Electric Heavy Duty Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1959329

리서치사:Global Market Insights Inc.

발행일:2026년 02월

페이지 정보:영문 270 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

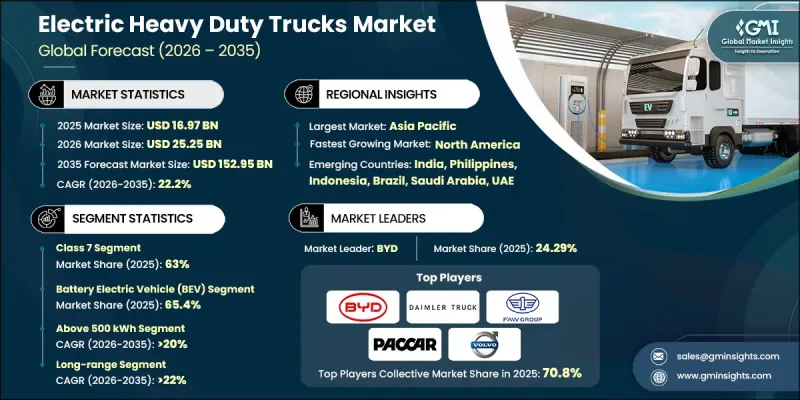

세계의 전기 대형 트럭 시장은 2025년에 169억 7,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 22.2%로 성장하여 1,529억 5,000만 달러에 이를 것으로 예측됩니다.

화물 운송의 탈탄소화를 향한 움직임은 차량 운영, 차량 설계, 도입 전략을 재구성하고 있습니다. 전기 대형 트럭(e-HDT)은 특히 도시 배송, 항만 업무, 지역 간 운송에서 지속 가능한 물류의 핵심이 되고 있습니다. 이 트럭은 디젤 배기가스, 연료 가격 변동, 상업 사업자에 대한 규제 압력을 줄여줍니다. 경량 EV와 달리 e-HDT는 무거운 적재량과 긴 운행 주기를 고려하여 설계되었기 때문에 배터리 수명, 충전 속도, 총 라이프사이클 비용이 도입의 중요한 요소입니다. 현대의 e-HDT는 디젤 모델의 개조가 아닌 전용 설계로 고에너지 배터리 시스템, 토크 최적화 전기 액슬, 첨단 파워 일렉트로닉스, 열 관리 솔루션, 차량 제어 소프트웨어를 갖추고 있습니다. 차량 관리자들은 초기 구매 비용보다는 노선 적합성, 적재량과 항속거리의 효율성, 인프라 구축 현황, 장기 운영 비용 등을 기준으로 차량을 평가하는 경향이 강해지고 있습니다. 민관의 투자 가속화로 전 세계 물류 및 산업 분야에서 대규모 도입이 진행되고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

169억 7,000만 달러

예측 금액

1,529억 5,000만 달러

CAGR

22.2%

클래스 7 부문은 2025년 63%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 복합 성장률(CAGR) 21.8%를 나타낼 것으로 예측됩니다. 총 중량 등급이 26,001-3만 3,000파운드인 클래스 7 트럭은 지역 화물 운송, 도심 배송, 높은 가동률의 상업적 운영에 적합합니다. 예측 가능한 경로, 잦은 정차, 디포 및 허브형 충전과의 호환성을 통해 사업자는 배터리 사용 최적화, 충전으로 인한 다운타임 감소, 운영 비용의 효율적 관리를 할 수 있습니다.

배터리 전기자동차(BEV) 부문은 2025년 65.4%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 22.6%를 나타낼 것으로 예측됩니다. BEV는 배기가스 배출이 없고, 에너지 효율이 뛰어나며, 도시 및 지역 운송 업무에 대한 적응성이 뛰어나 시장을 선도하고 있습니다. 첨단 배터리 기술, 회생 브레이크, 에너지 관리 시스템, 안정적인 성능, 낮은 유지보수성, 긴 수명을 보장하는 BEV는 지속 가능하고 비용 효율적인 솔루션을 원하는 차량 운영자에게 최적의 선택이 될 수 있습니다.

중국의 전기 대형 트럭 시장은 2025년에 큰 점유율을 차지했습니다. 확대의 배경에는 강력한 정부 정책, 배출가스 감축 목표, 도시화, 무공해 차량 도입 의무화 등이 있습니다. 현지 생산 능력, 비용 효율적인 대용량 배터리, 확장 가능한 전기 구동 시스템이 물류, 산업, 지역 운송 분야에서의 보급을 가속화하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 차종별, 2022-2035

제6장 시장 추산 및 예측 : 추진력별, 2022-2035

제7장 시장 추산 및 예측 : 범위별, 2022-2035

제8장 시장 추산 및 예측 : 배터리 용량별, 2022-2035

제9장 시장 추산 및 예측 : 용도별, 2022-2035

제10장 시장 추산 및 예측 : 총중량별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH

영문 목차

영문목차

The Global Electric Heavy Duty Trucks Market was valued at USD 16.97 billion in 2025 and is estimated to grow at a CAGR of 22.2% to reach USD 152.95 billion by 2035.

The increasing drive toward decarbonizing freight transportation is reshaping fleet operations, vehicle design, and deployment strategies. Electric heavy-duty trucks (e-HDTs) are becoming central to sustainable logistics, particularly for urban distribution, port operations, and regional haul applications. These trucks mitigate diesel emissions, fuel price volatility, and regulatory pressures on commercial operators. Unlike lighter EVs, e-HDTs are designed for heavy payloads and long duty cycles, making battery longevity, charging speed, and total lifecycle cost crucial for adoption. Modern e-HDTs are purpose-built rather than conversions from diesel models, featuring high-energy battery systems, torque-optimized electric axles, advanced power electronics, thermal management solutions, and vehicle control software. Fleet managers increasingly assess vehicles based on route compatibility, payload-range efficiency, infrastructure readiness, and long-term operating expenses rather than upfront purchase cost. Accelerated public and private investment is supporting large-scale deployment across logistics and industrial sectors worldwide.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$16.97 Billion

Forecast Value

$152.95 Billion

CAGR

22.2%

The Class 7 segment held 63% share in 2025 and is expected to grow at a CAGR of 21.8% through 2035. Class 7 trucks, with gross vehicle weight ratings of 26,001 to 33,000 pounds, are well-suited for regional freight, urban delivery, and high-utilization commercial operations. Their predictable routes, frequent stops, and compatibility with depot- and hub-based charging allow operators to optimize battery use, reduce charging downtime, and manage operational costs efficiently.

The battery electric vehicle (BEV) segment accounted for 65.4% share in 2025 and is projected to grow at a CAGR of 22.6% through 2035. BEVs dominate due to zero tailpipe emissions, superior energy efficiency, and suitability for both urban and regional haul operations. Advanced battery technologies, regenerative braking, and energy management systems ensure consistent performance, low maintenance, and long service life, making BEVs the preferred choice for fleet operators pursuing sustainable and cost-effective solutions.

China Electric Heavy Duty Trucks Market held a significant share in 2025. Expansion is driven by strong government policies, emission reduction targets, urbanization, and zero-emission fleet mandates. Local manufacturing capabilities, cost-efficient high-capacity batteries, and scalable electric drivetrains accelerate adoption across logistics, industrial, and regional applications.

Key players in the Global Electric Heavy Duty Trucks Market include BYD, Daimler Truck, Ford, GM, Komatsu, Nikola, PACCAR, Tesla, Traton, and Volvo. Companies in the Electric Heavy Duty Trucks Market are strengthening their presence by developing purpose-built platforms optimized for high payloads, long routes, and depot charging networks. Strategic partnerships with battery manufacturers, fleet operators, and infrastructure providers enable faster scaling and enhanced charging coverage. Investment in R&D focuses on improving energy density, thermal management, power electronics, and regenerative braking systems. Manufacturers are adopting modular vehicle architectures, expanding global production facilities, and leveraging government incentives for clean transportation. They are also deploying pilot fleets and digital fleet management tools to demonstrate performance, reduce operational risk, and accelerate customer adoption.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Vehicle Class

2.2.3 Propulsion

2.2.4 Range

2.2.5 Battery Capacity

2.2.6 Application

2.2.7 GVWR

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increase in government mandates for zero-emission commercial vehicles

3.2.1.2 Surge in adoption of electric trucks by logistics and industrial fleet operators

3.2.1.3 Rise in fuel cost volatility and total operating expenses of diesel trucks

3.2.1.4 Surge in advancements in battery energy density and charging technologies

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial cost associated with vehicle and infrastructure deployment

3.2.2.2 Limited charging availability for long-haul freight operations

3.2.3 Market opportunities

3.2.3.1 Increase in adoption of fleet-as-a-service and leasing models

3.2.3.2 Surge in electrification of ports, mining, and industrial operations

3.2.3.3 Rise in deployment of megawatt and ultra-fast charging solutions

3.2.3.4 Surge in integration of digital fleet management platforms

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S. EPA Diesel Emissions Reduction Act (DERA)

3.4.1.2 U.S. DOE Vehicle Technologies Office Programs

3.4.1.3 EPA Clean Truck Program

3.4.1.4 California Advanced Clean Trucks (ACT) Regulation.

3.4.2 Europe

3.4.2.1 EU CO2 Emission Standards & Clean Truck Directive

3.4.2.2 Germany Federal Zero-Emission Truck Program

3.4.2.3 United Kingdom ULEV Fleet Incentives

3.4.2.4 France Heavy Vehicle Decarbonization Support

3.4.3 Asia Pacific

3.4.3.1 China: New Energy Bus (NEB) Promotion & Procurement Policies

3.4.3.2 Japan: Green Growth Strategy for Decarbonized Public Transport

3.4.3.3 South Korea: Eco-Friendly Vehicle Roadmap for Public Transport

3.4.3.4 Singapore: Green Public Transport Programme (GPTP)

3.4.4 Latin America

3.4.4.1 Brazil Zero-Emission Truck Procurement

3.4.4.2 Mexico Clean Transport & Fleet Modernization Policies

3.4.4.3 Chile National Zero-Emission Truck Strategy

3.4.5 MEA

3.4.5.1 UAE Sustainable Transport Policy

3.4.5.2 Saudi Arabia Vision 2030 Freight Electrification

3.4.5.3 South Africa Green Freight Strategy

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Patent analysis

3.9 Sustainability and environmental impact analysis

3.9.1 Sustainable practices

3.9.2 Waste reduction strategies

3.9.3 Energy efficiency in production

3.9.4 Eco-friendly initiatives

3.9.5 Carbon footprint considerations

3.10 Future outlook & opportunities

3.11 Cost breakdown analysis

3.12 Sustainability and environmental impact analysis