산업용 제어 변압기 시장 : 위상별, 정격 전력별, 1차 전압별, 주파수별, 최종 용도별, 지역별 예측(-2030년)

Industrial Control Transformer Market by Power Rating (25-500 VA, 501-1,000 VA, 1,001-1,500 VA, above 1,500 VA), Primary Voltage (Up to 120 V, 121-240 V, above 240 V), Frequency (50 Hz, 60 Hz), Phase, End Use, and Region - Global Forecasts to 2030

상품코드:1810323

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 265 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

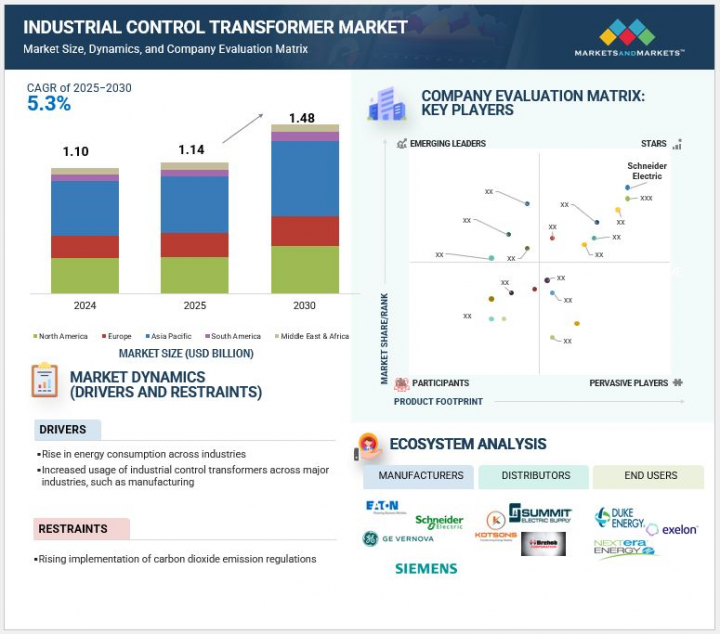

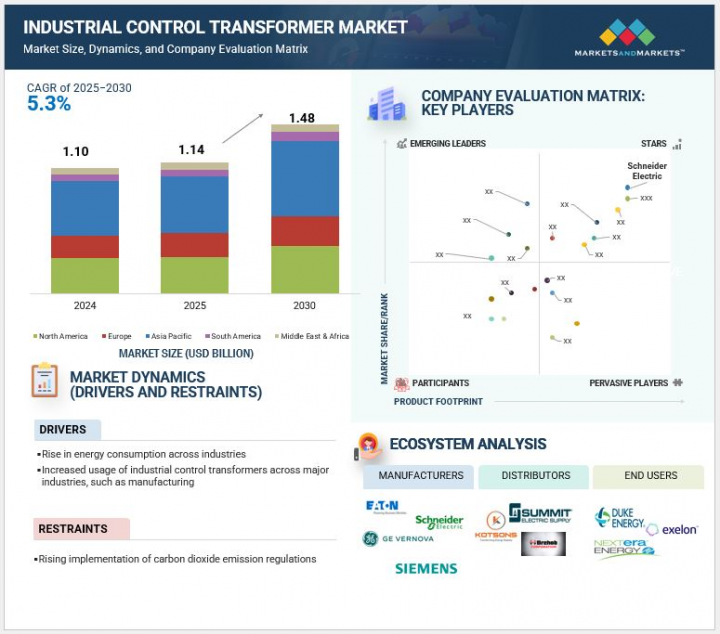

산업용 제어 변압기 시장 규모는 2025년에 11억 4,000만 달러에서 2030년에는 14억 8,000만 달러로 성장할 전망이며, 예측 기간 중 CAGR 5.3%로 성장할 것으로 예측됩니다.

이러한 성장은 산업 분야에서 안정적이고 신뢰할 수 있는 전력 공급에 대한 수요 증가, 자동화 및 인더스트리 4.0 기술 채택 증가, 제조 및 발전 인프라의 현대화로 인한 것입니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러/10억 달러)

부문별

위상별, 정격 전력별, 1차 전압별, 주파수별, 최종 용도별, 지역별

대상 지역

북미, 아시아태평양, 유럽, 남미, 중동 및 아프리카

신재생에너지 사업에 대한 투자 증가 및 엄격한 에너지 효율 규제가 첨단 제어 변압기의 요구를 더욱 가속화하고 있습니다. 또한 노후화된 설비의 갱신 및 스마트 모니터링 솔루션의 이용 확대가 새로운 기회를 만들어 시장의 상승 기조를 강화하고 있습니다.

정격 전력별로는 1500VA 이상의 부문이 2030년에 산업용 제어 변압기 시장에서 가장 큰 점유율을 차지할 것으로 예측되고, 이는 중부하의 산업 용도에서 중요한 역할 때문입니다. 이러한 대용량 변압기는 석유 및 가스, 금속 및 광업, 화학, 대규모 발전 등 복잡한 기계 및 자동화 시스템을 지원하기 위해 견고하고 안정된 전압 조정이 필수적인 에너지 집약형 부문에서 점점 도입이 진행되고 있습니다. 이 부문의 성장은 중공업의 현대화, 신재생에너지 플랜트 투자 증가, 신흥국 전반에 걸쳐 대규모 제조시설의 확장에 의해 더욱 촉진됩니다. 산업계는 중단 없는 조업을 위해 내구성이 있고 효율적이며 고성능 솔루션을 계속 요구하고 있기 때문에 1500VA를 넘는 카테고리는 강력한 채용이 예상되어 시장 전체 확대의 주요 촉진요인이 되고 있습니다.

120V까지의 부문은 북미에서의 광범위한 채용과 중소규모의 산업 용도 전체에서의 사용 증가에 힘입어 예측 기간 동안 산업용 제어 변압기 시장에서 두 번째로 급성장하는 카테고리가 될 것으로 예측되고 있습니다. 이 변압기는 자동화 패널, 조명 및 저전압 장비의 제어 회로에 특히 적합하며 제조, 전자 및 빌딩 자동화 분야에서 다목적입니다. 산업이 현대화되고 스마트 제어 시스템을 통합함에 따라 컴팩트하고 비용 효율적이며 에너지 효율적인 솔루션에 대한 수요가 증가하고 있는 것도 이 부문의 성장에 박차를 가하고 있습니다. 중소기업에서의 자동화 확대 및 구식 저전압 장비의 꾸준한 교체로 이 부문은 세계적으로 강력한 성장세를 기록할 것으로 보입니다.

아시아태평양은 급속한 산업화, 도시화, 제조업 및 인프라 개척에 대한 대규모 투자로 예측 기간 동안 산업용 제어 변압기 시장에서 가장 빠르게 성장할 것으로 예측됩니다. 중국, 인도, 일본, 한국은 자동화 기술 및 스마트 공장 구상의 도입을 주도하고 있으며, 고급 산업 운영을 지원하는 신뢰할 수 있는 제어 변압기에 대한 강한 수요를 창출하고 있습니다. 게다가 전력 소비량 증가, 재생에너지 프로젝트의 확대, 에너지 효율을 촉진하는 정부 지원 프로그램이 이 지역 시장 성장을 더욱 가속화하고 있습니다. 또한 세계 기업의 존재감이 늘어나 경쟁력 있는 현지 제조업체가 대두해 온 것으로, 시장 경쟁력이 강화되어, 이 지역은 산업용 제어 변압기 산업에 있어서 중요한 성장 거점이 되고 있습니다.

본 보고서에서는 세계의 산업용 제어 변압기 시장에 대해 조사했으며, 위상별, 정격 전력별, 1차 전압별, 주파수별, 최종 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

서문

시장 역학

고객사업에 영향을 주는 동향 및 혼란

생태계 분석

밸류체인 분석

기술 분석

가격 분석

주된 회의 및 이벤트(2025-2026년)

관세 및 규제 상황

무역 분석

특허 분석

Porter's Five Forces 분석

주요 이해관계자 및 구매 기준

투자 및 자금조달 시나리오

사례 연구 분석

생성형 AI 및 AI가 산업용 제어 변압기 시장에 미치는 영향

미국 관세가 산업용 제어 변압기 시장에 미치는 영향(2025년)

제6장 산업용 제어 변압기 시장 : 위상별

서문

삼상

단상

제7장 산업용 제어 변압기 시장 : 정격 전력별

서문

25-500VA

501-1,000 VA

1,001-1,500 VA

1,500VA 이상

제8장 산업용 제어 변압기 시장 : 1차 전압별

서문

120V 이하

121-240V

240V 이상

제9장 산업용 제어 변압기 시장 : 주파수별

서문

50 Hz

60 Hz

제10장 산업용 제어 변압기 시장 : 용도별

서문

발전

석유 및 가스

화학약품

금속 및 광업

기타

제11장 산업용 제어 변압기 시장 : 지역별

서문

아시아태평양

중국

인도

일본

호주

한국

북미

미국

캐나다

멕시코

유럽

독일

이탈리아

영국

프랑스

스페인

남미

브라질

아르헨티나

기타

중동 및 아프리카

GCC

남아프리카

기타

제12장 경쟁 구도

개요

주요 참가 기업의 전략 및 강점(2022-2025년)

시장 점유율 분석(2024년)

수익 분석(2020-2024년)

기업 평가 및 재무지표

제품 비교

기업 평가 매트릭스 : 주요 진입기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

경쟁 시나리오

제13장 기업 프로파일

주요 진출기업

ABB

SCHNEIDER ELECTRIC

SIEMENS

GE VERNOVA

EATON

EMERSON ELECTRIC CO.

ROCKWELL AUTOMATION

HUBBELL

BOARDMAN TRANSFORMERS

MCI TRANSFORMER CORPORATION

DONGAN ELECTRIC MANUFACTURING COMPANY

FOSTER TRANSFORMER COMPANY

TEMCO INDUSTRIAL

GEESYS TECHNOLOGIES(INDIA) PVT. LTD.

CONTROLLED MAGNETICS INCORPORATED

기타 기업

CUSTOM COILS

TROYTRANS

RECO TRANSFORMERS PVT LTD

TRUTECH PRODUCTS

GRANT TRANSFORMERS

제14장 부록

AJY

영문 목차

영문목차

The industrial control transformer market is likely to be valued at USD 1.14 billion in 2025 and USD 1.48 billion by 2030, recording a CAGR of 5.3% during the forecast period. This growth is attributed to the increasing demand for stable and reliable power supply in industrial applications, the rising adoption of automation and Industry 4.0 technologies, and the modernization of manufacturing and power generation infrastructure.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion)

Segments

By Phase, Power Rating, Primary Voltage, Frequency, End Use, and Region.

Regions covered

North America, Asia Pacific, Europe, South America, and Middle East & Africa

The increasing investment in renewable energy projects and the stringent energy efficiency regulations further accelerate the need for advanced control transformers. Additionally, the replacement of aging equipment and the growing use of smart monitoring solutions create new opportunities, reinforcing the market's upward trajectory.

"Above 1,500 VA power rating is expected to account for the largest market share in 2030."

By power rating, the above 1500 VA segment is anticipated to hold the largest share of the industrial control transformer market in 2030, owing to its critical role in heavy-duty industrial applications. These high-capacity transformers are increasingly deployed in energy-intensive sectors, such as oil & gas, metals & mining, chemicals, and large-scale power generation, where robust and stable voltage regulation is essential to support complex machinery and automation systems. The segmental growth is further fueled by the modernization of heavy industries, the increasing investment in renewable energy plants, and the expansion of large manufacturing facilities across emerging economies. As industries continue to demand durable, efficient, and high-performance solutions for uninterrupted operations, the above 1500 VA category is expected to witness strong adoption, positioning it as a key driver of overall market expansion.

"By primary voltage, up to 120 V is projected to be the second fastest-growing segment during the forecast period."

The up to 120 V segment is expected to be the second fastest-growing category in the industrial control transformer market during the forecast period, supported by its widespread adoption in North America and the growing use across small to mid-scale industrial applications. These transformers are particularly well-suited for control circuits in automation panels, lighting, and low-voltage equipment, making them highly versatile across manufacturing, electronics, and building automation sectors. The segmental growth is further fueled by the increasing demand for compact, cost-effective, and energy-efficient solutions, as industries modernize operations and integrate smart control systems. With the expansion of automation in SMEs and the steady replacement of older low-voltage equipment, this segment is positioned to record strong growth momentum globally.

"Asia Pacific is likely to exhibit the highest CAGR in the industrial control transformer market between 2025 and 2030."

Asia Pacific is projected to be the fastest-growing market for industrial control transformers during the forecast period, due to the rapid industrialization, urbanization, and large-scale investments in manufacturing and infrastructure development. China, India, Japan, and South Korea are leading the adoption of automation technologies and smart factory initiatives, creating strong demand for reliable control transformers to support advanced industrial operations. Additionally, the rising electricity consumption, expansion of renewable energy projects, and government-backed programs promoting energy efficiency further accelerate the market growth in the region. The increasing presence of global players and the emergence of competitive local manufacturers also enhance market accessibility, making the region a critical growth hub for the industrial control transformer industry.

Breakdown of Primaries:

In-depth interviews were conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 65%, Tier 2 - 24%, and Tier 3 - 11%

By Designation: C-level Executives - 25%, Directors - 30%, and Others - 45%

By Region: North America - 25%, Europe - 40%, Asia Pacific - 25%, Middle East & Africa - 5%, and South America - 5%

Note: Other designations include sales managers, marketing managers, product managers, and product engineers.

The tier of the companies is defined based on their total revenue as of 2024. Tier 1: USD 1 billion and above, Tier 2: from USD 500 million to USD 1 billion, and Tier 3: <USD 500 million.

A few major players with a wide regional presence dominate the industrial control transformer market. The leading players in the industrial control transformer market are ABB (Switzerland), Siemens (Germany), Eaton (Ireland), GE Vernova (US), and Schneider Electric (France).

Study Coverage:

The report defines, describes, and forecasts the industrial control transformer market by phase, power rating, primary voltage, frequency, end user, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various key aspects of the market, which include the analysis of the competitive landscape, market dynamics, market estimates in terms of value, and future trends in the industrial control transformer market.

Key Benefits of Buying the Report:

Product Development/Innovation: Key drivers (Rise in energy consumption across industries), restraints (Rising implementation of carbon dioxide emission regulations), opportunities (Escalating chemical production), and challenges (Reduced coal mining activities) influence the market.

Market Development: In March 2025, ABB expanded its operations in the US to strengthen its global manufacturing capabilities. As part of this growth strategy, the company invested USD 120 million to scale up transformer production. This includes establishing a state-of-the-art manufacturing facility in Selmer, Tennessee, and expanding its operations in Senatobia, Mississippi, effectively doubling the site's footprint.

Market Diversification: In February 2025, Eaton invested in a new manufacturing facility in South Carolina for its three-phase transformers, marking the company's third facility in the United States. The image shows the transformers' manufacturing process at the company's facility in Wisconsin.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as ABB (Switzerland), Siemens (Germany), Eaton (Ireland), GE Vernova (US), and Schneider Electric (France), in the industrial control transformer market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of primaries

2.1.2.4 List of primary interview participants

2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.3.3 DEMAND-SIDE ANALYSIS

2.3.3.1 Regional analysis

2.3.3.2 Country-level analysis

2.3.3.3 Demand-side assumptions

2.3.3.4 Demand-side calculations

2.3.4 SUPPLY-SIDE ANALYSIS

2.3.4.1 Supply-side assumptions

2.3.4.2 Supply-side calculations

2.4 FORECAST

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL CONTROL TRANSFORMER MARKET

4.2 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY REGION

4.3 INDUSTRIAL CONTROL TRANSFORMER MARKET IN ASIA PACIFIC, BY END USE AND COUNTRY

4.4 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY PHASE

4.5 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY POWER RATING

4.6 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY PRIMARY VOLTAGE

4.7 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY FREQUENCY

4.8 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY END USE

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising energy consumption across industries

5.2.1.2 Increasing requirement for smooth operations of industrial electrical equipment

5.2.2 RESTRAINTS

5.2.2.1 Rising implementation of carbon dioxide emission regulations

5.2.3 OPPORTUNITIES

5.2.3.1 Escalating chemical production

5.2.3.2 Mounting demand for reliable power infrastructure amid rise in manufacturing

5.2.4 CHALLENGES

5.2.4.1 Reduced coal mining activities

5.2.4.2 Heavy losses due to voltage spikes

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 ECOSYSTEM ANALYSIS

5.5 VALUE CHAIN ANALYSIS

5.6 TECHNOLOGY ANALYSIS

5.6.1 DC POWER

5.7 PRICING ANALYSIS

5.7.1 PRICING RANGE OF INDUSTRIAL CONTROL TRANSFORMERS, BY PRIMARY VOLTAGE, 2024

5.8 KEY CONFERENCES AND EVENTS, 2025-2026

5.9 TARIFF AND REGULATORY LANDSCAPE

5.9.1 TARIFFS ANALYSIS

5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.9.3 CODES AND REGULATIONS

5.10 TRADE ANALYSIS

5.10.1 IMPORT SCENARIO (HS CODE 8504)

5.10.2 EXPORT SCENARIO (HS CODE 8504)

5.11 PATENT ANALYSIS

5.12 PORTER'S FIVE FORCES ANALYSIS

5.12.1 THREAT OF SUBSTITUTES

5.12.2 BARGAINING POWER OF SUPPLIERS

5.12.3 BARGAINING POWER OF BUYERS

5.12.4 THREAT OF NEW ENTRANTS

5.12.5 INTENSITY OF COMPETITIVE RIVALRY

5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.13.2 BUYING CRITERIA

5.14 INVESTMENT AND FUNDING SCENARIO

5.15 CASE STUDY ANALYSIS

5.15.1 EFACEC GROUP ADVOCATES USE OF MODELING SOFTWARE TO TEST TRANSFORMER DESIGNS

5.15.2 CONDITION-BASED MAINTENANCE (CBM) TECHNOLOGIES HELP DETECT EARLY WARNING SIGNS OF FAILURE IN TRANSFORMERS

5.16 IMPACT OF GEN AI/AI ON INDUSTRIAL CONTROL TRANSFORMER MARKET

5.16.1 ADOPTION OF GEN AI/AI IN INDUSTRIAL CONTROL TRANSFORMER MARKET

5.16.2 IMPACT OF GEN AI/AI ON INDUSTRIAL CONTROL TRANSFORMER MARKET, BY REGION

5.17 IMPACT OF 2025 US TARIFF ON INDUSTRIAL CONTROL TRANSFORMER MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRIES/REGIONS

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END USES

6 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY PHASE

6.1 INTRODUCTION

6.2 THREE-PHASE

6.2.1 EFFECTIVENESS IN CONTROLLING POWER FOR HIGH INDUSTRIAL LOADS TO BOOST SEGMENTAL GROWTH

6.3 SINGLE-PHASE

6.3.1 ABILITY TO MAINTAIN STEADY VOLTAGE AND SMOOTH OPERATION TO FOSTER SEGMENTAL GROWTH

7 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY POWER RATING

7.1 INTRODUCTION

7.2 25-500 VA

7.2.1 ABILITY TO ADJUST VOLTAGE AND PROTECT AGAINST RISK OF FIRE OR SHOCK TO BOLSTER SEGMENTAL GROWTH

7.3 501-1,000 VA

7.3.1 NEED TO MAINTAIN CONSTANT VOLTAGE IN INDUSTRIAL PROCESSES TO AUGMENT SEGMENTAL GROWTH

7.4 1,001-1,500 VA

7.4.1 FOCUS ON MAINTAINING SPEED OF MATERIAL HANDLING SYSTEMS IN INDUSTRIES TO BOOST DEMAND

7.5 ABOVE 1,500 VA

7.5.1 RISE IN OIL & GAS EXPLORATION AND NEED TO RETROFIT AGING INFRASTRUCTURE IN POWER PLANTS TO DRIVE MARKET

8 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY PRIMARY VOLTAGE

8.1 INTRODUCTION

8.2 UP TO 120 V

8.2.1 REQUIREMENT FOR LOW VOLTAGES IN SMALL RESIDENTIAL AND COMMERCIAL SPACES TO EXPEDITE SEGMENTAL GROWTH

8.3 121-240 V

8.3.1 USE TO CONTROL IN-RUSH CURRENT INTO MOTORS, VARIABLE DRIVE SYSTEMS, AND CONTROL PANELS TO FUEL SEGMENTAL GROWTH

8.4 ABOVE 240 V

8.4.1 RISING INDUSTRIAL AUTOMATION TO CONTRIBUTE TO SEGMENTAL GROWTH

9 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY FREQUENCY

9.1 INTRODUCTION

9.2 50 HZ

9.2.1 IMPLEMENTATION OF POWER SUPPLY REGULATIONS TO ACCELERATE SEGMENTAL GROWTH

9.3 60 HZ

9.3.1 GROWING FOCUS ON SMOOTH INDUSTRIAL OPERATIONS TO FOSTER SEGMENTAL GROWTH

10 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY END USE

10.1 INTRODUCTION

10.2 POWER GENERATION

10.2.1 RAPID ADVANCES IN PROTECTION RELAYS TO FUEL SEGMENTAL GROWTH

10.3 OIL & GAS

10.3.1 INCREASING INVESTMENT IN ENHANCED OIL RECOVERY EXPLORATION TO AUGMENT SEGMENTAL GROWTH

10.4 CHEMICALS

10.4.1 INCREASING ADOPTION OF PROCESS AUTOMATION AND DIGITALIZATION TO FUEL DEMAND

10.5 METALS & MINING

10.5.1 MOUNTING DEMAND FOR ROBUST ELECTRICAL INFRASTRUCTURE TO BOOST SEGMENTAL GROWTH

10.6 OTHER END USES

11 INDUSTRIAL CONTROL TRANSFORMER MARKET, BY REGION

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 CHINA

11.2.1.1 Extensive energy consumption and environmental concerns to bolster market growth

11.2.2 INDIA

11.2.2.1 Mounting electricity demand due to expanding economy to fuel market growth

11.2.3 JAPAN

11.2.3.1 Growing emphasis on energy security and environmental sustainability to boost market growth

11.2.4 AUSTRALIA

11.2.4.1 Mounting power demand amid population growth to drive market

11.2.5 SOUTH KOREA

11.2.5.1 Strong commitment to supplying power through renewable energy to expedite market growth

11.2.5.2 Rest of Asia Pacific

11.3 NORTH AMERICA

11.3.1 US

11.3.1.1 Increasing production of crude oil and related products to drive market

11.3.2 CANADA

11.3.2.1 Growing focus on smart grid infrastructure and clean energy initiatives to boost market growth

11.3.3 MEXICO

11.3.3.1 Emergence as primary offshore energy production zone to contribute to market growth

11.4 EUROPE

11.4.1 GERMANY

11.4.1.1 Increasing investment in industrial automation to bolster market growth

11.4.2 ITALY

11.4.2.1 Rising focus on sustainable, less polluting, and efficient chemicals to augment market growth

11.4.3 UK

11.4.3.1 Aging infrastructure and increased risk of blackouts to fuel market growth

11.4.4 FRANCE

11.4.4.1 Increasing investment in renewable energy innovation projects to accelerate market growth

11.4.5 SPAIN

11.4.5.1 Growing emphasis on decarbonization and digitalization to boost market growth

11.4.5.2 Rest of Europe

11.5 SOUTH AMERICA

11.5.1 BRAZIL

11.5.1.1 Increasing investment in offshore exploration to contribute to market growth

11.5.2 ARGENTINA

11.5.2.1 Rapid industrial and infrastructural developments to boost market growth

11.5.3 REST OF SOUTH AMERICA

11.6 MIDDLE EAST & AFRICA

11.6.1 GCC

11.6.1.1 Saudi Arabia

11.6.1.1.1 Growing emphasis on reducing carbon emissions to accelerate market growth

11.6.1.2 UAE

11.6.1.2.1 Strong push toward modernizing and upgrading aging power plants to boost market growth

11.6.1.3 Rest of GCC

11.6.2 SOUTH AFRICA

11.6.2.1 Mounting power demand and infrastructure development to fuel market growth

11.6.3 REST OF MIDDLE EAST & AFRICA

12 COMPETITIVE LANDSCAPE

12.1 OVERVIEW

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

12.3 MARKET SHARE ANALYSIS, 2024

12.4 REVENUE ANALYSIS, 2020-2024

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 PRODUCT COMPARISON

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1 Company footprint

12.7.5.2 Region footprint

12.7.5.3 Phase footprint

12.7.5.4 Power rating footprint

12.7.5.5 Primary voltage footprint

12.7.5.6 End use footprint

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024