Data Center Solutions Market by Infrastructure (IT, Power, Cooling ), Rack, Software - Forecast to 2030

상품코드:1793322

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 491 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

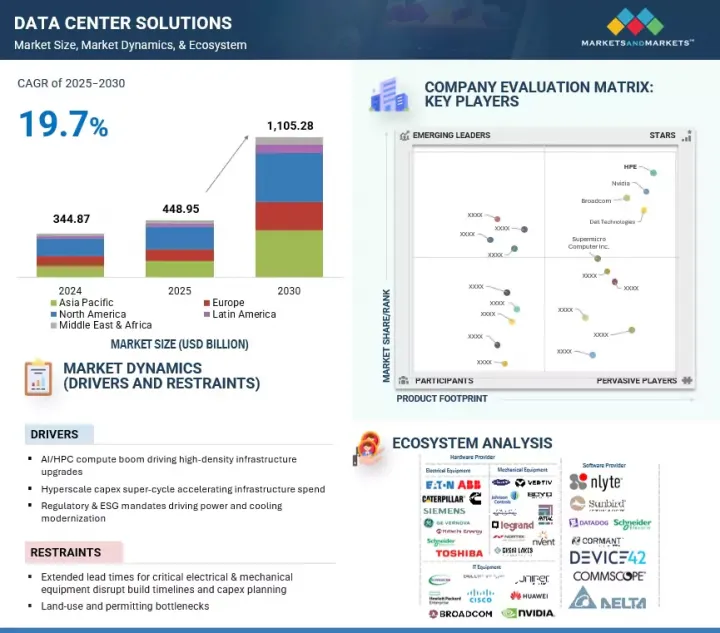

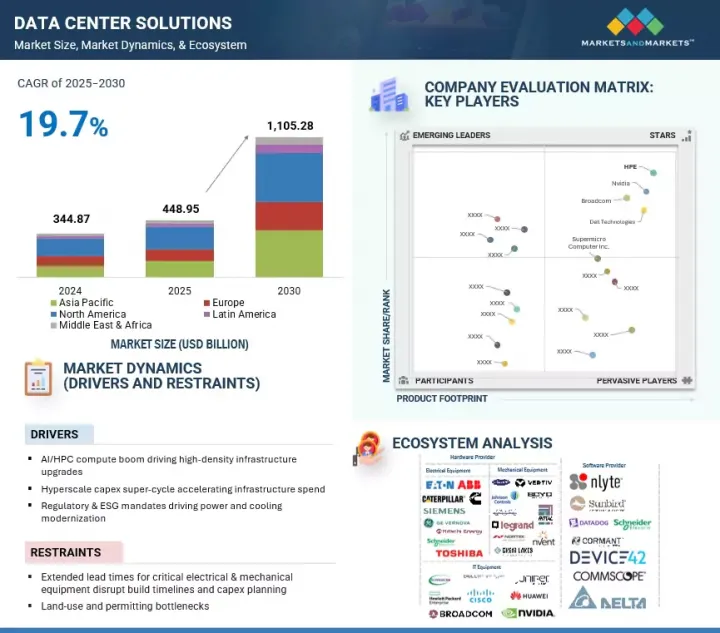

세계 데이터센터 솔루션 시장은 급속히 확대되고 있으며 시장 규모는 2025년 약 4,489억 5,000만 달러, 예측 기간 동안 CAGR 19.7%로 성장하고, 2030년에는 1조 1,052억 8,000만 달러로 확대될 것으로 예측되고 있습니다.

조사 범위

대상 연도

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

달러

부문

구성요소, 워크로드 유형, 티어 유형, 데이터센터 규모, 데이터센터 유형, 산업

대상 지역

북미, 유럽, 아시아태평양, 중동, 아프리카, 라틴아메리카

주요 성장 요인은 AI와 고성능 컴퓨팅(HPC) 워크로드의 급증으로 고밀도 인프라로의 대규모 업그레이드를 촉진하고 있습니다. 이를 더욱 뒷받침하고 있는 것은 주요 클라우드 및 디지털 플랫폼이 증가하는 용량 수요에 대응하기 위해 인프라 투자를 가속화하는 '하이퍼스케일 설비 투자의 슈퍼 사이클'입니다. 또한 규제 요건과 환경, 사회, 거버넌스(ESG)의 의무 강화로 전력 및 냉각 시스템의 대폭적인 현대화가 진행되고 있으며, 에너지 절약과 지속가능성이 강조되고 있습니다.

"산업별로는 헬스케어 생명과학 부문이 예측기간 중 가장 높은 성장률을 보여줄 전망"

이는 의료기관이 전자 의료진의 급속한 도입, 첨단 영상 진단, 유전체 연구, AI 진단을 진행하고 있으며, 데이터 양과 처리 수요가 급증하고 있기 때문입니다. 공급업체와 솔루션 제공업체의 경우 대규모 파일 처리, 실시간 분석 및 안전한 데이터 공유를 가능하게 하는 고성능, 견고하고 규제 준수 인프라 수요가 증가하고 있습니다. 병원, 연구소, 클리닉은 확장 가능한 랙, 중복 전원 공급 장치 및 고급 냉각 메커니즘을 갖춘 하이브리드 및 On-Premise 환경으로 전환하여 지속적인 가동을 보장합니다.

규제 요구 사항은 물리적 보안, 액세스 제어 및 내결함성 시스템에 대한 투자를 촉진하는 반면, 소프트웨어 정의 모니터링 및 자동화 도구는 복잡하고 분산된 워크플로우 관리를 지원합니다. 개인화된 의료 및 데이터 중심 진단이 확대됨에 따라 의료 제공업체는 고급 분석, 효율적인 스토리지 및 신뢰할 수 있는 재해 복구를 통합하는 솔루션을 찾고 있습니다. 벤더에게 이 부서는 모듈형, 안전하고 규제 준수 데이터센터 플랫폼을 제공하는 선호기이며 혁신성, 규제 준수, 미래 대응형 인프라라는 업계의 절실한 요구에 부합하고 있습니다.

"지역별로는 북미가 최대 시장 점유율을 차지하고 아시아태평양이 예측 기간 동안 가장 빠른 성장을 기록할 전망"

북미는 첨단 디지털 인프라, 강력한 클라우드 수요, 하이퍼스케일러 및 기업의 지속적인 투자에 힘입어 데이터센터 솔루션 시장을 선도하고 있습니다. 2025년 4월에는 Meta가 와이오밍 주에 8억 달러 규모의 하이퍼스케일 데이터센터를 발표했습니다. 이 시설은 신재생에너지 통합과 첨단 냉각기구를 갖추고 있어 증가하는 AI 및 클라우드 워크로드에 대응하는 설계로 되어 있습니다. 이는 버지니아, 달라스, 피닉스를 중심으로 한 지역의 확장 가능하고 지속 가능한 인프라에 대한 주력을 반영합니다. 반면 아시아태평양은 가장 빠르게 성장하고 있으며, 급속한 디지털 보급, 클라우드 및 5G 확대, 정부 주도 지역 인프라, 신재생에너지, 기술 인재 육성의 추진에 의해 지원되고 있습니다.

본 보고서에서는 세계 데이터센터 솔루션 시장을 조사했으며, 시장 개요, 시장 성장 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례연구, 시장 규모 추이와 예측, 각종 구분 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요와 업계 동향

시장 역학

성장 촉진요인

억제요인

기회

과제

사례 연구 분석

생태계 분석

공급망 분석

가격 분석

특허 분석

무역 분석

기술 분석

규제 상황

Porter's Five Forces 분석

구매 프로세스의 주요 이해관계자

2025년 주요 컨퍼런스 및 이벤트

고객의 사업에 영향을 미치는 동향/혼란

비즈니스 모델 분석

투자 및 자금조달 시나리오

데이터센터 솔루션 시장에서의 AI/생성형 AI의 영향

2025년 미국 관세 데이터센터 솔루션 시장에 미치는 영향

제6장 데이터센터 솔루션 시장 : 구성요소별

인프라

데이터센터 IT 인프라

데이터센터 전원 인프라

데이터센터 랙 및 인클로저

데이터센터 냉각 인프라

소프트웨어

DCIM 소프트웨어

빌딩/시설 관리 소프트웨어

가상화 및 오케스트레이션 소프트웨어

컴플라이언스 및 보안 소프트웨어

분석 및 AIOPS 소프트웨어

제7장 데이터센터 솔루션 시장 : 워크로드 유형별

HPC 및 AI

범용 IT

제8장 데이터센터 솔루션 시장 : 티어 유형별

Tier 1

Tier 2

Tier 3

Tier 4

제9장 데이터센터 솔루션 시장 : 데이터센터 규모별

소규모 데이터센터

중규모 데이터센터

대규모 데이터센터

제10장 데이터센터 솔루션 시장 : 데이터센터 유형별

하이퍼스케일 데이터센터

코로케이션 데이터센터

엔터프라이즈 데이터센터

제11장 데이터센터 솔루션 시장 : 산업별

은행, 금융서비스 및 보험(BFSI)

IT 및 통신

정부 및 공공 부문

헬스케어 & 생명과학

물류 및 운송

소매 및 E커머스

제조

에너지 및 유틸리티

기타

제12장 데이터센터 솔루션 시장 : 지역별

북미

거시경제 전망

시장 성장 촉진요인

미국

캐나다

유럽

거시경제 전망

시장 성장 촉진요인

영국

독일

프랑스

이탈리아

스페인

기타

아시아태평양

거시경제 전망

시장 성장 촉진요인

중국

일본

인도

기타

중동 및 아프리카

거시경제 전망

시장 성장 촉진요인

GCC 국가

남아프리카

기타

라틴아메리카

거시경제 전망

시장 성장 촉진요인

브라질

멕시코

기타

제13장 경쟁 구도

주요 기업의 전략/유력 기업

수익 분석

시장 점유율 분석

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 스타트업/중소기업

주요 벤더의 기업 평가 및 재무 지표

경쟁 시나리오와 동향

제14장 기업 프로파일

주요 기업

DELL TECHNOLOGIES

HPE

BROADCOM

NVIDIA

SUPERMICRO COMPUTER INC.

IBM

LENOVO

SCHNEIDER ELECTRIC

CISCO

HUAWEI

DDC SOLUTIONS

기타 기업

WESTERN DIGITAL

VERTIV

ARISTA NETWORKS

NETAPP

PURE STORAGE

EATON

RITTAL

CUMMINS

CATERPILLAR

GENERAL ELECTRIC(GE VERNOVA)

ABB

DELTA ELECTRONICS

SIEMENS

FUJITSU

SUNBIRD

LEGRAND

MODINE

STULZ

스타트업 및 SME

CHATSWORTH PRODUCTS

DEVICE42

COOLIT SYSTEM

SUBMER

ACTIVE POWER

GREEN REVOLUTION COOLING

RIELLO UPS

제15장 인접 시장과 관련 시장

제16장 부록

SHW

영문 목차

영문목차

The global data center solutions market is expanding rapidly, with a projected market size anticipated to rise from about USD 448.95 billion in 2025 to USD 1,105.28 billion by 2030, featuring a CAGR of 19.7%.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

USD Billion

Segments

Component, workload type, tier type, data center size, data center type, enterprise verticals

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, Latin America

The key drivers include the surge in AI and high-performance computing (HPC) workloads, which are leading to widespread upgrades to high-density infrastructure. This is further supported by a hyperscale capex super-cycle, as major cloud and digital platforms accelerate infrastructure spending to meet increasing capacity demands. Regulatory requirements and increasing environmental, social, and governance (ESG) mandates are driving significant modernization in power and cooling systems, emphasizing energy efficiency and sustainability.

In contrast, market restraints involve extended lead times for critical electrical and mechanical equipment, which can disrupt construction schedules and capex planning. Furthermore, land-use restrictions and permitting bottlenecks present challenges, often causing delays in site selection and data center development. These drivers and restraints shape the pace and direction of growth, investment, and innovation across the data center solutions sector.

"Healthcare & Life Sciences segment will account for the fastest growth rate during the forecast period"

The Healthcare & Life Sciences vertical is expected to record the fastest growth rate in the data center solutions market over the forecast period because healthcare organizations are rapidly adopting digital patient records, advanced imaging, genomics research, and AI diagnostics, creating a surge in data volume and processing demands. For vendors and solution providers, there is an increasing demand for high-performance, resilient, and compliant infrastructure that can manage large file processing, real-time analytics, and secure data sharing. Hospitals, research labs, and clinics are moving toward hybrid and on-premises environments with scalable racks, redundant power, and advanced cooling to maintain continuous operations.

Regulatory requirements drive investment in physical security, access control, and fault-tolerant systems, while software-defined monitoring and automation tools help manage complex, distributed workflows. As personalized medicine and data-driven diagnostics expand, providers are seeking solutions that integrate advanced analytics, efficient storage, and reliable disaster recovery. For vendors, this sector presents opportunities to deliver modular, secure, and compliant data center platforms that support current and emerging healthcare workloads, aligning with the industry's pressing need for innovation, compliance, and future-ready infrastructure.

"Tier 3 type to hold the largest market share during the forecast period"

Tier 3 facilities are expected to hold the largest market share during the forecast period, reflecting their position as the preferred choice for enterprise and cloud environments that require high availability and efficiency. These data centers deliver concurrently maintainable infrastructure with 99.982% uptime, N+1 redundancy for power and cooling, dual power paths, and fully monitored distribution systems. This level of reliability meets the needs of enterprises running mission-critical workloads while avoiding the added complexity and cost of Tier 4 designs. For vendors and solution providers, this presents a strong opportunity to deliver modular, scalable, and Tier 3-compliant infrastructure that supports the growing demand for predictable uptime and operational resilience.

Common hardware configurations in Tier 3 environments include redundant UPS and battery energy storage systems, medium to high-density server racks, and cooling systems such as CRAH units with water-cooled chillers. On the software side, platforms such as DCIM combined with EPMS and BMS provide visibility for capacity planning and automated incident response. As more organizations adopt hybrid models and compliance-ready infrastructure, solutions that balance performance, cost efficiency, and reliability will be critical, putting Tier 3 facilities at the center of future data center deployment strategies.

"North America is expected to hold the largest market share, while Asia Pacific will record the fastest growth during the forecast period"

North America leads the data center solutions market, supported by advanced digital infrastructure, strong cloud demand, and sustained investment from hyperscalers and enterprises. In April 2025, Meta announced a USD 800 million hyperscale data center in Wyoming, designed with renewable energy integration and advanced cooling to meet rising AI and cloud workloads. This reflects the regional focus on scalable, sustainable infrastructure across Virginia, Dallas, and Phoenix. Meanwhile, Asia Pacific is the fastest-growing region, driven by rapid digital adoption, cloud and 5G expansion, and government-backed initiatives supporting local infrastructure, renewable energy, and tech workforce development.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the data center solutions market.

By Company: Tier I - 30%, Tier II - 45%, and Tier III - 25%

By Designation: C-Level Executives - 50%, D-Level Executives -35%, and others - 15%

By Region: North America - 50%, Europe - 30%, Asia Pacific - 15%, and Rest of the world - 5%

The report includes a study of key players offering data center solutions. It profiles major vendors in the data center solutions market. These include Dell Technologies (US), Broadcom (US), Nvidia (US), HPE (US), Supermicro Computer Inc. (US), Lenovo (China), Schneider Electric (France), Huawei (China), IBM (US), Cisco (US), Vertiv (US), VMware (US), Eaton (Ireland), Western Digital (US), Siemens (Germany), DDC Solutions (US), Palo Alto Network (US), ABB (Switzerland), Arista (US), Nutanix (US), Pure Storage (US), Daikin (Japan), Rittal (Germany), 3M (US), Coolit Systems (Canada), and Delta Electronics (Taiwan).

Research Coverage

This research report categorizes the data center solutions market based on Component (Infrastructure (Data Center IT Infrastructure, Data Center Racks & Enclosure, Data Center Cooling Infrastructure), Software (DCIM Software, Building/Facility Management Software, Virtualization & Orchestration Software, Compliance & Security Software, Analytics & AIOps Software)), Workload Type (HPC & AI, General Purpose IT), Tier Type (Tier 1, Tier 2, Tier 3, Tier 4), Data Center Size (Small Data Centers, Medium-Sized Data Centers, Large Data Centers), Data Center Type (Hyperscale Data Center, Colocation Data Center, Enterprise Data Center), Enterprise Verticals (Banking, Financial Services, & Insurance (BFSI), IT & Telecom, Government & Public Sector, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Logistics & Transportation, Energy & Utilities, Other Verticals (Education, Media & Entertainment)), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the data center solutions market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers and acquisitions; and recent developments associated with the data center solutions market. Competitive analysis of upcoming startups in the data center solutions market ecosystem was also covered in this report.

Reasons to buy this Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall data center solutions market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (AI/HPC compute boom driving high-density infrastructure, Hyperscale capex super-cycle, accelerating infrastructure speed, regulatory and ESG mandates driving power and cooling modernization), restraints (Extended lead times for critical electrical & mechanical equipment disrupt building timelines & capex planning, Land-use & permitting bottlenecks), opportunities (Retrofitting legacy data centers to meet AI-driven density demands, Rise of liquid cooling in AI-driven data center infrastructure), and challenges (Skilled labour shortage, Grid capacity & power scarcity)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the data center solutions market

Market Development: Comprehensive information about lucrative markets - analysis of the data center solutions market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the data center solutions market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such Dell Technologies (US), Broadcom (US), Nvidia (US), HPE (US), Supermicro Computer Inc. (US), Lenovo (China), Schneider Electric (France), Huawei (China), IBM (US), Cisco (US), Vertiv (US), VMware (US), Eaton (Ireland), Western Digital (US), Siemens (Germany), DDC Solutions (US), Palo Alto Network (US), ABB (Switzerland), Arista (US), Nutanix (US), Pure Storage (US), Daikin (Japan), Rittal (Germany), 3M (US), Coolit Systems (Canada), and Delta Electronics (Taiwan).

The report also helps stakeholders understand the pulse of the data center solutions market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Breakup of primary profiles

2.1.2.3 Key industry insights

2.2 MARKET BREAKUP AND DATA TRIANGULATION

2.3 MARKET SIZE ESTIMATION

2.4 MARKET FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER SOLUTIONS MARKET

4.2 DATA CENTER SOLUTIONS MARKET, BY COMPONENT

4.3 DATA CENTER SOLUTIONS MARKET, BY WORKLOAD TYPE

4.4 DATA CENTER SOLUTIONS MARKET, BY DATA CENTER SIZE

4.5 DATA CENTER SOLUTIONS MARKET, BY TIER TYPE

4.6 DATA CENTER SOLUTIONS MARKET, BY DATA CENTER TYPE

4.7 DATA CENTER SOLUTIONS MARKET, BY ENTERPRISE VERTICALS

4.8 DATA CENTER SOLUTIONS MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 AI/HPC compute boom to drive high-density infrastructure upgrades

5.2.1.2 Hyperscale Capex super-cycle to accelerate infrastructure spend

5.2.1.3 Regulatory & ESG mandates to drive power and cooling modernization

5.2.2 RESTRAINTS

5.2.2.1 Extended lead times for critical electrical & mechanical equipment to disrupt build timelines and capex planning

5.2.2.2 Land use and permitting bottlenecks to affect equipment lead times

5.2.3 OPPORTUNITIES

5.2.3.1 Retrofitting legacy data centers to meet AI-driven density demands

5.2.3.2 Rise of liquid cooling in AI-driven data center infrastructure to meet next-gen density requirements

5.2.4 CHALLENGES

5.2.4.1 Skilled labor shortage to threaten project delivery timelines and long-term operational efficiency

5.2.4.2 Grid capacity & power scarcity to limit facility deployment

5.3 CASE STUDY ANALYSIS

5.3.1 CASE STUDY 1: EATON ENHANCES POWER RESILIENCE AND IT UPTIME FOR UNIVERSITY OF WINCHESTER

5.3.2 CASE STUDY 2: OXIGEN INTEGRATES VERTIV'S FREE COOLING AND ENERGY-SAVING TECHNOLOGY INTO ITS NEW HIGH-PERFORMANCE DATA CENTER

5.3.3 CASE STUDY 3: STULZ DELIVERS REDUNDANT, ENERGY-EFFICIENT COOLING FOR DEUTSCHE BAHN'S BATTERY TRAIN CHARGING SUBSTATION

5.3.4 CASE STUDY 4: ED NETZE DEPLOYS A NEXT-GEN SUBSTATION WITH PURE AIR MV SWITCHGEAR

5.3.5 CASE STUDY 5: CAT POWER SYSTEMS DRIVE LONG-TERM UPTIME FOR SCOTT DATA CENTER

5.4 ECOSYSTEM ANALYSIS

5.5 SUPPLY CHAIN ANALYSIS

5.6 PRICING ANALYSIS

5.6.1 INDICATIVE PRICING OF DATA CENTER UPS, BY REGION, 2024

5.6.2 INDICATIVE PRICING OF DATA-CENTER UPS FOR HYPERSCALE DEPLOYMENTS, 2024

5.7 PATENT ANALYSIS

5.7.1 LIST OF MAJOR PATENTS

5.8 TRADE ANALYSIS

5.8.1 EXPORT SCENARIO FOR HS CODE 8471

5.8.2 IMPORT SCENARIO FOR HS CODE 8471

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGY

5.9.1.1 Direct-to-Chip Cooling

5.9.1.2 Remote monitoring and data center infrastructure management

5.9.1.3 AIOps & Digital Twins

5.9.1.4 High-density GPUs

5.9.2 COMPLIMENTARY TECHNOLOGY

5.9.2.1 Lithium-ion & next-gen battery energy storage UPS

7.1.1 WORKLOAD TYPE: DATA CENTER SOLUTIONS MARKET DRIVERS

7.2 HPC & AI

7.2.1 SCALING DATA CENTER INFRASTRUCTURE TO SUPPORT AI MODEL TRAINING, HIGH-DENSITY GPU RACKS, AND LIQUID COOLING NEEDS

7.3 GENERAL-PURPOSE IT

7.3.1 OPTIMIZING MODULAR INFRASTRUCTURE AND ORCHESTRATION TOOLS TO SUPPORT DISTRIBUTED, COST-EFFICIENT GENERAL PURPOSE IT WORKLOADS

8 DATA CENTER SOLUTIONS MARKET, BY TIER TYPE

8.1 INTRODUCTION

8.1.1 TIER TYPE: DATA CENTER SOLUTIONS MARKET DRIVERS

8.2 TIER 1

8.2.1 DEPLOYING TIER 1 SITES FOR COST-EFFECTIVE, LOW-RISK IT LOADS

8.3 TIER 2

8.3.1 EXPANDING REGIONAL PRESENCE THROUGH MODULAR TIER 2 INFRASTRUCTURE

8.4 TIER 3

8.4.1 STANDARDIZING ENTERPRISE OPERATIONS WITH SCALABLE TIER 3 SYSTEMS

8.5 TIER 4

8.5.1 ENABLING FAULT-TOLERANT AI AND FINANCE WORKLOADS VIA TIER 4

9 DATA CENTER SOLUTIONS MARKET, BY DATA CENTER SIZE

9.1 INTRODUCTION

9.1.1 DATA CENTER SIZE: DATA CENTER SOLUTIONS MARKET DRIVERS

9.2 SMALL DATA CENTERS

9.2.1 POWERING LOCALIZED, LOW-LATENCY EDGE DEPLOYMENTS WITH MODULAR, COST-EFFICIENT, AND COMPACT INFRASTRUCTURE SOLUTIONS

9.3 MEDIUM DATA CENTER

9.3.1 BRIDGING EDGE AND CORE WITH SCALABLE, ENERGY-EFFICIENT SOLUTIONS FOR HYBRID IT AND REGIONAL CLOUD EXPANSION

9.4 LARGE DATA CENTERS

9.4.1 ENABLING SCALABLE, HIGH-DENSITY INFRASTRUCTURE FOR AI, CLOUD, AND ENTERPRISE WORKLOADS IN MISSION-CRITICAL GLOBAL FACILITIES

10 DATA CENTER SOLUTIONS MARKET, BY DATA CENTER TYPE

10.1 INTRODUCTION

10.1.1 DATA CENTER TYPE: DATA CENTER SOLUTIONS MARKET DRIVERS

10.2 HYPERSCALE DATA CENTER

10.2.1 POWERING GLOBAL AI AND CLOUD INFRASTRUCTURE WITH ULTRA-SCALABLE AND ENERGY-EFFICIENT HYPERSCALE DATA CENTER SOLUTIONS

10.3 COLOCATION DATA CENTER

10.3.1 ENABLING MULTI-TENANT DIGITAL INFRASTRUCTURE THROUGH MODULAR HARDWARE, INTELLIGENT NETWORKING, AND SUSTAINABLE OPERATIONS IN COLOCATION FACILITIES

10.4 ENTERPRISE DATA CENTER

10.4.1 MODERNIZING LEGACY IT THROUGH MODULAR INFRASTRUCTURE, HYBRID CLOUD ORCHESTRATION, AND OPEN-SOURCE TOOLS IN ENTERPRISE DATA CENTERS

11 DATA CENTER SOLUTIONS MARKET, BY ENTERPRISE VERTICALS

11.1 INTRODUCTION

11.1.1 ENTERPRISE VERTICALS: DATA CENTER SOLUTIONS MARKET DRIVERS