Blast Chillers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1959653

리서치사:Global Market Insights Inc.

발행일:2026년 02월

페이지 정보:영문 163 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

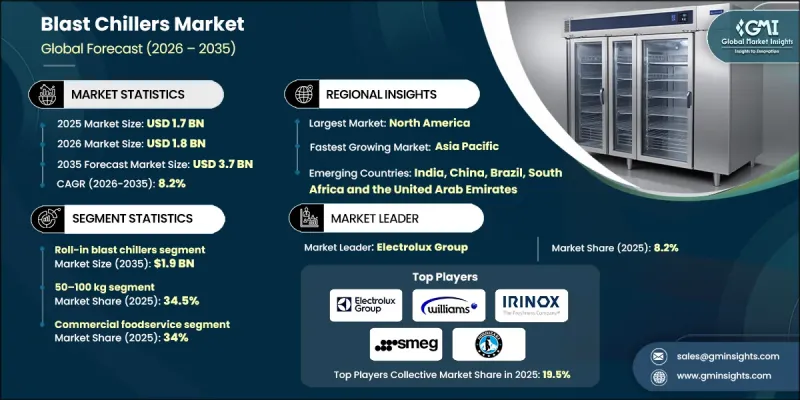

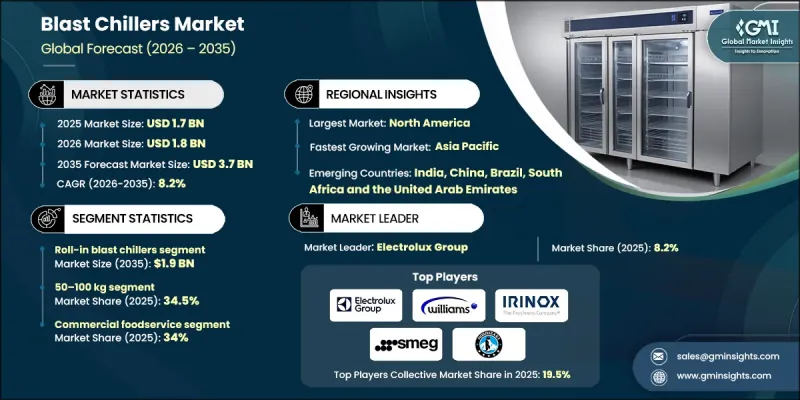

세계의 블라스트 칠러 시장은 2025년에 17억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 8.2%로 성장하여 37억 달러에 이를 것으로 예측됩니다.

시장 성장의 배경에는 세계 식품 안전 기준 강화, 외식 산업 및 가공 분야에서의 급속 냉각 기술 보급 확대, 콜드체인의 무결성을 유지하면서 식품 폐기물을 최소화하는 것의 중요성 증가 등이 있습니다. 온도 관리에 대한 엄격한 가이드라인을 포함한 규제 프레임워크는 사업자들이 최신 냉각 솔루션을 도입하도록 장려하고 있습니다. 식품 가공업체와 상업용 주방에서는 조리된 제품의 온도를 빠르게 낮추고, 병원균의 증식을 억제하며, 정부가 정한 식품 안전 기준을 준수하기 위해 블래스트 칠러에 대한 의존도가 높아지고 있습니다. 특히 가금류, 육류 및 즉석식품 생산자들은 즉각적인 냉각 및 오염 방지 권장 사항을 충족하기 위해 이러한 시스템에 크게 의존하고 있습니다. 블라스트 칠러 기술의 발전은 대량 처리 환경에서 작업 효율성, 일관성 및 운영 안전성을 향상시키는 데 기여하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

17억 달러

예측 금액

37억 달러

CAGR

8.2%

롤인형 블래스트 칠러 시장은 2035년까지 19억 달러 규모에 달할 것으로 예측됩니다. 롤인 유닛은 풀 사이즈의 이동식 랙을 수용할 수 있는 특성으로 인해 중앙 주방, 시설용 푸드서비스, 산업용 식품 가공 등 대규모 응용 분야에서 점점 더 많은 사랑을 받고 있습니다. 이 유닛은 일괄 조리 워크플로우를 지원하면서 균일하고 안정적인 냉각을 제공하여 점점 더 엄격해지는 식품 안전 기준과 온도 관리 요건을 충족합니다. 높은 운영 효율로 생산 피크 시 품질 유지에 최적입니다.

2025년 기준, 50-100kg 용량 부문은 34.5%의 점유율을 차지했습니다. 이 부문은 본격적인 산업용 장비에 대한 투자를 피하면서 높은 냉각 용량을 필요로 하는 중규모 레스토랑, 베이커리, 클라우드 키친에서 인기가 높아지고 있습니다. 생산량이 증가함에 따라 공간, 속도, 에너지 효율의 균형은 사업자에게 매우 중요합니다. 이 중용량 유닛은 신선도, 균일성, 엄격한 온도 관리를 유지하면서 제품을 신속하게 냉각하여 일상 업무와 규정 준수를 지원합니다.

북미 블라스트 냉각기 시장은 2025년 37.7%의 점유율을 차지했습니다. 이 지역 시장 확대는 엄격한 식품 안전 규제, 콜드체인 인프라의 현대화, 상업용 주방 및 외식 산업의 규모 확대에 의해 촉진되고 있습니다. 블라스트 칠러는 대량 생산 환경에서 제품 품질 유지, 폐기물 감소, 지역 온도 관리 기준 준수를 보장하기 위해 대량 생산 환경에서 널리 채택되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추산 및 예측 : 용량별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH

영문 목차

영문목차

The Global Blast Chillers Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 3.7 billion by 2035.

Market growth is fueled by rising global food safety standards, increasing adoption of rapid cooling technologies in foodservice and processing sectors, and growing emphasis on minimizing food waste while maintaining cold chain integrity. Regulatory frameworks, including strict guidelines on temperature control, are pushing operators to adopt modern cooling solutions. Food processors and commercial kitchens are increasingly relying on blast chillers to quickly reduce the temperature of cooked products, reducing pathogen growth and complying with government-mandated food safety standards. Producers of poultry, meat, and ready-to-eat foods are particularly dependent on these systems to meet recommendations for immediate chilling and contamination prevention. Advancements in blast chiller technology are also improving workflow efficiency, consistency, and operational safety in high-volume environments.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.7 Billion

Forecast Value

$3.7 Billion

CAGR

8.2%

The roll-in blast chillers segment is expected to reach USD 1.9 billion by 2035. Roll-in units are increasingly favored for large-scale applications, including central kitchens, institutional food service, and industrial food processing, due to their ability to accommodate full mobile racks. These units support batch preparation workflows while ensuring uniform and consistent cooling, aligning with stricter food safety and temperature control requirements. Their operational efficiency makes them ideal for maintaining quality in peak production periods.

The 50-100 kg capacity segment accounted for 34.5% share in 2025. This segment is growing in popularity among mid-sized restaurants, bakeries, and cloud kitchens that require higher cooling capabilities without investing in full-scale industrial equipment. Balancing space, speed, and energy efficiency is crucial for operators as production volumes increase. These mid-capacity units allow kitchens to cool products quickly while preserving freshness, consistency, and strict temperature control, supporting daily operations and regulatory compliance.

North America Blast Chillers Market held a 37.7% share in 2025. Market expansion in the region is driven by stringent food safety regulations, modernization of cold chain infrastructure, and the growing scale of commercial kitchens and foodservice operations. Blast chillers are widely adopted to maintain product quality, reduce spoilage, and ensure compliance with regional temperature-control standards across high-volume environments.

Key players in the Global Blast Chillers Market include Foster Refrigerator, Hoshizaki Europe B.V., Electrolux Group, IRINOX S.p.A., Lainox, TEFCOLD (UK), Cool Head Europe, Alto Shaam, Inc., Traulsen & Co., Inc., Victory Refrigeration LLC, Infrico, Friginox, SMEG S.p.A., Williams Refrigeration, and Fulgor Milano. Companies in the blast chillers market are focusing on strengthening their presence by investing in research and development to enhance cooling efficiency, durability, and user-friendly features. Many are expanding product lines with roll-in and mid-capacity units to cater to different commercial and industrial needs. Strategic partnerships with foodservice chains, catering businesses, and institutional kitchens ensure early adoption and long-term contracts. Firms are also emphasizing energy-efficient technologies, IoT-enabled monitoring, and smart cold chain integration.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Product type trends

2.2.2 Capacity trends

2.2.3 Application trends

2.2.4 Regional trends

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising demand for rapid cooling solutions in food processing facilities

3.2.1.2 Stringent food safety regulations and compliance requirements

3.2.1.3 Expansion of the global cold chain infrastructure

3.2.1.4 Growth of commercial kitchens, hotels, and quick-service restaurants (QSRs)

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment and maintenance costs

3.2.2.2 Energy consumption and operational efficiency concerns

3.2.3 Market opportunities

3.2.3.1 Adoption of energy-efficient and eco-friendly refrigeration technologies

3.2.3.2 Increasing demand from ready-to-eat and packaged food industries

3.3 Regulatory landscape

3.3.1 North America

3.3.2 Europe

3.3.3 Asia Pacific

3.3.4 Latin America

3.3.5 Middle East & Africa

3.4 Porter’s analysis

3.5 PESTEL analysis

3.6 Technology and innovation landscape

3.6.1 Current technological trends

3.6.2 Emerging technologies

3.7 Emerging business models

3.8 Compliance requirements

3.9 Patent and IP analysis

3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Million and Units)

5.1 Key trends

5.2 Roll In Blast Chillers

5.3 Reach-In Blast Chillers

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 ($ Million and Units)

6.1 Key trends

6.2 Below 50KG

6.3 50 - 100KG

6.4 101-200KG

6.5 More than 200KG

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million and Units)

7.1 Key trends

7.2 Commercial foodservice

7.2.1 Restaurants & QSR

7.2.2 Hotels & resorts

7.2.3 Catering companies

7.2.4 Bakeries & confectioneries

7.3 Institutional kitchens

7.3.1 Hospitals & healthcare facilities

7.3.2 Schools & universities

7.3.3 Correctional facilities

7.4 Food processing & manufacturing

7.4.1 Meat, seafood, poultry processors

7.4.2 Ready-to-eat (RTE) and frozen food manufacturers

7.4.3 Dairy processing

7.5 Logistics & cold chain

7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Million and Units)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 UK

8.3.3 France

8.3.4 Spain

8.3.5 Italy

8.3.6 Netherlands

8.4 Asia Pacific

8.4.1 China

8.4.2 India

8.4.3 Japan

8.4.4 Australia

8.4.5 South Korea

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.6 Middle East and Africa

8.6.1 South Africa

8.6.2 Saudi Arabia

8.6.3 UAE

Chapter 9 Company Profiles

9.1 Global Key Players

9.1.1 Alto Shaam, Inc

9.1.2 Electrolux Group

9.1.3 Hoshizaki Europe B.V. (Hoshizaki Corporation)