동물 감염병 진단 시장 : 제품별, 기술별, 동물 유형별, 최종 사용자별, 지역별 예측(-2030년)

Veterinary Infectious Disease Diagnostics Market by Product (Consumables, Instruments), Technology (Molecular Diagnostic, PCR, ELISA, Immunodiagnostics, Rapid Tests), Animal Type (Companion Animal, Livestock), End User & Region - Global Forecast to 2030

상품코드:1793324

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 548 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

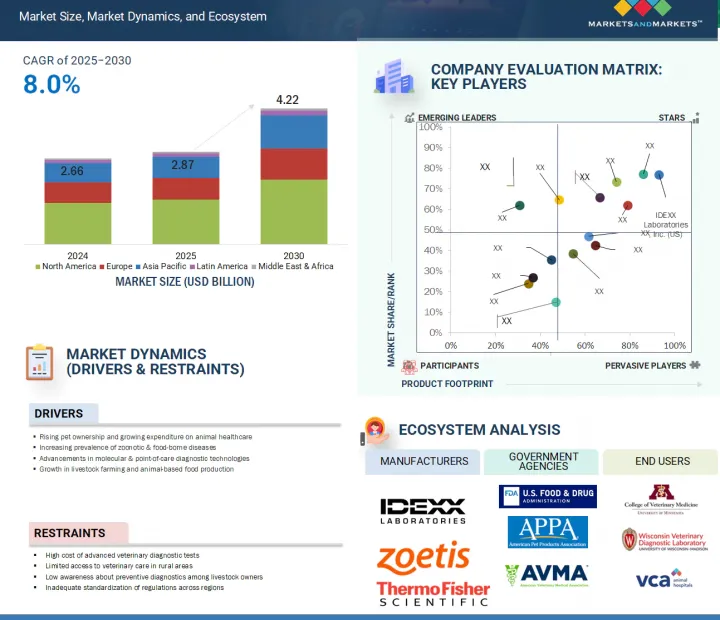

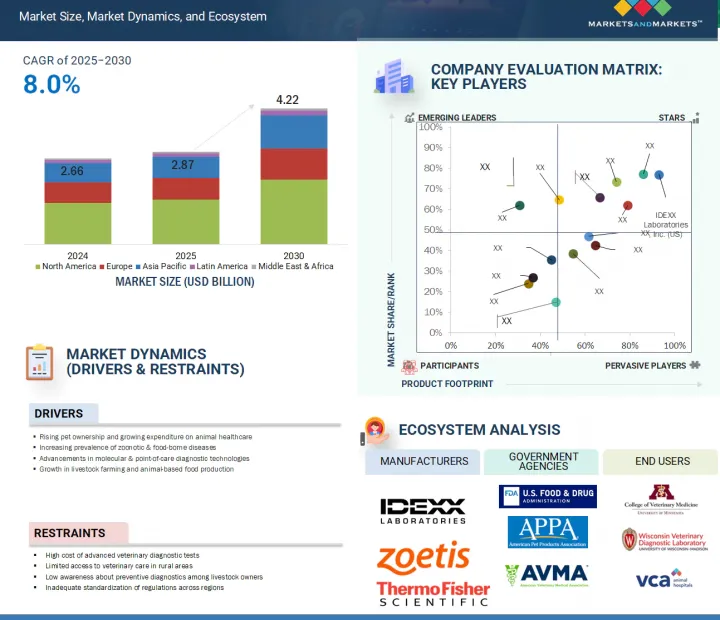

동물 감염병 진단 시장 규모는 2025년 28억 7,000만 달러에서 2030년에는 42억 2,000만 달러에 이를 것으로 예측되며, CAGR 8.0%의 성장이 전망됩니다.

이 성장은 동물 건강 및 질병 관리 분야의 변화하는 미래를 반영하는 여러 중요한 요인에 의해 촉진되고 있습니다.

조사 범위

조사 대상 연도

2024-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문별

제품별, 기술별, 동물 유형별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

주요 촉진 요인 중 하나는 반려동물과 가축 모두에서 감염병의 부담이 증가함에 따라 신속하고 신뢰할 수 있으며 현장 전개가 가능한 진단 솔루션에 대한 수요가 높아지고 있다는 점입니다. 조류 인플루엔자, 레프토스피라증, 브루셀라증 등 질병의 발생 증가로 인해 수의사 및 동물 사육자들은 위험을 완화하기 위해 조기 및 정확한 검출을 우선순위로 삼고 있습니다.

또 다른 중요한 요인은 예방적 수의학으로의 전환입니다. 반려동물 소유자와 가축 관리자의 인식이 높아지면서 감염이 악화되기 전에 감염을 조기에 발견하기 위한 정기 검진과 건강 모니터링에 대한 강조가 강화되고 있습니다. 이 동향은 인수공통 감염병의 전파와 관련된 경제적 및 퍼블릭 보건적 영향에 대한 인식이 증가함에 따라 더욱 강화되고 있습니다.

반려동물 세분화은 특히 도시 지역의 고소득 가구에서 반려동물 사육이 증가함에 따라 동물 감염병 진단 시장에서 가장 높은 성장이 예상됩니다. 반려동물의 주인은 인류 공통 감염에 대한 의식 증가와 조기 발견의 중요성으로부터 건강 진단 및 진단 서비스에 대한 투자에 적극적입니다. 게다가, 포인트 오브 케어와 재택 진단 도구의 기술 혁신은 반려동물 주인과 수의사 모두에게 접근성을 향상시킵니다. 동물 병원을 방문하는 빈도가 증가하고 반려동물의 건강 관리 지출이 증가하고 있기 때문에이 분야는 시장 급성장이 예측됩니다.

2024년 면역진단 부문은 비용 효율성과 높은 정확성으로 인해 동물 감염병 진단 시장에서 주도적인 위치를 차지했습니다. ELISA와 측면 유동 검사(lateral flow assays)와 같은 기술은 반려동물과 가축에서 다양한 감염병을 검출하는 데 널리 사용됩니다. 이러한 검사는 빠른 결과 제공, 사용 편의성, 최소한의 장비 요구사항으로 인해 수의사 클리닉과 현장 사용에 이상적입니다. 특정 항원이나 항체를 검출할 수 있는 능력은 조기 진단과 효과적인 질병 관리를 가능하게 하여 대규모 인구 검진 및 정기 감시 프로그램에 유용합니다.

아시아태평양 지역은 인구 통계적, 경제적, 의료적 요인으로 인해 동물 감염병 진단 시장 성장률이 가장 높을 것으로 예상됩니다. 해당 지역의 대규모 가축 인구는 발굽구진병과 조류 인플루엔자 등 증가하는 감염병에 대응하기 위한 정확한 진단 수요를 촉진하고 있습니다. 또한 중국과 인도 도시 지역에서 반려동물 수가 증가함에 따라 수의학 의료 지출이 확대되고 있습니다. 강화된 수의학 인프라, 인수공통 감염병 위협에 대한 인식 향상, 동물 건강에 대한 투자도 시장 성장에 기여하고 있습니다. 기업들은 고급 진단 기술에 대한 접근성을 개선하기 위해 해당 지역의 존재감을 확대하고 있습니다.

본 보고서에서는 세계의 동물 감염병 진단 시장에 대해 조사했으며, 제품별, 기술별, 동물 유형별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

시장 역학

업계 동향

기술 분석

Porter's Five Forces 분석

규제 분석

특허 분석

무역 분석

가격 분석

상환 분석

주된 회의 및 이벤트(2025-2026년)

주요 이해관계자와 구매 기준

최종 사용자의 시점과 미충족 요구

동물 감염병 진단 시장에 있어서의 AI의 영향

생태계 분석

밸류체인 분석

공급망 분석

인접 시장 분석

투자 및 자금조달 시나리오

미국 관세의 영향 및 동물 감염병 진단 시장에 미치는 영향(2025년)

제6장 동물 감염병 진단 시장(제품별)

소개

소모품

장비

제7장 동물 감염병 진단 시장(기술별)

소개

면역 진단

분자 진단

기타

제8장 동물 감염병 진단 시장(동물 유형별)

소개

반려동물

가축

제9장 동물 감염병 진단 시장(최종 사용자별)

소개

수의학 참고 실험실

동물병원 및 클리닉

현장 진단/내부 검사

수의학 연구 기관 및 대학

제10장 동물 감염병 진단 시장(지역별)

소개

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시 경제 전망

독일

영국

프랑스

이탈리아

스페인

네덜란드

기타

아시아태평양

아시아태평양의 거시 경제 전망

중국

일본

인도

호주

한국

뉴질랜드

베트남

기타

라틴아메리카

라틴아메리카의 거시 경제 전망

브라질

멕시코

기타

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타

제11장 경쟁 구도

개요

주요 진입기업의 전략 및 강점

수익 분석(2020-2024년)

시장 점유율 분석(2024년)

기업평가 매트릭스 : 주요 진출기업(2024년)

기업평가 매트릭스 : 스타트업/중소기업(2024년)

브랜드/제품 비교

주요 기업의 연구 개발비

기업평가와 재무지표

경쟁 시나리오

제12장 기업 프로파일

주요 진출기업

IDEXX LABORATORIES, INC.

ZOETIS SERVICES LLC

THERMO FISHER SCIENTIFIC INC.

VIRBAC

BIOMERIEUX

ANTECH DIAGNOSTICS, INC.

INNOVATIVE DIAGNOSTICS

NEOGEN CORPORATION

INDICAL BIOSCIENCE GMBH

AGROLABO SPA

BIONOTE

BIOGAL

BIOCHEK

MEGACOR DIAGNOSTIK GMBH

BIO-RAD LABORATORIES, INC.

기타 기업

FASSISI, GMBH

BIOTANGENTS LIMITED

SKYER, INC.

BIOPANDA REAGENTS LTD.

SHENZHEN BIOEASY BIOTECHNOLOGY, INC.

GOLD STANDARD DIAGNOSTICS

BIO-X DIAGNOSTICS SA

DEMEDITEC DIAGNOSTICS GMBH

EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG

BIOSTONE ANIMAL HEALTH

제13장 부록

HBR

영문 목차

영문목차

The veterinary infectious disease diagnostics market is expected to grow from USD 2.87 billion in 2025 to USD 4.22 billion by 2030, at a CAGR of 8.0%. This growth is driven by several important factors that reflect the changing landscape of animal health and disease management.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

By Product, Technology, Animal Type, End User, Region

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

One primary driver is the increasing burden of infectious diseases among both companion animals and livestock, which has heightened the need for rapid, reliable, and field-deployable diagnostic solutions. The rise in outbreaks of diseases such as avian influenza, leptospirosis, and brucellosis is leading veterinarians and animal producers to prioritize early and accurate detection to mitigate risks.

Another significant factor is the shift towards preventive veterinary care. As awareness grows among pet owners and livestock handlers, there is a stronger emphasis on routine screenings and health monitoring to identify infections before they escalate. This trend is also supported by a growing recognition of the economic and public health consequences associated with the transmission of zoonotic diseases.

"By animal type, the companion animals segment is projected to grow at the highest CAGR during the forecast period."

The companion animals segment is expected to see the highest growth in the veterinary infectious disease diagnostics market, driven by increasing pet ownership, especially in urban high-income households. Pet owners are more willing to invest in health check-ups and diagnostic services due to the growing awareness of zoonotic diseases and the importance of early detection. Additionally, innovations in point-of-care and home-based diagnostic tools enhance access for both pet owners and veterinarians. With more frequent visits to veterinary clinics and rising healthcare spending for pets, this segment is projected for rapid growth in the market.

"By technology, the immunodiagnostics segment accounted for the largest market share in 2024."

In 2024, the immunodiagnostics segment dominated the veterinary infectious disease diagnostics market due to its cost-effectiveness and high accuracy. Techniques like ELISA and lateral flow assays are commonly used to detect various infectious diseases in companion and livestock animals. These tests provide rapid results, are user-friendly, and require minimal equipment, making them ideal for veterinary clinics and field use. Their ability to detect specific antigens or antibodies enables early diagnosis and effective disease management, making them valuable for large population screenings and routine surveillance programs.

"The Asia Pacific region is expected to witness the highest growth rate during the forecast period."

The Asia Pacific is set to experience the highest growth in the veterinary infectious disease diagnostics market due to various demographic, economic, and healthcare factors. The region's large livestock population drives the demand for accurate diagnostics to address rising infectious diseases like foot-and-mouth disease and avian influenza. Additionally, the increasing number of companion animals, especially in urban areas of China and India, is boosting veterinary healthcare spending. Enhanced veterinary infrastructure, heightened awareness of zoonotic threats, and investments in animal health are also contributing to market growth. Companies are expanding their presence in the region to improve access to advanced diagnostic technologies.

Breakdown of supply-side primary interviews:

By Company Type: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

By Designation: C-level Executives (35%), Directors (25%), and Other Designations (40%)

By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

By End User: Veterinary Reference Laboratories (40%), Veterinary Hospitals & Clinics (25%), POC/In-house Testing (20%), and Veterinary Research Institutes & Universities (15%)

By Designation: Veterinary Healthcare Professionals (35%), Department Heads (27%), Procurement Heads (22%), and Other Designations (16%)

By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Research Coverage

The market study covers the veterinary infectious disease diagnostics market in various segments. It aims to estimate the market size and growth potential of this market by product, technology, animal type, end user, and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can assist established companies and newer or smaller firms in understanding market trends, enabling them to capture a larger market share. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

Analysis of key drivers (growth in companion animal population, increasing demand for animal-derived food products, growing concerns about infectious zoonotic diseases, rising demand for pet insurance and growing animal health expenditures, increasing number of veterinary practitioners and rising income levels in developed markets, and growing focus on disease control and prevention measures), restraints (rising pet care costs and high cost of veterinary diagnostic tests), opportunities (growth potential of emerging economies and integration of AI and ML), and challenges (low animal healthcare awareness in emerging countries and shortage of veterinary practitioners in emerging economies) influencing the growth of the veterinary infectious disease diagnostics market.

Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product launches in the veterinary infectious disease diagnostics market.

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of veterinary infectious disease diagnostic products across regions.

Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary infectious disease diagnostics market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary infectious disease diagnostics market.