정유소 및 석유화학 여과 시장 : 필터 유형별, 용도별, 최종 사용자별, 지역별 예측(-2030년)

Refinery and Petrochemical Filtration Market by Filter Type (Coalescer Filter, Cartridge Filter, Electrostatic Precipitator, Filter Press, Bag Filters, and Others) Application, End User, and Region - Global Forecast to 2030

상품코드:1804851

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 258 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

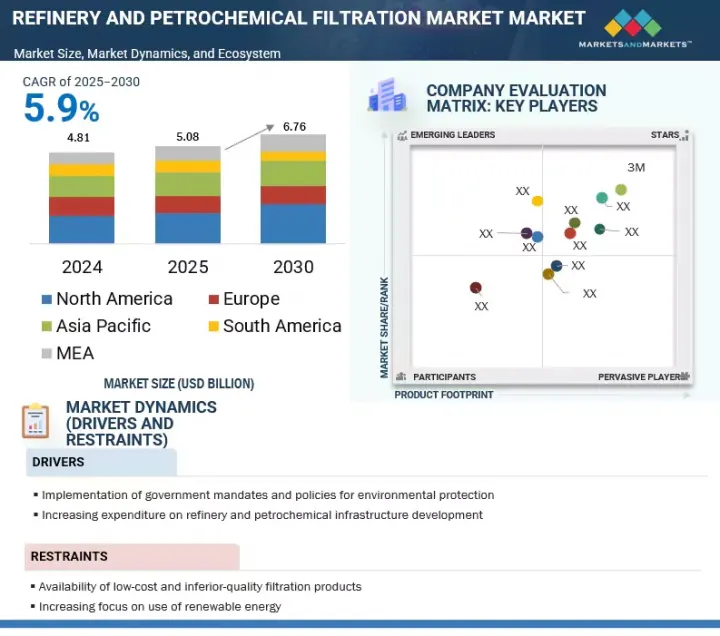

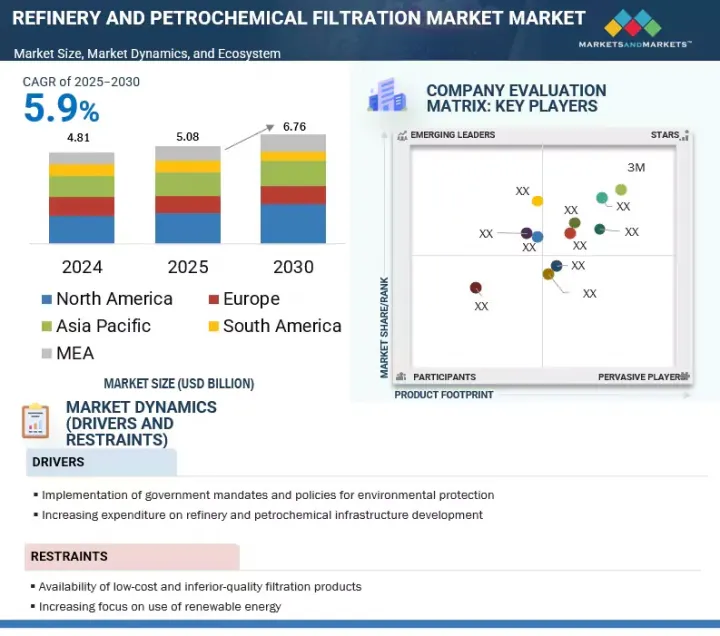

세계의 정유소 및 석유화학 여과 시장 규모는 2025년 50억 8,000만 달러에서 2030년까지 67억 6,000만 달러에 이를 것으로 예측되며, CAGR 5.9%로 성장할 전망입니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

100만 달러/10억 달러

부문

필터 유형, 용도, 최종 사용자

대상 지역

아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카

증가하는 에너지 수요는 다운스트림 투자를 촉진하여 시장 성장을 견인하고 있습니다. 그러나 여과기의 빈번한 교체 및 폐기는 운영 비용에 영향을 미치고 산업의 지속 가능성 및 폐기물 관리에 도전 과제를 야기하는 주요 제약 요인으로 작용합니다.

"석유화학 산업은 예측 기간 동안 가장 빠르게 성장하는 최종 사용자로 부상할 것으로 전망됩니다"

최종 사용자별로는 정유소 및 석유화학 여과 시장은 정유소와 석유화학 산업으로 세분화되었습니다. 석유화학 산업의 인프라 투자 증가가 석유화학 여과 수요를 견인할 것으로 예상됩니다. 경제 발전과 인구 증가에 따라 플라스틱, 합성 섬유, 비료, 화학 제품 등에 대한 수요가 증가하면서 석유화학 플랜트에 대한 투자가 확대되고 있습니다. 석유화학 플랜트 운영사는 원료 및 최종 제품에서 불순물, 오염 물질, 입자를 제거하기 위해 백 필터, 카트리지 필터, 멤브레인 필터, 응집기를 사용합니다.

"액체-액체 분리 부문이 두번쨰로 큰 용도 부문이 될 것으로 추정됩니다."

용도별로 보면, 액체-액체 분리 부문은 다운스트림 석유·가스 부문에서 핵심적인 역할을 수행하기 때문에 정유소 및 석유화학 여과 시장에서 두 번째로 큰 점유율을 차지합니다. 이는 제품 품질 사양을 충족하고 부식을 방지하기 위해 가솔린, 디젤, 등유, 제트 연료에서 물을 제거하는 데 필수적입니다. 이 분리 공정은 촉매 및 흡착제를 수분 오염으로부터 보호하고, 처리 공정에서 발생하는 가성 및 아민의 유출을 제거하며, 염 건조기 및 점토 타워와 같은 장비를 보호하는 데 도움이 됩니다. 액-액 분획의 높은 점유율은 전 세계 정제 능력 증가, 청정 연료에 대한 엄격한 규제, 효과적인 수분 및 불순물 제거를 통한 운영 효율성, 제품 순도 및 장비 수명 향상 필요성에 의해 주도되고 있습니다.

“아시아태평양이 2위 정유소 및 석유화학 여과시장이 될 것으로 추정됩니다.”

아시아태평양은 2025-2030년에 제2위의 정유소 및 석유화학 여과시장이 될 것으로 예측됩니다. 석유화학 제품 수요 증가로 인해 해당 지역의 다운스트림 부문이 성장하고 있습니다. 또한 이 지역 국가들은 정유소 입지에 있어 전략적 이점을 지니고 있어 중동 및 기타 지역으로부터 원유 공급에 접근할 수 있습니다. 또한 해당 지역 국가 정부들은 다운스트림 부문에 대한 외국인 투자를 유치하기 위한 정책과 인센티브를 시행해 왔습니다. 이러한 요소들이 아시아태평양 정유소 및 석유화학 여과 시장 성장을 촉진하는 핵심 요인입니다.

본 보고서에서는 세계의 정유소 및 석유화학 여과시장에 대해 조사 분석하여 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

정유소 및 석유화학 여과 시장의 기업에게 매력적인 기회

정유소 및 석유화학 여과 시장 : 지역별

북미의 정유소 및 석유화학 여과 시장 : 용도별, 국가별

정유소 및 석유화학 여과 시장 : 필터 유형별

정유소 및 석유화학 여과 시장 : 용도별

정유소 및 석유화학 여과 시장 : 최종 사용자별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

억제요인

기회

과제

고객사업에 영향을 주는 동향 및 혼란

생태계 분석

밸류체인 분석

원료 공급업체 및 공급자

정유소 및 석유화학 여과 시스템 제조업체

판매자 및 최종 사용자

애프터 서비스 제공업체

가격 설정 분석

치환율

기술 분석

관세 및 규제의 정세

정유소 및 석유화학 여과장치와 관련된 관세

규제기관, 정부기관, 기타 조직

정유소 및 석유화학 여과에 관한 규제

특허 분석

무역 분석

수출 시나리오

수입 시나리오

주요 컨퍼런스 및 이벤트(2025-2026년)

사례 연구 분석

JONELL SYSTEMS, 유럽의 정유소에서의 코어 레싱 비용을 삭감

JONELL SYSTEMS의 정유소용 전 여과 솔루션에 의해 미국의 정유소에서 200만 달러의 코스트 삭감을 실현

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

정유소 및 석유화학 여과 시장에 대한 생성형 AI/AI 영향

정유소 및 석유화학 여과 시장에 있어서의 생성형 AI/AI 채택

생성형 AI/AI 영향 : 최종 사용자별

정유소 및 석유화학 여과 시장에 대한 생성형 AI/AI 영향 : 지역별

세계의 거시경제 전망

소개

GDP의 동향과 예측

정유소 및 석유화학 여과시장에 대한 인플레이션 영향

미국 관세의 영향(2025년) - 개요

소개

주요 관세율

지역에 미치는 영향

제6장 정유소 및 석유화학 여과 시장 : 필터 유형별

소개

응집 필터

카트리지 필터

전기 집진기

여과 프레스

백 필터

기타 필터 유형

제7장 정유소 및 석유화학 여과 시장 : 용도별

소개

액체-액체 분리

액체-기체 분리

기타 용도

제8장 정유소 및 석유화학 여과 시장 : 최종 사용자별

소개

정유소

석유화학 산업

제9장 정유소 및 석유화학 여과 시장 : 지역별

소개

아시아태평양

필터 유형별

용도별

최종 사용자별

국가별

북미

필터 유형별

용도별

최종 사용자별

국가별

유럽

필터 유형별

용도별

최종 사용자별

국가별

중동 및 아프리카

필터 유형별

용도별

최종 사용자별

국가별

남미

필터 유형별

용도별

최종 사용자별

국가별

제10장 경쟁 구도

주요 기업이 채택한 전략

주요 참가 기업의 전략 및 강점(2020년 1월-2025년 7월)

상위 5개사의 시장 점유율 분석

수익 분석

기업 평가 및 재무 지표

브랜드 및 제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업의 평가 매트릭스 : 스타트업 기업/중소기업(2024년)

경쟁 시나리오

제11장 기업 프로파일

주요 기업

3M

EATON

PARKER HANNIFIN CORP.

PENTAIR

CAMFIL

WL GORE & ASSOCIATES, INC.

PALL CORPORATION

FILTRATION GROUP

FILTCARE TECHNOLOGY PVT. LTD.

FTC

PORVAIR FILTRATION GROUP

LENNTECH BV

AMAZON FILTERS LTD.

NORMAN FILTER COMPANY

SUNGOV ENGINEERING

기타 기업

FILSONFILTER

BROTHER FILTRATION

COMPOSITECH PRODUCTS MANUFACTURING, INC.

KEL INDIA FILTERS

YIXING HUADING MACHINERY CO., LTD.

제12장 부록

HBR

영문 목차

영문목차

The global refinery and petrochemical filtration market is projected to grow from USD 5.08 billion in 2025 to USD 6.76 billion by 2030, at a CAGR of 5.9%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion)

Segments

Refinery and petrochemical filtration market by filter type, application, and end user

Regions covered

Asia Pacific, North America, Europe, South America, and Middle East & Africa

Rising energy demand is driving increased downstream investments, boosting market growth. However, frequent replacement and disposal of filters pose a significant restraint, impacting operational costs and creating challenges for sustainability and waste management in the industry.

"The petrochemical industry is projected to emerge as the fastest-growing end user during the forecast period."

By end user, the refinery and petrochemical filtration market has been segmented into refineries and the petrochemical industry. Increasing infrastructure investments in the petrochemical industry are anticipated to drive the demand for petrochemical filtration. The rising investment in petrochemical plants is driven by increasing demand for products such as plastics, synthetic fibers, fertilizers, and chemicals as economies develop and populations grow. Petrochemical plant operators use bag filters, cartridge filters, membrane filters, and coalescers to remove impurities, contaminants, and particles from feedstocks and final products.

"The liquid-liquid segment is estimated to be the second-largest application."

Based on application, the liquid-liquid separation segment holds the second-largest share in the refinery and petrochemical filtration market due to its critical role in the downstream oil & gas sector. It is essential for removing water from gasoline, diesel, kerosene, and jet fuel to meet product quality specifications and prevent corrosion. This separation process helps to protect catalysts and adsorbents from water contamination, eliminates carryover of caustic and amine from treatment processes, and protects equipment such as salt dryers and clay towers. The high share of the liquid-liquid segment is driven by increasing refining capacity worldwide, stringent regulations for cleaner fuels, and the need to enhance operational efficiency, product purity, and equipment lifespan through effective water and impurity removal.

"Asia Pacific is estimated to be the second-largest refinery and petrochemical filtration market."

Asia Pacific is expected to be the second-largest refinery and petrochemical filtration market between 2025 and 2030. The downstream sector is growing in the region due to the increasing demand for petrochemical products. Moreover, countries in this region have strategic locations for refineries, which enable them to access crude oil supplies from the Middle East and other regions. Additionally, governments of countries in the region have implemented policies and incentives to attract foreign investments in the downstream sector. These are the key factors fostering the growth of the refinery and petrochemical filtration market in Asia Pacific.

Breakdown of Primaries:

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information, as well as to assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 45%, Tier 2 - 30%, and Tier 3 - 25%

By Designation: C-Level - 35%, Director Levels - 25%, and Others - 40%

By Region: Asia Pacific - 33%, North America - 27%, Europe - 20%, the Middle East & Africa - 12%, and South America - 8%

Notes: Others include product engineers, product specialists, and engineering leads.

The tiers of the companies are defined on the basis of their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: From USD 500 million to USD 1 billion, and Tier 3: < USD 500 million

The refinery and petrochemical filtration market is dominated by a few major players that have a wide geographical presence. The leading players in the refinery and petrochemical filtration market are 3M (US), Pall Corporation (US), Parker Hannifin Corporation (US), Eaton (Ireland), Pentair (US), and others.

Research Coverage:

The report defines, describes, and forecasts the global refinery and petrochemical filtration market by filter type, application, end user, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report provides a comprehensive review of the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates, in terms of value, and future trends in the refinery and petrochemical filtration market.

Key Benefits of Buying the Report

Analysis of key drivers (Implementation of government mandates and policies for environmental protection, Increasing expenditure on refinery and petrochemical infrastructure development), restraints (Availability of low-cost and inferior-quality filtration products, Increasing focus on use of renewable energy), opportunities (Continuous shale development activities to enhance shale refining potential, Expanding transportation sector), and challenges (Supply chain constraints, Frequent replacement and disposal of filters) influencing the growth of the refinery and petrochemical filtration market

Product Development/ Innovation: Trends such as innovative filter media materials, designs, and processes have led to more efficient, reliable, compact, and longer-lasting filters. The focus on sustainability and reducing carbon footprints has also led to the expectation that filter media will contribute to lower energy consumption.

Market Development: Eaton expanded its offline filter units portfolio by introducing a compact, portable hydraulic filtration solution ideal for the oil & gas and power generation sectors, especially refinery equipment. This mobile unit offers high-efficiency hydraulic fluid filtration in hard-to-reach locations, enhancing system reliability and equipment longevity. Its portability and robust design make it perfectly suited for demanding industrial environments, supporting continuous operation and reducing maintenance downtime in critical refinery and power generation applications.

Market Diversification: Eaton launched SENTINEL MAXPO and DURAGAF MAXPOXL specialty filter bags designed for oil, chemical, and petrochemical filtration. These polypropylene needle felt bags feature a fully-welded construction with an additional internal meltblown polypropylene core that enhances dirt-holding capacity and oil absorption. The DURAGAF MAXPOXL range offers a two to five times longer lifespan than standard bags, reducing operational costs. Both ranges are available with nominal retention rates from 1 to 200 µm, optimizing filtration efficiency and durability in industrial applications.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like 3M (US), Pall Corporation (US), Parker Hannifin Corporation (US), Eaton (Ireland), and Pentair (US), among others, in the refinery and petrochemical filtration market has been provided.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 INCLUSIONS AND EXCLUSIONS

1.2.1.1 Refinery and petrochemical filtration market, by filter type

1.2.1.2 Refinery and petrochemical filtration market, by application

1.2.1.3 Refinery and petrochemical filtration market, by end user

1.3 MARKET SCOPE

1.3.1 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

2.2.1 SECONDARY DATA

2.2.1.1 Key data from secondary sources

2.2.2 PRIMARY DATA

2.2.2.1 Key data from primary sources

2.2.2.2 Breakdown of primaries

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.3.3 DEMAND-SIDE ANALYSIS

2.3.3.1 Regional analysis

2.3.3.2 Country-level analysis

2.3.3.3 Demand-side assumptions

2.3.3.4 Demand-side calculations

2.3.4 SUPPLY-SIDE ANALYSIS

2.3.4.1 Supply-side calculations

2.3.4.2 Supply-side assumptions

2.3.5 MARKET GROWTH FORECAST

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN REFINERY AND PETROCHEMICAL FILTRATION MARKET

4.2 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY REGION

4.3 NORTH AMERICAN REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY APPLICATION AND COUNTRY

4.4 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY FILTER TYPE

4.5 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY APPLICATION

4.6 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY END USER

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Implementation of government mandates and policies for environmental protection

5.2.1.2 Increasing expenditure on refinery and petrochemical infrastructure development

5.2.2 RESTRAINTS

5.2.2.1 Availability of low-cost and inferior-quality filtration products

5.2.2.2 Increasing focus on use of renewable energy

5.2.3 OPPORTUNITIES

5.2.3.1 Rising shale development activities to enhance shale refining potential

5.2.3.2 Expanding transportation sector

5.2.4 CHALLENGES

5.2.4.1 Supply chain constraints

5.2.4.2 Frequent replacement and disposal of filters

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.3.1 REVENUE SHIFTS AND NEW REVENUE POCKETS FOR REFINERY AND PETROCHEMICAL FILTRATION SYSTEM MANUFACTURERS

5.4 ECOSYSTEM ANALYSIS

5.5 VALUE CHAIN ANALYSIS

5.5.1 RAW MATERIAL PROVIDERS/SUPPLIERS

5.5.2 REFINERY AND PETROCHEMICAL FILTRATION SYSTEM MANUFACTURERS

5.5.3 DISTRIBUTORS AND END USERS

5.5.4 POST-SALES SERVICE PROVIDERS

5.6 PRICING ANALYSIS

5.7 REPLACEMENT RATE

5.8 TECHNOLOGY ANALYSIS

5.8.1 NANOFIBER FILTRATION MEDIA AND MEMBRANE FILTERS

5.9 TARIFF AND REGULATORY LANDSCAPE

5.9.1 TARIFFS RELATED TO REFINERY AND PETROCHEMICAL FILTRATION UNITS

5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.9.3 CODES AND REGULATIONS RELATED TO REFINERY AND PETROCHEMICAL FILTRATION

5.10 PATENT ANALYSIS

5.11 TRADE ANALYSIS

5.11.1 EXPORT SCENARIO

5.11.2 IMPORT SCENARIO

5.12 KEY CONFERENCES AND EVENTS, 2025-2026

5.13 CASE STUDY ANALYSIS

5.13.1 JONELL SYSTEMS REDUCED COALESCING COSTS IN EUROPEAN REFINERY

5.13.2 JONELL SYSTEMS' REFINERY PRE-FILTRATION SOLUTION SAVED USD 2 MILLION FOR US REFINERY

5.14 PORTER'S FIVE FORCES ANALYSIS

5.14.1 THREAT OF SUBSTITUTES

5.14.2 BARGAINING POWER OF SUPPLIERS

5.14.3 BARGAINING POWER OF BUYERS

5.14.4 THREAT OF NEW ENTRANTS

5.14.5 INTENSITY OF COMPETITIVE RIVALRY

5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2 BUYING CRITERIA

5.16 IMPACT OF GEN AI/AI ON REFINERY AND PETROCHEMICAL FILTRATION MARKET

5.16.1 ADOPTION OF GEN AI/AI IN REFINERY AND PETROCHEMICAL FILTRATION MARKET

5.16.2 IMPACT OF GEN AI/AI, BY END USER

5.16.3 IMPACT OF GEN AI/AI ON REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY REGION

5.17 GLOBAL MACROECONOMIC OUTLOOK

5.17.1 INTRODUCTION

5.17.2 GDP TRENDS AND FORECAST

5.17.3 IMPACT OF INFLATION ON REFINERY AND PETROCHEMICAL FILTRATION MARKET

5.18 IMPACT OF 2025 US TARIFF - OVERVIEW

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 IMPACT ON REGIONS

5.18.3.1 North America

5.18.3.2 Europe

5.18.3.3 Asia Pacific

5.18.3.4 South america

5.18.3.5 Middle East & Africa

6 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY FILTER TYPE

6.1 INTRODUCTION

6.2 COALESCER FILTER

6.2.1 EFFECTIVENESS AT SEPARATING LIQUIDS FROM LIQUIDS AND GASES TO DRIVE MARKET

6.2.1.1 Liquid-liquid coalescer

6.2.1.1.1 Offers cost-effective solution for separating liquids from liquids

6.2.1.2 Liquid-gas coalescer

6.2.1.2.1 Offer efficient solution to enhance quality of end products

6.3 CARTRIDGE FILTER

6.3.1 OFFERS HIGH VERSATILITY AND REQUIRES LESS MAINTENANCE

6.3.1.1 Pleated cartridge filter

6.3.1.1.1 Offers good filtration efficiency due to large surface area

6.3.1.2 Depth cartridge filter

6.3.1.2.1 Long service life and effectiveness against different contaminants to drive demand

6.3.1.3 High flow cartridge filter

6.3.1.3.1 Demand in high-flow processes to drive segmental growth

6.4 ELECTROSTATIC PRECIPITATOR

6.4.1 HIGH EFFICIENCY IN REMOVING PARTICULATE MATTER AND POLLUTANTS FROM EXHAUST GASES TO FUEL DEMAND

6.5 FILTER PRESS

6.5.1 INCREASING USE IN DEWATERING, CLARIFICATION, AND SLUDGE HANDLING APPLICATIONS TO SUPPORT MARKET GROWTH

6.6 BAG FILTER

6.6.1 EASE OF INSTALLATION AND MAINTENANCE, HIGH DIRT-HOLDING CAPACITY, AND LONG SERVICE LIFE TO DRIVE DEMAND

6.7 OTHER FILTER TYPES

7 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 LIQUID-LIQUID SEPARATION

7.2.1 WIDE ADOPTION IN REMOVAL OF WATER FROM FUEL TO DRIVE DEMAND

7.3 LIQUID-GAS SEPARATION

7.3.1 NEED FOR HYDROGEN RECYCLE GAS COMPRESSOR PROTECTION AND OTHER PROCESSES TO FUEL DEMAND

7.4 OTHER APPLICATIONS

8 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY END USER

8.1 INTRODUCTION

8.2 REFINERIES

8.2.1 RISING INVESTMENTS IN REFINERIES TO DRIVE MARKET GROWTH

8.3 PETROCHEMICAL INDUSTRY

8.3.1 INVESTMENTS IN EXPANSION OF PETROCHEMICAL SECTOR TO DRIVE DEMAND

9 REFINERY AND PETROCHEMICAL FILTRATION MARKET, BY REGION

9.1 INTRODUCTION

9.2 ASIA PACIFIC

9.2.1 BY FILTER TYPE

9.2.2 BY APPLICATION

9.2.3 BY END USER

9.2.4 BY COUNTRY

9.2.4.1 China

9.2.4.1.1 Rising investments in refinery and petrochemical infrastructure development to drive market

9.2.4.2 India

9.2.4.2.1 Increasing investments in refineries and petrochemical plants to support market growth

9.2.4.3 Japan

9.2.4.3.1 Favorable government policies to support market growth

9.2.4.4 Australia

9.2.4.4.1 Government-led initiatives to enhance fuel quality to drive demand

9.2.4.5 South Korea

9.2.4.5.1 Capacity expansion and major foreign investments accelerating market growth

9.2.4.6 Rest of Asia Pacific

9.3 NORTH AMERICA

9.3.1 BY FILTER TYPE

9.3.2 BY APPLICATION

9.3.3 BY END USER

9.3.4 BY COUNTRY

9.3.4.1 US

9.3.4.1.1 Government policies and funding for development of downstream oil & gas industry to drive demand

9.3.4.2 Canada

9.3.4.2.1 Environmental initiatives to reduce greenhouse gas emissions to support market growth

9.3.4.3 Mexico

9.3.4.3.1 Increasing investments in downstream infrastructure to fuel market

9.4 EUROPE

9.4.1 BY FILTER TYPE

9.4.2 BY APPLICATION

9.4.3 BY END USER

9.4.4 BY COUNTRY

9.4.4.1 Russia

9.4.4.1.1 High crude production to boost downstream investment

9.4.4.2 Germany

9.4.4.2.1 High energy requirement to fuel market growth

9.4.4.3 UK

9.4.4.3.1 Favorable government policies related to industrial waste management to support market growth

9.4.4.4 France

9.4.4.4.1 Technological advancements in refineries to increase demand

9.4.4.5 Italy

9.4.4.5.1 High refining potential and presence of stringent environmental regulations to fuel market

9.4.4.6 Rest of Europe

9.5 MIDDLE EAST & AFRICA

9.5.1 BY FILTER TYPE

9.5.2 BY APPLICATION

9.5.3 BY END USER

9.5.4 BY COUNTRY

9.5.4.1 Saudi Arabia

9.5.4.1.1 Rising infrastructure development investments to drive market growth

9.5.4.2 UAE

9.5.4.2.1 Favorable government policies and partnerships with international companies to support market growth

9.5.4.3 South Africa

9.5.4.3.1 Government initiatives to support petrochemical industry to drive market

9.5.4.4 Rest of Middle East & Africa

9.6 SOUTH AMERICA

9.6.1 BY FILTER TYPE

9.6.2 BY APPLICATION

9.6.3 BY END USER

9.6.4 BY COUNTRY

9.6.4.1 Brazil

9.6.4.1.1 Rising investments in infrastructure development in refineries and petrochemical industry to drive demand

9.6.4.2 Argentina

9.6.4.2.1 Increase in new infrastructure development investments to fuel market growth

9.6.4.3 Rest of South America

10 COMPETITIVE LANDSCAPE

10.1 STRATEGIES ADOPTED BY KEY PLAYERS

10.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN, JANUARY 2020-JULY 2025

10.3 MARKET SHARE ANALYSIS OF TOP FIVE PLAYERS

10.4 REVENUE ANALYSIS

10.5 COMPANY VALUATION AND FINANCIAL METRICS

10.6 BRAND/PRODUCT COMPARISON

10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.7.1 STARS

10.7.2 PERVASIVE PLAYERS

10.7.3 EMERGING LEADERS

10.7.4 PARTICIPANTS

10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.7.5.1 Company footprint

10.7.5.2 Region footprint

10.7.5.3 Filter type footprint

10.7.5.4 End user footprint

10.7.5.5 Application footprint

10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMALL AND MEDIUM-SIZED ENTERPRISES (SMES), 2024