트럭 플래투닝 시장의 성장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)

Truck Platooning Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928986

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

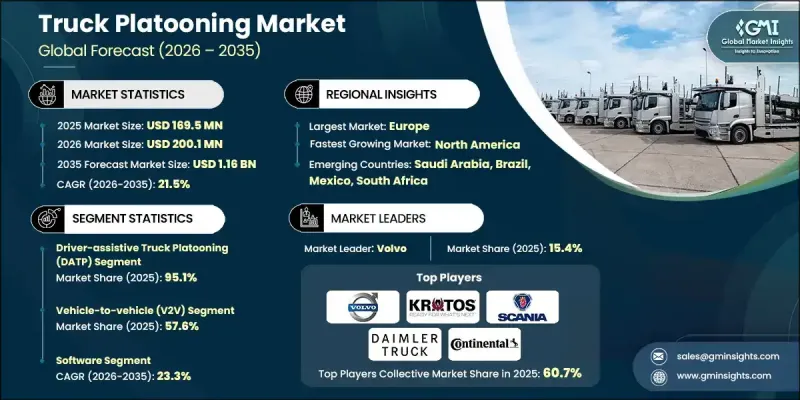

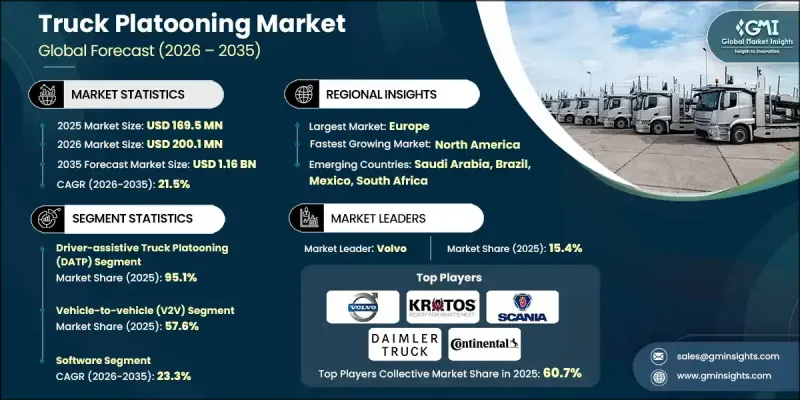

세계의 트럭 플래투닝 시장은 2025년에 1억 6,950만 달러로 평가되었으며, 2035년까지 CAGR 21.5%로 성장하여 11억 6,000만 달러에 달할 것으로 예측됩니다.

이러한 시장 성장은 효율성, 연료 절감, 빈번하게 이용되는 노선의 안전성 향상에 대한 물류 및 운송 기업의 관심 증가에 의해 주도되고 있습니다. 각국 정부는 도로 인프라, 도입 비용, 안전성, 위험 관리 등의 요소를 신중하게 평가하면서 파일럿 프로그램이나 도로 테스트를 적극적으로 지원하고 있습니다. 트럭 플래투닝 기술이 성숙하고 상업적으로 실현 가능해짐에 따라, 주요 물류 기업 및 E-Commerce 기업들은 플래투닝을 도입하고, 자사 차량군에 플래투닝을 도입하여 업무 효율성을 향상시킬 것으로 예상됩니다. 규제 측면의 지원이 강화되고, 운송 네트워크가 정비되고, 화물 운송량이 많은 지역에서는 보다 빠른 도입이 이루어질 것으로 예상됩니다. 또한, 커넥티드카 기술의 보급, 화물 운송 업무의 디지털화 진전, 물류업계의 지속가능성에 대한 지속적인 노력도 시장 성장에 기여하고 있습니다.

시장 범위

시작 연도

2025년

예측 기간

2026-2035

개시시 가치

1억 6,950만 달러

예측 금액

11억 6,000만 달러

CAGR

21.5%

운전자 지원형 트럭 플래투닝(DATP) 부문은 2025년 95.1%의 점유율을 차지했습니다. DATP 시스템에서는 적어도 한 명의 운전자가 대열을 이끌어야 하며, 뒤따라오는 트럭은 반자동 운전 상태를 유지해야 합니다. 완전자율주행 플래투닝은 도로 인프라의 제약, 교통 밀도, 규제 제약으로 인해 도전에 직면해 있기 때문에 당분간 이 우위는 지속될 것으로 예상됩니다. 인간 운전자에 대한 의존도는 안전을 보장하는 동시에 물류 사업자가 연료 소비를 줄이고 대열 효율을 향상시키는 이점을 누릴 수 있게 해줍니다. DATP는 또한 기술 및 규제 프레임워크가 완전 자율주행 솔루션을 향해 성숙해가는 과정에서 차량 그룹에 실용적인 전환 단계를 제공합니다.

차량 간 통신(V2X) 기술 부문은 2026년부터 2035년까지 CAGR 23.1%로 성장할 것으로 예상됩니다. V2X는 차량, 인프라, 운전 지원 시스템 간의 원활한 연결을 가능하게 하며, 대열 내 실시간 연계를 실현합니다. 이를 도입하면 대열운행의 효율성, 안전성, 정확성이 향상되고, 보다 원활한 가속, 제동, 경로관리가 가능해집니다. V2X가 성숙해짐에 따라 디지털 트윈 시뮬레이션, 자율주행 차량 제어와 같은 첨단 기술과의 통합이 진행되어 트럭 대열 주행 시스템의 성능과 확장성이 더욱 향상될 것으로 기대됩니다.

미국 트럭 플래투닝 시장은 2025년 5,300만 달러 규모에 달할 것으로 예상됩니다. 정부 정책과 연방 및 주정부 기관 간의 협력으로 폐쇄된 시험장에서의 테스트에서 일반 고속도로에서 실제 화물 운송 업무로 전환이 진행되고 있습니다. 미국 교통부는 트럭 플래투닝을 화물 운송에 있어 자율주행차량의 초기 적용 사례 중 하나로 보고, 안전 규정 통일, 인프라 구축, 운영 전략 수립을 위한 주 간 협력을 추진하고 있습니다. 운전 지원 시스템 도입, 지원적 법제 정비, 장거리 운송 네트워크의 효율성 향상과 비용 절감의 필요성에 의해 성장이 촉진되고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

비용 구조

각 단계의 부가가치

밸류체인에 영향을 미치는 요인

디스럽션

업계에 대한 영향요인

성장 촉진요인

연료비 급등에 따른 절감의 필요성

차량간 통신(V2V) 기술 진전

ADAS(첨단 운전자 보조 시스템) 보급 확대

커넥티드·자율주행 모빌리티에 대한 정부 지원

업계의 잠재적 리스크와 과제

사이버 보안과 데이터 프라이버시에 관한 우려사항

신흥 경제국의 인프라 정비 지연

시장 기회

레벨 2- 4자율주행 트럭 솔루션과의 통합

전용 화물 회랑의 도입

자동차 제조업체, 플릿 사업자, 기술 프로바이더 간의 파트너십

대규모 물류·EC 플릿에 의한 도입 상황

성장 가능성 분석

규제 상황

북미

미국 연방 자율주행차 정책 가이던스(NHTSA 가이드라인)

연방 자율주행차 관련 법안

캐나다 운송 성 가이드라인

주 마다 자율주행차 관련 법규

유럽

유엔 규칙 제 157호-자동차 섬유지시스템(ALKS)

EU규칙(EU)

자율주행 법

아시아태평양

중국 자율주행 도로 시험 규제

일본의 도로 교통법 및 자동차 운송 사업법

ASEAN의 자율주행차 현황

라틴아메리카

브라질 자율주행차 시험 가이드라인

칠레의 자율주행차 파일럿 사업 인가

RCEP 지역 기술 협력 프레임워크

중동 및 아프리카

UAE/두바이 자율주행 운송 전략 및 트럭 프레임워크

남아프리카공화국 자율주행/커넥티드카 정책 초안

Porters 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

비용 내역 분석

지속가능성과 환경 영향

환경 영향 평가

사회적 영향과 지역사회에 대한 기여

거버넌스와 기업 사회적 책임

지속가능한 금융과 투자 동향

사례 연구

플릿 경제성, 투자 이익률(ROI) 및 회수기간 분석

상용화 준비 상황과 도입 성숙도 평가

유망한 회랑 및 사용 사례 우선순위 지정

하드웨어 아키텍처와 초기 투자 분석

소프트웨어 및 서비스 수익화 모델

플래투닝 소프트웨어 스택

벤더가 채용하는 가격 모델

구독 및 지속 과금 구조

운영 서비스 비용

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴·협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 플래투닝에 의한 2022-2035

운전 지원형 트럭 플래투닝(DATP)

자율주행 트럭 플래투닝

제6장 시장 추정 및 예측 : 구성요소별, 2022-2035

하드웨어

레이더

LiDAR

카메라

기타 하드웨어

소프트웨어

서비스

제7장 시장 추정 및 예측 : 통신 기술별, 2022-2035

차량간 통신(V2V)

차량과 인프라 간의 통신(V2I)

Vehicle-to-Everything(V2X)

제8장 시장 추정 및 예측 : 차량별, 2022-2035

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

제9장 시장 추정 및 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

베네룩스

아시아태평양

중국

인도

일본

한국

ANZ

싱가포르

말레이시아

인도네시아

베트남

태국

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제10장 기업 개요

세계 기업

Daimler Truck

Volvo

Scania

Continental

IVECO

MAN Truck & Bus

DAF Trucks

ZF Friedrichshafen

Robert Bosch

Knorr-Bremse

Plus(PlusAI)

지역 기업

Kratos Defense & Security Solutions

Waabi

Gatik

Bendix Commercial Vehicle Systems

Denso

Hyundai Motor

신흥 기업

UD Trucks

Hino Motors

Cohda Wireless

KSM

영문 목차

영문목차

The Global Truck Platooning Market was valued at USD 169.5 million in 2025 and is estimated to grow at a CAGR of 21.5% to reach USD 1.16 billion by 2035.

The market growth is driven by increasing interest from logistics and transportation companies seeking efficiency, fuel savings, and safety improvements along frequently used routes. Governments worldwide are actively supporting pilot programs and on-road trials, carefully evaluating factors such as road infrastructure, deployment costs, safety, and risk management. As truck platooning technology matures and becomes commercially viable, major logistics and e-commerce players are expected to be early adopters, deploying platooning in their fleets to improve operational efficiency. Regions with strong regulatory support, robust transportation networks, and higher freight volumes are poised to experience faster adoption. The market is also benefiting from the rise of connected vehicle technologies, increasing digitalization in freight operations, and the ongoing push toward sustainability in the logistics industry.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$169.5 Million

Forecast Value

$1.16 Billion

CAGR

21.5%

The driver-assistive truck platooning (DATP) segment held a 95.1% share in 2025. DATP systems require at least one driver to lead the convoy, while following trucks remain semi-automated. This dominance is expected to continue in the near term as fully autonomous platooning faces challenges due to road infrastructure limitations, traffic density, and regulatory constraints. The reliance on a human operator ensures safety while allowing logistics operators to benefit from reduced fuel consumption and improved convoy efficiency. DATP also provides a practical transition stage for fleets as technology and regulatory frameworks mature toward fully autonomous solutions.

The vehicle-to-everything (V2X) communication technology segment is projected to grow at a CAGR of 23.1% from 2026 to 2035. V2X enables seamless connectivity between vehicles, infrastructure, and driver assistance systems, allowing real-time coordination within platoons. Its adoption is driving efficiency, safety, and precision in convoy operations, enabling smoother acceleration, braking, and route management. As V2X matures, it is expected to integrate with advanced technologies such as digital twin simulations and autonomous vehicle controls, further enhancing the performance and scalability of truck platooning systems.

U.S. Truck Platooning Market reached USD 53 million in 2025. The market is transitioning from closed-track testing to actual freight operations on public highways, supported by government policies and collaborative efforts between federal and state agencies. The U.S. Department of Transportation has identified truck platooning as one of the earliest applications of automated vehicles in freight, encouraging partnerships between states to align safety regulations, develop infrastructure, and plan operational strategies. Growth is driven by the adoption of driver-assistive systems, supportive legislation, and the need for greater efficiency and cost savings in long-haul transportation networks.

Major players operating in the Global Truck Platooning Market include MAN Truck & Bus, Daimler Truck, Volvo, IVECO, Robert Bosch, Kratos, Scania, Knorr-Bremse, Continental, and DAF Trucks. These companies lead through technological innovation, strategic partnerships, and early involvement in pilot programs, ensuring strong positions in the emerging truck platooning market. They continue to invest in R&D, autonomous driving technologies, and connected vehicle systems to meet evolving market demands and regulatory requirements. Companies in the Global Truck Platooning Market are employing several strategies to strengthen their foothold. They focus on technological innovation, including the development of V2X-enabled systems, driver-assistive solutions, and autonomous-ready platooning platforms. Strategic partnerships with logistics operators, e-commerce companies, and government agencies accelerate testing, adoption, and infrastructure readiness. Mergers and acquisitions are used to consolidate expertise, expand geographic reach, and enhance product portfolios.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Platooning

2.2.3 Component

2.2.4 Communication Technology

2.2.5 Vehicle

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising fuel cost reduction imperative

3.2.1.2 Advancements in vehicle-to-vehicle (V2V) communication

3.2.1.3 Growing adoption of advanced driver assistance systems (ADAS)

3.2.1.4 Government support for connected and autonomous mobility

3.2.2 Industry pitfalls and challenges

3.2.2.1 Cybersecurity and data privacy concerns

3.2.2.2 Limited infrastructure readiness in emerging economies

3.2.3 Market opportunities

3.2.3.1 Integration with level 2-4 autonomous trucking solutions

3.2.3.2 Deployment in dedicated freight corridors

3.2.3.3 Partnerships between OEMs, fleet operators, and tech providers

3.2.3.4 Adoption by large logistics and e-commerce fleets

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S. Federal AV Policy Guidance (NHTSA Guidelines)

3.4.1.2 Federal AV Legislation Bills

3.4.1.3 Transport Canada Guidelines

3.4.1.4 State Autonomous Vehicle Laws

3.4.2 Europe

3.4.2.1 UN Regulation No. 157 - Automated Lane Keeping Systems (ALKS)

3.4.2.2 EU Regulation (EU)

3.4.2.3 Automated Driving Act

3.4.3 Asia Pacific

3.4.3.1 China Autonomous Driving Road Test Regulations

3.4.3.2 Japan Road Traffic Act & Road Transport Vehicle Act

3.4.3.3 ASEAN Autonomous Vehicle Landscape

3.4.4 Latin America

3.4.4.1 Brazil Autonomous Vehicle Testing Guidelines