, 이러한 시스템과 관련된 전선의 수가 많고 매우 복잡하기 때문에 신속성을 보장하면서 안전한 환경을 구축하기 위해서는 매우 효율적으로 처리해야 합니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러/10억 달러)

부문

제품별, 케이블 유형별, 재료별, 설치별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카

미국에서, 인프라는 만성적인 자금 부족과 노후화가 계속되고 있으며, 연방 인프라 투자 정책은 인프라 투자 및 고용법 서명법안에 따라 1조 달러 규모의 지출을 포함한 에너지, 수송, 디지털 네트워크의 대폭적인 개선을 목표로 하고 있습니다. 이러한 첨단 인프라 개발로 송전망의 신뢰성을 높이고, 설치를 용이하게 하며, 운용 및 보수를 가능하게 하는 첨단 케이블 관리에 대한 수요가 높아지고 있습니다.

와이어 및 케이블 관리 시장에서 가장 중요한 부문에는 금속 부문이 포함됩니다. 이 부문의 케이블 및 와이어는 매우 강하고 내구성이 있으며 산업용 및 옥외 용도의 특징인 가혹한 환경을 견딜 수 있기 때문입니다. 금속 도관과 트레이는 높은 전자기장(EMI) 차폐를 제공하기 때문에 특수 전력 케이블 및 통신 케이블을 운반하는 장비에서 중요합니다. 또한 견고하고 건설 현장 및 산업 작업장과 같은 위험도가 높은 설비에 적합합니다. 이러한 보급은 구조의 안정성 및 신뢰성에 의해 촉진되고 금속 재료를 시장의 권위로 만듭니다.

특히 오프쇼어의 재생에너지 프로젝트 및 광대역 통신 네트워크 등 세계적인 데이터 전송 및 전력 상호 접속을 위한 해저 케이블 배치 증가에 따라 해저 케이블이 급속히 확대되고 있기 때문에 설치 부문은 와이어 및 케이블 관리 시장에서 가장 급성장하는 부문이 될 것으로 예측되고 있습니다. 해저 케이블은 대륙과 섬, 원격지의 해상 시설을 연결하기 위해 해저에 특수 케이블을 부설하는 것으로, 그 길이는 수천 킬로미터에 이르는 경우가 많습니다. 케이블 부설선, 고도의 매설 기술, 고전압 직류(HVDC) 시스템 등의 기술 진보가 성장을 뒷받침하고, 장거리의 송전 손실을 최소화하고, 재생에너지의 국가 송전망에 대한 통합을 지원하고 있습니다.

북미의 와이어 및 케이블 관리 시장은 인프라 개척 및 보수, 풍력 및 태양광 발전 프로젝트, 5G 도입 등 신흥국 통신 네트워크 증가 등 막대한 투자가 이루어지고 있기 때문에 2위 시장이 될 것으로 예측되고 있습니다. 이 지역의 혁신, 특히 청정 에너지와 지속 가능한 이니셔티브는 노후화된 인프라를 업데이트할 필요성과 함께 고품질의 오래된 케이블 솔루션에 대한 수요를 창출하고 있습니다. 게다가, 주택 및 상업 시설의 건설활동 증가와 전기차의 보급도 시장에 이익을 가져오고 있습니다. 또한 주요 기업의 시장 점유율 및 기술력이 높은 것도 북미가 주요 세계 시장임을 뒷받침하고 있습니다.

ABB(스위스), Legrand(프랑스), Atkore(미국), Eaton(아일랜드), nVent(미국)는 와이어 및 케이블 관리 시장의 주요 진출기업입니다. 이 조사에는 이러한 주요 기업의 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석이 포함되어 있습니다.

이 조사 보고서는 세계의 와이어 및 케이블 관리 시장을 제품 유형, 케이블 유형, 재료, 설치, 최종 사용자, 지역별로 정의, 설명 및 예측합니다. 또한 시장의 상세한 질적 및 양적 분석도 실시했습니다. 주요 시장 성장 촉진요인 및 억제요인, 기회 및 과제를 종합적으로 검토하고 있습니다. 또한 시장의 다양한 중요한 측면을 다룹니다. 여기에는 경쟁 구도, 시장 역학, 금액 기준 시장 추정, 와이어 및 케이블 관리 시장 전망 동향 등의 분석이 포함됩니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

서문

시장 역학

고객사업에 영향을 주는 동향 및 혼란

가격 분석

밸류체인 분석

생태계 분석

기술 분석

특허 분석

무역 분석

관세 및 규제 상황

주된 회의 및 이벤트(2025-2026년)

Porter's Five Forces 분석

주요 이해관계자 및 구매 기준

투자 및 자금조달 시나리오

사례 연구 분석

생성형 AI 및 AI가 와이어 및 케이블 관리 시장에 미치는 영향

와이어 및 케이블 관리 시장의 거시 경제 전망

미국 관세의 영향-개요(2025년)

제6장 와이어 및 케이블 관리 시장 : 제품별

서문

도관 및 트렁크

케이블 트레이 및 사다리

케이블 레이스웨이

접지 및 커넥터

박스 및 커버

배선 덕트

넥타이, 패스너, 클립

기타

제7장 와이어 및 케이블 관리 시장 : 케이블 유형별

서문

전원 케이블

통신 와이어 및 케이블

제8장 와이어 및 케이블 관리 시장 : 재료별

서문

금속

비금속

제9장 와이어 및 케이블 관리 시장 : 설치별

서문

가상

지하

해저

제10장 와이어 및 케이블 관리 시장 : 최종 사용자별

서문

주택

상업

공업

제11장 와이어 및 케이블 관리 시장 : 지역별

서문

아시아태평양

중국

인도

일본

호주

한국

기타

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

기타

중동 및 아프리카

GCC

남아프리카

기타

남미

브라질

아르헨티나

콜롬비아

기타

제12장 경쟁 구도

개요

주요 참가 기업의 전략 및 강점(2021-2025년)

시장 점유율 분석(2024년)

수익 분석(2020-2024년)

기업 평가 및 재무지표

브랜드 및 제품 비교

기업 평가 매트릭스 : 주요 진입기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

경쟁 시나리오

제13장 기업 프로파일

주요 진출기업

ABB

LEGRAND

ATKORE

EATON

NVENT

PANDUIT CORP.

BELDEN INC.

SCHNEIDER ELECTRIC

HUBBELL

HILTI

TE CONNECTIVITY

SALZER

3M

ILLINOIS TOOL WORKS INC.

NOVOFLEX

기타 기업

OBO BETTERMANN HOLDING GMBH & CO.KG

FISCHER GROUP

HELLERMANNTYTON

NIEDAX GROUP

CELO

LAPP GROUP

HELUKABEL

MOLEX

ICOTEK GMBH & CO. KG

PACER GROUP

제14장 부록

AJY

영문 목차

영문목차

The global wire and cable management market is estimated to grow from USD 26.44 billion in 2025 to USD 39.55 billion by 2030, at a CAGR of 8.4% during the forecast period. The need to drive faster expansion of infrastructural development in the key markets worldwide is a major factor that is spurring the demand for advanced wire and cable management solutions. India is witnessing a resurgence of state-driven investment in infrastructure through the National Infrastructure Pipeline and increased capital expenditure, which is seeing renewed investment in mature assets like power and transportation, and the growth of new digital-related infrastructure. Such endeavors entail major overhauls in electrical and communication systems, and the number of wires involved in these systems is large and highly complex, and needs to be handled very efficiently to create a secure environment with a guarantee of expediency.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion)

Segments

Product, Cable Type, Material, Installation, and End User

Regions covered

North America, Europe, Asia Pacific, South America, and Middle East & Africa

In the United States, infrastructure continues to be chronically underfunded and deteriorated, and federal infrastructure investment policy is targeting greatly upgrading energy, transport, and digital networks, including trillion-dollar spending, with the signature legislation of the Infrastructure Investment and Jobs Act. This high level of infrastructure development increases the demand for high-level cable management to drive grid reliability, ease installation, and enable operations and maintenance.

"By material, the metallic segment is expected to be the largest material segment in the wire and cable management market during the forecast period."

The segments that are the most significant in the wire and cable management market include the metallic segment since cables and wires in this segment are very strong, durable, and able to withstand rough environments, which are characteristic of the industrial and outdoor applications. Metal conduits and trays provide high electromagnetic field (EMI) shielding, making them important in equipment transporting special power and telecom cables. They are also rugged and therefore suitable for high-stakes installations such as construction sites and industrial workplaces. Such a prevalence, facilitated by structural stability and reliability, makes metallic materials the market authority.

"By installation, the submarine segment is the fastest segment in the wire and cable management market during the forecast period."

The installation segment is projected to be the fastest-growing segment in the wire and cable management market, as submarines are experiencing rapid expansion with increasing deployment of undersea cables for global data transmission and power interconnection, particularly in offshore renewable energy projects and high-bandwidth telecommunications networks. Submarine installations involve laying specialized cables on the ocean floor, often spanning thousands of kilometers, to connect continents, islands, and remote offshore facilities. The growth is fueled by technological advancements in cable-laying vessels, sophisticated burial techniques, and high-voltage direct current (HVDC) systems, which minimize transmission losses over long distances and support the integration of renewable energy into national grids.

"By region, North America is estimated to be the second-largest market during the forecast period."

The wire and cable management market in North America is forecast to be the second biggest market because of the vast investments in infrastructure development and maintenance, wind and solar energy projects, and increasing telecommunication networks, such as the 5G implementation. Innovation in the region, especially clean energy and sustainable initiatives, combined with the need to update aging infrastructure, generates demand for high-quality, long-lasting cable solutions. Moreover, rising residential and commercial construction activities, as well as the mounting electric cars, are also beneficial to the market. The significant market share of major players and technology also promotes North America's positioning as a major global market.

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 30%, Tier 2- 55%, and Tier 3 - 15%

By Designation: C-level Executives - 30%, Directors - 20%, and Others - 50%

By Region: North America - 20%, Europe - 8%, Asia Pacific - 55%, Middle East & Africa - 13%, and South America - 4%

Notes: The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million.

Other designations include sales managers, engineers, and regional managers.

ABB (Switzerland), Legrand (France), Atkore (US), Eaton ( Ireland), and nVent (US) are some of the major players in the wire and cable management market. The study includes an in-depth competitive analysis of these key players, including their company profiles, recent developments, and key market strategies.

Research Coverage:

The report defines, describes, and forecasts the global wire and cable management market by product, cable type, material, installation, end user, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates in terms of value, and future trends in the wire and cable management market.

Key Benefits of Buying the Report

It provides an analysis of key drivers (Strategic investments in power grid modernization are likely to propel the wire and cable management market; Accelerating infrastructure growth fueling demand for advanced wire and cable management solutions; Housing construction and renovation are major drivers of wiring and cable demand), restraints (Raw material price volatility; Strengthening compliance and certification to drive quality and innovation in the wire and cable management market), opportunities (Europe's investment in digital & submarine cable security; Clean cable and cybersecurity initiative), challenges (Counterfeit products and quality assurance are causing hindrance in the market) influencing the growth of the wire and cable management market.

Market Development: Comprehensive information about lucrative markets - the report analyses the wire and cable management market across varied regions.

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the wire and cable management market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like ABB (Switzerland), Legrand (France), Atkore (US), Eaton (Ireland), nVent (US), Panduit Corp (US), Belden Inc. (US), Schneider Electric (France), Hebbell (US), Hilti (Liechtenstein) and TE Connectivity (Ireland); among others in the wire and cable management market.

Product Innovation/Development: The market is investigating large product introduction rates, especially with the incorporation of IoT-based systems and predictive maintenance functionality, including LS Cable & System's i-Check platform to monitor applications remotely to prevent fires and outages. With use cases increasing in areas like renewable energy, data centers, and telecommunications as observed in the 5G, smart grids, 3D-printed custom components, and sustainable materials such as biodegradable ties, recycled plastics, the nature of modular solutions is evolving with the likes of AWM with its Helios Beam Rod and Photon Kit to make installation simple and efficient, and Panduit with its Wire Basket Cable Tray Routing System that provides versatile fiber and power cabling baskets.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.4 INCLUSIONS AND EXCLUSIONS

1.4.1 YEARS CONSIDERED

1.5 UNIT CONSIDERED

1.6 CURRENCY CONSIDERED

1.7 LIMITATIONS

1.8 STAKEHOLDERS

1.9 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of key primary interview participants

2.1.2.2 Key data from primary sources

2.1.2.3 Key data from primary sources

2.1.2.4 Breakdown of primaries

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Regional analysis

2.2.1.2 Country-wise analysis

2.2.1.3 Demand-side assumptions

2.2.1.4 Demand-side calculations

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Supply-side assumptions

2.2.2.2 Supply-side calculations

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 GROWTH FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RISK ANALYSIS

2.7 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WIRE AND CABLE MANAGEMENT MARKET

4.2 WIRE AND CABLE MANAGEMENT MARKET, BY REGION

4.3 WIRE AND CABLE MANAGEMENT MARKET IN ASIA PACIFIC, BY END USER AND COUNTRY

4.4 WIRE AND CABLE MANAGEMENT MARKET, BY PRODUCT

4.5 WIRE AND CABLE MANAGEMENT MARKET, BY CABLE TYPE

4.6 WIRE AND CABLE MANAGEMENT MARKET, BY MATERIAL

4.7 WIRE AND CABLE MANAGEMENT MARKET, BY INSTALLATION

4.8 WIRE AND CABLE MANAGEMENT MARKET, BY END USER

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Surging investments in clean energy

5.2.1.2 Emphasis on infrastructure modernization

5.2.1.3 Housing construction and renovations

5.2.2 RESTRAINTS

5.2.2.1 Susceptibility of raw materials to fluctuations

5.2.2.2 Extensive documentation, training, and quality control measures

5.2.3 OPPORTUNITIES

5.2.3.1 Substantial investments in submarine cable infrastructure

5.2.3.2 Growing emphasis on clean cable and cybersecurity initiatives

5.2.4 CHALLENGES

5.2.4.1 Issues related to counterfeit products and quality assurance

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE TREND OF WIRE AND CABLE MANAGEMENT, BY PRODUCT, 2021-2024

5.4.2 AVERAGE SELLING PRICE TREND OF WIRE AND CABLE MANAGEMENT, BY REGION, 2021-2024

5.5 VALUE CHAIN ANALYSIS

5.6 ECOSYSTEM ANALYSIS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Polyphenylene ether in cable accessories

5.7.1.2 Self-adhesive and flexible mounting clips

5.7.2 COMPLIMENTARY TECHNOLOGIES

5.7.2.1 Slip-on and cold-shrink

5.7.2.2 AI-driven cable management

5.7.3 ADJACENT TECHNOLOGIES

5.7.3.1 Hollow-core fiber optic cable

5.7.3.2 Science monitoring and reliable telecommunications (SMART) cables

5.8 PATENT ANALYSIS

5.9 TRADE ANALYSIS

5.9.1 IMPORT DATA (HS CODE 8547)

5.9.2 EXPORT DATA (HS CODE 8547)

5.10 TARIFF AND REGULATORY LANDSCAPE

5.10.1 TARIFF ANALYSIS

5.10.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.11 KEY CONFERENCES AND EVENTS, 2025-2026

5.12 PORTER'S FIVE FORCES ANALYSIS

5.12.1 THREAT OF NEW ENTRANTS

5.12.2 BARGAINING POWER OF BUYERS

5.12.3 BARGAINING POWER OF SUPPLIERS

5.12.4 THREAT OF SUBSTITUTES

5.12.5 INTENSITY OF COMPETITIVE RIVALRY

5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.13.2 BUYING CRITERIA

5.14 INVESTMENT AND FUNDING SCENARIO

5.15 CASE STUDY ANALYSIS

5.15.1 AFFORDABLE WIRE MANAGEMENT OPTIMIZES CABLE ROUTING AND REDUCES COSTS FOR MIDWEST SOLAR FARMS

5.15.2 ONESTOP CONTROLS AND PANDUIT SIMPLIFY CABLE MANAGEMENT AND ENHANCE ENCLOSURE PROTECTION FOR TEMPERATURE CONTROLLERS

5.15.3 EGAN COMPANY AND HELLERMANNTYTON CUT LABOR COSTS AND IMPROVE CABLE MANAGEMENT WITH RATCHET P-CLAMPS

5.16 IMPACT OF GEN AI/AI ON WIRE AND CABLE MANAGEMENT MARKET

5.16.1 ADOPTION OF GEN AI/AI IN WIRE AND CABLE MANAGEMENT MARKET

5.16.2 IMPACT OF GEN AI/AI ON WIRE AND CABLE MANAGEMENT MARKET, BY REGION

5.17 MACROECONOMIC OUTLOOK FOR WIRE AND CABLE MANAGEMENT MARKET

5.18 IMPACT OF 2025 US TARIFF - OVERVIEW

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 PRICE IMPACT ANALYSIS

5.18.4 IMPACT ON COUNTRIES/REGIONS

5.18.4.1 North America

5.18.4.2 Europe

5.18.4.3 Asia Pacific

5.18.4.4 South America

5.18.4.5 Middle East & Africa

5.18.5 IMPACT ON END USERS

6 WIRE AND CABLE MANAGEMENT MARKET, BY PRODUCT

6.1 INTRODUCTION

6.2 CONDUITS & TRUNKING

6.2.1 EMPHASIS ON MODERNIZING EXISTING WIRING INFRASTRUCTURE TO DRIVE MARKET

6.3 CABLE TRAYS & LADDERS

6.3.1 NEED TO COMPLY WITH SAFETY STANDARDS TO BOOST DEMAND

6.4 CABLE RACEWAYS

6.4.1 EASE OF INSTALLATION TO SUPPORT MARKET GROWTH

6.5 GLANDS & CONNECTORS

6.5.1 GROWING TECHNICAL COMPLEXITIES OF ELECTRONIC SYSTEMS TO DRIVE MARKET

6.6 BOXES & COVERS

6.6.1 REGULATORY EMPHASIS ON ACCIDENT PREVENTION AND WORKSPACE TIDINESS TO DRIVE MARKET

6.7 WIRING DUCTS

6.7.1 ORGANIZED CABLE ROUTING TO SUPPORT COMPLEX CONTROL SYSTEMS AND PANELS TO PROPEL MARKET GROWTH

6.8 TIES, FASTENERS, & CLIPS

6.8.1 EXPANDING TELECOMMUNICATION NETWORKS AND DIGITALIZATION ACROSS INDUSTRIES TO FUEL SEGMENTAL GROWTH

6.9 OTHER PRODUCTS

7 WIRE AND CABLE MANAGEMENT MARKET, BY CABLE TYPE

7.1 INTRODUCTION

7.2 POWER CABLES

7.2.1 RAPID URBANIZATION AND INFRASTRUCTURE MODERNIZATION TO DRIVE MARKET

7.3 COMMUNICATION WIRES & CABLES

7.3.1 EVOLVING DIGITAL ECOSYSTEM TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

8 WIRE AND CABLE MANAGEMENT MARKET, BY MATERIAL

8.1 INTRODUCTION

8.2 METALLIC

8.2.1 ONGOING ADVANCEMENTS IN ALLOY TECHNOLOGY TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

8.3 NON-METALLIC

8.3.1 GROWING EMPHASIS ON SUSTAINABILITY AND RECYCLABLE MATERIALS TO DRIVE MARKET

9 WIRE AND CABLE MANAGEMENT MARKET, BY INSTALLATION

9.1 INTRODUCTION

9.2 OVERHEAD

9.2.1 DEPLOYMENT IN REGIONS PRONE TO NATURAL DISASTERS TO FUEL SEGMENTAL GROWTH

9.3 UNDERGROUND

9.3.1 ABILITY TO WITHSTAND HARSH WEATHER CONDITIONS TO DRIVE MARKET

9.4 SUBMARINE

9.4.1 EXPANDING OFFSHORE ENERGY INFRASTRUCTURE TO FUEL MARKET GROWTH

10 WIRE AND CABLE MANAGEMENT MARKET, BY END USER

10.1 INTRODUCTION

10.2 RESIDENTIAL

10.2.1 GROWING APPLICATION OF IOT DEVICES AND HOME AUTOMATION SYSTEMS TO FUEL MARKET GROWTH

10.3 COMMERCIAL

10.3.1 OFFICES

10.3.1.1 Increasing adoption of hybrid work models and smart office technologies to foster market growth

10.3.2 RETAIL STORES AND MALLS

10.3.2.1 Rising popularity of interactive kiosks and LED lighting to support market growth

10.3.3 OTHER COMMERCIAL END USERS

10.4 INDUSTRIAL

10.4.1 IT & TELECOMMUNICATIONS

10.4.1.1 Adoption of Industry 4.0 and smart manufacturing technologies to drive market

10.4.2 ENERGY & UTILITIES

10.4.2.1 Global shift toward renewable energy and grid modernization to boost demand

10.4.3 MANUFACTURING

10.4.3.1 Rise of automated production lines and robotic systems to fuel market growth

10.4.4 OIL & GAS

10.4.4.1 Global need to maintain energy production and enhance operational safety to drive market

10.4.5 METALS & MINING

10.4.5.1 Increasing demand for metals critical to renewable energy and electrification to support market growth

10.4.6 WAREHOUSING & LOGISTICS

10.4.6.1 Expanding e-commerce and automation in logistics to boost demand

10.4.7 OTHER INDUSTRIAL END USERS

11 WIRE AND CABLE MANAGEMENT MARKET, BY REGION

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 CHINA

11.2.1.1 Growing investments in power grids to boost demand

11.2.2 INDIA

11.2.2.1 Expanding digital economy and telecom services to fuel market growth

11.2.3 JAPAN

11.2.3.1 Increasing focus on bridging urban-rural digital gap to support market growth

11.2.4 AUSTRALIA

11.2.4.1 Rise in natural gas production to drive market

11.2.5 SOUTH KOREA

11.2.5.1 Growing shift toward Industry 4.0 and smart factories to offer lucrative growth opportunities

11.2.6 REST OF ASIA PACIFIC

11.3 NORTH AMERICA

11.3.1 US

11.3.1.1 Rising investments in energy infrastructure, renewable projects, and grid modernization to boost demand

11.3.2 CANADA

11.3.2.1 Rapid modernization of electricity grids and expansion of renewable energy capacity to drive market

11.3.3 MEXICO

11.3.3.1 Robust investments in grid modernization and renewable energy capacity to boost demand

11.4 EUROPE

11.4.1 GERMANY

11.4.1.1 Rising emphasis on Industry 4.0 to fuel market growth

11.4.2 UK

11.4.2.1 Growing investments in electricity infrastructure to drive market

11.4.3 ITALY

11.4.3.1 Expansion of grid infrastructure to fuel market growth

11.4.4 FRANCE

11.4.4.1 Government-led initiatives to boost EV charging infrastructure to support market growth

11.4.5 SPAIN

11.4.5.1 Increasing demand for structured cable trays, conduits, and junction boxes to foster market growth

11.4.6 REST OF EUROPE

11.5 MIDDLE EAST & AFRICA

11.5.1 GCC

11.5.1.1 Saudi Arabia

11.5.1.1.1 Expanding smart city and giga-projects to offer lucrative growth opportunities

11.5.1.2 UAE

11.5.1.2.1 Rising demand for modular routing systems and robust containment in high-density IT environments to fuel market growth

11.5.1.3 REST OF GCC

11.5.2 SOUTH AFRICA

11.5.2.1 Expanding power network to drive market

11.5.3 REST OF MIDDLE EAST & AFRICA

11.6 SOUTH AMERICA

11.6.1 BRAZIL

11.6.1.1 Rising focus on strengthening data centers to support market growth

11.6.2 ARGENTINA

11.6.2.1 Increasing emphasis on enhancing fiber backbone infrastructure to fuel market growth

11.6.3 COLOMBIA

11.6.3.1 Growing data center investments and enhanced fiber connectivity to support market growth

11.6.4 REST OF SOUTH AMERICA

12 COMPETITIVE LANDSCAPE

12.1 OVERVIEW

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

12.3 MARKET SHARE ANALYSIS, 2024

12.4 REVENUE ANALYSIS, 2020-2024

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 BRAND/PRODUCT COMPARISON

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1 Company footprint

12.7.5.2 Region footprint

12.7.5.3 Product footprint

12.7.5.4 Material footprint

12.7.5.5 Cable type footprint

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024