X-Ray Detectors Market by Technology (FPD, Line scan, CCD, CR), Application (Medical, Vet, Defence, Industry) - Global Forecast to 2030

상품코드:1780343

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 287 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

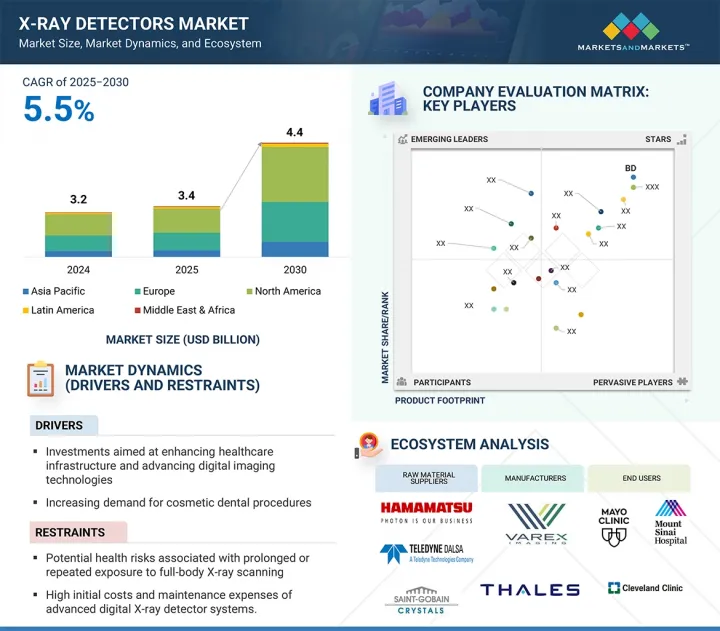

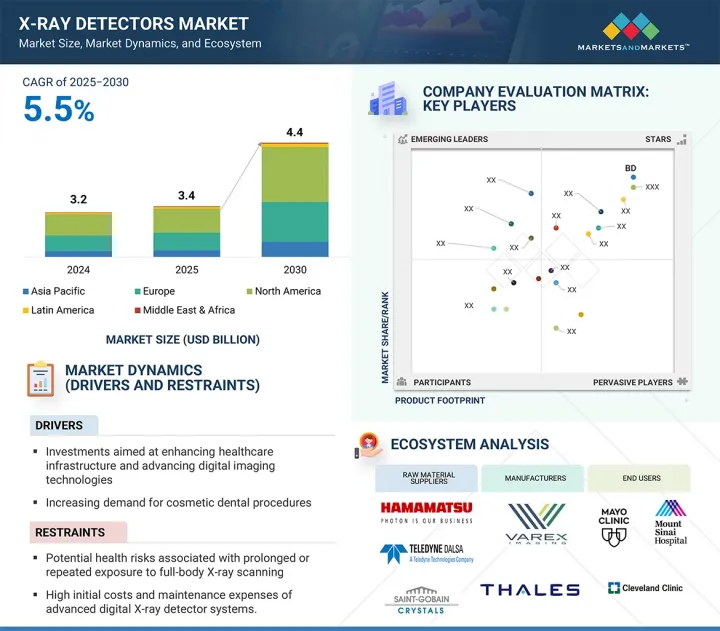

세계의 X선 검출기 시장 규모는 2025년 34억 달러에서 2030년에는 44억 달러로 성장할 것으로 예측되며, 예측 기간의 CAGR 5.5%로 성장할 전망입니다.

조사 범위

조사 대상 연도

2023-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액(달러)

부문

기술, 용도 및 지역

대상 지역

북미, 아시아태평양, 유럽, 중동 및 아프리카, 라틴 아메리카

업계의 성장은 적시 질병 발견의 필요성, 조기 진단에 대한 강조, 환자 인구 증가, 의료 인프라 및 디지털 이미징 솔루션의 현대화에 대한 투자 증가 등 여러 요인에 의해 촉진되고 있습니다. 고급 진단 도구에 대한 수요는 계속 증가하여 X선 검출기의 임상 용도가 더욱 확대되고 있습니다. 또한 휴대용 X선 시스템, AI 지원 이미징 분석 애플리케이션, 검출기의 감도 향상과 같은 혁신이 진단 이미징의 효율성과 정확성을 향상시키고 있습니다.

기술별로는 평면 패널 검출기 부문이 예측 기간 동안 가장 높은 CAGR은 성장할 것으로 예상됩니다.

X선 검출기 시장은 기술에 따라 플랫 패널 검출기, 라인 스캔 검출기, 컴퓨터 방사선 검출기, 전하 결합 소자 검출기, 광자 계수 검출기로 분류됩니다. 평면 패널 검출기 부문은 예측 기간 동안 가장 높은 CAGR은 성장할 것으로 예상됩니다. 응급실, 중환자실 및 의료 서비스가 부족한 지역에서 모바일 X선 시스템에 대한 수요가 증가함에 따라 병원은 경량 무선 평면 패널 검출기를 채택하고 있습니다. 이러한 첨단 검출기는 빠르고 유연하며 고해상도 이미징을 제공하여 병상 X선 기능을 크게 향상시키고 중증 및 고압의 임상 환경에서 환자 치료를 개선합니다. 또한, 휴대용 및 케이블이 없는 평면 패널 검출기는 중증 환자를 진료 장소에서 중앙 영상 시설로 이송할 필요가 없기 때문에 위험을 줄이고 효율성을 높입니다. 응급 상황, 공중 보건 상황, 임시 또는 현장 의료 환경에서 휴대하기 쉽고 배터리로 작동하는 X선 장치는 지연을 더욱 줄이는 데 도움이 될 것입니다.

지역별로는 북미가 2024년에 가장 큰 시장 점유율을 차지했습니다.

X선 검출기 시장은 북미, 유럽, 아시아태평양, 라틴 아메리카, 중동 및 아프리카의 5개 지역으로 나뉩니다. 북미 X선 검출기 시장은 의료 서비스의 효율성, 환자 안전 및 정확한 진단에 대한 지역적 관심이 높기 때문에 활발하게 성장하고 있습니다. 덜 침습적이고 빠른 진단 절차에 대한 동향으로 의료 서비스 제공자들은 신속한 임상적 의사 결정을 지원하는 고급 영상 장치를 채택하고 있습니다. 또한, 정부에서 의료 인프라 개선을 위한 정책을 추진하고 의료 기관의 디지털화 추세가 강화되면서 전통적인 영상 시스템에서 고성능 디지털 X선 검출기로의 전환이 가속화되고 있습니다. 또한 분산형 의료 서비스 제공에 대한 강조가 증가함에 따라 현장 진단 및 이동형 영상 솔루션에 대한 수요가 증가하고 있습니다.

본 보고서에서는 세계의 X선 검출기 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분 및 지역 및 주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

시장 역학

성장 촉진요인

억제요인

기회

과제

고객의 사업에 영향을 미치는 동향 및 혼란

가격 분석

밸류체인 분석

공급망 분석

에코시스템 시장 맵

투자 및 자금조달 시나리오

기술 분석

특허 분석

무역 분석

주요 회의 및 이벤트(2025-2026년)

규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

미충족 요구

AI가 X선 검출기 시장에 미치는 영향

미국 관세의 영향(2025년)

제6장 X선 검출기 시장 : 기술별

플랫 패널 검출기

컴퓨터 방사선 검출기

라인 스캔 검출기

전하 결합 소자 검출기

광자 계수 검출기

제7장 X선 검출기 시장 :

유형별

요오드화 세슘 플랫 패널 검출기

가돌리늄산황화물 플랫 패널 검출기

비정질 실리콘 플랫 패널 검출기

비정질 셀레늄 플랫 패널 검출기

CMOS 플랫 패널 검출기

기타

패널 유형별

대면적 플랫 패널 검출기

중면적 평판 검출기

소면적 플랫 패널 검출기

이동성별

휴대용

고정형

플랫폼별

디지털 플랫 패널 검출기

레트로 피트 플랫 패널 검출기

제8장 X선 검출기 시장 : 용도별

의료

정적 이미지

동적 이미지

치과용

보안/방위용

국토 안보

공공 및 민간 기업

방어

수의용

산업용

비파괴 검사

전자 검사

기타

제9장 X선 검출기 시장 : 지역별

북미

거시경제 전망

미국

캐나다

유럽

거시경제 전망

독일

프랑스

영국

이탈리아

스페인

기타

아시아태평양

거시경제 전망

일본

중국

인도

호주

한국

기타

라틴아메리카

거시경제 전망

브라질

멕시코

기타

중동 및 아프리카

거시경제 전망

GCC 국가

기타

제10장 경쟁 구도

주요 기업의 전략

수익 분석

시장 점유율 분석

기업평가와 재무지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업

기업평가 매트릭스 : 스타트업 및 중소기업

경쟁 시나리오

제11장 기업 프로파일

주요 기업

VAREX IMAGING

THALES

CANON INC.

IRAY GROUP

KONICA MINOLTA, INC.

AGFA-GEVAERT GROUP

CARESTREAM HEALTH

FUJIFILM HOLDINGS CORPORATION

ANALOGIC CORPORATION

HAMAMATSU PHOTONICS KK

TELEDYNE TECHNOLOGIES INCORPORATED

DRTECH

DETECTION TECHNOLOGY PLC

RIGAKU HOLDINGS CORPORATION

NEW MEDICAL IMAGING CO., LTD

기타 기업

ASTEL

MOXTEK, INC.

JPI HEALTHCARE SOLUTIONS

IBIS SRL

VIEWORKS CO., LTD

KA IMAGING

ACTEON

RAYENCE

DECTRIS AG

BMI BIOMEDICAL INTERNATIONAL SRL

제12장 부록

HBR

영문 목차

영문목차

The global market for X-ray detectors is projected to grow from USD 3.4 billion in 2025 to reach USD 4.4 billion in 2030, at a CAGR of 5.5% over the forecast period.

Scope of the Report

Years Considered for the Study

2023-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Technology, Type, Application, and Region

Regions covered

North America, Asia Pacific, Europe, Middle East & Africa, and Latin America

The industry's growth is driven by multiple factors, such as the need for timely disease detection, the emphasis on early diagnosis, a growing patient population, and rising investments in modernizing healthcare infrastructure and digital imaging solutions. The demand for advanced diagnostic tools continues to increase, further broadening the clinical applications of X-ray detectors. Additionally, innovations like portable X-ray systems, AI-enabled imaging analysis applications, and increased sensitivity in detectors are enhancing the efficiency and accuracy of diagnostic imaging.

By technology, the flat-panel detectors segment is expected to grow at the highest CAGR during the forecast period.

The X-ray detectors market is segmented by technology into flat-panel, computed radiography, line scans, charge-coupled devices, and photo-counting detectors. The flat-panel detectors segment is expected to grow at the highest CAGR during the forecast period. The growing demand for mobile X-ray systems in emergency departments, ICUs, and underserved areas drives hospitals to adopt lightweight, wireless flat-panel detectors. These advanced detectors offer fast, flexible, and high-resolution imaging, significantly enhancing bedside X-ray capabilities and supporting improved patient care in critical and high-pressure clinical environments. Additionally, portable and cable-free flat-panel detectors minimize the need to transfer critically ill patients from their point of care to central imaging facilities, thereby reducing risk and improving efficiency. During emergencies, public health situations, or in temporary or field-medicine environments, these easily portable and battery-operated X-ray units will help further reduce delays.

By portability type, the fixed flat-panel detectors segment accounted for the largest market share in 2024.

Based on the portability type, the market for X-ray detectors is divided into portable and fixed flat-panel detectors. The growth of fixed flat-panel detectors (FPDs) in X-ray imaging is driven by their widespread use in high-throughput clinical environments such as radiology departments, diagnostic centers, and hospitals where consistent, high-quality imaging is essential. Fixed FPDs offer superior image resolution, fast acquisition times, and enhanced durability, making them ideal for applications like chest radiography, orthopedic imaging, and mammography. Additionally, increasing investment in hospital infrastructure, rising demand for digital radiography systems, and the need for efficient workflow integration with PACS are further accelerating the adoption of fixed FPDs in routine diagnostic imaging.

By application, the medical applications segment accounted for the largest share of the market.

Based on the application, the market for X-ray detectors is divided into medical, dental, security/defense, veterinary, industrial, and other applications. The increase in demand for X-ray detectors used in medical imaging procedures arises principally from an ever-growing need to provide timely and accurate diagnoses of chronic ailments, e.g., cancer, cardiovascular diseases, and musculoskeletal disorders. Technological refinements in the detector systems directed towards the highest spatial resolution, lowest radiation dose, and fastest image acquisition simultaneously enhance diagnostic accuracy and clinical efficiency. The shift toward digital radiography, coupled with the rising use of portable and mobile imaging devices, is also crucial in increasing detector adoption, particularly as healthcare systems modernize and expand, especially in emerging markets.

By region, North America accounted for the largest market share in 2024.

The market for X-ray detectors encompasses five regions: North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The North American X-ray detector market is growing vigorously, driven by the high regional focus on enhancing the efficiency of healthcare, patient safety, and correct diagnosis. The trend towards less invasive and faster diagnosis procedures is compelling healthcare providers to adopt more advanced imaging devices that support rapid clinical decision-making. Furthermore, initiatives taken by the governments to enhance healthcare infrastructure, combined with the push towards digitalization in healthcare organizations, encourage the transition from conventional imaging systems to high-performance digital X-ray detectors. Moreover, the growing emphasis on decentralized healthcare provision is fuelling the demand for point-of-care and mobile imaging solutions.

The primary interviews conducted for this report can be categorized as follows:

By Respondent: Supply Side- 60% and Demand Side 40%

By Designation: Managers - 20%, CXO & Directors - 30%, and Executives - 50%

By Region: North America -40%, Europe -30%, Asia Pacific -20%, Latin America -5%, and the Middle East & Africa- 5%

List of Key Companies Profiled in the Report:

The prominent players in the X-ray detectors market are Varex Imaging (US), Canon (Japan), Thales Group (France), Analogic Corporation (US), Agfa-Gevaert Group (Belgium), Carestream Health (US), Drtech (South Korea), Detection Technology PLC (Finland), Fujifilm Holdings Corporation (Japan), and Hamamatsu Photonics K.K (Japan), among others.

Research Coverage:

This report studies the X-ray detectors market based on technology, type, application, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets concerning their growth trends. It forecasts the revenue of the market segments relating to five central regions (and the respective countries in these regions).

Key Benefits of Buying the Report:

The report will help market leaders/new entrants by providing the closest approximations of the X-ray detectors market's revenue numbers and subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their business better and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

Analysis of key drivers (investments to advance healthcare facilities and digital imaging technologies, rising target patient population), restraints (high cost of x-ray detectors, health hazards of full-body scanning), opportunities (rising healthcare expenditure across emerging economies and rising technological advancements), and challenges (lack of animal healthcare awareness in emerging countries and the increasing adoption of refurbished x-ray units).

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product approvals/launches in the X-ray detectors market.

Market Development: Comprehensive information about lucrative markets - the report analyses the market across varied regions.

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the X-ray detectors market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/approvals, pipeline analysis, acquisitions, partnerships, agreements, collaborations, other recent developments, investment and funding activities, brand/product comparative analysis, and vendor valuation and financial metrics of the X-ray detectors market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.1.1 SECONDARY RESEARCH

2.1.1.1 Key secondary sources

2.1.2 PRIMARY RESEARCH

2.1.2.1 Primary sources

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of primaries

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Company revenue estimation approach

2.2.1.2 Customer-based market estimation

2.2.1.3 CAGR projections

2.3 GROWTH FORECAST MODEL

2.4 DATA TRIANGULATION APPROACH

2.5 MARKET SHARE ESTIMATION

2.6 RESEARCH ASSUMPTIONS

2.7 RESEARCH LIMITATIONS

2.8 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 X-RAY DETECTORS MARKET OVERVIEW

4.2 REGIONAL SNAPSHOT OF X-RAY DETECTORS MARKET

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising investments in healthcare infrastructure and digital imaging technologies

5.2.1.2 Growing demand for X-ray detectors in security and industrial applications

5.2.1.3 Technological advancements in X-ray detectors

5.2.1.4 Increasing target patient population

5.2.2 RESTRAINTS

5.2.2.1 High cost of X-ray detectors

5.2.2.2 Health concerns associated with full-body X-ray scanning

5.2.2.3 Stringent regulatory and compliance requirements

5.2.3 OPPORTUNITIES

5.2.3.1 Rising demand for portable and mobile imaging

5.2.3.2 Growth opportunities in developing and emerging markets

5.2.3.3 Emerging non-medical uses of X-ray detectors

5.2.4 CHALLENGES

5.2.4.1 Lack of skilled radiologists and technicians

5.2.4.2 Rising adoption of refurbished X-ray units

5.2.4.3 Hospital budget constraints

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE OF FLAT PANEL DETECTORS

5.4.2 AVERAGE SELLING PRICE, BY KEY PLAYER

5.4.3 AVERAGE SELLING PRICE TREND, BY REGION

5.5 VALUE CHAIN ANALYSIS

5.5.1 RESEARCH & DEVELOPMENT

5.5.2 RAW MATERIAL PROCUREMENT & PRODUCT DEVELOPMENT

5.5.3 MARKETING, SALES, AND DISTRIBUTION

5.5.4 POST-SALES SERVICES

5.6 SUPPLY CHAIN ANALYSIS

5.6.1 PROMINENT COMPANIES

5.6.2 SMALL AND MEDIUM-SIZED ENTERPRISES

5.6.3 SMALL AND MEDIUM-SIZED ENTERPRISES

5.6.4 END USERS

5.7 ECOSYSTEM MARKET MAP

5.8 INVESTMENT AND FUNDING SCENARIO

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Flat panel detectors

5.9.1.2 Photon counting detectors

5.9.2 COMPLEMENTARY TECHNOLOGIES

5.9.2.1 Artificial intelligence and machine learning

5.9.3 ADJACENT TECHNOLOGIES

5.9.3.1 Computed tomography

5.9.3.2 Magnetic resonance imaging

5.10 PATENT ANALYSIS

5.11 TRADE ANALYSIS

5.11.1 IMPORT SCENARIO (HS CODE 902214)

5.11.2 EXPORT SCENARIO (HS CODE 902214)

5.12 KEY CONFERENCES AND EVENTS, 2025-2026

5.13 REGULATORY LANDSCAPE

5.13.1 REGULATORY GUIDELINES

5.13.1.1 North America

5.13.1.1.1 US

5.13.1.1.2 Canada

5.13.1.2 Europe

5.13.1.2.1 UK

5.13.1.2.2 France

5.13.1.2.3 Germany

5.13.1.3 Asia Pacific

5.13.1.3.1 China

5.13.1.3.2 Japan

5.13.1.3.3 India

5.13.1.4 Latin America

5.13.1.4.1 Brazil

5.13.1.4.2 Mexico

5.13.1.5 Middle East & Africa

5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.14 PORTER'S FIVE FORCE ANALYSIS

5.14.1 BARGAINING POWER OF SUPPLIERS

5.14.2 BARGAINING POWER OF BUYERS

5.14.3 THREAT OF NEW ENTRANTS

5.14.4 THREAT OF SUBSTITUTES

5.14.5 INTENSITY OF COMPETITIVE RIVALRY

5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2 KEY BUYING CRITERIA

5.16 UNMET NEEDS

5.17 IMPACT OF AI ON X-RAY DETECTORS MARKET

5.17.1 INTRODUCTION

5.17.2 MARKET POTENTIAL OF AI ON X-RAY DETECTORS

5.17.3 AI USE CASES

5.17.4 KEY COMPANIES IMPLEMENTING AI

5.17.5 FUTURE OF GENERATIVE AI ON X-RAY DETECTORS MARKET

5.18 IMPACT OF 2025 US TARIFF

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 PRICE IMPACT ANALYSIS

5.18.4 IMPACT ON COUNTRY/REGION

5.18.4.1 US

5.18.4.2 Europe

5.18.4.3 Asia Pacific

5.18.5 IMPACT ON END-USE INDUSTRIES

6 X-RAY DETECTORS MARKET, BY TECHNOLOGY

6.1 INTRODUCTION

6.2 FLAT PANEL DETECTORS

6.2.1 INCREASING LAUNCHES OF FLAT PANEL DETECTORS BY KEY PLAYERS TO FUEL MARKET

6.3 COMPUTED RADIOGRAPHY DETECTORS

6.3.1 WIRELESS COMMUNICATION AND REMOTE MONITORING CAPABILITIES TO PROMOTE GROWTH

6.4 LINE-SCAN DETECTORS

6.4.1 INCREASING ADOPTION OF X-RAY DETECTORS IN SECURITY APPLICATIONS AND MEDICAL IMAGING TO FAVOR GROWTH

6.5 CHARGE-COUPLED DEVICE DETECTORS

6.5.1 COST-EFFECTIVENESS AND FAST PROCESSING CAPABILITIES TO AID GROWTH

6.6 PHOTON-COUNTING DETECTORS

6.6.1 RISING NEED FOR HIGH-RESOLUTION IMAGING WITH LOW RADIATION TO EXPEDITE GROWTH

7 FLAT PANEL DETECTORS MARKET

7.1 INTRODUCTION

7.2 BY TYPE

7.2.1 CESIUM IODIDE FLAT PANEL DETECTORS

7.2.1.1 High detective quantum efficiency to foster growth

7.2.2 GADOLINIUM OXYSULFIDE FLAT PANEL DETECTORS

7.2.2.1 Affordability, mechanical resilience, and adaptability to support growth

7.2.3 AMORPHOUS SILICON FLAT PANEL DETECTORS

7.2.3.1 Superior image quality and minimized radiation exposure to favor growth

7.2.4 AMORPHOUS SELENIUM FLAT PANEL DETECTORS

7.2.4.1 Enhanced sensitivity, robust durability, and extended lifespan to drive market

7.2.5 CMOS FLAT PANEL DETECTORS

7.2.5.1 Increasing use of CMOS in medical imaging, industrial inspection, and scientific research to aid growth

7.2.6 OTHER FLAT PANEL DETECTORS

7.3 BY PANEL TYPE

7.3.1 LARGE-AREA FLAT PANEL DETECTORS

7.3.1.1 Broader imaging coverage and improved workflow efficiency to amplify growth

7.3.2 MEDIUM-AREA FLAT PANEL DETECTORS

7.3.2.1 Increasing adoption of detectors in medical and industrial applications to stimulate growth

7.3.3 SMALL-AREA FLAT PANEL DETECTORS

7.3.3.1 Faster image acquisition and compact design to facilitate growth

7.4 BY PORTABILITY

7.4.1 PORTABLE FLAT PANEL DETECTORS

7.4.1.1 Reduced radiation exposure and user-friendly operation to encourage growth

7.4.2 FIXED FLAT PANEL DETECTORS

7.4.2.1 Consistent and efficient imaging performance to contribute to growth

7.5 BY PLATFORM

7.5.1 DIGITAL FLAT PANEL DETECTORS

7.5.1.1 Increasing use of detectors for digital mammography and angiography to accelerate growth

7.5.2 RETROFIT FLAT PANEL DETECTORS

7.5.2.1 Ability to improve diagnostic capabilities and streamline workflow to promote growth

8 X-RAY DETECTORS MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 MEDICAL APPLICATIONS

8.2.1 STATIC IMAGING APPLICATIONS

8.2.1.1 Chest imaging application

8.2.1.1.1 Need for diagnostic precision and improved patient outcomes to boost market

8.2.1.2 Orthopedics application

8.2.1.2.1 Increasing prevalence of obesity and related lifestyle disorders to spur growth

8.2.1.3 Mammography application

8.2.1.3.1 Growing incidence of breast cancer to propel market

8.2.1.4 Oncology application

8.2.1.4.1 Growing emphasis on early detection and timely treatment to drive market

8.2.1.5 Other static imaging applications

8.2.2 DYNAMIC IMAGING

8.2.2.1 Fluoroscopy application

8.2.2.1.1 Rising health awareness to bolster growth

8.2.2.2 Surgical imaging

8.2.2.2.1 Growing preference for minimally invasive techniques to fuel market

8.2.2.3 Cardiovascular imaging application

8.2.2.3.1 Rising demand for early diagnosis and effective management of cardiovascular diseases to propel market

8.2.2.4 Spinal imaging application

8.2.2.4.1 Growing integration of digital radiography to boost market

8.3 DENTAL APPLICATIONS

8.3.1 INCREASING PREVALENCE OF DENTAL CARIES AND PERIODONTAL DISEASES TO AID GROWTH

8.4 SECURITY/DEFENSE APPLICATIONS

8.4.1 HOMELAND SECURITY

8.4.1.1 Need for surveillance in high-security environments to support growth

8.4.2 PUBLIC & PRIVATE ENTERPRISES

8.4.2.1 Evolving security needs to accelerate growth

8.4.3 DEFENSE

8.4.3.1 Rising use of X-ray detection systems in border checkpoints and crossings to facilitate growth

8.5 VETERINARY APPLICATIONS

8.5.1 RISING PET ADOPTION AND GROWING FOCUS ON ANIMAL HEALTH TO BOOST MARKET

8.6 INDUSTRIAL APPLICATIONS

8.6.1 NON-DESTRUCTIVE TESTING

8.6.1.1 Stricter safety norms and aging infrastructure to contribute to growth

8.6.2 ELECTRONIC INSPECTION

8.6.2.1 Rising need for precision in electronics to augment growth

8.7 OTHER APPLICATIONS

9 X-RAY DETECTORS MARKET, BY REGION

9.1 INTRODUCTION

9.2 NORTH AMERICA

9.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

9.2.2 US

9.2.2.1 Rising incidence of chronic conditions to spur growth

9.2.3 CANADA

9.2.3.1 Favorable government initiatives to bolster growth

9.3 EUROPE

9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

9.3.2 GERMANY

9.3.2.1 Booming automotive and defense sectors to aid growth

9.3.3 FRANCE

9.3.3.1 Shifting demography toward elderly population to facilitate growth

9.3.4 UK

9.3.4.1 Strategic investments in digital health technologies to foster growth

9.3.5 ITALY

9.3.5.1 Growing focus on security to boost market

9.3.6 SPAIN

9.3.6.1 Growing focus on digital health transformation to propel market

9.3.7 REST OF EUROPE

9.4 ASIA PACIFIC

9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

9.4.2 JAPAN

9.4.2.1 Growing elderly population to drive market

9.4.3 CHINA

9.4.3.1 Decreasing prices of flat panel detectors to boost market

9.4.4 INDIA

9.4.4.1 Rising disposable incomes to facilitate growth

9.4.5 AUSTRALIA

9.4.5.1 Increasing focus on early detection and preventive care to boost market

9.4.6 SOUTH KOREA

9.4.6.1 Favorable insurance coverage to expedite growth

9.4.7 REST OF ASIA PACIFIC

9.5 LATIN AMERICA

9.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

9.5.2 BRAZIL

9.5.2.1 Rising disease burden to contribute to growth

9.5.3 MEXICO

9.5.3.1 Increasing number of hospitals to expedite growth

9.5.4 REST OF LATIN AMERICA

9.6 MIDDLE EAST & AFRICA

9.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

9.6.2 GCC COUNTRIES

9.6.2.1 Increasing adoption of AI and cloud-based imaging technologies to foster growth

9.6.3 REST OF MIDDLE EAST & AFRICA

10 COMPETITIVE LANDSCAPE

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES

10.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN X-RAY DETECTORS MARKET

10.3 REVENUE ANALYSIS, 2021-2024

10.4 MARKET SHARE ANALYSIS, 2024

10.5 COMPANY VALUATION AND FINANCIAL METRICS

10.6 BRAND/PRODUCT COMPARISON

10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.7.1 STARS

10.7.2 EMERGING LEADERS

10.7.3 PERVASIVE PLAYERS

10.7.4 PARTICIPANTS

10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.7.5.1 Company footprint

10.7.5.2 Region footprint

10.7.5.3 Technology footprint

10.7.5.4 Type footprint

10.7.5.5 Application footprint

10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

10.8.1 PROGRESSIVE COMPANIES

10.8.2 RESPONSIVE COMPANIES

10.8.3 DYNAMIC COMPANIES

10.8.4 STARTING BLOCKS

10.8.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2024

10.8.5.1 Detailed list of key startups/SMEs

10.8.5.2 Competitive benchmarking of key startups/SMEs