Copper Tubes Market by Type (Type K, Type L, Type M, Other Types), Form (Straight Tubes, Coils, Capillary Tubes, Other Forms), Application (HVACR, Plumbing, Industrial, Automotive, Medical, Other Applications), Region - Global Forecast to 2030

상품코드:1777129

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 272 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

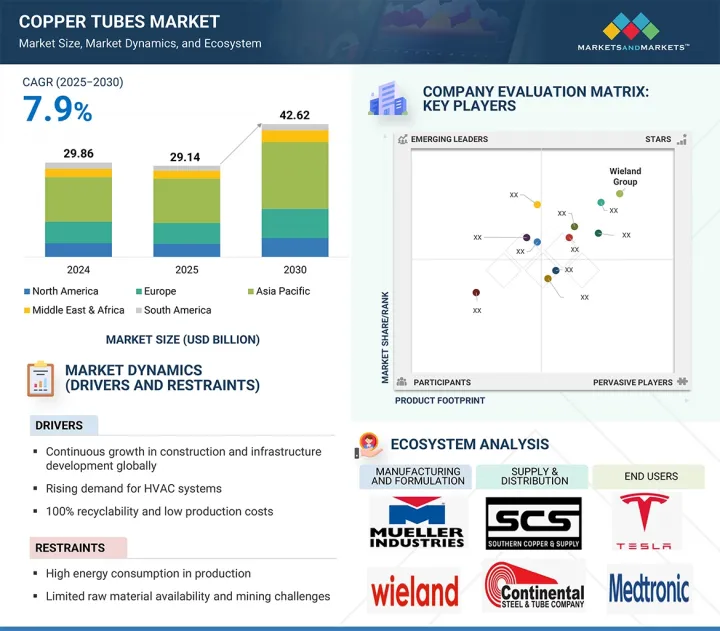

동관 시장 규모는 7.9%의 연평균 성장률(CAGR)로 성장할 것으로 전망되고 2025년의 291억 4,000만 달러에서 2030년에는 426억 2,000만 달러로 성장할 것으로 예측되고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러/10억 달러) 및 킬로톤

부문

용도별, 형상별, 두께별, 유형별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동, 아프리카, 남미

동관 시장은 에너지 효율적인 HVACR 솔루션에 대한 수요 증가, 의료 인프라의 확장, 지속 가능한 건축 관행에 대한 강조가 강화됨에 따라 상당한 성장을 경험하고 있습니다. 구리는 고유한 강도, 우수한 열전도율 및 재활용성으로 인해 의료, 배관 및 산업용으로 선호되는 재료로 떠오르고 있습니다. 스마트 시티의 개발, 기존 인프라의 개조, 첨단 열 관리 시스템이 필요한 전기자동차의 채택 증가로 시장 확대에 상당한 기회가 생기고 있습니다. 또한, 국내 생산은 유리한 정부 정책에 의해 지원되고 있으며, 친환경 빌딩 인증은 시장 성장을 더욱 촉진하고 있습니다. 산업이 운영 효율성과 지속 가능성을 점점 더 우선시함에 따라, 동관은 현재의 수요와 장기적인 목표를 모두 충족하는 실용적이고 미래에 대비한 대안으로 자리매김하고 있습니다.

K형 동관은 여러 주요 요인의 촉진으로 동관 시장에서 가장 빠르게 성장하는 부문입니다. 우수한 강도와 두꺼운 벽은 뛰어난 압력 처리 능력을 제공하여 다양한 용도에 매우 다재다능합니다. K형 관의 주요 응용 분야로는 의료용 가스 관, 지하 배관 시스템 및 유체 수송 네트워크가 있으며, 이들 모두는 해당 부문의 수요 증가에 기여하고 있습니다. 또한, 이러한 동향은 서비스 수명이 연장된 지속 가능하고 부식에 강하며 내구성이 뛰어난 관 솔루션에 대한 세계의의 관심이 높아지는 추세와도 일치합니다. 따라서 K형 구리관은 시장에서 지속적인 성장을 기대할 수 있습니다.

최근 몇 년 동안 실내 공기질 개선과 에너지 효율 향상에 대한 추세가 뚜렷하게 나타나면서 여러 국가 정부가 탄소 배출량 감축을 위한 노력을 시작했습니다. 이러한 변화는 운영에 동관에 크게 의존하는 에너지 효율적인 HVACR 시스템에 대한 수요가 증가하고 있음을 강조합니다. 동시에 도시화와 산업화가 HVACR 시스템에 대한 수요를 더욱 부추겨 동관의 필요성을 촉진했습니다. 동관은 뛰어난 열전도율과 내식성으로 이러한 HVACR 시스템에 매우 선호되며, 이러한 특성으로 인해 시스템의 작동 수명이 연장됩니다. 지속 가능하고 효율적인 솔루션에 대한 관심이 높아짐에 따라 HVACR 응용 분야에서 동관의 역할은 더욱 중요해지고 있습니다.

아시아태평양 지역은 지난 10년 동안 지속적인 도시화와 산업 발전에 힘입어 동관 시장에서 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 이 지역의 각국 정부는 산업화와 함께 지속 가능성을 점점 더 우선 순위로 삼고 있으며, 특히 배관, 의료, 자동차, 산업 및 HVACR 분야와 같은 동관의 주요 응용 분야에서 그 경향이 두드러지고 있습니다. 특히, 농촌 및 반도시 지역을 중심으로 주택, 수도 인프라 및 위생 시설을 개선하기 위한 정부 지원 사업이 구리 튜브에 대한 수요를 더욱 부추기고 있습니다. 또한, 아시아태평양 지역은 HVACR 시스템, 전자 제품 및 자동차 부품의 주요 제조 허브로, 구리 튜브에 대한 수요가 증가할 것으로 보입니다. 이 지역은 풍부한 원자재 공급, 저렴한 인건비, 동관 전문 국내 제조업체의 증가 등 지속적인 시장 성장에 기여하는 요소를 모두 갖추고 있어 생산의 중요한 경제 동력 역할을 하고 있습니다.

본 보고서에서는 세계의 구리관 시장에 대해 조사했으며, 용도별, 형상별, 두께별, 유형별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

생성형 AI가 동관 시장에 미치는 영향

제6장 업계 동향

소개

고객사업에 영향을 주는 동향/혼란

공급망 분석

미국 관세가 동관 시장에 미치는 영향(2025년)

투자 및 자금조달 시나리오

가격 분석

생태계 분석

기술 분석

특허 분석

무역 분석

주된 회의와 이벤트(2025-2026년)

관세 및 규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

거시경제지표

사례 연구 분석

제7장 동관 시장(용도별)

소개

HVACR

배관

산업

의료

자동차

기타

제8장 동관 시장(형상별)

소개

직관

코일

모세관

기타

제9장 동관 시장(두께별)

소개

표준 게이지

초중량 게이지

얇은 게이지

기타

제10장 동관 시장(유형별)

소개

K형

M형

L형

기타

제11장 동관 시장(지역별)

소개

아시아태평양

중국

일본

인도

한국

기타

북미

미국

캐나다

멕시코

유럽

독일

이탈리아

프랑스

영국

스페인

기타

중동 및 아프리카

GCC 국가

남아프리카

기타

남미

아르헨티나

브라질

기타

제12장 경쟁 구도

소개

주요 참가 기업의 전략/강점(2020년 1월-2025년 6월)

시장 점유율 분석(2024년)

수익 분석(2020-2024년)

브랜드/제품 비교

기업평가 매트릭스 : 주요 진입기업(2024년)

기업평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제13장 기업 프로파일

주요 진출기업

MUELLER INDUSTRIES

WIELAND GROUP

HAILIANG GROUP

KME GROUP SPA

LUVATA

CERRO FLOW PRODUCTS LLC

KOBE STEEL, LTD.

CAMBRIDGE-LEE INDUSTRIES LLC

SHANGHAI METAL CORPORATION

QINGDAO HONGTAI COPPER CO., LTD.

기타 기업

MM KEMBLA: COMPANY OVERVIEW

UNIFLOW COPPER TUBES

GOLDEN DRAGON PRECISE COPPER TUBE GROUP INC.

INTERSTATE METAL, INC.

MEHTA TUBES LIMITED

BRASSCO TUBE INDUSTRIES

NIPPONTUBE

NINGBO JINTIAN COPPER(GROUP) CO., LTD.

CUPORI

MAKSAL TUBES(PTY) LTD.

METTUBE

LYON COPPER ALLOYS

CUBEX TUBINGS LIMITED

SEAH FS CO., LTD.

TUBE TECH COPPER & ALLOYS PVT. LTD.

제14장 부록

HBR

영문 목차

영문목차

The copper tubes market is projected to grow from USD 29.14 billion in 2025 to USD 42.62 billion by 2030, at a CAGR of 7.9%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/USD Billion) and Volume (Kiloton)

Segments

Type, Form, Application, and Region

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, and South America

The copper tubes market is experiencing significant growth driven by increased demand for energy-efficient HVACR solutions, the expansion of healthcare infrastructure, and a heightened emphasis on sustainable building practices. Copper is emerging as the preferred material for medical, plumbing, and industrial applications due to its inherent strength, excellent thermal conductivity, and recyclability. The development of smart cities, the retrofitting of existing infrastructure, and the rising adoption of electric vehicles-necessitating advanced thermal management systems-present substantial opportunities for market expansion. Additionally, domestic production is supported by favorable government policies, while green building certifications further catalyze market growth. As industries increasingly prioritize operational efficiency and sustainability, copper tubes are positioning themselves as a viable and future-proof alternative, meeting both current demands and long-term objectives.

"Type K to be fastest-growing segment of copper tubes market during forecast period"

Type K copper tubes represent the fastest-growing segment in the copper tubing market, driven by several key factors. Their superior strength and thicker walls provide exceptional pressure-handling capabilities, making them highly versatile for various applications. Major application areas for Type K tubes include medical gas tubing, underground plumbing systems, and fluid transport networks, all of which contribute to increasing demand across these sectors. Furthermore, this trend aligns with the growing global emphasis on sustainable, corrosion-resistant, and durable tubing solutions with an extended service life. Consequently, Type K copper tubes are poised for continued growth in the market.

"HVACR to be fastest-growing application segment of copper tubes market during forecast period"

In recent years, there has been a marked trend towards improving indoor air quality and enhancing energy efficiency, prompting various governments to initiate efforts aimed at reducing carbon footprints. This shift underscores the increasing demand for energy-efficient HVACR systems, which significantly depend on copper tubes for their operation. Concurrently, urbanization and industrialization have further fueled the demand for HVACR systems, thereby driving the necessity for copper tubes. Copper tubes are highly preferred in these HVACR systems due to their exceptional thermal conductivity and corrosion resistance, which collectively extend the operational lifespan of these systems. As the focus on sustainable and efficient solutions intensifies, the role of copper in HVACR applications becomes even more critical.

"Asia Pacific to be fastest-growing regional market for copper tubes during forecast period"

The Asia Pacific region is emerging as the fastest-growing market for copper tubes, driven by continuous urbanization and industrial development observed over the past decade. Governments across the region are increasingly prioritizing sustainability alongside industrialization, particularly in key applications for copper tubes, such as plumbing, medical, automotive, industrial, and HVACR sectors. Significantly, government-sponsored initiatives aimed at upgrading housing, water infrastructure, and sanitation facilities-especially in rural and semi-urban areas-are further bolstering the demand for copper tubes. Additionally, Asia Pacific is a leading manufacturing hub for HVACR systems, electronics, and automotive components, which will increase the demand for copper tubing. The region serves as a vital economic engine for production, benefitting from an abundant supply of raw materials, cost-effective labor, and a growing number of indigenous manufacturers specializing in copper tubes-all contributing to sustained market growth.

In the process of determining and verifying the market size for several segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees is as follows:

By Company Type: Tier 1 - 60%, Tier 2 - 25%, and Tier 3 - 15%

By Designation: Manger-Level - 30%, Director Level - 20%, and Others - 50%

By Region: North America - 20%, Europe -30%, Asia Pacific - 30%, Middle East & Africa - 10%, and South America-10%

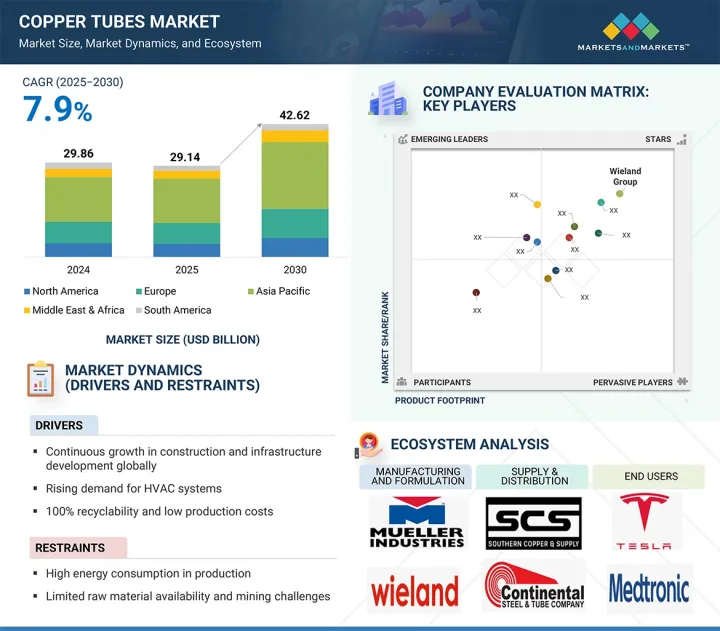

The key players in this market are Mueller Industries (US), Wieland Group (Germany), Hailiang Group (China), KME Group SpA (Italy), LUVATA (Finland), Cerro Flow Products LLC (US), KOBE STEEL, LTD. (Japan), Cambridge-Lee Industries LLC (US), Shanghai Metal Corporation (China), Quindao Hongtai Copper Tube Co., Ltd. (China).

Research Coverage

This report segments the market for the copper tubes based on type, form, application, and region. It provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and partnerships associated with the market for the copper tubes market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the copper tubes market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following points:

Analysis of key drivers: Continuous Growth in Construction and Infrastructure Development Globally, Rising Demand for HVAC Systems and Copper's 100% recyclability drives the global market by reducing production cost, ensuring supply stability and meeting sustainability demands

Market Penetration: Comprehensive information on the copper tubes offered by top players in the global copper tubes market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the copper tubes market.

Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for the copper tubes across regions.

Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global copper tubes market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the copper tubes market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 INCLUSIONS & EXCLUSIONS

1.3.2 COPPER TUBES MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Primary data sources

2.1.2.3 Key primary participants

2.1.2.4 Breakdown of interviews with experts

2.1.2.5 Key industry insights

2.2 BASE NUMBER CALCULATION

2.2.1 SUPPLY-SIDE APPROACH

2.2.2 DEMAND-SIDE APPROACH

2.3 FORECAST NUMBER CALCULATION

2.3.1 SUPPLY SIDE

2.3.2 DEMAND SIDE

2.4 MARKET SIZE ESTIMATION

2.4.1 BOTTOM-UP APPROACH

2.4.2 TOP-DOWN APPROACH

2.5 DATA TRIANGULATION

2.6 RESEARCH ASSUMPTIONS

2.7 GROWTH FORECAST

2.8 RISK ASSESSMENT

2.9 FACTOR ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN COPPER TUBES MARKET

4.2 COPPER TUBES MARKET, BY TYPE

4.3 COPPER TUBES MARKET, BY FORM

4.4 COPPER TUBES MARKET, BY APPLICATION

4.5 COPPER TUBES MARKET, BY THICKNESS

4.6 COPPER TUBES MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing construction and infrastructure development globally

5.2.1.2 Rising demand for HVAC systems

5.2.1.3 100% recyclability reduces production costs, ensures supply stability, and meets sustainability demands

5.2.2 RESTRAINTS

5.2.2.1 Highly energy-intensive production process

5.2.2.2 Limited raw material availability and mining challenges

5.2.3 OPPORTUNITIES

5.2.3.1 High growth in demand for renewable energy and electric vehicles

5.2.4 CHALLENGES

5.2.4.1 Increasing competition from aluminum and cross-linked polyethylene

5.3 IMPACT OF GENERATIVE AI ON COPPER TUBES MARKET

5.3.1 INTRODUCTION

5.3.2 OPTIMIZATION OF MANUFACTURING

5.3.3 PREDICTIVE MAINTENANCE

5.3.4 MARKET FORECASTING AND COMPETITIVE INTELLIGENCE

5.3.5 SUPPLY CHAIN OPTIMIZATION

5.3.6 CUSTOMER EXPERIENCE AND TECHNICAL SUPPORT

5.3.7 SUSTAINABILITY AND CARBON FOOTPRINT ANALYSIS

6 INDUSTRY TRENDS

6.1 INTRODUCTION

6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.2.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR COPPER TUBES MANUFACTURERS

6.3 SUPPLY CHAIN ANALYSIS

6.3.1 RAW MATERIAL SOURCING

6.3.1.1 Copper ore extraction

6.3.1.2 Processing

6.3.2 MANUFACTURE OF COPPER TUBES

6.3.2.1 Casting and smelting

6.3.2.2 Extrusion and drawing

6.3.2.3 Annealing

6.3.2.4 Cutting and shaping

6.3.2.5 Surface treatment

6.3.3 DISTRIBUTORS

6.3.4 END USERS

6.4 IMPACT OF 2025 US TARIFFS ON COPPER TUBES MARKET

6.4.1 INTRODUCTION

6.4.2 KEY TARIFF RATES

6.4.3 PRICE IMPACT ANALYSIS

6.4.4 IMPACT ON COUNTRY/REGION

6.4.4.1 US

6.4.4.2 Europe

6.4.4.3 Asia Pacific

6.4.5 IMPACT ON APPLICATIONS

6.5 INVESTMENT AND FUNDING SCENARIO

6.6 PRICING ANALYSIS

6.6.1 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2024

6.6.2 AVERAGE SELLING PRICE TREND, BY TYPE, 2021-2024

6.6.3 AVERAGE SELLING PRICE TREND, BY THICKNESS, 2021-2024

6.6.4 AVERAGE SELLING PRICE TREND, BY FORM, 2021-2024

6.6.5 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2021-2024

6.6.6 AVERAGE SELLING PRICE OF TOP THREE COPPER TUBE TYPES, BY KEY PLAYERS, 2024

6.7 ECOSYSTEM ANALYSIS

6.8 TECHNOLOGY ANALYSIS

6.8.1 KEY TECHNOLOGIES

6.8.2 COMPLEMENTARY TECHNOLOGIES

6.8.3 ADJACENT TECHNOLOGIES

6.9 PATENT ANALYSIS

6.9.1 METHODOLOGY

6.9.2 GRANTED PATENTS, 2015-2024

6.9.2.1 Publication trends for last ten years

6.9.3 INSIGHTS

6.9.4 LEGAL STATUS

6.9.5 JURISDICTION ANALYSIS

6.9.6 TOP APPLICANTS

6.9.7 KEY PATENTS FOR COPPER TUBES

6.10 TRADE ANALYSIS

6.10.1 IMPORT SCENARIO (HS CODE 741110)

6.10.2 EXPORT SCENARIO (HS CODE 741110)

6.11 KEY CONFERENCES AND EVENTS, 2025-2026

6.12 TARIFF AND REGULATORY LANDSCAPE

6.12.1 TARIFF AND REGULATIONS RELATED TO COPPER TUBES

6.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.12.3 REGULATIONS RELATED TO COPPER TUBES MARKET

6.13 PORTER'S FIVE FORCES ANALYSIS

6.13.1 THREAT OF NEW ENTRANTS

6.13.2 THREAT OF SUBSTITUTES

6.13.3 BARGAINING POWER OF SUPPLIERS

6.13.4 BARGAINING POWER OF BUYERS

6.13.5 INTENSITY OF COMPETITIVE RIVALRY

6.14 KEY STAKEHOLDERS AND BUYING CRITERIA

6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.14.2 BUYING CRITERIA

6.15 MACROECONOMIC INDICATORS

6.15.1 GDP TRENDS AND FORECAST OF MAJOR ECONOMIES

6.16 CASE STUDY ANALYSIS

6.16.1 SUMITOMO'S ENHANCED THERMAL CONDUCTIVITY COPPER TUBES FOR HVAC SYSTEMS

6.16.2 KME GROUP'S SUSTAINABLE COPPER TUBE PRODUCTION WITH ECO-FRIENDLY PRACTICES

6.16.3 HINDALCO INDUSTRIES' HIGH-PRECISION COPPER TUBES FOR HVAC&R IN INDIA

7 COPPER TUBES MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 HVACR

7.2.1 RISING DEMAND FOR ENERGY-EFFICIENT AND CORROSION-RESISTANT MATERIALS TO DRIVE MARKET

7.3 PLUMBING

7.3.1 EXPANDING CONSTRUCTION AND INFRASTRUCTURE DEVELOPMENT TO BOOST GROWTH

7.4 INDUSTRIAL

7.4.1 RISING DEMAND FOR RELIABLE HEAT TRANSFER SOLUTIONS UNDER EXTREME PRESSURE AND CORROSIVE ENVIRONMENTS TO PROPEL MARKET

7.5 MEDICAL

7.5.1 GROWING EMPHASIS ON CONTAMINATION-FREE GAS DELIVERY AND THERMAL PRECISION TO FUEL MARKET

7.6 AUTOMOTIVE

7.6.1 INCREASING NEED FOR DURABLE AND HEAT-EFFICIENT MATERIALS IN HIGH-PERFORMANCE VEHICLES TO SUPPORT GROWTH

7.7 OTHER APPLICATIONS

7.7.1 MARINE

7.7.2 ELECTRICAL & ELECTRONICS

7.7.3 SOLAR ENERGY SYSTEMS

8 COPPER TUBES MARKET, BY FORM

8.1 INTRODUCTION

8.2 STRAIGHT TUBES

8.2.1 STRENGTH, RELIABILITY, AND VERSATILITY TO DRIVE MARKET

8.3 COILS

8.3.1 FLEXIBILITY TO DRIVE ADOPTION

8.4 CAPILLARY TUBES

8.4.1 COMPACT AND EFFICIENT PERFORMANCE IN REFRIGERATION UNITS TO SUPPORT MARKET GROWTH

8.5 OTHER FORMS

8.5.1 INNER GROOVED TUBES

8.5.2 FINNED TUBES

8.5.3 FLATTENED TUBES

9 COPPER TUBES MARKET, BY THICKNESS

9.1 INTRODUCTION

9.2 STANDARD GAGE

9.2.1 EXCELLENT THERMAL CONDUCTIVITY AND CORROSION RESISTANCE TO DRIVE DEMAND FOR RESIDENTIAL, COMMERCIAL, AND INDUSTRIAL APPLICATIONS

9.3 EXTRA-HEAVY GAGE

9.3.1 INCREASED DURABILITY TO FUEL SUITABILITY FOR HEAVY-DUTY APPLICATIONS

9.4 THIN-WALL GAGE

9.4.1 COST-EFFECTIVENESS AND EASE OF INSTALLATION IN TIGHT SPACES FOR LOW PRESSURE APPLICATIONS TO BOOST MARKET

9.5 OTHER THICKNESSES

9.5.1 COPPER CLAD TUBES

9.5.2 MICRO TUBES

10 COPPER TUBES MARKET, BY TYPE

10.1 INTRODUCTION

10.2 TYPE K

10.2.1 THICKEST WALL AND DURABILITY TO DRIVE DEMAND FOR UNDERGROUND WATER SUPPLY AND HIGH-PRESSURE APPLICATIONS

10.3 TYPE M

10.3.1 UTILITY IN LOW-PRESSURE INDOOR WATER DISTRIBUTION TO BOOST MARKET

10.4 TYPE L

10.4.1 BALANCE OF STRENGTH AND WORKABILITY TO FUEL DEMAND IN RESIDENTIAL WATER PIPING AND HVAC SYSTEMS

10.5 OTHER TYPES

10.5.1 DMV (DRAIN, WASTE, AND VENT) TUBES

10.5.2 ACR (AIR CONDITIONING AND REFRIGERATION) TUBES

10.5.3 MEDICAL GAS TUBING

11 COPPER TUBES MARKET, BY REGION

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 CHINA

11.2.1.1 Significant investments in power grid expansion and green building projects to propel market

11.2.2 JAPAN

11.2.2.1 Aging infrastructure and energy-efficient retrofitting to drive adoption in residential and commercial buildings

11.2.3 INDIA

11.2.3.1 Rapid urbanization and government-led smart city initiatives to boost demand for HVAC and plumbing systems

11.2.4 SOUTH KOREA

11.2.4.1 Rising electric vehicle production and expansion of battery cooling systems to fuel demand

11.2.5 REST OF ASIA PACIFIC

11.3 NORTH AMERICA

11.3.1 US

11.3.1.1 Government focus on improving aging infrastructure, water, and HVAC systems to drive market

11.3.2 CANADA

11.3.2.1 Green building initiatives and renewable energy goals to support market growth

11.3.3 MEXICO

11.3.3.1 Growth in automotive production to propel market

11.4 EUROPE

11.4.1 GERMANY

11.4.1.1 Expanding electric vehicle production and battery cooling infrastructure to drive demand

11.4.2 ITALY

11.4.2.1 Rising construction and plumbing activities fueled by infrastructure projects to boost market

11.4.3 FRANCE

11.4.3.1 Large-scale investments in healthcare infrastructure to drive market

11.4.4 UK

11.4.4.1 Major investments in 5G and digital infrastructure to propel market

11.4.5 SPAIN

11.4.5.1 Focus on renewable energy to drive demand

11.4.6 REST OF EUROPE

11.5 MIDDLE EAST & AFRICA

11.5.1 GCC COUNTRIES

11.5.1.1 UAE

11.5.1.1.1 Smart city initiatives and high-rise building developments to fuel demand

11.5.1.2 Saudi Arabia

11.5.1.2.1 Massive infrastructure projects and increased HVACR installations to boost market

11.5.1.3 Rest of GCC countries

11.5.2 SOUTH AFRICA

11.5.2.1 Expanding healthcare infrastructure and medical gas systems to boost demand

11.5.3 REST OF MIDDLE EAST & AFRICA

11.6 SOUTH AMERICA

11.6.1 ARGENTINA

11.6.1.1 Growing demand for energy-efficient cooling systems amid rising temperatures to fuel market

11.6.2 BRAZIL

11.6.2.1 Rising urbanization and large-scale residential construction projects to boost demand

11.6.3 REST OF SOUTH AMERICA

12 COMPETITIVE LANDSCAPE

12.1 INTRODUCTION

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN (JANUARY 2020-JUNE 2025)

12.3 MARKET SHARE ANALYSIS, 2024

12.3.1 MARKET SHARE OF KEY PLAYERS, 2024

12.4 REVENUE ANALYSIS, 2020-2024

12.5 BRAND/PRODUCT COMPARISON

12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.6.1 STARS

12.6.2 EMERGING LEADERS

12.6.3 PERVASIVE PLAYERS

12.6.4 PARTICIPANTS

12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.6.5.1 Company footprint

12.6.5.2 Region footprint

12.6.5.3 Type footprint

12.6.5.4 Application footprint

12.6.5.5 Form footprint

12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024