HVDC 송전 시장 : 프로젝트 유형별, 용도별, 컴포넌트별, 기술별, 지역별 예측(-2030년)

HVDC Transmission Market by LCC, VSC, CCC, Converter Stations, Transmission Cables, Point-to-Point Transmission, Back-to-Back Stations, Multi Terminal Systems, Bulk Power Transmission and Interconnecting Grids - Global Forecast to 2030

상품코드:1804849

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 265 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

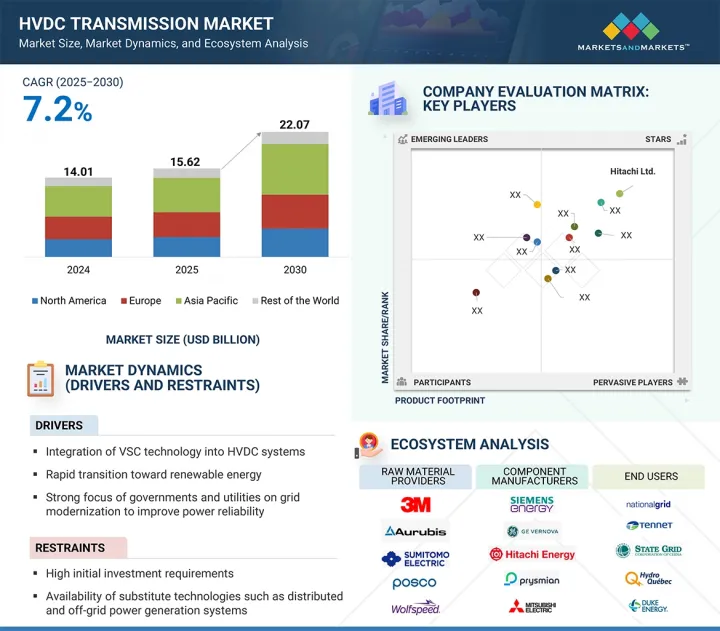

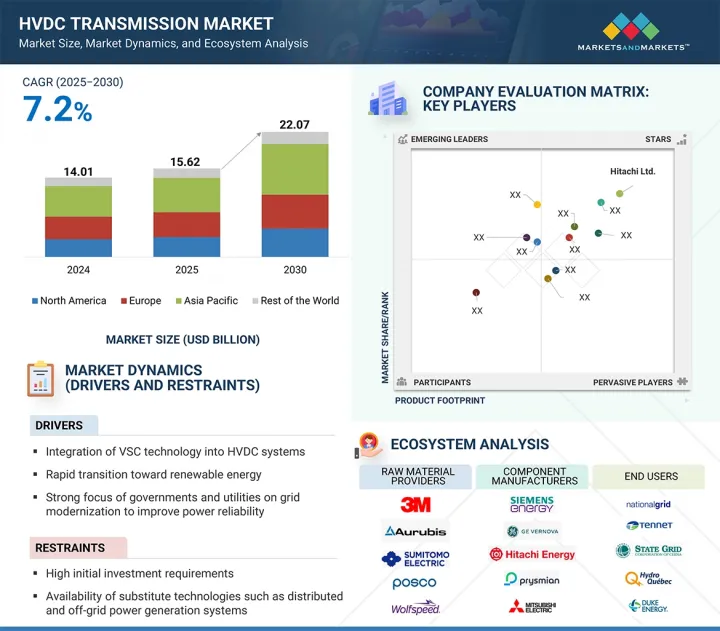

세계의 HVDC 송전 시장 규모는 2025년 156억 2,000만 달러에서 2030년에는 220억 7,000만 달러에 달할 것으로 추정되며, 예측 기간 중 CAGR 7.2%로 성장할 전망입니다.

HVDC 송전 시장은 VSC(전압원 변환기) 기술의 통합, 재생에너지로의 급속한 전환, 전력 신뢰성 향상을 위한 전력망 현대화에 대한 정부 및 전력사의 강력한 관심에 힘입어 상당한 성장을 경험하고 있습니다. 또한 HVDC 송전을 촉진하는 정부 주도 이니셔티브가 시장 채택을 더욱 가속화하고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문별

프로젝트 유형별, 용도별, 컴포넌트별, 기술별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

그러나 시장은 높은 초기 투자 요구 사항과 분산형 및 독립형 발전 시스템과 같은 대체 기술의 가용성으로 인해 어려움을 겪고 있습니다. 또한 HVDC 프로젝트의 복잡한 수명 주기는 실행을 지연시키고 비용을 증가시켜 전체 시장 확장을 다소 제한할 수 있습니다.

전압원 변환기(VSC) 기술은 예측 기간 동안 HVDC 송전 시장에서 가장 빠르게 성장할 것으로 전망됩니다. VSC는 기존 라인 정류 변환기(LCC) 시스템 대비 공간 효율성, 모듈식 설계, 블랙 스타트 기능, 무효 전력 지원 등 주요 장점을 제공합니다. 이러한 특징으로 인해 VSC 시스템은 해상 풍력 발전단지, 태양광 발전소, 분산형 에너지 시스템과 같은 재생에너지 원천을 전력망에 통합하는 데 특히 적합합니다. 또한 VSC 기술은 원격 및 섬 기반 에너지 공급에 필수적인 취약하거나 수동적인 전력망과의 연결을 가능하게 합니다. 국가들이 재생에너지 설비를 확대하고 분산형 발전으로 전환함에 따라 유연하고 공간 효율적인 송전 솔루션에 대한 수요가 급증하고 있습니다. VSC 기반 HVDC 시스템은 지하 및 해저 케이블 송전도 가능하게 하여 도시 중심부와 환경 민감 지역에 이상적입니다. 또한 모듈형 다중 레벨 변환기(MMC)의 기술 발전은 VSC 시스템의 확장성, 신뢰성 및 비용 효율성을 더욱 향상시키고 있습니다. 유럽, 아시아태평양 및 북미 지역의 정부들은 새로운 전력망 현대화 프로젝트와 국경 간 상호 연결에 VSC를 점점 더 선호하고 있습니다. 에너지 전환에 대한 강조가 커짐에 따라 VSC는 차세대 HVDC 인프라에서 중추적인 역할을 수행하며 전 세계적으로 신속한 채택을 주도할 준비가 되어 있습니다.

예측 기간 동안 HVDC 송전 컴포넌트 시장의 변환소 부문 내에서 회로 차단기가 가장 빠른 성장을 보일 것으로 전망됩니다. HVDC 시스템에서 회로 차단기는 고장 전류를 차단하고 결함 구간을 격리함으로써 장비를 보호하는 핵심 역할을 수행하여 시스템 안정성과 신뢰성을 보장합니다. 해상 풍력 및 대규모 태양광과 같은 재생 에너지 원의 통합으로 인한 신뢰성 있고 유연한 전력 전송에 대한 수요 증가로, 첨단 HVDC 보호 솔루션에 대한 필요성이 크게 증가했습니다.

하이브리드 HVDC 회로 차단기 개발을 포함한 최근 기술 발전은 교류 시스템에 비해 전통적으로 더 복잡한 작업인 직류 차단 문제를 해결했습니다. 이러한 혁신은 더 빠른 고장 제거와 가동 중단 시간 최소화를 가능하게 하여 장거리 대용량 HVDC 프로젝트 확장을 지원합니다. 또한 대륙간 및 국경 간 전력 연계에 대한 투자 증가와 노후화된 전력망 인프라 현대화가 회로 차단기 채택을 촉진하고 있습니다. 전력사들이 운영 안전성과 시스템 효율성에 집중함에 따라 차단기 부문은 다른 변환소 컴포넌트보다 높은 성장률을 보이며 강력한 모멘텀을 유지할 것으로 예상됩니다.

아시아태평양 지역은 급속한 산업화, 증가하는 에너지 수요, 재생에너지 통합을 위한 대규모 투자에 힘입어 예측 기간 동안 HVDC 송전 시장에서 가장 빠른 성장을 기록할 것으로 예상됩니다. 중국과 인도 같은 국가들은 전력망 안정성 문제 해결, 장거리 전력 전송 지원, 원격 재생에너지 발전지와 소비 허브 연결을 위해 HVDC 시스템 구축을 주도하고 있습니다. 특히 중국은 수천 킬로미터에 걸쳐 수 기가와트의 전력을 수송하는 여러 국가 간 프로젝트를 통해 초고압(UHV) 직류 송전 분야의 글로벌 선구자로 부상했습니다. 인도 역시 그린 에너지 회랑 및 지역 간 전력 이동 계획을 통해 HVDC 인프라를 확장하고 있습니다. 베트남, 인도네시아 등 동남아시아 국가들은 원격 섬 및 농촌 지역의 전력망 안정성 강화와 증가하는 에너지 수요 충족을 위해 점차 HVDC 도입을 모색 중입니다. 정부 주도 계획, 유리한 정책 프레임워크, 지역 업체들의 HVDC 부품 제조 참여가 도입을 더욱 가속화하고 있습니다. 또한 증가하는 도시화와 전기화 노력, 국경 간 연계 프로젝트(예 : 중국-라오스, 인도-방글라데시)가 결합되어 아시아태평양 지역을 가장 빠르게 성장하는 시장으로 자리매김하고 있습니다. 이 지역의 지속 가능한 발전과 에너지 안보에 대한 집중은 HVDC를 미래 전력 전송 환경의 핵심 촉진제로 만들고 있습니다.

본 보고서에서는 세계의 HVDC 송전 시장에 대해 조사했으며, 프로젝트 유형별, 용도별, 컴포넌트별, 기술별, 지역별 동향, 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

공급망 분석

에코시스템 매핑

투자 및 자금조달 시나리오

기술 분석

가격 분석

특허 분석

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

사례 연구

무역 분석

관세 및 규제 상황

고객사업에 영향을 주는 동향 및 혼란

주된 회의와 이벤트(2025-2026년)

AI/생성형 HVDC 송전 시장에 대한 영향

HVDC 송전 시장의 미국 관세 영향(2025년)

제6장 HVDC 송전에 있어서의 전력 정격

소개

500MW 미만

501-999MW

1,000-2,000MW

2,000MW 초과

제7장 HVDC 송전 시장(프로젝트 유형별)

소개

지점간 송전

BTB

멀티터미널 시스템

제8장 HVDC 송전 시장(용도별)

소개

대용량 전력 송전

상호 연결 그리드

도시 지역 전력 공급

제9장 HVDC 송전 시장(컴포넌트별)

소개

변환소

송전 케이블

기타

제10장 HVDC 송전 시장(기술별)

소개

라인 정류 변환기(LCC)

전압원 변환기(VSC)

커패시터 정류 컨버터(CCC)

제11장 HVDC 송전 시장(지역별)

소개

북미

북미 : 거시경제 전망

미국

캐나다

멕시코

유럽

유럽: 거시경제 전망

영국

독일

프랑스

이탈리아

스페인

폴란드

북유럽

기타

아시아태평양

아시아태평양 : 거시경제 전망

중국

일본

한국

인도

호주

인도네시아

말레이시아

태국

베트남

기타

기타 지역

기타 지역 : 거시 경제 전망

중동

아프리카

남미

제12장 경쟁 구도

소개

주요 참가 기업이 채택하는 전략 및 강점(2020-2025년)

시장 점유율 분석(2024년)

수익 분석(2020-2024년)

기업평가와 재무지표

브랜드 및 제품 비교

기업평가 매트릭스 : 주요 진입기업(2024년)

기업평가 매트릭스 : 스타스업 및 중소기업(2024년)

경쟁 시나리오

제13장 기업 프로파일

소개

주요 진출기업

HITACHI, LTD.

SIEMENS ENERGY

MITSUBISHI ELECTRIC CORPORATION

GE VERNOVA

PRYSMIAN GROUP

TOSHIBA CORPORATION

NKT A/S

NEXANS

LS ELECTRIC CO., LTD.

NR ELECTRIC CO., LTD.

기타 기업

SUMITOMO ELECTRIC INDUSTRIES, LTD.

ZAPOROZHTRANSFORMATOR

TRENCH GROUP

TAIHAN CABLE & SOLUTION CO., LTD.

AMERICAN SEMICONDUCTOR, INC.

ZTT

TBEA CO., LTD.

EFACEC

SIEYUAN ELECTRIC CO., LTD.

XJ ELECTRIC CO., LTD.

BTW

CG POWER & INDUSTRIAL SOLUTIONS LTD.

SGB SMIT

C-EPRI ELECTRIC POWER ENGINEERING CO., LTD.

HYOSUNG HEAVY INDUSTRIES

제14장 부록

HBR

영문 목차

영문목차

The global HVDC transmission market is estimated to be valued at USD 22.07 billion by 2030, up from USD 15.62 billion in 2025, at a CAGR of 7.2% during the forecast period. The HVDC transmission market is experiencing significant growth driven by the integration of VSC (voltage source converter) technology, rapid transition toward renewable energy, and strong government and utility focus on modernizing grids to improve power reliability. Additionally, government-led initiatives promoting HVDC transmission are further accelerating market adoption.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Technology, Component, Project Type, Application, and Region

Regions covered

North America, Europe, APAC, RoW

However, the market faces challenges due to high initial investment requirements and the availability of substitute technologies such as distributed and off-grid power generation systems. Moreover, the complex lifecycles of HVDC projects can delay implementation and increase costs, slightly restraining overall market expansion.

"VSC technology is likely to register the fastest growth in the technology segment during the forecast period."

Voltage source converter (VSC) technology is expected to grow fastest in the HVDC transmission market during the forecast period. VSC offers key advantages over traditional Line Commutated Converter (LCC) systems, such as a smaller footprint, modular design, black start capability, and reactive power support. These features make VSC systems particularly suitable for integrating renewable energy sources like offshore wind farms, solar power plants, and distributed energy systems into the grid. Additionally, VSC technology allows for connection to weak or passive grids, which is essential for remote and island-based energy deployments. As countries expand their renewable capacity and move toward decentralized power generation, the demand for flexible, space-efficient transmission solutions is surging. VSC-based HVDC systems also enable underground and subsea cable transmission, making them ideal for urban centers and environmentally sensitive zones. Moreover, technological advancements in modular multilevel converters (MMC) are further enhancing the scalability, reliability, and cost-effectiveness of VSC systems. Governments across Europe, Asia Pacific, and North America increasingly favor VSC for new grid modernization projects and cross-border interconnections. With growing emphasis on energy transition, VSC is poised to play a pivotal role in the next generation of HVDC infrastructure, driving its rapid adoption globally.

Circuit breakers are expected to register the fastest growth rate in the converter station segment during the forecast period.

Circuit breakers are projected to witness the fastest growth within the converter station segment of the HVDC transmission component market during the forecast period. In HVDC systems, circuit breakers play a critical role in protecting equipment by interrupting fault currents and isolating faulty sections, thereby ensuring system stability and reliability. The rising demand for reliable and flexible power transmission, driven by the integration of renewable energy sources such as offshore wind and large scale solar, has significantly increased the need for advanced HVDC protection solutions.

Recent technological advancements, including the development of hybrid HVDC circuit breakers, have addressed the challenges of interrupting direct current which is traditionally a more complex task compared to AC systems. These innovations enable faster fault clearance and minimize downtime, supporting the expansion of long distance high capacity HVDC projects. Furthermore, growing investments in intercontinental and cross border power links, as well as modernization of aging grid infrastructure, are boosting circuit breaker adoption. As utilities focus on operational safety and system efficiency, the circuit breaker segment is expected to maintain strong momentum, outpacing other converter station components in growth rate.

"Asia Pacific is projected to expand at the fastest growth rate during the forecast period."

Asia Pacific is anticipated to register the fastest growth in the HVDC transmission market during the forecast period, driven by rapid industrialization, growing energy demand, and large-scale investments in renewable energy integration. Countries like China and India are leading the deployment of HVDC systems to address grid stability challenges, support long-distance electricity transmission, and connect remote renewable energy generation sites with consumption hubs. China, in particular, has become a global pioneer in ultra-high-voltage (UHV) DC transmission, with several cross-country projects that span thousands of kilometers and transport gigawatts of power. India also expands its HVDC infrastructure through green energy corridors and inter-regional power transfer initiatives. Southeast Asian nations such as Vietnam and Indonesia are gradually exploring HVDC to enhance grid reliability and meet rising energy needs in remote islands and rural areas. Government-led initiatives, favorable policy frameworks, and the involvement of regional players in HVDC component manufacturing are further accelerating adoption. Moreover, rising urbanization and electrification efforts, coupled with cross-border interconnection projects (e.g., China-Laos, India-Bangladesh), position the Asia Pacific as the fastest-growing market. The region's focus on sustainable development and energy security makes HVDC a key enabler for its future power transmission landscape.

The break-up of the profile of primary participants in the HVDC transmission market-

By Company Type: Tier 1 - 50%, Tier 2 - 30%, Tier 3 - 20%

By Designation Type: C Level - 35%, Director Level - 30%, Others - 35%

By Region Type: Asia Pacific - 40%, Europe - 25%, North America - 20%, Rest of the World - 15%

Note: Other designations include sales, marketing, and product managers.

The three tiers of the companies are based on their total revenues as of 2024: Tier 1: >USD 1 billion, Tier 2: USD 500 million-1 billion, and Tier 3: USD 500 million

The major players in the HVDC transmission market with a significant global presence include Hitachi, Ltd. (Japan), Siemens Energy (Germany), Mitsubishi Electric Corporation (Japan), GE Vernova (US), Prysmian Group (Italy), and others.

Research Coverage

The report segments the HVDC transmission market and forecasts its size by technology, component, project type, application, and region. It also provides a comprehensive review of drivers, restraints, opportunities, and challenges influencing market growth. The report covers qualitative aspects in addition to quantitative aspects of the market.

Reasons to buy the report:

The report will help the market leaders/new entrants in this market with information on the closest approximate revenues for the overall HVDC transmission market and related segments. This report will help stakeholders understand the competitive landscape and gain more insights to strengthen their position in the market and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

Analysis of key drivers (integration of VSC technology into HVDC systems, rapid transition toward renewable energy, strong focus of governments and utilities on grid modernization to improve power reliability, and government-led policies and initiatives promoting HVDC transmission technology), restraints (high initial investment requirements, availability of substitute technologies such as distributed and off-grid power generation systems, and complex project lifecycles), opportunities (constant advances in power electronics and adoption of digital and automation technologies, electrification of transportation sector, growing demand for integrated networks across long distances, and energy transition strategies in oil-rich economies), and challenges (interoperability issues due to lack of standardization, stringent regulatory landscape and complexities associated with obtaining permit for HVDC projects)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the HVDC transmission market.

Market Development: Comprehensive information about lucrative markets - the report analyses the HVDC transmission market across varied regions.

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the HVDC transmission market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, including include Hitachi, Ltd. (Japan), Siemens Energy (Germany), Mitsubishi Electric Corporation (Japan), GE Vernova (US), and Prysmian Group (Italy).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.1.1 SECONDARY DATA

2.1.1.1 Major secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of key primary interview participants

2.1.2.2 Breakdown of primaries

2.1.2.3 Key data from primary sources

2.1.2.4 Key industry insights

2.1.3 SECONDARY AND PRIMARY RESEARCH

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to estimate market size using bottom-up analysis

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to estimate market size using top-down analysis

2.3 FACTOR ANALYSIS

2.3.1 DEMAND-SIDE ANALYSIS

2.3.2 SUPPLY-SIDE ANALYSIS

2.4 GROWTH FORECAST

2.5 MARKET BREAKDOWN AND DATA TRIANGULATION

2.6 RESEARCH ASSUMPTIONS

2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HVDC TRANSMISSION MARKET

4.2 HVDC TRANSMISSION MARKET, BY COMPONENT

4.3 HVDC TRANSMISSION MARKET, BY TECHNOLOGY

4.4 HVDC TRANSMISSION MARKET, BY PROJECT TYPE

4.5 HVDC TRANSMISSION MARKET, BY APPLICATION

4.6 ASIA PACIFIC: HVDC TRANSMISSION MARKET, BY COMPONENT AND COUNTRY, 2024

4.7 HVDC TRANSMISSION MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Integration of VSC technology into HVDC systems

5.2.1.2 Global shift toward renewable energy sources

5.2.1.3 Importance of grid modernization and reliable energy transmission

5.2.1.4 Government-led policies and initiatives to promote HVDC transmission technology

5.2.2 RESTRAINTS

5.2.2.1 High initial investment

5.2.2.2 Availability of substitute technologies

5.2.2.3 Complex project lifecycles

5.2.3 OPPORTUNITIES

5.2.3.1 Growing adoption of digital and automation technologies

5.2.3.2 Electrification of transportation sector

5.2.3.3 Increasing demand for integrated networks across long distances

5.2.3.4 Strategic shift from traditional fossil fuels to sustainable energy

5.2.4 CHALLENGES

5.2.4.1 Interoperability issues due to lack of standardization

5.2.4.2 Complexities associated with obtaining necessary permits

5.3 SUPPLY CHAIN ANALYSIS

5.4 ECOSYSTEM MAPPING

5.5 INVESTMENT AND FUNDING SCENARIO

5.6 TECHNOLOGY ANALYSIS

5.6.1 KEY TECHNOLOGIES

5.6.1.1 Modular multilevel converters (MMC)

5.6.1.2 Control & protection systems

5.6.2 COMPLEMENTARY TECHNOLOGIES

5.6.2.1 SCADA

5.6.2.2 HVDC grid control software

5.6.3 ADJACENT TECHNOLOGIES

5.6.3.1 Offshore energy hubs and interconnectors

5.6.3.2 Advanced grid planning and simulation tools

5.7 PRICING ANALYSIS

5.7.1 AVERAGE SELLING PRICE TREND OF COMPONENTS, BY KEY PLAYER, 2021-2024

5.7.2 AVERAGE SELLING PRICE TREND OF COMPONENTS, BY REGION, 2021-2024

5.8 PATENT ANALYSIS

5.9 PORTER'S FIVE FORCES ANALYSIS

5.9.1 THREAT OF NEW ENTRANTS

5.9.2 THREAT OF SUBSTITUTES

5.9.3 BARGAINING POWER OF SUPPLIERS

5.9.4 BARGAINING POWER OF BUYERS

5.9.5 INTENSITY OF COMPETITIVE RIVALRY

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 CASE STUDIES

5.11.1 ELECTRIFICATION OF STATOIL TROLL A PLATFORM WITH ABB HVDC LIGHT TECHNOLOGY DELIVERS LOWER EMISSIONS AND IMPROVED EFFICIENCY

5.11.2 HITACHI ENERGY HVDC LIGHT INTEGRATION STRENGTHENS NORDIC GRID RESILIENCE AND ENABLES EFFICIENT CROSS-BORDER RENEWABLE ENERGY EXCHANGE

5.11.3 SCOTTISH HYDRO ELECTRIC TRANSMISSION AND CAITHNESS-MORAY HVDC COLLABORATED TO STRENGTHEN SCOTLAND'S POWER NETWORK AND ENABLE RELIABLE RENEWABLE ENERGY INTEGRATION

5.11.4 MITSUBISHI ELECTRIC CORPORATION ASISTS SWANSEA NORTH SUBSTATION UPGRADE TO HIGHER VOLTAGE SYSTEM

5.11.5 HITACHI ENERGY EMPOWERS CROSS-BORDER ENERGY FLOW WITH EAST WEST HVDC INTERCONNECTOR

5.12 TRADE ANALYSIS

5.12.1 IMPORT DATA

5.12.2 EXPORT DATA

5.13 TARIFF AND REGULATORY LANDSCAPE

5.13.1 TARIFF ANALYSIS

5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13.3 STANDARDS

5.13.3.1 Europe

5.13.3.2 Asia Pacific

5.13.3.3 North America

5.13.3.4 RoW

5.13.4 REGULATIONS

5.13.4.1 North America

5.13.4.2 Europe

5.13.4.3 Asia Pacific

5.13.4.4 RoW

5.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.15 KEY CONFERENCES AND EVENTS, 2025-2026

5.16 IMPACT OF AI/GEN AI ON HVDC TRANSMISSION MARKET

5.16.1 INTRODUCTION

5.17 IMPACT OF 2025 US TARIFF - HVDC TRANSMISSION MARKET

5.17.1 INTRODUCTION

5.17.1.1 Key tariff rates

5.17.2 PRICE IMPACT ANALYSIS

5.17.3 IMPACT ON COUNTRY/ REGION

5.17.3.1 US

5.17.3.2 Europe

5.17.3.3 Asia Pacific

5.17.4 IMPACT ON APPLICATIONS

6 POWER RATINGS IN HVDC TRANSMISSION

6.1 INTRODUCTION

6.2 BELOW 500 MW

6.3 501-999 MW

6.4 1,000-2,000 MW

6.5 ABOVE 2,000 MW

7 HVDC TRANSMISSION MARKET, BY PROJECT TYPE

7.1 INTRODUCTION

7.2 POINT-TO-POINT TRANSMISSION

7.2.1 MONOPOLAR TRANSMISSION SYSTEMS

7.2.1.1 Suitability for remote area electrification and early-stage HVDC projects to support market growth

7.2.2 BIPOLAR TRANSMISSION SYSTEMS

7.2.2.1 Rising demand for bulk power transmission from remote renewable sources to fuel market growth

7.3 BACK-TO-BACK STATIONS

7.3.1 GROWING NEED FOR CROSS-BORDER ELECTRICITY TRADE BETWEEN ASYNCHRONOUS NETWORKS TO FOSTER MARKET GROWTH

7.4 MULTI-TERMINAL SYSTEMS

7.4.1 ABILITY TO AGGREGATE LARGE AMOUNTS OF RENEWABLE ENERGIES COST-EFFECTIVELY TO FUEL MARKET GROWTH

8 HVDC TRANSMISSION MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 BULK POWER TRANSMISSION

8.2.1 OVERHEAD

8.2.1.1 Growing emphasis on enhancing inter-regional connectivity to boost demand

8.2.2 UNDERWATER & UNDERGROUND

8.2.2.1 Improved energy security with electricity trading to fuel market growth

8.3 INTERCONNECTING GRIDS

8.3.1 ONGOING ADVANCEMENTS IN VSC TECHNOLOGY TO DRIVE MARKET

8.4 INFEED URBAN AREAS

8.4.1 RISING ELECTRICITY DEMAND FROM DENSELY POPULATED URBAN AREAS TO BOOST DEMAND

9 HVDC TRANSMISSION MARKET, BY COMPONENT

9.1 INTRODUCTION

9.2 CONVERTER STATIONS

9.2.1 VALVES

9.2.1.1 Thyristor valves

9.2.1.1.1 Ongoing advancements to enhance switching speed and efficiency to drive market