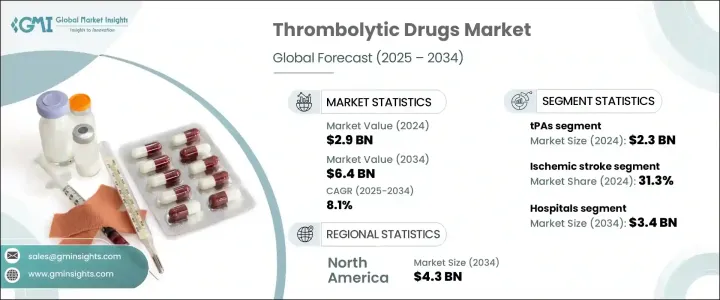

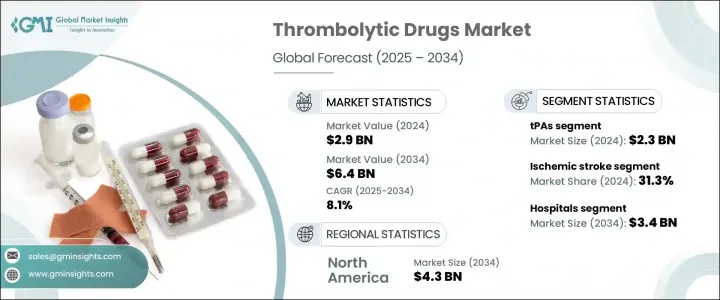

세계의 혈전용해제 시장은 2024년 29억 달러로 평가되었으며 CAGR 8.1%로 성장해 2034년까지 64억 달러에 이를 것으로 추정됩니다.

이 꾸준한 증가는 심장 마비, 뇌졸중, 폐 색전증 및 기타 혈전 관련 질환과 같은 전 세계적으로 심혈관 질환의 부담이 증가하고 있음을 반영합니다. 이러한 추세는 응급 시 효과적으로 투여할 수 있는 즉각적인 혈전 용해제에 대한 큰 수요를 촉구하고 있습니다.

시장을 전진시키는 데 있어서 기술은 중요한 역할을 하고 있습니다. 약제 개발과 약물 전달법의 진보는 혈전 용해 요법의 정확성과 효율 향상에 도움이 되고 있습니다. 이 약들이 가장 많이 사용되는 병원이나 응급 외래에서는 시기 적절한 발견과 신속한 치료가 표준이되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도년 | 2025-2034 |

| 시작 금액 | 29억 달러 |

| 예측 금액 | 64억 달러 |

| CAGR | 8.1% |

혈전 용해제는 종종 선용약이라고 불리며, 다양한 심혈관계 질환에 의해 형성되는 혈전을 용해하는데 필수적입니다. 현장은 조직 플라스미노겐 활성화제(tPAs), 스트렙토키나제, 우로키나제형 플라스미노겐 활성화제(uPAs)와 같은 몇 가지 주요 범주로 구성되며, 그 용도는 주로 병원 및 중증 환자에 대한 치료에 집중되어 있습니다.

이 중 tPAs 분야는 세계 시장을 선도했으며 2024년에는 23억 달러의 매출을 기록했습니다. 8.2%로 성장해 2034년에는 51억 달러에 이를 것으로 예측됩니다. tPA의 사용량 증가의 근본적인 요인의 하나는 세계의 당뇨병 환자의 급증입니다. 당뇨병은 혈관 장애, 혈액 응고 경향의 항진, 대사의 불균형 등을 통해 혈전성 이벤트의 리스크를 높여, 이들 모두가 적극적인 혈전 용해 요법의 필요성을 높여

혈전 용해제로 치료되는 질환으로는 허혈성 뇌졸중이 최대의 적응증이며, 2024년 세계 시장 점유율의 31.3%를 차지하고 있습니다. 뇌졸중 증례의 세계 증가와 더불어 뇌졸중 예방과 관리에 대한 의식 증가가 혈전 용해 요법에 대한 수요를 높입니다.

최종 사용자별로 병원이 2024년 시장의 54.8%를 차지하는 주요 부문이 되었습니다. 7.7%로 성장을 지속하여 2034년에는 34억 달러에 이를 것으로 예측됩니다. 또한, 치명타 케어 인프라에의 세계의 투자에 의해 특히 도시나 선진 헬스 케어 시스템에 있어서, 이러한 치료에의 액세스가 확대되고 있습니다.

지역별로 북미는 2024년 시장을 선도하여 20억 달러의 수익을 올렸습니다. 7.9%로 성장해 2034년에는 43억 달러에 달할 것으로 예측되고 있습니다. 헬스케어 정책도 충실하기 때문에 혈전용해제 수요가 계속 높아지고 있습니다.

경쟁 환경은 주요 기업이 연구 투자를 수행하고 제품 라인을 확대하고 신흥 시장을 목표로 액세스를 확대함으로써 정의됩니다.

The Global Thrombolytic Drugs Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 6.4 billion by 2034. This steady rise reflects the growing burden of cardiovascular diseases across the globe, including heart attacks, strokes, pulmonary embolism, and other clot-related conditions. As sedentary lifestyles, obesity, hypertension, and aging populations become increasingly common, the prevalence of thromboembolic events is accelerating. These trends are driving significant demand for fast-acting clot-dissolving medications that can be administered effectively in emergencies. Health systems are recognizing the urgency of such treatments, especially in acute care settings, where rapid intervention is critical for improving patient outcomes.

Technology is playing a vital role in propelling the market forward. Advancements in drug development and delivery methods are helping enhance the precision and efficiency of thrombolytic therapies. Innovations in dosing and formulation are also supporting broader clinical adoption. Alongside these developments, awareness surrounding early intervention is growing, thanks to improved diagnostic and imaging technologies. Timely detection and prompt treatment are becoming the standard in hospitals and emergency rooms, where these drugs are most commonly used. As clinical practice evolves, so does the need for therapeutics that are not only effective but also safe and easy to administer.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 8.1% |

Thrombolytic drugs, often referred to as fibrinolytic agents, are essential in dissolving blood clots that form due to various cardiovascular conditions. These medications work by activating the body's fibrinolytic system to break down fibrin, the primary protein found in clots. The market comprises several key categories, including tissue plasminogen activators (tPAs), streptokinase, and urokinase-type plasminogen activators (uPAs), with applications mostly concentrated in hospitals and critical care settings.

Among these, the tPAs segment led the global market, generating USD 2.3 billion in revenue in 2024. This segment is expected to rise to USD 5.1 billion by 2034, growing at a CAGR of 8.2%. The dominance of tPAs stems from their high efficacy in clot resolution during critical health events. These agents are widely prescribed due to well-documented clinical benefits when used promptly in acute cases. One of the underlying drivers of increased tPA utilization is the global surge in diabetes cases. The disease heightens the risk of thrombotic events through vascular damage, increased clotting tendencies, and metabolic imbalances, all of which raise the need for aggressive clot-busting therapies.

In terms of medical conditions treated with thrombolytics, ischemic stroke represented the largest indication segment, accounting for 31.3% of the global market share in 2024. This segment is on track to maintain strong growth through 2034, supported by the high incidence of ischemic strokes, which make up the majority of stroke cases globally. These strokes are typically caused by obstructions in cerebral blood flow and require immediate medical attention. The growing number of stroke cases worldwide, combined with rising awareness of stroke prevention and management, is increasing the demand for thrombolytic therapies. Conditions such as diabetes, high blood pressure, and obesity-commonly linked to stroke risk-are further boosting the need for effective medical intervention using these drugs.

By end user, hospitals emerged as the leading segment in 2024, holding a 54.8% share of the market. This segment is expected to reach USD 3.4 billion by 2034, progressing at a CAGR of 7.7%. Hospitals serve as the primary point of care for patients requiring thrombolytic treatment, thanks to their ability to conduct rapid diagnostics and initiate therapy without delay. The increasing frequency of emergency admissions due to heart attacks and strokes continues to support hospital demand. Additionally, global investment in critical care infrastructure is expanding access to such treatments, especially in urban areas and developed healthcare systems. While outpatient centers are gaining traction, hospital settings remain the cornerstone of thrombolytic drug administration.

Regionally, North America led the market in 2024, generating USD 2 billion in revenue. The region is forecasted to reach USD 4.3 billion by 2034, growing at a CAGR of 7.9%. The market leadership of North America can be attributed to its advanced healthcare infrastructure, favorable reimbursement environment, and high prevalence of thrombotic disorders. The increased adoption of advanced therapies and supportive healthcare policies in this region continue to drive the demand for thrombolytics. Additionally, pharmaceutical innovation, a robust clinical pipeline, and strong industry presence contribute to the region's dominance in the global landscape.

The competitive environment is defined by leading players investing in research, expanding product lines, and targeting emerging markets to broaden access. Companies are striving to improve drug safety profiles and streamline delivery methods to maintain their edge in a tightly regulated, performance-focused market. These efforts underscore the ongoing evolution of thrombolytic drug development, shaped by innovation, clinical demand, and strategic positioning.