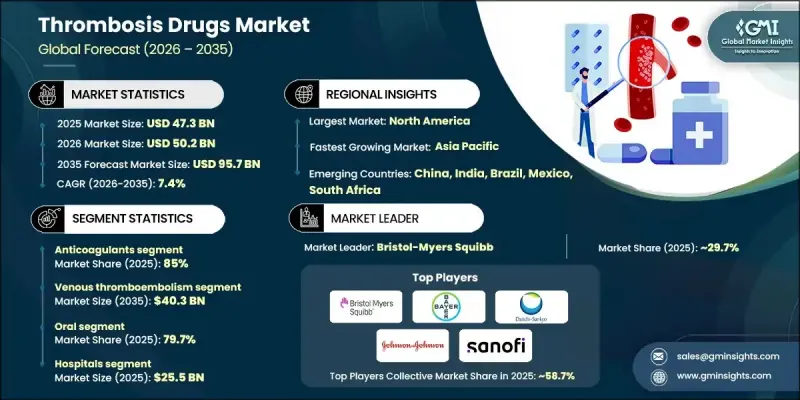

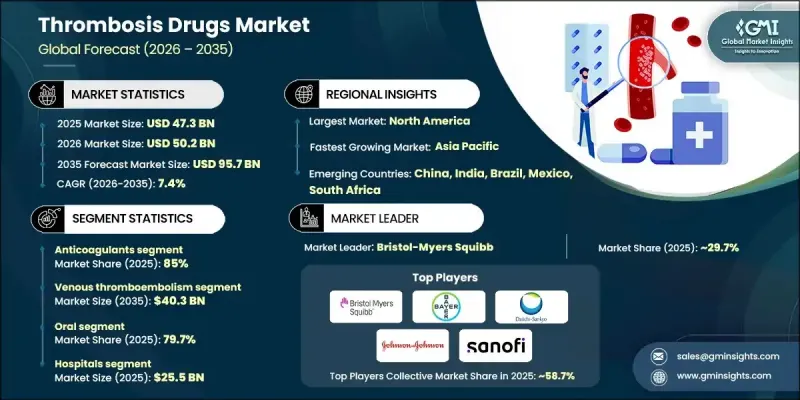

세계의 혈전증 치료제 시장은 2025년에 473억 달러로 평가되었으며, 2035년까지 CAGR 7.4%로 성장하여 957억 달러에 달할 것으로 예측됩니다.

이러한 성장은 심근경색, 폐색전증, 허혈성 뇌졸중 등 심혈관질환의 유병률 증가에 따른 것입니다. 이러한 질환은 빠른 혈류 회복이 필수적이며, 응급의료에서 혈전증 치료는 매우 중요합니다. 혈전증 치료제는 혈관 내 혈전 형성을 예방 및 치료하기 위해 고안된 약물로 응고인자를 억제하는 항응고제, 혈소판 응집을 억제하는 항혈소판제, 기존 혈전을 용해하는 혈전용해제 등이 있습니다. 편의성과 안전성 프로파일을 개선한 직접 경구용 항응고제(DOAC)의 채택이 확대되면서 시장의 성장을 더욱 가속화하고 있습니다. 외과 수술의 증가, 암 관련 혈전증 발생률 증가, 항응고 치료의 장기화, 혈전성 합병증에 대한 임상적 관심의 증가가 복합적으로 작용하여 수요를 촉진하고 있습니다. 새로운 경구용 항응고제(NOAC)는 허혈성 뇌졸중 예방 효과가 입증되어 특히 비판막성 심방세동에서 선호되는 치료제로 떠오르고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 473억 달러 |

| 예측 금액 | 957억 달러 |

| CAGR | 7.4% |

항응고제 부문은 85%의 점유율을 차지했으며, 2025년에는 402억 달러의 매출을 기록했습니다. 이 부문에는 직접 경구용 항응고제, 헤파린, 비타민 K 길항제, 주사용 직접 트롬빈 억제제 등이 포함됩니다. 심방세동, 뇌졸중 예방, 정맥혈전색전증 관리, 수술 후 혈전 예방 등 예방적 및 치료적 환경에서 광범위하게 사용되고 있는 것이 그 장점입니다. 강력한 임상 가이드라인, 의사 숙련도, 예측 가능한 효과, 편리한 투여, 최소한의 모니터링으로 평가되는 직접 경구용 항응고제의 사용이 증가하면서 이 부문에서의 리더십을 더욱 공고히 하고 있습니다.

정맥혈전색전증 부문은 2035년까지 403억 달러에 달할 것으로 예상됩니다. 심부정맥혈전증과 폐색전증을 포함한 이 분야의 성장은 고령화, 비만과 암의 증가율, 입원 기간의 장기화, 수술 건수의 증가에 의해 주도되고 있습니다. 병원 및 외래 진료 환경에서의 혈전 예방 가이드라인에 대한 인식 개선과 시행 확대는 전 세계적으로 진단 및 치료율 상승에 기여하고 있습니다.

북미 혈전증 치료제 시장은 2025년 59.5%의 점유율을 차지했습니다. 이 지역은 첨단 병원, 전문 심장센터, 경구용 및 비경구용 항응고제 접근성 등 탄탄한 의료 인프라의 혜택을 누리고 있습니다. 특히 고령층에서 심혈관질환, 심방세동, 정맥혈전색전증의 높은 유병률이 혈전증 치료에 대한 강력한 수요를 견인하고 있습니다. 새로운 경구용 항응고제(NOAC)의 조기 도입, 지원적인 상환 제도, 의료진들의 혈전 예방 프로토콜에 대한 폭넓은 지식은 이 지역의 선도적 지위를 더욱 공고히 하고 있습니다.

The Global Thrombosis Drugs Market was valued at USD 47.3 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 95.7 billion by 2035.

The growth is driven by the rising prevalence of cardiovascular disorders, including myocardial infarction, pulmonary embolism, and ischemic stroke, which necessitate rapid restoration of blood flow, making thrombosis treatment critical in emergency care. Thrombosis drugs are designed to prevent and treat clot formation in blood vessels, including anticoagulants that inhibit clotting factors, antiplatelet agents that block platelet aggregation, and thrombolytics that dissolve existing clots. The growing adoption of direct oral anticoagulants, which offer convenience and improved safety profiles, has further accelerated market expansion. Increased surgical procedures, rising incidences of cancer-associated thrombosis, and prolonged anticoagulation therapy, alongside growing clinical focus on thrombotic complications, collectively fuel demand. Novel oral anticoagulants (NOACs) emerge as a preferred therapy, particularly for non-valvular atrial fibrillation, due to their proven efficacy in preventing ischemic stroke.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $47.3 Billion |

| Forecast Value | $95.7 Billion |

| CAGR | 7.4% |

The anticoagulants segment held an 85% share, generating USD 40.2 billion in 2025. This segment includes direct oral anticoagulants, heparin, vitamin K antagonists, and injectable direct thrombin inhibitors. Its dominance is attributed to widespread use in both prophylactic and therapeutic settings, including atrial fibrillation, stroke prevention, venous thromboembolism management, and post-surgical thromboprophylaxis. Strong clinical guidelines, physician familiarity, and growing use of direct oral anticoagulants valued for predictable efficacy, convenient dosing, and minimal monitoring have further solidified this segment's leadership.

The venous thromboembolism segment is expected to reach USD 40.3 billion by 2035. It encompasses deep vein thrombosis and pulmonary embolism, with growth driven by aging populations, increasing rates of obesity and cancer, longer hospital stays, and higher volumes of surgical procedures. Greater awareness and implementation of thromboprophylaxis guidelines in both hospital and outpatient settings are contributing to rising diagnosis and treatment rates globally.

North America Thrombosis Drugs Market held a 59.5% share in 2025. The region benefits from a well-established healthcare infrastructure, including advanced hospitals, specialized cardiac centers, and access to both oral and parenteral anticoagulants. High prevalence of cardiovascular diseases, atrial fibrillation, and venous thromboembolism, especially in older populations, drives strong demand for thrombosis therapies. Early adoption of NOACs, supportive reimbursement frameworks, and widespread knowledge of thromboprophylaxis protocols among healthcare professionals further reinforce the region's leadership.

Leading players in the Global Thrombosis Drugs Market include AstraZeneca, Sanofi, Dr. Reddy's Laboratories, Johnson & Johnson, Pfizer, Novartis, Bayer, Boehringer Ingelheim, Microbix Biosystems, Karma Pharmatech, Daiichi Sankyo, Bristol-Myers Squibb, Aspen Pharmacare, Chiesi Farmaceutici, Teva Pharmaceuticals, and Lupin. Key strategies adopted by companies in the Thrombosis Drugs Market to strengthen their market position include heavy investments in research and development to enhance drug efficacy, safety, and patient adherence. Firms are entering strategic collaborations and licensing agreements with hospitals, research institutions, and biotech companies to expand their product portfolios and clinical reach. Expanding into emerging markets and improving supply chain distribution networks ensures wider therapy accessibility.