자동차용 컴퓨터 비전 AI 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Automotive Computer Vision AI Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936477

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 255 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

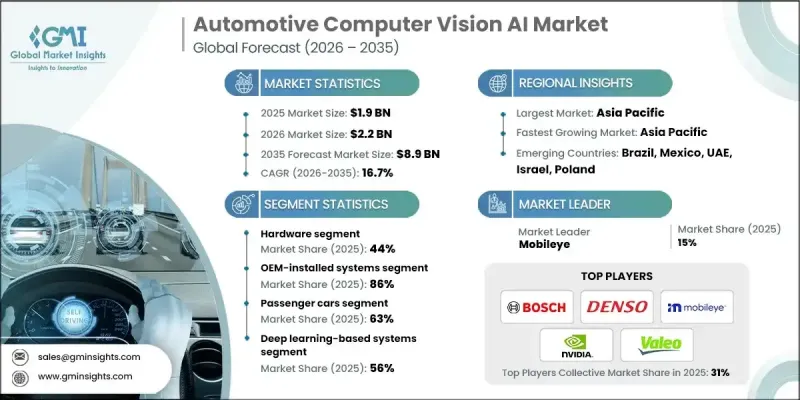

세계의 자동차용 컴퓨터 비전 AI 시장은 2025년 19억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 16.7%로 성장할 전망이며, 89억 달러에 이를 것으로 예측됩니다.

자동차 제조업체는 차량이 도로 상황을 해석하고, 물체를 감지하며, 실시간으로 반응할 수 있도록 비전 기반 AI를 통합하고 있습니다. 이로 인해 안전성과 운전 효율이 크게 향상됩니다. 자동차 분야에서의 디지털 전환의 진전은 승용차 및 상용차에서의 AI 도입을 가속화하고 있습니다. 양산화, 반도체 기술의 혁신, 알고리즘의 개선에 의해 첨단 운전 지원 기술 전체의 비용 절감이 진행되고, 컴퓨터 비전 솔루션은 프리미엄 부문을 넘어 실용화 가능하게 되었습니다. 비전 AI는 이제 옵션 강화 기능이 아닌 차세대 이동성의 핵심 기술로 자리매김하고 있습니다. 업계는 동적 환경에서 지각 정확도를 향상시키는 데이터 중심 학습 아키텍처로 꾸준히 전환하고 있습니다. 이러한 발전이 결합되어 세계 자동차 생태계 전반에 걸쳐 시장의 급속한 침투, 강력한 투자 동향 및 장기 수요를 지원합니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

19억 달러

예측 금액

89억 달러

CAGR

16.7%

첨단 운전 지원 시스템(ADAS) 및 시각 기반 안전 기능은 대중 시장용 차량 및 엔트리 모델에서도 점점 표준 장비화가 진행되고 있습니다. 지난 5년간 ADAS 관련 비용이 40% 삭감된 것으로, 저렴한 가격 및 보급이 진행되고 있습니다. 이 비용 절감은 생산 효율성 향상, 최적화된 AI 모델 및 칩 성능 향상을 반영하여 자동차 제조업체가 컴퓨터 비전 AI를 대규모로 도입할 수 있도록 합니다. 그 결과 차량 구매자는 이제 지능형 안전 기능 및 지각 능력을 프리미엄 추가 장비가 아닌 표준 장비로 기대하게 되었습니다. 자동차 컴퓨터 비전 AI 분야는 세분화된 규칙 기반 워크플로우 없이 원시 센서 데이터를 처리하고 운전 작업을 생성하는 통합 딥러닝 아키텍처로 진화하고 있습니다.

하드웨어 분야는 2025년에 44%의 점유율을 차지했으며, 2026-2035년 CAGR 16.9%로 성장이 예상됩니다. 이 분야에는 카메라, 이미지 센서, AI 가속 칩, 메모리 유닛, 전원 제어 부품, 통합 센서 모듈이 포함됩니다. 자동차 등급 하드웨어는 높은 내구성, 기능 안전 표준 준수, 긴 수명이 요구되며 개발 및 제조 비용이 증가합니다. 이러한 요인으로 인해 차량에서 안정적인 컴퓨터 비전 성능을 실현할 때 하드웨어가 중심적인 역할을 하는 것이 더욱 강화되고 있습니다.

OEM 탑재 솔루션 분야는 2025년에 86%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 17%로 성장할 것으로 예측됩니다. 자동차 제조업체는 규제 적합성, 원활한 차량 통합, 보증 적용 범위, 대규모 도입으로 인한 비용 효율성 관점에서 공장 출하 시 설치 시스템을 선호합니다. 컴퓨터 비전 AI는 여러 차량 카테고리에서 제조 공정 중에 통합되었으며, 이전에는 고가격 모델로 제한된 기능의 신속한 표준화를 지원합니다.

중국의 자동차용 컴퓨터 비전 AI 시장은 2025년에 38%의 점유율을 차지했으며, 2035년까지 14억 달러에 이를 전망이고, CAGR 17.2%로 성장할 것으로 예측됩니다. 이 국가는 지능화 차량에 대한 강력한 정책 지원, 전기 이동성의 보급, 비용 효율적인 국내 공급망의 혜택을 누리고 있습니다. 현지 제조업체는 비전 기반 시스템을 표준 장비로 적극적으로 경쟁하고 있으며 중국의 대규모 도입에서 주도적 입장을 강화하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

차량에 있어서 ADAS(선진 운전 지원 시스템) 도입 확대

자율주행차 및 준자율주행차에 대한 수요 증가

엄격한 안전 및 배출 가스 규제가 AI 기반 비전 시스템 도입 촉진

AI, 머신러닝, 센서 퓨전의 기술적 진보

자동차 제조업체(OEM) 및 Tier 1 공급업체에 의한 스마트 차량 기술에 대한 투자 확대

업계의 잠재적 위험 및 과제

높은 개발 비용 및 통합 비용

센서 퓨전 및 실시간 데이터 처리의 복잡성

시장 기회

자율주행차 및 준자율주행차의 성장

고급 AI 알고리즘으로 인식 능력 향상

커넥티드카 기술과의 통합

차내 모니터링 및 안전 기능에 대한 수요 증가

자동차 제조업체 및 기술 제공업체 간 제휴

신흥 자동차 시장에서의 확대

성장 가능성 분석

규제 상황

북미

미국-FMVSS 및 NHTSA 가이드라인

캐나다-자동차 안전 규제(MVSR)

유럽

독일-EU 일반안전규제(GSR)

영국-도로 차량(인가) 규칙

프랑스-EU 자율주행차 및 도로 안전 틀

이탈리아-국가 도로 안전 계획(PNSS)

아시아태평양

중국-GB/T규격 및 GB규격

인도-자동차(개정)법 및 AIS 기준

일본-도로교통법 및 국토교통성 자율주행 가이드라인

호주-호주 설계 규칙(ADR)

LATAM

멕시코-NOM 차량 안전 기준

아르헨티나-국가교통법 24.449

중동 및 아프리카

남아프리카공화국-국도교통법(1996년)

사우디아라비아-교통법규 및 비전 2030 수송 이니셔티브

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

특허 분석

이용 사례 및 성공 사례

지속가능성 및 환경면

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

전망 및 기회

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

하드웨어

카메라(모노, 스테레오, 서라운드, 적외선)

센서(LiDAR, 레이더, 초음파)

프로세서 및 에지 AI 칩

소프트웨어

인공지능(AI) 및 머신러닝 알고리즘

컴퓨터 비전 플랫폼

화상 처리 및 물체 검출 소프트웨어

서비스

시스템 통합

컨설팅 및 커스터마이즈

도입 및 설치

보수 및 서포트

제6장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

해치백

SUV

세단

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

전기자동차(EV)

자율주행차

제7장 시장 추계 및 예측 : 기술별(2022-2035년)

머신 비전 기반 시스템

딥러닝 기반 시스템

센서 퓨전 기술에 기반한 시스템

제8장 시장 추계 및 예측 : 도입 형태별(2022-2035년)

OEM

애프터마켓

제9장 시장 추계 및 예측 : 용도별(2022-2035년)

ADAS(선진 운전 지원 시스템)

전방 충돌 경보(FCW)

자동 긴급 브레이크(AEB)

차선 일탈 경보(LDW)

차선 유지 지원 시스템(LKA)

어댑티브 크루즈 컨트롤(ACC)

교통 표지 인식(TSR)

블라인드 스팟 감지(BSD)

주차 지원 및 서라운드 뷰 모니터

자율주행

물체 및 보행자의 검출

도로 끝 및 차선 경계 검출

빈 공간 감지

환경 매핑

경로 계획 지원

차내 모니터링 시스템

드라이버 모니터링 시스템(DMS)

승무원 모니터링 시스템(OMS)

제스처 인식

안전벨트 및 어린이용 시트 사용 감지 시스템

기타

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

네덜란드

스웨덴

덴마크

폴란드

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

이스라엘

제11장 기업 프로파일

세계 기업

Aptiv PLC

Continental

Denso

Intel

Magna International

Mobileye

NVIDIA

Qualcomm Technologies

Robert Bosch

Valeo

지역 기업

Aisin Seiki

Hitachi Astemo

Hyundai Mobis

Panasonic Automotive

Renesas Electronics

Samsung Electronics

ZF Friedrichshafen

신흥 기술 이노베이터

Ambarella

Arbe Robotics

DeepRoute.ai

Ficosa International

Horizon Robotics

Innoviz Technologies

StradVision

Veoneer

AJY

영문 목차

영문목차

The Global Automotive Computer Vision AI Market was valued at USD 1.9 billion in 2025 and is estimated to grow at a CAGR of 16.7% to reach USD 8.9 billion by 2035.

Automotive manufacturers are embedding vision-based AI to enable vehicles to interpret road conditions, detect objects, and react in real time, significantly improving safety and driving efficiency. The ongoing digital transformation of the automotive sector continues to accelerate adoption across passenger and commercial vehicles. Cost reductions across advanced driver assistance technologies, driven by scale manufacturing, semiconductor innovation, and improved algorithms, are making computer vision solutions viable beyond premium segments. Vision AI is now positioned as a core enabler of next-generation mobility rather than an optional enhancement. The industry is steadily shifting toward data-driven learning architectures that improve perception accuracy in dynamic environments. These developments collectively support rapid market penetration, strong investment momentum, and long-term demand across global automotive ecosystems.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.9 Billion

Forecast Value

$8.9 Billion

CAGR

16.7%

Advanced driver assistance and vision-based safety features are increasingly offered across mass-market and entry-level vehicles. A 40% reduction in ADAS-related costs over the past five years has improved affordability and adoption. This decline reflects production efficiencies, optimized AI models, and improved chip performance, enabling automakers to deploy computer vision AI at scale. As a result, vehicle buyers now expect intelligent safety and perception capabilities as standard offerings rather than premium add-ons. The automotive computer vision AI landscape is evolving toward unified deep learning architectures that process raw sensor data and generate driving actions without segmented rule-based workflows.

The hardware segment held 44% share in 2025, growing at a CAGR of 16.9% from 2026 to 2035. This segment includes cameras, image sensors, AI acceleration chips, memory units, power control components, and integrated sensor modules. Automotive-grade hardware requires high durability, functional safety compliance, and long operational life, which increases development and production costs. These factors reinforce the central role of hardware in enabling reliable computer vision performance in vehicles.

The OEM-installed solutions segment held an 86% share in 2025 and is projected to grow at a CAGR of 17% through 2035. Automakers prefer factory-installed systems due to regulatory alignment, seamless vehicle integration, warranty coverage, and cost efficiencies achieved through large-scale deployment. Computer vision AI is being embedded during manufacturing across multiple vehicle categories, supporting rapid standardization of features that were once limited to higher-priced models.

China Automotive Computer Vision AI Market held 38% share in 2025 and is forecast to reach USD 1.4 billion by 2035, growing at a CAGR of 17.2%. The country benefits from strong policy support for intelligent vehicles, widespread adoption of electric mobility, and cost-efficient domestic supply chains. Local manufacturers actively compete by integrating vision-based systems as standard features, reinforcing China's leadership in large-scale deployment.

Key companies operating in the Global Automotive Computer Vision AI Market include NVIDIA, Robert Bosch, Mobileye, Continental, Qualcomm Technologies, Magna, Denso, Intel, Valeo, and Aptiv. Companies in the automotive computer vision AI market focus on vertical integration, long-term OEM partnerships, and continuous investment in AI model optimization to strengthen their market position. Many players prioritize scalable hardware-software platforms that can be deployed across multiple vehicle models and regions. Strategic collaborations with semiconductor manufacturers help ensure access to high-performance, automotive-grade chips. Firms also invest heavily in data acquisition and simulation to improve model accuracy and reliability. Expanding manufacturing footprints and localizing supply chains allow companies to reduce costs and meet regional regulatory requirements.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.3 Research trail and confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Best estimates and calculations

1.6.1 Base year calculation for any one approach

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Components

2.2.3 Vehicles

2.2.4 Technology

2.2.5 Deployment Mode

2.2.6 Application

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Increasing adoption of advanced driver assistance systems (ADAS) in vehicles

3.2.1.3 Rising demand for autonomous and semi-autonomous vehicles

3.2.1.4 Stringent safety and emission regulations encouraging AI-based vision systems

3.2.1.5 Technological advancements in AI, machine learning, and sensor fusion

3.2.1.6 Growing investment by OEMs and Tier-1 suppliers in smart vehicle technologies

3.2.2 Industry pitfalls and challenges

3.2.2.1 High development and integration costs

3.2.2.2 Complexity in sensor fusion and real-time data processing

3.2.3 Market opportunities

3.2.3.1 Growth of autonomous and semi-autonomous vehicles

3.2.3.2 Advanced AI algorithms for better perception

3.2.3.3 Integration with connected vehicle technologies

3.2.3.4 Rising demand for in-cabin monitoring and safety features

3.2.3.5 Collaborations between OEMs and tech providers

3.2.3.6 Expansion in emerging automotive markets

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 US- FMVSS and NHTSA guidelines

3.4.1.2 Canada - Motor vehicle safety regulations (MVSR)

3.4.2 Europe

3.4.2.1 Germany- EU General Safety Regulation (GSR)

3.4.2.2 UK- Road Vehicles (Approval) Regulations

3.4.2.3 France- EU AV and road safety frameworks

3.4.2.4 Italy- National Road Safety Plan (PNSS)

3.4.3 Asia Pacific

3.4.3.1 China- GB/T and GB standards

3.4.3.2 India- Motor Vehicles (Amendment) Act and AIS standards

3.4.3.3 Japan- Road Traffic Act and MLIT autonomous driving guidelines

3.4.3.4 Australia- Australian Design Rules (ADR)

3.4.4 LATAM

3.4.4.1 Mexico- NOM vehicle safety standards

3.4.4.2 Argentina- National traffic law 24.449

3.4.5 MEA

3.4.5.1 South Africa- National road traffic act (1996)

3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives