ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

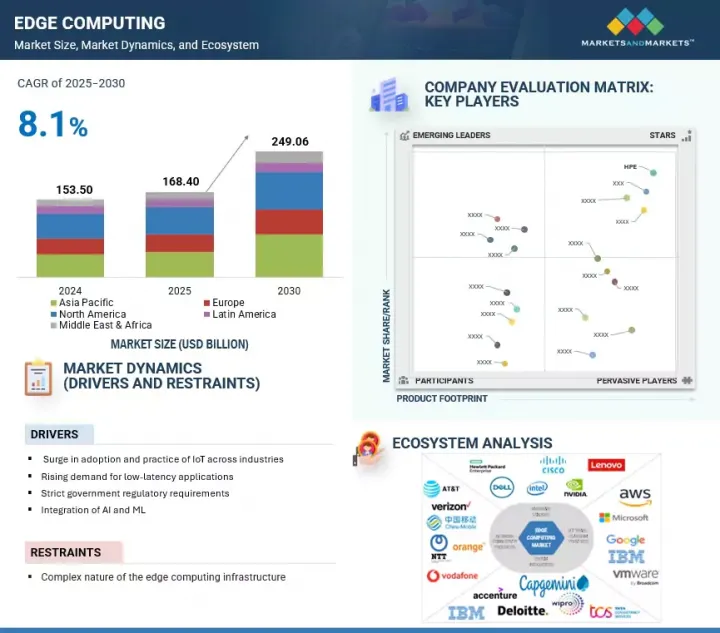

세계의 엣지 컴퓨팅 시장 규모는 급속히 확대되고 있으며, 2025년 약 1,684억 달러에서 2030년에는 2,490억 6,000만 달러에 이를 것으로 예측되며, CAGR 8.1%의 성장이 전망됩니다.

엣지 컴퓨팅 시장 성장을 촉진하는 주요 요인과 제약 요인이 존재합니다. 주요 요인으로는 사물인터넷(IoT) (IoT) 솔루션의 확산으로 네트워크의 엣지에서 실시간 데이터 처리 및 분석의 필요성이 촉진되고 있습니다.

조사 범위

조사 대상 연도

2020-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

10억 달러

부문

컴포넌트별, 용도별, 조직 규모별, 전개 유형별, 업계별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동, 아프리카, 라틴아메리카

저지연 용도에 대한 수요 증가가 시장 확장을 더욱 촉진하고 있으며, 안전한 및 준수 가능한 엣지 전개를 장려하는 엄격한 정부 규제 요건도 이에 기여하고 있습니다. 또한 인공지능(AI)과 머신 러닝(ML)의 통합은 조직이 엣지에서 직접 더 스마트하고 자율적인 운영을 실현할 수 있도록 지원합니다. 반면, 제약 요인은 엣지 컴퓨팅 인프라의 복잡한 특성으로, 전개, 관리, 기존 시스템과의 원활한 통합에 있어 심각한 도전 과제를 제기합니다.

엣지의 네트워크 관리는 연결성 관리, 성능 모니터링, 네트워크 최적화, 네트워크 보안 등을 포함하며, 분산된 인프라의 신뢰성과 효율성을 보장하는 데 필수적입니다. 조직이 다양한 환경에 많은 엣지 장치를 전개함에 따라, 데이터 병목 현상을 방지하고 위협을 조기에 탐지하며 지연 시간을 줄이기 위해 실시간 네트워크 가시성과 제어의 중요성이 점점 더 커지고 있습니다. 고급 네트워크 관리 솔루션을 제공하는 벤더들은 기업이 지속적인 워크플로우를 지원하고 문제 해결을 가속화하며, 원격 또는 대역폭 제약 환경에서도 높은 서비스 가용성을 보장할 수 있도록 지원합니다. 5G 채택의 증가와 IoT 및 AI의 산업 간 통합은 네트워크에 대한 압력을 가중시키며, 강력한 관리 도구는 전략적 투자로 부상하고 있습니다. 이는 솔루션 제공업체가 산업별 요구사항에 맞춤형으로 설계된 플랫폼 독립적, 보안 강화, 확장 가능한 네트워크 관리 기능을 제공하는 강력한 기회를 제공합니다. 자동화, 간소화된 오케스트레이션, 사전 예방적 문제 해결에 초점을 맞춘 업체들은 기업 수요를 충족시키고 확장되는 엣지 컴퓨팅 생태계에서 중심 역할을 할 것으로 예상됩니다.

온프레미스 엣지는 예측 기간 동안 엣지 컴퓨팅 시장 최대 시장 점유율을 유지할 것으로 예상됩니다. 이는 기업과 조직이 현지화된 데이터 처리, 강화된 개인정보 보호, 디지털 인프라에 대한 직접적인 통제를 요구하기 때문입니다. 이 성장 추세는 운영 연속성, 규제 준수, 신속한 대응이 필수적인 의료, 고급 제조, 핵심 인프라 등 분야에서 특히 두드러집니다. 조직은 시설 내 엣지 리소스를 전개함으로써 클라우드 의존성으로 인한 잠재적 위험(네트워크 중단, 데이터 주권 문제 등)을 회피하며, 실시간 분석과 같은 용도에 대해 최저의 지연 시간을 보장합니다. 자동화, 품질 관리와 같은 애플리케이션에 대해 가능한 가장 낮은 지연 시간을 확보할 수 있습니다. 디지털 전환이 가속화되면서 투자와 혜택의 균형이 변화하고 있으며, 온프레미스 엣지의 총 소유 비용은 보안, 신뢰성, 운영 유연성 측면의 실질적인 이점으로 정당화되고 있습니다. 현재의 엣지 솔루션은 점점 더 모듈화되고 확장 가능해져 모든 규모의 기업이 정확한 요구사항에 맞는 전용 엣지 노드를 도입할 수 있게 되었습니다. 벤더 및 솔루션 제공업체에게는 견고하고 상호운용 가능한 플랫폼, 원활한 통합 도구, 전개 및 라이프사이클 관리를 간소화하는 관리형 서비스에 대한 지속적인 수요가 발생합니다. 시장 추세는 고객 파트너십 강화, 산업별 맞춤형 엣지 솔루션 개발, 신뢰성, 성능, 복원력이 경쟁 우위를 결정하는 시장에서 리더십 확립의 지속적인 기회를 시사합니다. 기업들이 분산형 아키텍처에 투자함에 따라, 채택 용이성, 투명한 보안, 목적에 맞는 솔루션을 우선시하는 공급업체들은 차별화된 서비스를 제공하며 이 역동적인 환경에서 장기적인 성장을 확보할 것입니다.

북미는 고급 인프라, 강력한 5G 커버리지, 실시간 솔루션에 대한 기업 수요로 인해 엣지 컴퓨팅 시장을 선도하고 있으며, 아시아태평양 지역은 클라우드 채택 가속화, 대규모 IoT 전개, 정부 지원의 지역별 엣지 인프라 투자로 인해 가장 빠르게 성장하는 지역입니다.

북미는 기업들의 실시간 데이터 처리, 저지연 용도, 안전한 분산형 아키텍처에 대한 수요 증가에 의해 촉진되어 엣지 컴퓨팅 시장을 주도할 것으로 예상됩니다. 공급업체와 솔루션 제공업체에게는 제조, 의료, 통신, 자율주행 차량 등 산업에 확장 가능한 플랫폼과 서비스를 제공하는 데 중요한 기회를 제공합니다. 해당 지역의 성숙한 5G 인프라와 IoT 전개 확대는 중앙 집중형 클라우드에서 엣지 기반 처리로의 전환을 촉진하며, 데이터 주권 규정을 준수하는 현지화 솔루션에 대한 필수적인 수요를 창출합니다. 통신 네트워크에 엣지 기능을 통합하는 전략적 파트너십은 엣지 컴퓨팅이 운영 효율성과 사용자 경험을 향상시키는 방식을 보여줍니다. 이러한 동향을 활용하면 공급업체는 진화하는 고객 요구사항을 충족시키고 지연 문제를 줄이며, 급속한 성장과 혁신을 앞두고 있는 시장에서 강력한 입지를 구축할 수 있습니다.

본 보고서에서는 세계의 엣지 컴퓨팅 시장에 대해 조사했으며, 컴포넌트별, 용도별, 조직 규모별, 전개 유형별, 업계별, 지역별 동향, 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요와 업계 동향

소개

시장 역학

사례 연구 분석

생태계 분석

공급망 분석

기술 분석

Porter's Five Forces 분석

가격 분석

특허 분석

규제 상황

고객의 비즈니스에 영향을 미치는 동향과 혼란

주요 이해관계자와 구매 기준

주된 회의 및 이벤트(2025-2026년)

무역 분석

엣지 컴퓨팅 시장의 생성형 AI의 영향

비즈니스 모델

투자 상황과 자금 조달 시나리오

미국 관세의 영향(2025년)

엣지로 처리되는 데이터의 유형

제6장 엣지 컴퓨팅 시장(컴포넌트별)

소개

엣지 하드웨어

엣지 소프트웨어

서비스

제7장 엣지 컴퓨팅 시장(용도별)

소개

실시간 처리 및 제어

엣지 AI 및 추론

IoT 및 산업 자동화

콘텐츠 전달 및 미디어

몰입형 및 상호작용형 경험

기타

제8장 엣지 컴퓨팅 시장(조직 규모별)

소개

대기업

중소기업(SMES)

제9장 엣지 컴퓨팅 시장(전개 유형별)

소개

클라우드 엣지

On-Premise 엣지

디바이스 엣지

제10장 엣지 컴퓨팅 시장(업계별)

소개

제조

에너지 및 유틸리티

소프트웨어 및 IT 서비스

통신

자동차

미디어 및 엔터테인먼트

소매 및 소비재

운송 및 물류

의료 및 생명과학

기타

제11장 엣지 컴퓨팅 시장(지역별)

소개

북미

북미 : 엣지 컴퓨팅 시장 성장 촉진요인

북미 : 거시경제 전망

미국

캐나다

유럽

유럽 : 엣지 컴퓨팅 시장 성장 촉진요인

유럽 : 거시경제 전망

영국

독일

프랑스

이탈리아

기타

아시아태평양

아시아태평양 : 엣지 컴퓨팅 시장 성장 촉진요인

아시아태평양 : 거시경제 전망

중국

일본

호주 및 뉴질랜드(ANZ)

기타

중동 및 아프리카

중동 및 아프리카 : 엣지 컴퓨팅 시장 성장 촉진요인

중동 및 아프리카 : 거시경제 전망

걸프 협력 이사회(GCC)

남아프리카

기타

라틴아메리카

라틴아메리카 : 엣지 컴퓨팅 시장 성장 촉진요인

라틴아메리카 : 거시경제 전망

브라질

멕시코

기타

제12장 경쟁 구도

소개

주요 진입기업의 전략 및 강점

시장 점유율 분석

제품/브랜드 비교

수익 분석

기업평가 매트릭스 : 주요 진출기업(2024년)

기업평가 매트릭스 : 스타트업/중소기업(2024년)

주요 벤더의 기업 평가 및 재무 지표

경쟁 시나리오와 동향

제13장 기업 프로파일

소개

주요 진출기업

DELL TECHNOLOGIES

AWS

MICROSOFT

CISCO

HPE

IBM

GOOGLE

NVIDIA

INTEL

HUAWEI

기타 기업

NOKIA

VMWARE

FASTLY

ADLINK

ORACLE

SEMTECH

MOXA

BELDEN

GE DIGITAL

DIGI INTERNATIONAL

LITMUS AUTOMATION

ZEDEDA

CLEARBLADE

VAPOR IO

SIXSQ

EDGEWORX

SUNLIGHT.IO

SAGUNA NETWORKS

ALEF EDGE

MUTABLE 326 13.3.21 ZTE CORPORATION

ADVANTECH CO., LTD.

LENOVO GROUP LTD

제14장 인접 시장과 관련 시장

제15장 부록

HBR

영문 목차

영문목차

The global edge computing market is expanding rapidly, with a projected market size expected to rise from about USD 168.40 billion in 2025 to USD 249.06 billion by 2030, at a CAGR of 8.1%. Several key drivers and restraints primarily shape the growth of the edge computing market. Drivers include the surge in adoption and practice of Internet of Things (IoT) solutions across various industries, driving the need for real-time data processing and analytics at the network's edge.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

USD Billion

Segments

Component, application, organization size, deployment mode, and vertical

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, and Latin America

Rising demand for low-latency applications further propels market expansion, alongside strict government regulatory requirements that encourage secure and compliant edge deployments. Additionally, integrating artificial intelligence (AI) and machine learning (ML) empowers organizations to realize smarter, autonomous operations directly at the edge. On the other hand, restraints center around the complex nature of edge computing infrastructure, which poses significant challenges in deployment, management, and seamless integration with legacy systems.

By edge software, network management to account for the highest growth rate during the forecast period

Network management is expected to account for the highest growth rate during the forecast period. This growth is driven by edge deployments' rising complexity and scale, where maintaining seamless connectivity, secure communication, and consistent performance is critical to business operations. Network management at the edge includes connectivity management, performance monitoring, network optimization, and network security, all of which are essential to ensure the reliability and efficiency of distributed infrastructure. As organizations deploy many edge devices across diverse environments, real-time network visibility and control become increasingly important to prevent data bottlenecks, detect threats early, and reduce latency. Vendors that deliver advanced network management solutions enable enterprises to support continuous workflows, achieve faster issue resolution, and ensure high service availability even in remote or bandwidth-constrained locations. The increase in 5G adoption and the integration of IoT and AI across industries add to the pressure on networks, making robust management tools a strategic investment. This presents a strong opportunity for solution providers to offer platform-agnostic, secure, and scalable network management capabilities tailored to industry-specific needs. Those focusing on automation, simplified orchestration, and proactive troubleshooting are expected to be better positioned to meet enterprise demand and play a central role in the expanding edge computing ecosystem.

On-premises edge deployment mode to hold the largest market share during the forecast period

On-premises edge is expected to maintain the largest share of the edge computing market during the forecast period, reflecting a strong demand from enterprises and organizations that require localized data processing, heightened privacy, and direct control over their digital infrastructure. This growth is particularly evident in sectors where operational continuity, regulatory compliance, and rapid response are non-negotiable, such as healthcare, advanced manufacturing, and critical infrastructure. By deploying edge resources within their facilities, organizations bypass the potential risks of cloud dependency, such as network outages and data sovereignty concerns, while securing the lowest possible latency for applications such as real-time analytics, automation, and quality control. As digital transformation accelerates, the balance between investment and benefit shifts, with the total cost of ownership for on-premises edge being justified by tangible gains in security, reliability, and operational agility. Today's edge offerings are increasingly modular and scalable, making it feasible for enterprises of all sizes to adopt dedicated edge nodes that fit their precise requirements. For vendors and solution providers, this means steady demand for robust, interoperable platforms, seamless integration tools, and managed services that simplify deployment and lifecycle management. The market's trajectory signals ongoing opportunities to deepen client partnerships, develop sector-specific edge solutions, and establish leadership in markets where trust, performance, and resilience define competitive advantage. As enterprises invest in distributed architectures, vendors prioritizing ease of adoption, transparent security, and fit-for-purpose solutions will differentiate their offerings and secure long-term growth in this dynamic environment.

North America leads the edge computing market with advanced infrastructure, strong 5G coverage, and high enterprise demand for real-time solutions, while Asia Pacific is the fastest-growing region driven by rapid cloud adoption, large-scale IoT deployments, and government-backed investments in localized edge infrastructure.

North America is expected to lead the edge computing market, driven by increasing enterprise demand for real-time data processing, low-latency applications, and secure distributed architectures. For vendors and solution providers, this means significant opportunities to deliver scalable platforms and services that support industries such as manufacturing, healthcare, telecommunications, and autonomous vehicles. The region's mature 5G infrastructure and growing IoT deployments enable the shift from centralized cloud to edge-based processing, creating a critical need for localized solutions that ensure compliance with data sovereignty regulations. Strategic partnerships, such as integrating edge capabilities into telecommunications networks, demonstrate how edge computing enhances operational efficiency and user experience. Capitalizing on these trends allows vendors to address evolving customer requirements, reduce latency challenges, and establish strong footholds in a market poised for rapid growth and innovation.

Breakdown of Primary interviews

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the edge computing market.

By Company: Tier I - 35%, Tier II - 25%, and Tier III - 40%

By Designation: C-Level Executives - 25%, D-Level Executives -30%, and Others - 45%

By Region: North America - 42%, Europe - 25%, Asia Pacific - 18%, and Rest of the World - 15%

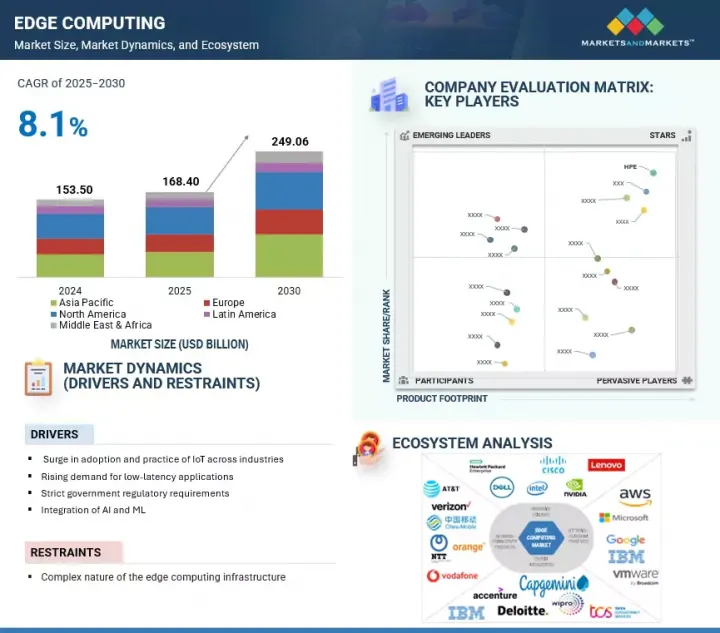

The report includes a study of key players offering edge computing services. It profiles major vendors in the edge computing market. The major market players include HPE (US), AWS (US), Dell Technologies (US), Cisco (US), Microsoft (US), IBM (US), Google (US), Nvidia (US), Intel (US), Huawei (China), Nokia (Finland), VMware (US), Fastly (US), Adlink (Taiwan), Oracle (US), Semtech (US), Moxa (US), Belden (US), GE Digital (US), DG International (US), Litmus Automation (US), Zededa (US), Clearblade (US), and Vapor IO (US).

Research Coverage

This research report categorizes the edge computing market based on Component (edge hardware (edge servers, edge gateways, edge sensors, edge devices)), edge software (data management, device management, application management, network management), and services (professional services, and managed services)), Application (real-time processing & control, edge-AI & inference, IoT & industrial automation, content delivery & media, immersive & interactive experiences, and other applications (security & access control, healthcare & telemedicine, consumer & smart living)), Organization size (large enterprises, small & medium sized enterprises), Deployment mode (cloud edge, on-premises edge, device edge), Vertical (manufacturing/industrial, energy & utilities, software & IT services, telecommunications, automotive, media & entertainment, retail & consumer goods, transportation & logistics, healthcare & life sciences, and other verticals (education, government & public sector, BFSI)) and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the edge computing market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers & acquisitions; and recent developments associated with the edge computing market. This report also covers the competitive analysis of upcoming startups in the edge computing market ecosystem.

Reason to buy this Report

The report provides market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall edge computing market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (Surge in adoption and practice of IoT across industries, Rising demand for low-latency applications, Strict government regulatory requirements, Integration of AI and ML), restraints (Complex nature of the edge computing infrastructure ), opportunities (Advent of 5G network to provide open avenues for large-scale 5G network deployment, Proliferation of IoT, Rapid adoption of edge computing solutions across sectors, Emergence of autonomous automobiles and connected car infrastructure), and challenges (Increasing data privacy and security concerns, Challenges in compatibility or interoperability).

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the edge computing market.

Market Development: Comprehensive information about lucrative markets - the report analyses the edge computing market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the edge computing market.

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such HPE (US), AWS (US), Dell Technologies (US), Cisco (US), Microsoft (US), IBM (US), Google (US), Nvidia (US), Intel (US), Huawei (China), Nokia (Finland), VMware (US), Fastly (US), Adlink (Taiwan), Oracle (US), Semtech (US), Moxa (US), Belden (US), GE Digital (US), DG International (US), Litmus Automation (US), Zededa (US), Clearblade (US), and Vapor IO (US). The report also helps stakeholders understand the edge computing market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Breakup of primary profiles

2.1.2.3 Key industry insights

2.2 MARKET BREAKUP AND DATA TRIANGULATION

2.3 MARKET SIZE ESTIMATION

2.4 MARKET FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN EDGE COMPUTING MARKET

4.2 EDGE COMPUTING MARKET, BY COMPONENT (2025 VS 2030)

4.3 EDGE COMPUTING MARKET, BY APPLICATION (2025 VS 2030)

4.4 EDGE COMPUTING MARKET, BY DEPLOYMENT TYPE (2025 VS 2030)

4.5 EDGE COMPUTING MARKET, BY ORGANIZATION SIZE (2025 VS 2030)

4.6 EDGE COMPUTING MARKET, BY VERTICAL (2025 VS 2030)

4.7 EDGE COMPUTING MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Exponential scale of IoT and endpoint intelligence

5.2.1.2 Rising demand for low-latency applications

5.2.1.3 Integration of edge AI/ML for autonomous decision-making

5.2.1.4 Stringent government regulatory requirements

5.2.2 RESTRAINTS

5.2.2.1 Economic and policy constraints in emerging markets

5.2.2.2 Complex nature of edge computing infrastructure

5.2.3 OPPORTUNITIES

5.2.3.1 Advent of 5G network to provide open avenues for large-scale 5G network deployment

5.2.3.2 Remote and mission-critical edge deployment

5.2.3.3 Rapid adoption of edge computing solutions across sectors

5.2.3.4 Emergence of autonomous automobiles and connected car infrastructure

5.2.4 CHALLENGES

5.2.4.1 Increasing data privacy and security concerns

5.2.4.2 Skill gap and operational expertise

5.2.4.3 Challenges in compatibility or interoperability

5.3 CASE STUDY ANALYSIS

5.3.1 AKAMAI HELPED MATRIMONY.COM ACHIEVE WEBSITE OPTIMIZATION AND INCREASED USER RETENTION

5.3.2 ESPN ADOPTED MICROSOFT'S INNOVATIVE TECHNOLOGIES TO RESHAPE FUTURE OF SPORTS PRODUCTION

5.3.3 VMWARE HELPED NORTHERN BEACHES COUNCIL BE PACESETTER TO DRIVE AND DIGITALIZE REGIONAL MUNICIPAL SERVICES

5.3.4 MASERATI MSG RACING AUTOMATED WORKFLOW ENABLEMENT WITH HEWLETT-PACKARD ENTERPRISE TO OPTIMIZE TEAM PERFORMANCE

5.3.5 99BRIDGES HELPED HUMAN HABITS RESTORE AND PROTECT ENVIRONMENT WITH CISCO'S IOT OPERATIONS DASHBOARD

5.4 ECOSYSTEM ANALYSIS

5.5 SUPPLY CHAIN ANALYSIS

5.5.1 EDGE COMPUTING TECHNOLOGY PROVIDERS

5.5.2 EDGE COMPUTING HARDWARE VENDORS

5.5.3 NETWORK SERVICE PROVIDERS

5.5.4 END USERS

5.6 TECHNOLOGY ANALYSIS

5.6.1 KEY TECHNOLOGIES

5.6.1.1 Edge AI

5.6.1.2 Virtual Network Functions

5.6.1.3 Content Delivery Network

5.6.1.4 Container Orchestration

5.6.1.5 Containerization

5.6.1.6 Zero-trust Security

5.6.2 COMPLEMENTARY TECHNOLOGIES

5.6.2.1 Internet of Things (IoT)

5.6.2.2 Digital Twin

5.6.2.3 Remote Device Management

5.6.2.4 Multi-access Edge Computing

5.6.2.5 Computer vision SDKs

5.6.2.6 Cybersecurity For Edge

5.6.3 ADJACENT TECHNOLOGIES

5.6.3.1 Cloud Computing

5.6.3.2 Blockchain

5.6.3.3 AR/VR

5.7 PORTER'S FIVE FORCES ANALYSIS

5.7.1 THREAT OF NEW ENTRANTS

5.7.2 THREAT OF SUBSTITUTES

5.7.3 BARGAINING POWER OF SUPPLIERS

5.7.4 BARGAINING POWER OF BUYERS

5.7.5 INTENSITY OF COMPETITIVE RIVALRY

5.8 PRICING ANALYSIS

5.8.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY REGION, 2025

5.8.2 INDICATIVE PRICING ANALYSIS OF EDGE COMPUTING SOLUTIONS

5.9 PATENT ANALYSIS

5.10 REGULATORY LANDSCAPE

5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.10.1.1 Regulatory implications and industry standards

5.10.1.2 General Data Protection Regulation

5.10.1.3 SEC Rule 17a-4

5.10.1.4 ISO/IEC 27001

5.10.1.5 System and Organization Controls 2 Type II compliance

5.10.1.6 Financial Industry Regulatory Authority

5.10.1.7 Freedom of Information Act

5.10.1.8 Health Insurance Portability and Accountability Act

5.10.2 REGULATIONS, BY REGION

5.11 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.12.2 BUYING CRITERIA

5.13 KEY CONFERENCES AND EVENTS, 2025-2026

5.14 TRADE ANALYSIS

5.14.1 IMPORT SCENARIO

5.14.2 EXPORT SCENARIO

5.15 IMPACT OF GENERATIVE AI ON EDGE COMPUTING MARKET

5.15.1 TOP USE CASES & MARKET POTENTIAL

5.15.2 KEY USE CASES

5.15.3 CASE STUDIES

5.15.3.1 Case Study: McDonald's with Google Cloud: AI-powered Edge at Scale

10.6.1 DRIVING REAL-TIME INTELLIGENCE FOR SAFE, CONNECTED, AND AUTONOMOUS VEHICLES

10.6.2 AUTOMOTIVE: USE CASES

10.6.2.1 Autonomous driving and advanced driver assistance (ADAS)

10.6.2.2 Vehicle-to-everything (V2X) communication and smart mobility

10.6.2.3 In-vehicle infotainment and personalized experiences

10.7 MEDIA & ENTERTAINMENT

10.7.1 EDGE COMPUTING PROVIDES INSTANTANEOUS CONNECTION AND BETTER SCALABILITY FOR CONTENT CREATION AND DISTRIBUTION

10.7.2 MEDIA & ENTERTAINMENT: USE CASES

10.7.2.1 Personalized content recommendation

10.7.2.2 Real-time video streaming

10.7.2.3 Edge-based gaming

10.7.2.4 Virtual production

10.7.2.5 Interactive live events

10.8 RETAIL & CONSUMER GOODS

10.8.1 EDGE COMPUTING LEVERAGES NEW TECHNOLOGIES TO GATHER INSIGHTS ON PURCHASING PREFERENCES OF CONSUMERS

10.8.2 RETAIL & CONSUMER GOODS: USE CASES

10.8.2.1 Real-time inventory management

10.8.2.2 Personalized marketing

10.8.2.3 In-store analytics

10.8.2.4 Smart checkout

10.8.2.5 Dynamic pricing

10.9 TRANSPORTATION & LOGISTICS

10.9.1 EDGE COMPUTING REDUCES DATA SHARING AND LATENCY, FACILITATING EFFECTIVE AND EFFICIENT CONNECTION WITH DEVICES AND SENSORS IN VEHICLES AND DATABASES

10.9.2 TRANSPORTATION & LOGISTICS: USE CASES

10.9.2.1 Fleet management

10.9.2.2 Route optimization

10.9.2.3 Real-time cargo monitoring

10.9.2.4 Warehouse automation

10.10 HEALTHCARE & LIFE SCIENCES

10.10.1 IOT AND SMART WEARABLE EDGE DEVICES RECORD REAL-TIME VITAL INFORMATION

10.10.2 HEALTHCARE & LIFE SCIENCES: USE CASES

10.10.2.1 Remote patient monitoring

10.10.2.2 Smart hospitals

10.10.2.3 Secure data processing

10.10.2.4 Wearable health devices

10.10.2.5 Genomic analysis at the edge

10.11 OTHER VERTICALS

11 EDGE COMPUTING MARKET, BY REGION

11.1 INTRODUCTION

11.2 NORTH AMERICA

11.2.1 NORTH AMERICA: EDGE COMPUTING MARKET DRIVERS

11.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

11.2.3 US

11.2.3.1 Higher adoption of edge computing solutions and associated services (professional, managed) to drive US market

11.2.4 CANADA

11.2.4.1 Enhanced data security and operational efficiency achieved by practicing edge computing software and services

11.3 EUROPE

11.3.1 EUROPE: EDGE COMPUTING MARKET DRIVERS

11.3.2 EUROPE: MACROECONOMIC OUTLOOK

11.3.3 UK

11.3.3.1 Real-time data processing by companies to drive market in UK

11.3.4 GERMANY

11.3.4.1 Strong emphasis on Industry 4.0 and digital transformation initiatives taken to propel market

11.3.5 FRANCE

11.3.5.1 Real-time data processing and analytics, and personalized customer experiences to drive the French market

11.3.6 ITALY

11.3.6.1 Presence of key edge computing vendors with plans to implement smart cities and industrial automation to leverage market proliferation

11.3.7 REST OF EUROPE

11.4 ASIA PACIFIC

11.4.1 ASIA PACIFIC: EDGE COMPUTING MARKET DRIVERS

11.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

11.4.3 CHINA

11.4.3.1 Rapid proliferation and surge in adoption of edge computing solutions to drive Chinese market

11.4.4 JAPAN

11.4.4.1 Fusion of technologies such as AI & robotics with edge computing to propel market growth

11.4.5 AUSTRALIA & NEW ZEALAND (ANZ)

11.4.5.1 Extensive adoption of edge computing products to leverage market proliferation in ANZ, increasing agility in application deployment

11.4.6 REST OF ASIA PACIFIC

11.5 MIDDLE EAST & AFRICA

11.5.1 MIDDLE EAST & AFRICA: EDGE COMPUTING MARKET DRIVERS

11.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

11.5.3 GULF COOPERATION COUNCIL (GCC)

11.5.3.1 kingdom of Saudi Arabia

11.5.3.1.1 Fueling Vision 2030 goals using edge computing software and services to drive market adoption

11.5.3.2 United Arab Emirates (UAE)

11.5.3.2.1 Edge computing products to leverage data-driven insights to gain competitive advantage for UAE businesses

11.5.3.3 Other GCC Countries

11.5.4 SOUTH AFRICA

11.5.4.1 Edge computing software solves challenges such as lower latency, bandwidth, and data sovereignty

11.5.5 REST OF MIDDLE EAST & AFRICA

11.6 LATIN AMERICA

11.6.1 LATIN AMERICA: EDGE COMPUTING MARKET DRIVERS

11.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

11.6.3 BRAZIL

11.6.3.1 Innovative edge computing practices across agriculture, healthcare, and urban infrastructure to fuel market growth

11.6.4 MEXICO

11.6.4.1 Comprehensive edge computing solutions designed to meet diverse needs of Mexican enterprises to drive market

11.6.5 REST OF LATIN AMERICA

12 COMPETITIVE LANDSCAPE

12.1 INTRODUCTION

12.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

12.3 MARKET SHARE ANALYSIS

12.4 PRODUCT/BRAND COMPARISON

12.4.1 HEWLETT-PACKARD ENTERPRISE (HPE)

12.4.2 AMAZON WEB SERVICES (AWS)

12.4.3 DELL TECHNOLOGIES

12.4.4 CISCO

12.4.5 MICROSOFT

12.5 REVENUE ANALYSIS

12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.6.1 STARS

12.6.2 EMERGING LEADERS

12.6.3 PERVASIVE PLAYERS

12.6.4 PARTICIPANTS

12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024