자동차용 AI 시뮬레이션 및 합성 데이터 생성 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Automotive AI Simulation and Synthetic Data Generation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936478

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 246 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

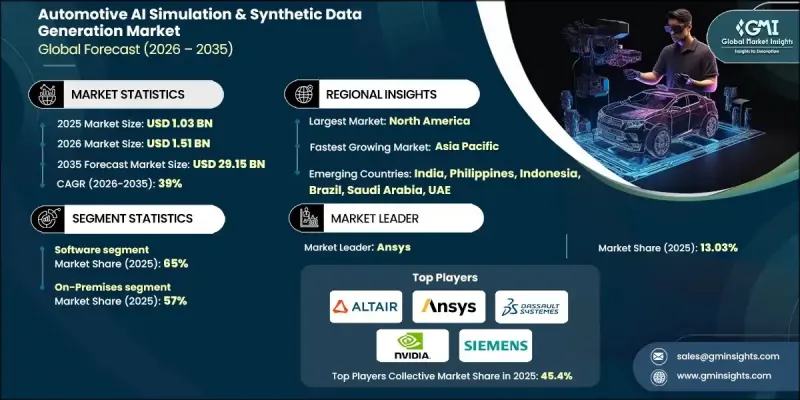

세계의 자동차용 AI 시뮬레이션 및 합성 데이터 생성 시장은 2025년에 10억 3,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 39%로 성장할 전망이며, 291억 5,000만 달러에 이를 것으로 예측됩니다.

이 급속한 확대는 ADAS(선진운전지원시스템) 및 자율주행 기술이 양산 단계로 본격적으로 이행하는 중 차량의 설계 및 검증 방법이 근본적으로 변혁되고 있음을 반영하고 있습니다. AI 구동 시뮬레이션 및 합성 데이터 툴은 복잡한 자동차 소프트웨어의 가상 개발, 대규모 AI 교육 및 안전 검증의 핵심 기반 기술이 되고 있습니다. 이러한 플랫폼을 통해 제조업체 및 공급업체는 방대한 주행 시나리오, 센서 간 상호작용, 환경 변수를 제어된 환경에서 디지털 복제할 수 있어 비용과 시간이 걸리는 현장 테스트에 대한 의존도를 크게 줄일 수 있습니다. 또한 자동차 제조업체, Tier 1 공급업체, 클라우드 인프라 제공업체, 시뮬레이션 소프트웨어 공급업체가 협력하여 개발 워크플로우를 효율화하여 에코시스템 전반의 협력 관계를 강화하여 시장이 더욱 혜택을 누리고 있습니다. 시뮬레이션을 최우선으로 하는 개발 모델은 현재 자율주행 및 ADAS 프로그램에 널리 통합되어 있으며, 통합 솔루션은 엔지니어링의 복잡성 감소, 모델 정밀도 향상, 전체 차량 개발 비용 절감에 기여하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

10억 3,000만 달러

예측 금액

291억 5,000만 달러

CAGR

39%

소프트웨어 부문은 2025년에 65%의 점유율을 차지하였고, 2035년까지 연평균 복합 성장률(CAGR) 38.5%로 성장할 것으로 예측됩니다. 이 이점은 업계가 물리적 프로토타입이 아닌 디지털 환경을 통해 핵심 운전 지능을 구축, 테스트 및 개선하는 소프트웨어 정의 차량으로의 전환을 가속화하고 있음을 반영합니다. 시뮬레이션 소프트웨어는 차량의 거동, 센서 성능 및 교통 역학의 광범위한 가상 테스트를 가능하게 하고 수백만의 이용 사례를 효율적이고 반복적으로 평가할 수 있습니다.

온프레미스 부문은 2025년에 57%의 점유율을 차지하였으며, 2026-2035년 연평균 복합 성장률(CAGR) 37.9%를 나타낼 것으로 예측됩니다. 이러한 추세는 데이터 프라이버시, 지적 재산 보호, 자동차 안전 및 사이버 보안 프레임워크 준수에 대한 엄격한 요구 사항에 의해 추진되고 있습니다. 자동차 제조업체 및 Tier 1 공급업체는 외부 환경에서 제한되는 고도로 민감한 차량 시스템, 지각 로직 및 고유 데이터 세트를 관리합니다. 온프레미스 인프라는 데이터, 시뮬레이션 자산, AI 워크플로우에 대한 완전한 소유권과 거버넌스를 제공하는 동시에 내부 보안 및 규제 기준을 준수합니다.

북미의 자동차용 인공지능 시뮬레이션 및 합성 데이터 생성 시장은 2025년 85%의 점유율을 차지하였으며, 3억 2,830만 달러 규모에 이르렀습니다. 이 지역의 성장은 자율주행 기술 및 ADAS 기술에 대한 강력한 투자 외에도 안전성 검증과 규제 대응에 대한 기대감이 높아짐에 따라 추진되고 있습니다. 조직이 물리적 테스트를 제한하면서 시스템 성능에 대한 높은 신뢰성을 유지하려고 하는 동안 시나리오 기반 시뮬레이션 및 가상 테스트 도입이 가속화되고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

ADAS 및 자율주행차 개발에 대한 수요 증가

차량 소프트웨어 시스템의 복잡화

가상 검증 및 시나리오 기반 테스트에 대한 수요 급증

센서 퓨전 및 지각 시스템에서의 AI/ML 도입 증가

업계의 잠재적 위험 및 과제

높은 초기 투자 비용

시뮬레이션 툴의 복잡성

시장 기회

클라우드 기반 시뮬레이션 Az A 서비스 모델 성장

인증된 가상 검증 프레임워크에 대한 수요 증가

차량 개발에 있어서 디지털 트윈 도입 증가

승용차 이외의 시뮬레이션 용도 확대

성장 가능성 분석

규제 상황

북미

미국-NHTSA 자율주행 시스템 안내 및 자율주행차 시험 이니셔티브

유럽

유럽 연합-유엔 유럽 경제위원회 규칙 R157(ALKS)

독일-자동 운전법

영국-커넥티드 오토메이티드 모빌리티(CAM) 규제

프랑스-자동 운전 차량 실험 프레임워크

아시아태평양

중국-지능형 커넥티드 차량(ICV) 시뮬레이션 기준

일본-국토교통성 자동운전 안전 가이드라인

한국-자동운전차법

싱가포르-자동 운전 차량 안전 평가 프레임워크

라틴아메리카

브라질-국가 지적 이동성, IoT 전략

멕시코-스마트 모빌리티 및 자율주행차 파일럿 규제

칠레-첨단 도로교통 시스템(ITS) 정책

중동 및 아프리카

아랍에미리트(UAE)-두바이 자율 주행 교통 전략

사우디아라비아-비전 2030 스마트 모빌리티 프레임워크

남아프리카-녹색 수송 및 자동 운전 이동성 정책

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

특허 분석

지속가능성 및 환경 영향 분석

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

전망 및 기회

OEM 실장 프레임워크

평가 및 전략

인프라 구축

파일럿 프로그램

통합 및 확장

최적화 및 확장

성공의 중요한 요소

일반적인 함정 및 대책

이용 사례 및 용도 시나리오

도시 자율주행 시뮬레이션

고속도로 자동운전 및 트럭 대열 주행

안전 시험을 위한 엣지 케이스 생성

지각 모델 훈련용 합성 데이터

드라이버 모니터링 시스템의 검증

V2X 통신 시뮬레이션

한랭지 및 극한 환경 하에서의 시험

주차 및 저속 조작

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 제공별(2022-2035년)

소프트웨어

서비스

제6장 시장 추계 및 예측 : 시뮬레이션 유형별(2022-2035년)

센서 시뮬레이션

시나리오 생성

차량 다이나믹스

HIL/SIL 테스트

제7장 시장 추계 및 예측 : 합성 데이터별(2022-2035년)

이미지 및 동영상

표 형식

시계열

기타

제8장 시장 추계 및 예측 : 용도별(2022-2035년)

ADAS 테스트

자율주행차 개발

AI 및 머신러닝 모델 트레이닝

안전성 및 컴플라이언스

설계 검증

제9장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

OEM

Tier 1 공급업체

기술기업

연구기관

제10장 시장 추계 및 예측 : 도입 형태별(2022-2035년)

온프레미스

클라우드 기반

하이브리드

제11장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

세단

해치백

SUV

상용차

경상용차(LCV)

MCV

대형 상용차(HCV)

제12장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

한국

필리핀

인도네시아

싱가포르

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제13장 기업 프로파일

세계 기업

Altair Engineering

Ansys

Autodesk

Dassault Systemes

IBM

MSC Software(Hexagon)

NVIDIA

PTC

Siemens

Synopsys

The MathWorks

지역 기업

AVL List

AVSimulation

dSPACE

ESI Group(Keysight)

IPG Automotive

SIMUL8

신흥 기업

Anyverse

Applied Intuition

Cognata

Foretellix

Mechanical Simulation

MOOG

Parallel Domain

SimScale

AJY

영문 목차

영문목차

The Global Automotive AI Simulation & Synthetic Data Generation Market was valued at USD 1.03 billion in 2025 and is estimated to grow at a CAGR of 39% to reach USD 29.15 billion by 2035.

The rapid expansion reflects a fundamental transformation in how vehicles are designed and validated as advanced driver assistance systems and autonomous technologies move deeper into production. AI-driven simulation and synthetic data tools are becoming core enablers of virtual development, large-scale AI training, and safety validation for increasingly complex automotive software. These platforms allow manufacturers and suppliers to digitally replicate massive volumes of driving scenarios, sensor interactions, and environmental variables in controlled settings, significantly reducing dependence on costly and time-intensive real-world testing. The market is also benefiting from growing collaboration across the ecosystem, as vehicle manufacturers, Tier-1 suppliers, cloud and infrastructure providers, and simulation software vendors align to streamline development workflows. Sim-first development models are now widely embedded into autonomous and ADAS programs, while integrated solutions are helping reduce engineering complexity, improve model accuracy, and lower overall vehicle development costs.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.03 Billion

Forecast Value

$29.15 Billion

CAGR

39%

The software segment accounted for 65% share in 2025 and is forecast to grow at a CAGR of 38.5% through 2035. This dominance reflects the industry's accelerated transition toward software-defined vehicles, where core driving intelligence is built, tested, and refined through digital environments rather than physical prototypes. Simulation software enables extensive virtual testing of vehicle behavior, sensor performance, and traffic dynamics, allowing millions of use cases to be evaluated efficiently and repeatedly.

The on-premises segment held 57% share in 2025 and is expected to grow at a CAGR of 37.9% from 2026 to 2035. This preference is driven by strict requirements around data privacy, intellectual property protection, and compliance with automotive safety and cybersecurity frameworks. Automotive manufacturers and Tier-1 suppliers manage highly confidential vehicle systems, perception logic, and proprietary datasets that are often restricted from external environments. On-premises infrastructure provides full ownership and governance over data, simulation assets, and AI workflows while aligning with internal security and regulatory standards.

North America Automotive AI Simulation & Synthetic Data Generation Market held 85% share and generated USD 328.3 million in 2025. Growth in the country is being fueled by strong investment in autonomous and ADAS technologies, alongside rising expectations for safety validation and regulatory readiness. The adoption of scenario-based simulation and virtual testing is accelerating as organizations seek to limit physical testing while maintaining high confidence in system performance.

Key companies active in the Global Automotive AI Simulation & Synthetic Data Generation Market include NVIDIA, Siemens, Dassault Systemes, Ansys, The MathWorks, dSPACE, Altair Engineering, PTC, Autodesk, and ESI Group. Leading companies in the Automotive AI simulation and synthetic data generation market are strengthening their positions through platform integration, strategic partnerships, and continuous innovation. Many vendors are expanding end-to-end simulation ecosystems that combine scenario creation, sensor modeling, AI validation, and regression testing into unified offerings. Collaboration with OEMs and Tier-1 suppliers is being used to tailor solutions to real-world development needs and accelerate adoption.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Offering

2.2.3 Simulation type

2.2.4 Synthetic data type

2.2.5 Application

2.2.6 End use

2.2.7 Deployment mode

2.2.8 Vehicle

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing demand for ADAS & autonomous vehicle development

3.2.1.2 Rising complexity of vehicle software systems

3.2.1.3 Surge in demand for virtual validation and scenario-based testing

3.2.1.4 Increase in AI/ML adoption for sensor fusion and perception systems

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment costs

3.2.2.2 Complexity of simulation tools

3.2.3 Market opportunities

3.2.3.1 Growth in cloud-based simulation-as-a-service models

3.2.3.2 Increase in demand for certified virtual validation frameworks

3.2.3.3 Rise in digital twin adoption for vehicle development

3.2.3.4 Expansion of simulation use beyond passenger vehicles

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 United States: NHTSA ADS Guidance & AV TEST Initiative.

3.4.2 Europe

3.4.2.1 European Union: UNECE Regulation R157 (ALKS)

3.4.2.2 Germany: Autonomous Driving Act

3.4.2.3 United Kingdom: Connected and Automated Mobility (CAM) Regulations