듀얼 클러치 변속기 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)

Dual Clutch Transmission Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936636

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

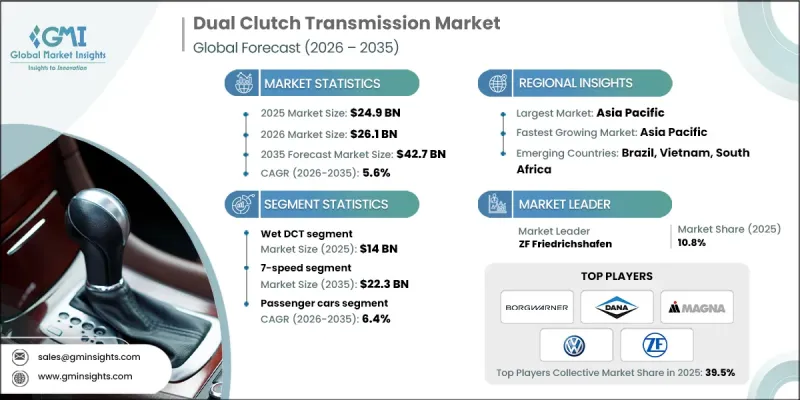

세계의 듀얼 클러치 변속기 시장은 2025년에 249억 달러로 평가되었으며, 2035년까지 CAGR 5.6%로 성장하여 427억 달러에 달할 것으로 예측됩니다.

DCT는 빠르고 매끄러운 변속을 실현하는 첨단 변속기 시스템으로, 초기에는 고급 승용차나 고성능 차량에 보급되었고, 점차 상용차나 일부 오토바이로 확대되고 있습니다. 이러한 채택 확대는 연비 효율성 향상, 부드러운 가속, 주행 역동성 개선에 대한 요구로 인해 추진되고 있습니다. 제조사들은 DCT를 하이브리드 및 커넥티드카 플랫폼에 통합하는 한편, 경량 소재와 첨단 제어 시스템에 대한 투자를 강화하여 토크 제어를 최적화하고 에너지 손실을 줄이기 위해 노력하고 있습니다. 습식 클러치와 건식 클러치의 설계는 열 관리, 내구성, 비용 효율성 측면에서 개선되고 있습니다. 또한, 차량 진단 시스템과의 소프트웨어 통합을 통해 자율주행차 및 고성능 차량이라는 트렌드에 대응하고 있습니다. 이러한 발전으로 DCT는 현대 자동차 기술 혁신의 핵심 기술로 자리매김하고 있으며, 세계 시장의 성능, 효율성, 지속가능성 요구 사항을 연결하는 역할을 하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035

개시 금액

249억 달러

예측 금액

427억 달러

CAGR

5.6%

습식 DCT 부문은 55%의 점유율을 차지했으며, 2025년에는 140억 달러의 수익을 창출했습니다. 습식 듀얼 클러치 변속기는 오일 윤활 클러치를 채택하고 있어 고토크, 고성능 차량에 선호되고 있습니다. 이 구조는 교통 체증이나 가혹한 조건에서도 방열성, 신뢰성, 성능을 향상시킵니다.

7단 부문은 2025년 52.7%를 차지했으며, 2035년까지 223억 달러에 달할 것으로 전망됩니다. 이 변속기는 효율성, 주행 성능, 신뢰성의 균형을 이루며 부드러운 가속과 정밀한 토크 제어를 실현합니다. 중형 세단, 해치백, 소형 SUV에는 일반적으로 7단 DCT가 적용되어 8단 변속기와 같은 복잡함 없이 최적의 성능을 제공합니다.

북미 듀얼 클러치 변속기 시장은 2026년부터 2035년까지 CAGR 5.2%로 성장하여 2035년까지 52억 달러에 달할 것으로 예상됩니다. 이 지역의 강력한 자동차 산업 기반, 주요 자동차 제조업체의 존재, 고성능 차량의 보급 확대, 특히 프리미엄 및 스포츠카 부문의 DCT 수요를 견인하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2035

제6장 시장 추정 및 예측 : 전송 속도별, 2022-2035

제7장 시장 추정 및 예측 : 파워트레인별, 2022-2035

제8장 시장 추정 및 예측 : 차량별, 2022-2035

제9장 시장 추정 및 예측 : 판매 채널별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM

영문 목차

영문목차

The Global Dual Clutch Transmission Market was valued at USD 24.9 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 42.7 billion by 2035.

DCTs are advanced transmission systems that offer rapid, seamless gear shifts, initially popularized in premium passenger cars and high-performance vehicles, and gradually expanding into commercial vehicles and select motorcycles. Their growing adoption is driven by the pursuit of better fuel efficiency, smoother acceleration, and improved driving dynamics. Manufacturers are increasingly integrating DCTs with hybrid and connected vehicle platforms, while investing in lightweight materials and advanced control systems to optimize torque handling and reduce energy loss. Wet and dry clutch designs are enhanced for heat management, durability, and cost efficiency, while software integration with vehicle diagnostics supports trends in autonomous and performance-oriented vehicles. These developments position DCTs as a key technology for modern automotive innovation, bridging performance, efficiency, and sustainability demands across global markets.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$24.9 Billion

Forecast Value

$42.7 Billion

CAGR

5.6%

The wet DCT segment held 55% share, generating USD 14 billion in 2025. Wet dual clutch transmissions are preferred for high-torque and performance vehicles due to their oil-lubricated clutches, which improve heat dissipation, reliability, and performance under heavy traffic and extreme conditions.

The 7-speed segment accounted for 52.7% in 2025 and is expected to reach USD 22.3 billion by 2035. These transmissions balance efficiency, drivability, and reliability, offering smooth acceleration and precise torque control. Mid-range sedans, hatchbacks, and compact SUVs commonly employ 7-speed DCTs, providing optimal performance without the complexity of 8-speed alternatives.

North America Dual Clutch Transmission Market is projected to reach USD 5.2 billion by 2035, growing at a CAGR of 5.2% from 2026 to 2035. The region's strong automotive base, presence of leading carmakers, and growing adoption of high-performance vehicles drive demand for DCTs, particularly in premium and sports segments.

Key players in the Global Dual Clutch Transmission Market include Magna, ZF Friedrichshafen, BorgWarner, Volkswagen, Aisin, Schaeffler, Great Wall Motors, Dana, TREMEC, and Punch Powertrain. Companies in the Dual Clutch Transmission Market are strengthening their foothold through multiple strategies. They invest heavily in R&D to enhance clutch materials, torque handling, and software integration for hybrid and electric drivetrains. Partnerships with automakers allow tailored solutions for premium, mid-range, and commercial vehicles. Manufacturers are expanding global production facilities to meet rising demand, optimizing supply chains for cost efficiency and faster delivery. Innovation in adaptive and connected transmission systems enhances compatibility with autonomous and smart vehicle platforms. Firms also focus on aftermarket services, retrofitting, and customer support to increase brand loyalty. Strategic collaborations, licensing agreements, and acquisitions help widen geographic reach and consolidate market presence while maintaining competitive advantage.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Transmission Speed

2.2.4 Powertrain

2.2.5 Vehicle

2.2.6 Sales Channel

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Expansion of the worldwide passenger car production

3.2.1.2 Growing adoption of automatic and semi-automatic transmissions

3.2.1.3 Strong penetration of DCT in premium and sports cars

3.2.1.4 Increasing adoption of DCT in hybrid vehicles

3.2.2 Industry pitfalls and challenges

3.2.2.1 Rising penetration of battery electric vehicles (BEVs)

3.2.2.2 Complexity in design and manufacturing

3.2.3 Market opportunities

3.2.3.1 Rising adoption of DCT in hybrid powertrains

3.2.3.2 Growing demand for DCT in compact and mid-segment vehicles

3.2.3.3 Expansion opportunities in emerging automotive markets

3.2.3.4 OEM collaborations and strategic partnerships

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

3.4.1.2 Environmental Protection Agency (EPA)

3.4.1.3 Canadian Motor Vehicle Safety Standards (Transport Canada)

3.4.2 Europe

3.4.2.1 European Committee for Standardization (CEN)

3.4.2.2 European Union Vehicle Type Approval Authorities

3.4.2.3 European Environment Agency (EEA)

3.4.3 Asia Pacific

3.4.3.1 China National Standards (GB / Guobiao Standards)

3.4.3.2 Automotive Research Association of India (ARAI)

3.4.3.3 Japan Automobile Standards Internationalization Center (JASIC)