Transformer Market by Type, Coooling Type, Power Rating, Phase, Insulation, End User, and Region - Global Forecast to 2030

상품코드:1796191

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 351 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

세계의 변압기 시장 규모는 2025년 646억 4,000만 달러에서 2030년까지 884억 8,000만 달러에 달할 것으로 추정되며, CAGR로 6.5%의 성장이 전망됩니다.

조사 범위

조사 대상연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

금액(100만/10억 달러), 수량(1,000대)

부문

유형, 냉각 유형, 정격 전력, 상, 단열재, 최종사용자

대상 지역

북미, 아시아태평양, 유럽, 남미, 중동 및 아프리카

이러한 성장은 신흥 경제권과 첨단 경제권의 전력 소비 증가, 전력망 인프라 현대화에 대한 대규모 투자, 재생에너지 자원의 빠른 통합의 조합에 의해 촉진되고 있습니다. 각국이 기후 변화 목표 달성과 에너지 접근성 향상을 위해 노력하는 가운데, 고효율의 스마트하고 환경적으로 지속가능한 변압기에 대한 수요가 빠르게 증가하고 있습니다. 또한 도시화, 데이터센터 건설, 교통 및 산업 전기화의 급격한 증가로 인해 신뢰할 수 있는 고급 변압기 기술의 필요성이 더욱 높아졌습니다.

"유형별로는 전력용 변압기가 2024년 변압기 시장에서 가장 큰 점유율을 차지했습니다. "

세계에서 고압 송전망의 확장 및 강화로 인해 전력용 변압기가 유형별 변압기 시장에서 가장 큰 점유율을 차지했습니다. 각국이 대규모 태양광발전소, 풍력발전소, 수력발전소, 화력발전소 등의 발전소에서 도시하센터까지 일괄 송전에 투자하고 있으며, 고전압 장거리 송전에 대응할 수 있는 전력용 변압기 수요가 지속적으로 증가하고 있습니다. 또한 선진국에서는 노후화된 전력망 인프라가, 신흥 경제권에서는 야심찬 전력망 확장 계획이 대대적인 교체 및 신설을 촉진하고 있습니다. 특히 아시아태평양, 유럽, 아프리카 등의 지역에서는 지역 간 및 국경을 초월한 전력 거래로의 전환이 진행되고 있으며, 이에 따라 대형의 효율적인 대용량 변압기에 대한 수요가 더욱 증가하고 있습니다.

"정격 전력별로는 중전력이 예측 기간 중 가장 빠른 성장세를 보일 것으로 보입니다. "

중전력(10.1-100MVA)은 산업시설, 재생에너지 프로젝트, 도시 변전소, 대형 복합상업시설 등 다양한 부문에 걸쳐 다양한 용도로 사용됨에 따라 정격 전력별로 가장 빠르게 성장하는 부문이 될 것으로 예측됩니다. 경제권의 산업화와 인프라 현대화가 진행됨에 따라 송전 시스템과 배전 시스템을 연결하는 중전압 네트워크를 지원하는 중전압 변압기의 보급이 증가하고 있습니다. 태양광발전소 및 풍력발전소(특히 분산형)의 급속한 증가도이 정격 범위의 변압기 수요를 촉진하고 있습니다. 또한 정부가 지원하는 도시 전기화 및 스마트그리드 사업에서 성능, 비용, 확장성의 균형이 가장 잘 맞기 때문에 중전압 변압기에 대한 지지가 높아지고 있습니다.

"북미는 예측 기간 중 변압기 시장에서 두 번째로 빠르게 성장하는 지역이 될 것입니다. "

북미는 전력망 현대화, 노후화된 인프라 교체, 재생에너지원 통합을 위한 대규모 투자로 인해 예측 기간 중 변압기 시장에서 두 번째로 빠르게 성장하는 지역이 될 가능성이 높습니다. 미국과 캐나다는 신뢰성을 높이고 전기자동차(EV) 보급을 지원하며 옥상 태양광, 축전지 등 분산형 에너지 자원에 대응하기 위해 송배전망의 업그레이드를 추진하고 있습니다. 미국의 Infrastructure Investment and Jobs Act, 캐나다의 Clean Electricity Regulations 등 연방정부의 구상으로 디지털 모델, 환경 효율이 높은 모델 등 첨단 변압기 기술의 보급이 가속화되고 있습니다. 또한 이 지역에서는 데이터센터의 설치 면적이 확대되고 교통 및 산업 부문의 전기화가 진행됨에 따라 고성능 및 탄력적인 변압기에 대한 수요가 더욱 증가하고 있습니다.

세계의 변압기 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요한 인사이트

변압기 시장의 기업에 매력적인 기회

변압기 시장 : 지역별

아시아태평양의 변압기 시장 : 유형별, 국가별

변압기 시장 : 유형별

변압기 시장 : 냉각 유형별

변압기 시장 : 정격 전력별

변압기 시장 : 상별

변압기 시장 : 절연별

변압기 시장 : 최종사용자별

제5장 시장 개요

서론

시장 역학

촉진요인

억제요인

기회

과제

고객 비즈니스에 영향을 미치는 동향/혼란

가격결정 분석

변압기의 가격대 : 유형별(2024년)

변압기의 가격대 : 정격 전력별(2024년)

변압기의 평균 판매 가격 동향 : 지역별(2021-2024년)

공급망 분석

에코시스템 분석

기술 분석

주요 기술

인접 기술

보완 기술

특허 분석

무역 분석

수입 시나리오(HS 코드 8504)

수출 시나리오(HS 코드 8504)

2025년 - 주요 컨퍼런스와 이벤트(2026년)

관세와 규제 상황

관세 분석

규제기관, 정부기관, 기타 조직

규제와 규제

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

투자와 자금조달 시나리오

사례 연구 분석

EASYDRY 기술을 이용한 부싱 신뢰성, 안전성, 환경 리스크에 대한 대응

TXPERT HUB에 의한 그리드 레질리언스와 변압기 건전성의 최적화

TVP 기술에 의한 변압기 수명과 그리드 신뢰성의 보호

변압기 시장에 대한 생성형 AI/AI의 영향

변압기 시장에서 생성형 AI/AI의 채택

변압기 시장에 대한 생성형 AI/AI의 영향 : 지역별

변압기 시장의 거시경제적 전망

2025년 미국 관세의 영향 - 개요

서론

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

최종사용자에 대한 영향

제6장 변압기 시장 : 유형별

서론

전력용 변압기

배전용 변압기

계기용 변압기

특수 변압기

제7장 변압기 시장 : 냉각 유형별

서론

유냉

공랭

제8장 변압기 시장 : 정격 전력별

서론

저

중

고

제9장 변압기 시장 : 상별

서론

삼상

단상

제10장 변압기 시장 : 절연별

서론

오일

고체

가스

공기

제11장 변압기 시장 : 최종사용자별

서론

전력 기업

산업

주택·상업 시설

데이터센터

기타 최종사용자

제12장 변압기 시장 : 지역별

서론

아시아태평양

중국

인도

일본

호주

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

이탈리아

영국

프랑스

스페인

기타 유럽

중동 및 아프리카

GCC

남아프리카공화국

기타 중동 및 아프리카

남미

브라질

아르헨티나

기타 남미

제13장 경쟁 구도

개요

주요 참여 기업의 전략/강점(2022-2025년)

시장 점유율 분석(2024년)

매출 분석, 2020년 - 2024년

기업의 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2023년)

경쟁 시나리오

제14장 기업 개요

주요 기업

HITACHI ENERGY LTD.

SIEMENS ENERGY

EATON

GE VERNOVA

TOSHIBA ENERGY SYSTEMS & SOLUTIONS CORPORATION

SCHNEIDER ELECTRIC

ABB

MITSUBISHI ELECTRIC CORPORATION

BHARAT HEAVY ELECTRICALS LIMITED

HD HYUNDAI ELECTRIC CO., LTD.

HUBBELL

CG POWER & INDUSTRIAL SOLUTIONS LTD.

HYOSUNG HEAVY INDUSTRIES

FUJI ELECTRIC CO., LTD.

WEG

LS ELECTRIC CO., LTD.

ARTECHE GROUP

KONCAR D.D.

JSHP TRANSFORMER

TBEA

기타 기업

CHINA XD GROUP

VOLTAMP TRANSFORMER

MEIDENSHA CORPORATION

ORMAZABAL

HENAN HENGYU ELECTRIC GROUP CO., LTD.

제15장 부록

KSA

영문 목차

영문목차

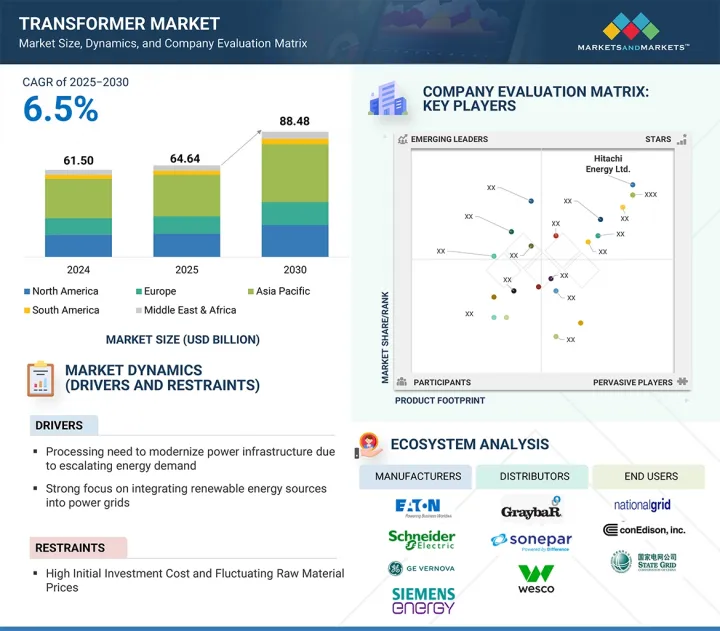

The transformer market is estimated to grow from USD 64.64 billion in 2025 to USD 88.48 billion by 2030, at a CAGR of 6.5%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion), Volume (Thousand Units)

Segments

By Type, By Cooling Type, By Power Rating, By Phase, By Insulation, and By End User

Regions covered

North America, Asia Pacific, Europe, South America, and Middle East & Africa.

This growth is driven by a combination of rising electricity consumption across emerging and developed economies, large-scale investments in grid infrastructure modernization, and the accelerated integration of renewable energy sources. As nations aim to meet climate goals and improve energy access, the demand for high-efficiency, smart, and environmentally sustainable transformers is rapidly expanding. Additionally, the surge in urbanization, data center construction, and electrification of transport and industry further fuels the need for reliable and advanced transformer technologies.

"By type, power transformer held largest share of transformer market in 2024"

Power transformers represented the largest share of the transformer market, by type, primarily due to the global expansion and reinforcement of high-voltage transmission networks. As countries invest in bulk power transmission from generation sources, including large-scale solar, wind, hydro, and thermal plants, to urban load centers, the demand for power transformers capable of handling high voltage and long-distance transmission continues to rise. Moreover, aging grid infrastructure in developed regions and ambitious grid expansion plans in emerging economies drive substantial replacements and new installations. The transition toward inter-regional and cross-border power trade, particularly in regions such as Asia Pacific, Europe, and Africa, further amplifies the need for large, efficient, and high-capacity power transformers, solidifying this segment's dominant market position.

"By power rating, the medium segment to exhibit fastest growth during forecast period"

Medium (10.1-100 MVA) is expected to be the fastest-growing segment, by power rating, driven by its versatile applications across a broad range of sectors, including industrial facilities, renewable energy projects, urban substations, and large commercial complexes. As economies continue to industrialize and modernize their infrastructure, medium power transformers are increasingly being deployed to support medium-voltage networks that bridge transmission and distribution systems. The rapid growth of solar and wind farms-especially in decentralized formats-also fuels demand for transformers in this rating range, as they are ideally suited to manage fluctuating loads while ensuring grid stability. Furthermore, government-backed urban electrification and smart grid initiatives increasingly favor medium-rated transformers due to their optimal balance between performance, cost, and scalability.

"North America to be second fastest-growing region in transformer market during forecast period"

North America is likely to be the second fastest-growing region in the transformer market during the forecast period, driven by substantial investments in grid modernization, aging infrastructure replacement, and the integration of renewable energy sources. The US and Canada are upgrading their transmission and distribution networks to improve reliability, support electric vehicle (EV) expansion, and accommodate distributed energy resources such as rooftop solar and battery storage. Federal initiatives such as the US Infrastructure Investment and Jobs Act and Canada's Clean Electricity Regulations are accelerating the deployment of advanced transformer technologies, including digital and eco-efficient models. Additionally, the region's growing data center footprint and increased electrification across transportation and industry sectors further propel the demand for high-performance and resilient transformers.

Breakdown of Primaries:

In-depth interviews were conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among others, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 65%, Tier 2 - 24%, and Tier 3 - 11%

By Designation: C-level Executives - 25%, Directors - 30%, and Others - 45%

By Region: North America - 25%, Europe - 40%, Asia Pacific - 25%, Middle East & Africa - 5%, and South America - 5%

Note: Other designations include sales managers, marketing managers, product managers, and product engineers.

The tier of the companies is defined based on their total revenue as of 2024. Tier 1: USD 1 billion and above, Tier 2: From USD 500 million to USD 1 billion, and Tier 3: <USD 500 million.

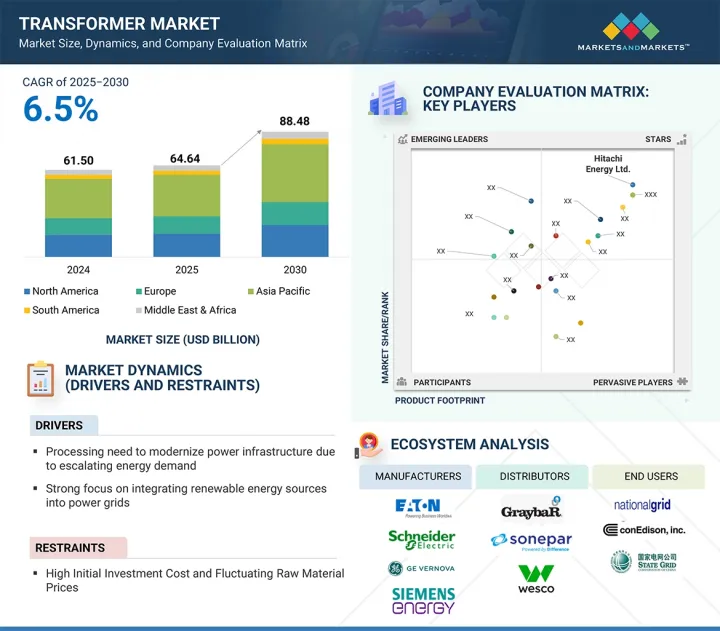

A few major players with a wide regional presence dominate the transformer market. The leading players are Hitachi Energy Ltd. (Switzerland), Siemens Energy (Germany), Eaton (Ireland), GE Vernova (US), and Toshiba Energy Systems & Solutions Corporation (Japan).

Study Coverage:

The report defines, describes, and forecasts the transformer market by type, cooling type, power rating, phase, insulation end user, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market, which include the analysis of the competitive landscape, market dynamics, market estimates in terms of value, and future trends in the transformer market.

Key Benefits of Buying Report

Product Development/Innovation: Key drivers (Need to modernize power infrastructure due to escalating energy demand), restraints (High initial investment cost and fluctuating raw material prices), opportunities (Evolution of smart, digital, and resilient grids), and challenges (Sustainability and safety challenges linked to transformer insulating oils) influence the market.

Market Development: In June 2024, Siemens Energy invested in expanding its grid division, a strategic move to strengthen global energy infrastructure and accelerate the energy transition. This expansion includes building new manufacturing facilities, such as a large power transformer plant in Charlotte, North Carolina, which will help address the critical shortage of transformers in the US and support aging grid infrastructure.

Market Diversification: In February 2025, Eaton invested in a new manufacturing facility in South Carolina for its three-phase transformers, marking the company's third facility in the United States. The image shows the transformers' manufacturing process at the company's facility in Wisconsin.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, Hitachi Energy Ltd. (Switzerland), Siemens Energy (Germany), Eaton (Ireland), GE Vernova (US), and Toshiba Energy Systems & Solutions Corporation (Japan), among others, in the transformer market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

2.2.1 SECONDARY DATA

2.2.1.1 Key data from secondary sources

2.2.1.2 List of major secondary sources

2.2.2 PRIMARY DATA

2.2.2.1 Breakdown of primaries

2.2.2.2 Key data from primary sources

2.2.2.3 Participants in primary interviews

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.3.3 DEMAND-SIDE ANALYSIS

2.3.3.1 Regional analysis

2.3.3.2 Country-level analysis

2.3.3.3 Demand-side assumptions

2.3.3.4 Demand-side calculations

2.3.4 SUPPLY-SIDE ANALYSIS

2.3.4.1 Supply-side assumptions

2.3.4.2 Supply-side calculations

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TRANSFORMER MARKET

4.2 TRANSFORMER MARKET, BY REGION

4.3 TRANSFORMER MARKET IN ASIA PACIFIC, BY TYPE AND COUNTRY

4.4 TRANSFORMER MARKET, BY TYPE

4.5 TRANSFORMER MARKET, BY COOLING TYPE

4.6 TRANSFORMER MARKET, BY POWER RATING

4.7 TRANSFORMER MARKET, BY PHASE

4.8 TRANSFORMER MARKET, BY INSULATION

4.9 TRANSFORMER MARKET, BY END USER

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Pressing need to modernize the power infrastructure due to escalating energy demand

5.2.1.2 Strong focus on integrating renewable energy sources into power grids

5.2.1.3 Urgent need to upgrade aging grid infrastructure

5.2.2 RESTRAINTS

5.2.2.1 High initial investment cost and fluctuating raw material prices

5.2.3 OPPORTUNITIES

5.2.3.1 Evolution of smart, digital, and resilient grids

5.2.3.2 Growing focus of developing countries on electrification

5.2.4 CHALLENGES

5.2.4.1 Sustainability and safety challenges linked to transformer insulating oils

5.2.4.2 Supply chain disruptions and component shortages

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 PRICING RANGE OF TRANSFORMERS, BY TYPE, 2024

5.4.2 PRICING RANGE OF TRANSFORMERS, BY POWER RATING, 2024

5.4.3 AVERAGE SELLING PRICE TREND OF TRANSFORMERS, BY REGION, 2021-2024

5.5 SUPPLY CHAIN ANALYSIS

5.6 ECOSYSTEM ANALYSIS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Solid-state transformers (SSTs)

5.7.1.2 Digital twin technology for transformers

5.7.2 ADJACENT TECHNOLOGIES

5.7.2.1 Adjacent cooling system for transformers

5.7.2.2 Renewable energy integration systems

5.7.3 COMPLEMENTARY TECHNOLOGIES

5.7.3.1 Transformer condition monitoring system

5.7.3.2 Smart transformer substation automation

5.8 PATENT ANALYSIS

5.9 TRADE ANALYSIS

5.9.1 IMPORT SCENARIO (HS CODE 8504)

5.9.2 EXPORT SCENARIO (HS CODE 8504)

5.10 KEY CONFERENCES AND EVENTS, 2025-2026

5.11 TARIFF AND REGULATORY LANDSCAPE

5.11.1 TARIFF ANALYSIS

5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.11.3 CODES AND REGULATIONS

5.12 PORTER'S FIVE FORCES ANALYSIS

5.12.1 THREAT OF SUBSTITUTES

5.12.2 BARGAINING POWER OF SUPPLIERS

5.12.3 BARGAINING POWER OF BUYERS

5.12.4 THREAT OF NEW ENTRANTS

5.12.5 INTENSITY OF COMPETITIVE RIVALRY

5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.13.2 BUYING CRITERIA

5.14 INVESTMENT AND FUNDING SCENARIO

5.15 CASE STUDY ANALYSIS

5.15.1 ADDRESSING RELIABILITY, SAFETY, AND ENVIRONMENTAL RISKS IN BUSHINGS THROUGH EASYDRY TECHNOLOGY

5.15.2 OPTIMIZING GRID RESILIENCE AND TRANSFORMER HEALTH WITH TXPERT HUB

5.15.3 SAFEGUARDING TRANSFORMER LIFESPAN AND GRID RELIABILITY USING TVP TECHNOLOGY

5.16 IMPACT OF GEN AI/AI ON TRANSFORMER MARKET

5.16.1 ADOPTION OF GEN AI/AI IN TRANSFORMER MARKET

5.16.2 IMPACT OF GEN AI/AI ON TRANSFORMER MARKET, BY REGION

5.17 MACROECONOMIC OUTLOOK FOR TRANSFORMER MARKET

5.18 IMPACT OF 2025 US TARIFF - OVERVIEW

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 PRICE IMPACT ANALYSIS

5.18.4 IMPACT ON COUNTRIES/REGIONS

5.18.4.1 US

5.18.4.2 Europe

5.18.4.3 Asia Pacific

5.18.5 IMPACT ON END USERS

6 TRANSFORMER MARKET, BY TYPE

6.1 INTRODUCTION

6.2 POWER TRANSFORMER

6.2.1 GRID MODERNIZATION AND CROSS-BORDER TRANSMISSION PROJECTS TO DRIVE DEMAND

6.3 DISTRIBUTION TRANSFORMER

6.3.1 URBANIZATION AND ELECTRIFICATION PROGRAMS TO ELEVATE ADOPTION

6.4 INSTRUMENT TRANSFORMER

6.4.1 GLOBAL SHIFT TOWARD SMART GRID INFRASTRUCTURE AND DIGITAL SUBSTATIONS TO CREATE OPPORTUNITIES

6.5 SPECIALTY TRANSFORMER

6.5.1 SPECIALIZED INDUSTRIAL AND TRANSPORT APPLICATIONS TO ACCELERATE IMPLEMENTATION

7 TRANSFORMER MARKET, BY COOLING TYPE

7.1 INTRODUCTION

7.2 OIL-COOLED

7.2.1 SUPERIOR THERMAL CONDUCTIVITY AND DURABILITY TO BOOST DEMAND

7.3 AIR-COOLED

7.3.1 ENVIRONMENTAL SAFETY AND LOW MAINTENANCE REQUIREMENTS TO FACILITATE DEMAND

8 TRANSFORMER MARKET, BY POWER RATING

8.1 INTRODUCTION

8.2 LOW

8.2.1 RAPID URBANIZATION AND SMART CITY INITIATIVES TO FACILITATE MARKET GROWTH

8.3 MEDIUM

8.3.1 INDUSTRIAL EXPANSION IN EMERGING ECONOMIES TO FUEL MARKET GROWTH

8.4 HIGH

8.4.1 INCREASING INVESTMENTS IN REINFORCING GRID STABILITY TO SPUR DEMAND

9 TRANSFORMER MARKET, BY PHASE

9.1 INTRODUCTION

9.2 THREE-PHASE

9.2.1 WIDESPREAD USE IN TRANSMISSION NETWORKS AND LARGE COMMERCIAL COMPLEXES TO FUEL SEGMENTAL GROWTH

9.3 SINGLE-PHASE

9.3.1 GOVERNMENT-LED INITIATIVES TO EXPAND ELECTRICITY ACCESS ACROSS REMOTE AND UNDERSERVED REGIONS TO DRIVE MARKET

10 TRANSFORMER MARKET, BY INSULATION

10.1 INTRODUCTION

10.2 OIL

10.2.1 HIGH DIELECTRIC STRENGTH AND SUPERIOR THERMAL CONDUCTIVITY TO SPIKE DEMAND

10.3 SOLID

10.3.1 SIGNIFICANT DEMAND FOR SUSTAINABLE, LOW-EMISSION TECHNOLOGIES IN URBAN INFRASTRUCTURE TO PROPEL MARKET

10.4 GAS

10.4.1 SPACE OPTIMIZATION AND ENVIRONMENTAL SAFETY TO ESCALATE DEMAND

10.5 AIR

10.5.1 SIMPLICITY, FLEXIBILITY, AND COST-EFFECTIVENESS TO ELEVATE ADOPTION

11 TRANSFORMER MARKET, BY END USER

11.1 INTRODUCTION

11.2 POWER UTILITIES

11.2.1 PRESSING NEED TO UPGRADE AGING GRID ASSETS TO ELEVATE DEMAND

11.3 INDUSTRIAL

11.3.1 RISING FOCUS ON DECARBONIZATION AND ENERGY OPTIMIZATION TO FACILITATE ADOPTION

11.4 RESIDENTIAL & COMMERCIAL

11.4.1 RAPID URBANIZATION AND REAL ESTATE DEVELOPMENT TO TRIGGER DEMAND

11.5 DATA CENTERS

11.5.1 PROLIFERATION OF CLOUD COMPUTING TO CREATE GROWTH OPPORTUNITIES

11.6 OTHER END USERS

12 TRANSFORMER MARKET, BY REGION

12.1 INTRODUCTION

12.2 ASIA PACIFIC

12.2.1 CHINA

12.2.1.1 Government's push for smart grid and digital substation deployment to drive demand

12.2.2 INDIA

12.2.2.1 Growing focus on renewable energy expansion to accelerate demand

12.2.3 JAPAN

12.2.3.1 Surging deployment of energy storage systems and electric vehicle charging networks to propel market

12.2.4 AUSTRALIA

12.2.4.1 Significant investments in transmission and distribution infrastructure to support market growth

12.2.5 REST OF ASIA PACIFIC

12.3 NORTH AMERICA

12.3.1 US

12.3.1.1 Digital infrastructure and grid modernization programs to spike demand

12.3.2 CANADA

12.3.2.1 Clean energy and transmission system upgrade initiatives to foster market growth

12.3.3 MEXICO

12.3.3.1 Government focus on improving grid resilience to facilitate adoption

12.4 EUROPE

12.4.1 GERMANY

12.4.1.1 Rising deployment of green hydrogen and digital factories to spur demand

12.4.2 ITALY

12.4.2.1 Growing digital economy to create opportunities

12.4.3 UK

12.4.3.1 Strong focus on deploying SF6-free substations to facilitate market growth

12.4.4 FRANCE

12.4.4.1 Pressing need to enhance transmission and distribution infrastructure to increase demand

12.4.5 SPAIN

12.4.5.1 Solar PV capacity expansion projects to support market growth

12.4.6 REST OF EUROPE

12.5 MIDDLE EAST & AFRICA

12.5.1 GCC

12.5.1.1 Saudi Arabia

12.5.1.1.1 Urban expansion and smart city initiatives to surge demand

12.5.1.2 UAE

12.5.1.2.1 Greater emphasis on expanding clean energy proportion in overall energy mix to boost demand

12.5.1.3 Rest of GCC

12.5.2 SOUTH AFRICA

12.5.2.1 Push to modernize transmission and distribution infrastructure to create growth opportunities

12.5.3 REST OF MIDDLE EAST& AFRICA

12.6 SOUTH AMERICA

12.6.1 BRAZIL

12.6.1.1 Investment in metro rail systems, marine terminals, and public transport electrification to support market growth

12.6.2 ARGENTINA

12.6.2.1 Expansion of high-voltage transmission lines to strengthen market growth

12.6.3 REST OF SOUTH AMERICA

13 COMPETITIVE LANDSCAPE

13.1 OVERVIEW

13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

13.3 MARKET SHARE ANALYSIS, 2024

13.4 REVENUE ANALYSIS, 2020-2024

13.5 COMPANY VALUATION AND FINANCIAL METRICS

13.6 BRAND/PRODUCT COMPARISON

13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.7.1 STARS

13.7.2 EMERGING LEADERS

13.7.3 PERVASIVE PLAYERS

13.7.4 PARTICIPANTS

13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.7.5.1 Company footprint

13.7.5.2 Region footprint

13.7.5.3 Type footprint

13.7.5.4 Cooling type footprint

13.7.5.5 Phase footprint

13.7.5.6 End user footprint

13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023