의약품용 금속 감지기 시장 : 제품별, 기술별, 용도별, 최종 사용자별, 지역별 예측(-2030년)

Pharmaceutical Metal Detector Market by Product, Technology, and Application - Global Forecast to 2030

상품코드:1786130

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 247 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

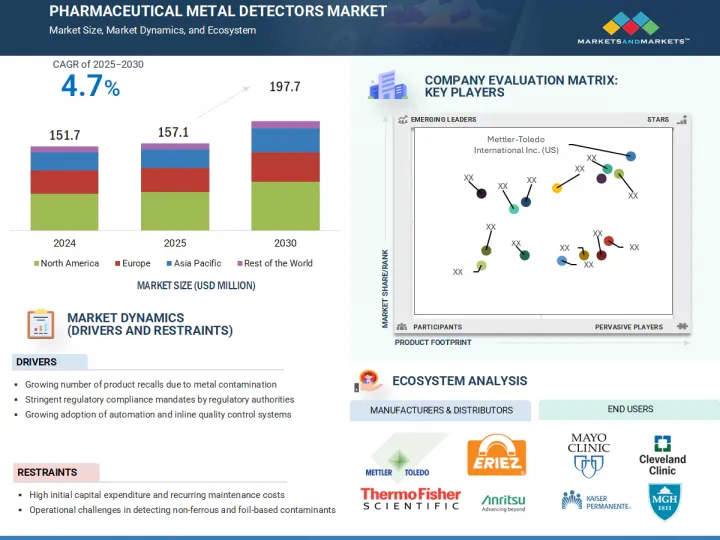

세계의 의약품용 금속 감지기 시장 규모는 2025년 1억 5,710만 달러에서 2030년에는 1억 9,770만 달러에 이를 전망이며, 예측 기간 중 CAGR 4.7%로 성장할 것으로 예측됩니다.

성장의 주요 원인은 제품 안전에 대한 엄격한 규제 요건과 오염이 없는 의약품에 대한 수요 증가입니다. 제품 리콜 사례 및 품질과 관련된 우려가 증가함에 따라 제조업체는 고급 감지 기술을 채택해야 합니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러)

부문

제품별, 기술별, 용도별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

자동화된 지능형 금속 감지 시스템의 통합이 진행됨에 따라 센서 감도와 실시간 모니터링 기술 혁신과 함께 시장 확대가 더욱 기대되고 있습니다. 또한 GMP 및 FDA 기준을 준수하는 데 중점을 둔 제약 회사는 고정밀 검사 장비에 대한 투자를 촉진하고 있습니다. 게다가 업계 각사는 경쟁력을 강화하고 프로세스의 신뢰성을 확보하기 위해 제품 혁신 및 전략적 제휴에 임하는 경향이 강해지고 있습니다.

정제용 금속 감지기는 2024년에 의약품 금속 감지기 시장을 독점했는데, 이는 주로 세계 제약 업계 전체에서 정제가 널리 생산되고 있기 때문입니다. 정제는 편의성, 긴 보존 기간 및 환자의 컴플라이언스로부터 여전히 가장 선호되고 일반적으로 제조되는 고체 투여 형태입니다. 정제용 금속 감지기는 통합의 용이성, 비용 효율성, 신뢰성이 높기 때문에 주요 제약 제조업체와 수탁 제조 기관(CMO) 모두에서 널리 채택되었습니다. 세계의 의약품 수요 증가 및 품질 관리의 엄격화로 정제 금속 감지기의 사용은 계속 확대되고 있으며, 이 시장에서 주요 제품 유형으로서의 지위를 확고하게 하고 있습니다.

자기장 감지기는 2024년에 의약품 금속 감지기 시장에서 가장 큰 점유율을 차지했으며, 효능, 비용 효율성 및 다양한 의약품 적용에 대한 적응성이 입증되었습니다. 자기장 감지기는 X선 감지기 및 다중 주파수 감지기와 같은 고급 시스템보다 적은 자본으로 끝납니다. 많은 제약 제조업체, 특히 비용에 민감한 시장과 신흥 시장에서 사업을 전개하는 제조업체의 경우,이 저렴한 가격과 성능의 조합은 자기장 기술을 선호하는 선택입니다. 전반적으로 정확성, 범용성 및 경제적 가치의 조합은 의약품용 금속 감지기 시장에서 우위를 확고하게 합니다.

북미의 시장 성장을 가속하는 주요 요인으로는 의약품 제조 시설에서 높은 수준의 기술 도입과 자동화가 포함됩니다. 이러한 환경은 실시간 데이터 추적, AI 기반 교정, 자동 거부 시스템을 특징으로 하는 고급 금속 감지 시스템의 통합을 지원합니다. 연구개발비 증가와 인더스트리 4.0의 조기 도입으로 북미의 시설 전체에서 다중 주파수 감지기 및 자기장 감지기의 사용이 추진되고 있습니다. 이러한 기술 혁신과 업무효율의 중시가 이 지역 수요를 더욱 밀어 올리고 있습니다. 오염 위험으로 인한 의약품 리콜 증가, 미국 및 캐나다 의약품 수출량 증가도 견고한 검사 프로토콜을 필요로 하여 의약품 금속 감지기 시장에서 북미의 우위를 더욱 강화하고 있습니다.

본 보고서에서는 세계의 의약품용 금속 감지기 시장에 대해 조사했으며, 제품별, 기술별, 용도별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

서문

시장 역학

기술 분석

Porter's Five Forces 분석

규제 분석

특허 분석

무역 분석

주된 회의 및 이벤트(2025-2026년)

주요 이해관계자 및 구매 기준

가격 분석

밸류체인 분석

생태계 분석

AI 및 GEN AI가 의약품용 금속 감지기 시장에 미치는 영향

고객의 비즈니스에 영향을 미치는 동향 및 혼란

투자 및 자금조달 시나리오

미국 관세가 의약품용 금속 감지기 시장에 미치는 영향(2025년)

제6장 의약품용 금속 감지기 시장 : 제품별

서문

정제용 금속 감지기

캡슐용 금속 감지기

분말용 금속 감지기

액체용 금속 감지기

파이프라인용 금속 감지기

제7장 의약품용 금속 감지기 시장 : 기술별

서문

자기장 감지기

멀티 주파수 감지기

금속 감지기에 의한 X선 검사

기타

제8장 의약품용 금속 감지기 시장 : 용도별

서문

품질 관리

오염물질 검출

포장

컴플라이언스

제9장 의약품용 금속 감지기 시장 : 최종 사용자별

서문

제약회사

의약품 개발 제조 수탁 기관(CDMO)

바이오의약품기업

기타

제10장 의약품용 금속 감지기 시장 : 지역별

서문

북미

북미의 거시 경제 전망

미국

캐나다

유럽

유럽의 거시 경제 전망

독일

영국

프랑스

이탈리아

스페인

기타

아시아태평양

아시아태평양의 거시 경제 전망

중국

일본

인도

호주

한국

기타

기타 지역

기타 지역의 거시 경제 전망

제11장 경쟁 구도

개요

주요 진입기업의 전략 및 강점

수익 분석(2022-2024년)

시장 점유율 분석(2024년)

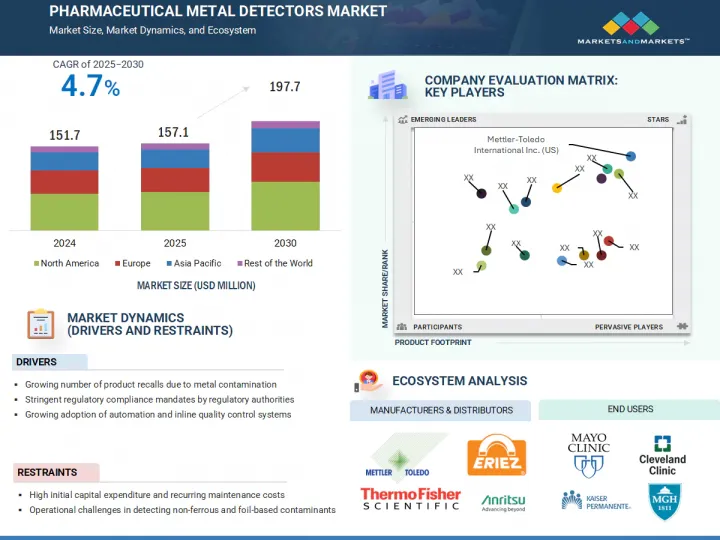

기업 평가 매트릭스 : 주요 진입기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

브랜드 및 제품 비교

주요 기업의 연구 개발비

기업 평가 및 재무지표

경쟁 시나리오

제12장 기업 프로파일

주요 진출기업

METTLER-TOLEDO INTERNATIONAL INC.

THERMO FISHER SCIENTIFIC INC.

ANRITSU CORPORATION

MINEBEAMITSUMI INC.

ILLINOIS TOOL WORKS INC.

ERIEZ MANUFACTURING CO.

CEIA SPA

FORTRESS TECHNOLOGY INC.

CASSEL MESSTECHNIK GMBH

BUNTING

NIKKA DENSOK LIMITED

PRISMA INDUSTRIALE SRL

WIPOTEC GMBH

DONGGUAN COSO ELECTRONIC TECH CO., LTD.

VINSYST TECHNOLOGIES

기타 기업

SED PHARMA

NEMESIS SRL

SOLLAU SRO

TECHNOFOUR ELECTRONICS PVT. LTD.

INOS

ACG

ULTRACON ENGIMECH PVT. LTD.

DAS ELECTRONICS

UNIQUE EQUIPMENT

LODHA INTERNATIONAL LLP

제13장 부록

AJY

영문 목차

영문목차

The global pharmaceutical metal detectors market is projected to reach USD 197.7 million by 2030 from USD 157.1 million in 2025, registering a CAGR of 4.7% during the forecast period. The growth is primarily driven by stringent regulatory requirements for product safety and the rising demand for contamination-free pharmaceutical products. Increasing cases of product recalls and quality-related concerns have compelled manufacturers to adopt advanced detection technologies.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD million)

Segments

Product, Technology, Application, End User, Region

Regions covered

North America, Europe, APAC, RoW

The growing integration of automated and intelligent metal detection systems, coupled with innovations in sensor sensitivity and real-time monitoring, is further expected to boost market expansion. Emphasis on compliance with GMP and FDA standards also encourages pharmaceutical companies to invest in high-precision inspection equipment. Moreover, industry players are increasingly engaging in product innovation and strategic collaborations to enhance their competitive edge and ensure process reliability.

By product type, the tablet metal detectors segment accounted for the largest market share in 2024.

Tablet metal detectors dominated the pharmaceutical metal detectors market in 2024, primarily due to the widespread production of tablets across the global pharmaceutical industry. Tablets remain the most preferred and commonly manufactured solid dosage form because of their convenience, long shelf life, and patient compliance. The ease of integration, cost-efficiency, and reliability of tablet metal detectors have led to their wide adoption by both large pharmaceutical manufacturers and contract manufacturing organizations (CMOs). With rising global drug demand and tighter quality controls, the use of tablet metal detectors continues to expand, solidifying their position as the leading product type in this market.

By technology, the magnetic field detectors segment accounted for the largest share of the market in 2024.

Magnetic field detectors held the largest share of the pharmaceutical metal detectors market in 2024 due to their proven effectiveness, cost-efficiency, and adaptability across various pharmaceutical applications. Magnetic field detectors require less capital than more advanced systems like X-ray or multi-frequency detectors. For many pharmaceutical manufacturers, especially those operating in cost-sensitive or emerging markets, this affordability, paired with performance, makes magnetic field technology the preferred choice. Altogether, their combination of precision, versatility, and economic value solidifies their dominance in the pharmaceutical metal detectors market.

By region, North America is expected to witness the highest growth rate during the forecast period.

The key factors driving market growth in North America include a high level of technological adoption and automation in pharmaceutical manufacturing facilities. This environment supports the integration of advanced metal detection systems that feature real-time data tracking, AI-based calibration, and automated rejection systems. Higher R&D spending and early adoption of Industry 4.0 practices have driven the use of multi-frequency and magnetic field detectors across North American facilities. This focus on innovation and operational efficiency further boosts the regional demand. The increasing number of drug recalls due to contamination risks and the growing export volume of US- and Canada-manufactured pharmaceutical products also necessitate robust inspection protocols, further reinforcing the dominance of North America in the pharmaceutical metal detectors market.

Breakdown of supply-side primary interviews:

By Company Type: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

By Designation: C-level Executives (35%), Directors (25%), and Others (40%)

By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

By Company Type: Pharmaceutical Companies (50%), CDMOs (25%), Biopharmaceutical Companies (15%), and Other End Users (10%)

By Designation: Heads of Manufacturing/Production (40%), Quality Assurance Managers (30%), Regulatory Compliance Officers (20%), and Other Designations (10%)

By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Research Coverage

This report studies the pharmaceutical metal detectors market by product, technology, application, end user, and region. The report also studies factors affecting market growth (drivers, restraints, opportunities, and challenges). It analyzes the opportunities and challenges in the market and provides details of the competitive landscape for market leaders. Additionally, the report examines micromarkets concerning their growth trends and predicts the revenue of the market segments across four key regions and their respective countries.

Reasons to Buy the Report

The report can assist both established and smaller firms in assessing the market, which would enable them to capture a larger share. Companies that purchase the report could utilize one or a combination of the five strategies outlined below.

This report provides insights into the following pointers:

Analysis of key drivers (growing number of product recalls due to metal contamination, stringent regulatory compliance mandates by regulatory authorities, and growing adoption of automation and inline quality control systems), restraints (high initial capital expenditure and recurring maintenance costs and operational challenges in detecting non-ferrous and foil-based contaminants), opportunities (focus on production optimization and high R&D investments and expansion of pharmaceutical exports and contract manufacturing), and challenges (integration complexity with existing production lines) are expected to influence the growth of the pharmaceutical metal detectors market.

Product Development/Innovation: Detailed insights into upcoming technologies, R&D activities, and product launches in the pharmaceutical metal detectors market.

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for several types of pharmaceutical metal detection processes across regions.

Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the pharmaceutical metal detectors market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the pharmaceutical metal detectors market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.2 MARKET SIZE ESTIMATION

2.3 MARKET BREAKDOWN & DATA TRIANGULATION

2.4 MARKET SHARE ESTIMATION

2.5 STUDY ASSUMPTIONS

2.6 RISK ASSESSMENT

2.7 RESEARCH LIMITATIONS

2.7.1 METHODOLOGY-RELATED LIMITATIONS

2.7.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PHARMACEUTICAL METAL DETECTORS MARKET OVERVIEW

4.2 NORTH AMERICA: PHARMACEUTICAL METAL DETECTORS MARKET OVERVIEW

4.3 PHARMACEUTICAL METAL DETECTORS MARKET: REGIONAL MIX

4.4 PHARMACEUTICAL METAL DETECTORS MARKET: GEOGRAPHICAL GROWTH OPPORTUNITIES

4.5 PHARMACEUTICAL METAL DETECTORS MARKET: DEVELOPING VS. DEVELOPED ECONOMIES

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing number of product recalls due to metal contamination

5.2.1.2 Stringent regulatory compliance mandates

5.2.1.3 Growing adoption of automation and inline quality control systems

5.2.2 RESTRAINTS

5.2.2.1 High initial capital expenditure and recurring maintenance costs

5.2.2.2 Operational challenges in detecting non-ferrous and foil-based contaminants

5.2.3 OPPORTUNITIES

5.2.3.1 Focus on production optimization and high R&D investment

5.2.3.2 Expansion of pharmaceutical exports and contract manufacturing

5.2.4 CHALLENGES

5.2.4.1 Integration complexity with existing production lines

5.3 TECHNOLOGY ANALYSIS

5.3.1 KEY TECHNOLOGIES

5.3.1.1 Electromagnetic induction technology

5.3.1.2 Multi frequency detection

5.3.2 COMPLEMENTARY TECHNOLOGIES

5.3.2.1 Conveyor and reject mechanism systems

5.3.2.2 Human-machine interface (HMI) and touchscreen controls

5.4 PORTER'S FIVE FORCES ANALYSIS

5.4.1 INTENSITY OF COMPETITIVE RIVALRY

5.4.2 BARGAINING POWER OF BUYERS

5.4.3 BARGAINING POWER OF SUPPLIERS

5.4.4 THREAT OF SUBSTITUTES

5.4.5 THREAT OF NEW ENTRANTS

5.5 REGULATORY ANALYSIS

5.5.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.5.2 REGULATORY FRAMEWORK

5.5.2.1 North America

5.5.2.1.1 US

5.5.2.1.2 Canada

5.5.2.2 Europe

5.5.2.2.1 Germany

5.5.2.3 Asia Pacific

5.5.2.3.1 China

5.5.2.3.2 Japan

5.5.2.3.3 India

5.5.2.3.4 Australia

5.5.2.4 Rest of the World

5.6 PATENT ANALYSIS

5.6.1 INSIGHTS ON PATENT PUBLICATION TRENDS, TOP APPLICANTS, AND JURISDICTION FOR PHARMACEUTICAL METAL DETECTORS MARKET, JANUARY 2015-MAY 2025

5.6.2 LIST OF MAJOR PATENTS, 2023-2024

5.7 TRADE ANALYSIS

5.7.1 IMPORT DATA FOR HS CODE 854370, 2020-2024

5.7.2 EXPORT DATA FOR HS CODE 854370, 2020-2024

5.8 KEY CONFERENCES & EVENTS, 2025-2026

5.9 KEY STAKEHOLDERS & BUYING CRITERIA

5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.9.2 KEY BUYING CRITERIA

5.10 PRICING ANALYSIS

5.10.1 INDICATIVE PRICING ANALYSIS OF KEY PLAYERS, BY PRODUCT TYPE, 2022-2024

5.10.2 INDICATIVE PRICING ANALYSIS OF PHARMACEUTICAL METAL DETECTORS, BY REGION, 2022-2024

5.11 VALUE CHAIN ANALYSIS

5.12 ECOSYSTEM ANALYSIS

5.13 IMPACT OF AI/GEN AI ON PHARMACEUTICAL METAL DETECTORS MARKET