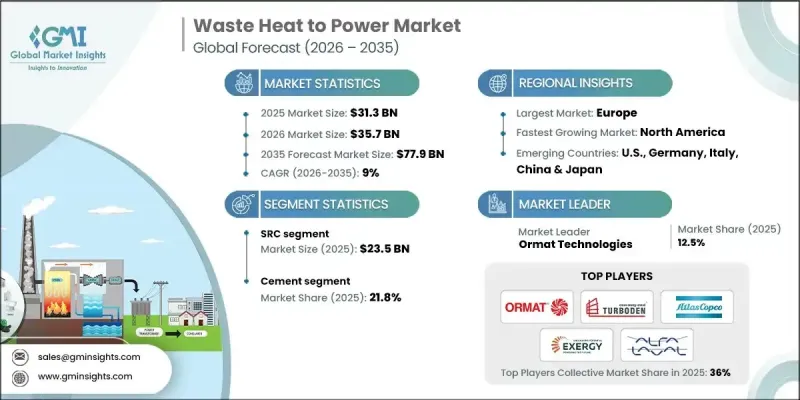

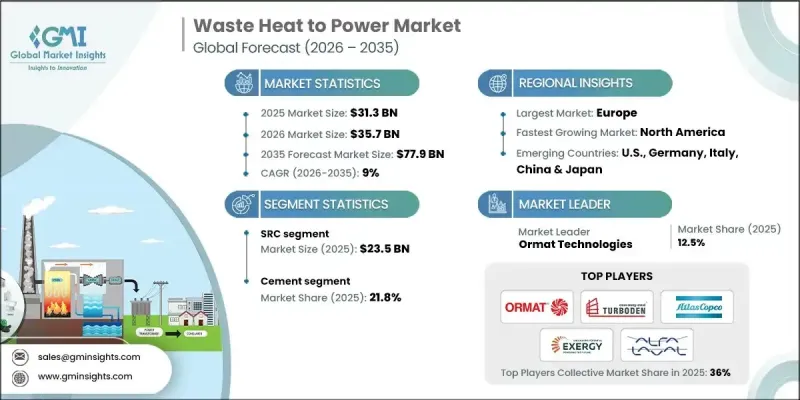

세계의 폐열발전 시장은 2025년에 313억 달러로 평가되었으며, 2035년까지 CAGR 9%로 성장하여 779억 달러에 달할 것으로 예측됩니다.

시장 성장은 보다 엄격한 에너지 효율 규제와 산업 탈탄소화에 대한 필요성이 증가함에 따라 주도되고 있습니다. 시멘트, 철강, 유리, 화학, 펄프 및 제지 등 중공업은 고온 공정으로 운영되고 있어 막대한 열 손실이 발생합니다. 폐열 발전 시스템은 이 버려지는 열을 회수하여 전력으로 전환함으로써 시설의 에너지 소비를 줄이고, 효율 목표를 달성하며, 내부 탄소 예산 및 ISO 50001 스타일 프로그램을 준수할 수 있도록 도와줍니다. 에너지 가격의 변동성으로 인해 자가발전의 가치는 더욱 높아지고 있습니다. 열병합발전은 안정적인 저비용 전력을 공급하는 동시에 전력망 의존도 및 피크 시 요금 부담을 줄일 수 있습니다. 여러 공장에 도입하면 비용 시너지를 창출하고, 역률을 개선하며, 수요 요금을 절감할 수 있습니다. ESG에 대한 노력 강화와 지속가능한 산업 운영 추진으로 열병합발전은 에너지 및 배출량 집약형 산업에서 전략적 에너지 관리 도구로 자리매김하고 있습니다. 장기적으로 이러한 시스템은 다양한 분야에서 측정 가능한 비용 절감과 비즈니스 연속성을 제공합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 313억 달러 |

| 예측 금액 | 779억 달러 |

| CAGR | 9% |

스팀 랭킨 사이클(SRC) 부문은 2025년 235억 달러에 달했으며, 2035년까지 연평균 7.5%의 성장률을 기록할 것으로 전망됩니다. SRC는 검증된 터빈 성능과 플랜트 운영자들 사이에서 높은 인지도를 바탕으로 고온 폐열을 사용할 수 있는 산업에서 여전히 선호되는 기술입니다. 기존 보일러 및 증기 인프라와의 호환성을 통해 대규모 산업 응용 분야에 적합하며 시멘트, 철강, 석유화학, 발전 시설 등에서 폭넓게 채택되고 있습니다. SRC 시스템의 오랜 운영 실적과 신뢰성은 연속적인 산업 공정에의 도입에 대한 확신을 강화합니다.

시멘트 분야는 2025년 21.8%의 점유율을 차지했으며, 2035년까지 연평균 8.5%의 성장률을 기록할 것으로 전망됩니다. 시멘트 제조 및 정유 공장의 고온 공정은 발전에 적합한 안정적인 폐열 스트림을 생성합니다. 에너지 비용의 상승과 탈탄소화 압력으로 인해 플랜트에서는 연료 사용량, 전력 구매량, 전력망 의존도를 줄이기 위해 폐열발전(WHP) 시스템 활용이 추진되고 있습니다. 규제 요건과 기업의 ESG(환경, 사회, 지배구조) 이니셔티브도 지속가능성 목표와 운영 최적화를 지원하면서 에너지 효율을 향상시키는 솔루션으로 폐열발전(WHP)의 도입을 더욱 촉진하고 있습니다.

북미 폐열 발전 시장은 2025년 33억 달러 규모에 달했습니다. 정유, 화학, 철강, 식품가공, 시멘트 등 에너지 집약형 산업에서는 현장 발전에 활용할 수 있는 열 손실이 현저하게 발생하고 있습니다. 유기랭킨사이클(ORC) 시스템의 채택은 다양한 온도 프로파일에 대한 대응력과 기존 산업시설에 대한 개보수 가능성으로 확대되고 있습니다. 청정에너지 프로그램의 인센티브와 더불어 전력 비용 상승 및 기업의 지속가능성 요구사항이 결합되어 분산형 발전의 비용 효율적이고 환경 친화적인 솔루션으로 WHP 시스템의 도입이 가속화되고 있습니다.

The Global Waste Heat to Power Market was valued at USD 31.3 billion in 2025 and is estimated to grow at a CAGR of 9% to reach USD 77.9 billion by 2035.

The market growth is driven by stricter energy efficiency regulations and the rising need for industrial decarbonization. Heavy industries such as cement, steel, glass, chemicals, and pulp & paper operate with high-temperature processes that generate significant thermal losses. WHP systems capture this otherwise wasted heat and convert it into electricity, helping facilities reduce energy consumption, meet efficiency targets, and comply with internal carbon budgets or ISO 50001-style programs. Energy price volatility makes self-generation particularly valuable, as WHP provides reliable, low-cost power while reducing dependence on the grid and exposure to peak tariffs. Multi-plant deployments create cost synergies, improve power factor, and lower demand charges. Increasing ESG commitments and the drive toward sustainable industrial operations have positioned WHP as a strategic energy management tool for energy- and emissions-intensive industries. Over time, these systems provide measurable cost savings and operational resilience across sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.3 Billion |

| Forecast Value | $77.9 Billion |

| CAGR | 9% |

The Steam Rankine Cycle (SRC) segment reached USD 23.5 billion in 2025 and is forecasted to grow at a CAGR of 7.5% through 2035. SRC remains the preferred technology in industries with high-temperature waste heat availability due to its proven turbine performance and familiarity among plant operators. Its compatibility with existing boiler and steam infrastructure makes it ideal for large-scale industrial applications, supporting widespread adoption in cement, steel, petrochemical, and power generation facilities. The long operational history and reliability of SRC systems reinforce confidence in deploying them for continuous industrial processes.

The cement segment held a 21.8% share in 2025 and is expected to grow at a CAGR of 8.5% through 2035. High-temperature processes in cement and refinery operations create consistent waste heat streams suitable for electricity generation. Rising energy costs and decarbonization pressures are encouraging plants to leverage WHP systems to reduce fuel use, electricity purchases, and grid reliance. Regulatory requirements and corporate ESG initiatives further drive the adoption of WHP as a solution to enhance energy efficiency while supporting sustainability goals and operational optimization.

North America Waste Heat to Power Market generated USD 3.3 billion in 2025. Energy-intensive sectors such as petroleum refining, chemicals, steel, food processing, and cement contribute significant thermal losses that can be captured for on-site power generation. The adoption of Organic Rankine Cycle (ORC) systems is growing due to their flexibility in handling diverse temperature profiles and retrofitting capabilities for existing industrial sites. Incentives under clean energy programs, coupled with rising electricity costs and corporate sustainability mandates, are accelerating the deployment of WHP systems as a cost-effective and environmentally responsible solution for distributed power generation.

Key players operating in the Global Waste Heat to Power Market include AC Boiler SpA, ALFA LAVAL, Atlas Copco, Aura GmbH & CO. KG, Climeon, Cochran Ltd., Durr Group, Exergy International Srl, Forbes Marshall, General Electric, IHI Corporation, Mitsubishi Heavy Industries, Ltd., Ormat Technologies, Rentech Boiler System, Siemens Energy, Thermax Ltd, Turboden, and Walchandnagar Industries Limited (WIL). Companies in the waste heat to power market are adopting multiple strategies to strengthen their position and expand market share. These include investing in R&D to enhance efficiency and retrofit capabilities for diverse industrial heat sources. Firms are forming strategic alliances and partnerships with energy service providers and technology companies to expand deployment opportunities and integrate advanced control systems. Companies are also entering new geographic markets and providing turnkey solutions to increase adoption among heavy industrial clients.