자동차 통신 기술 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)

Automotive Communication Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928981

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

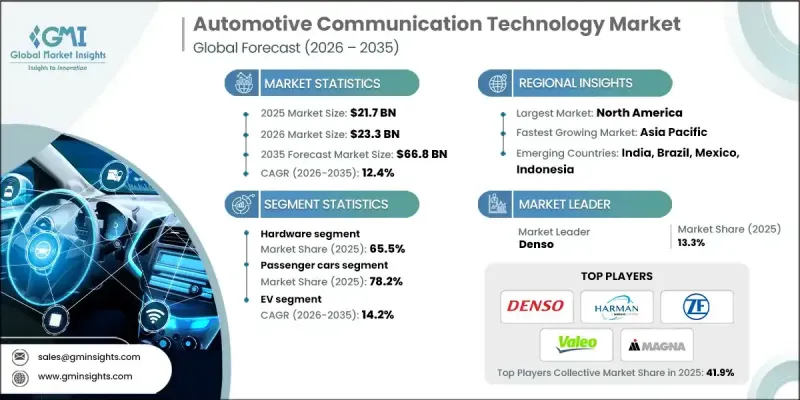

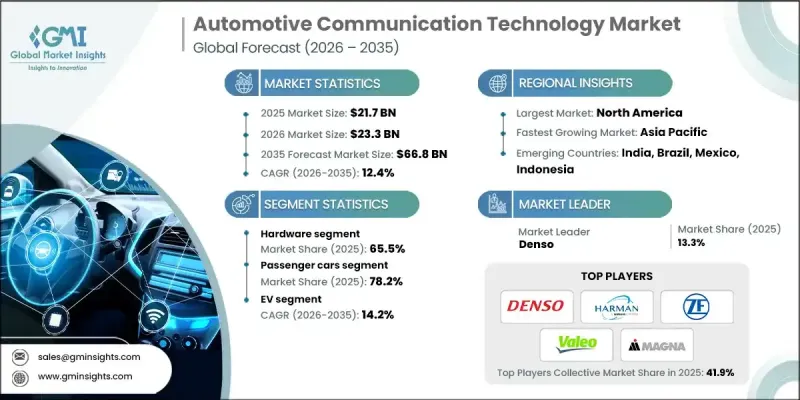

세계의 자동차 통신 기술 시장은 2025년에 217억 달러로 평가되었으며, 2035년까지 CAGR 12.4%로 성장하여 668억 달러에 달할 것으로 예측됩니다.

시장 확대는 커넥티드카와 데이터 집약형 차량으로의 전환에 의해 촉진되고 있습니다. 자동차 제조업체와 공급업체들은 차량과 차량, 인프라, 클라우드 기반 서비스와의 통신을 가능하게 하는 기술 채택을 가속화하고 있습니다. 여기에는 텔레매틱스 제어 장치, 네트워크 모듈과 같은 물리적 구성요소와 커넥티드 서비스를 지원하는 소프트웨어 플랫폼이 모두 포함됩니다. 증가하는 데이터 요구사항에 대응하고 차량 내 경험을 향상시킬 수 있는 차세대 커넥티비티 솔루션이 개발되고 있습니다. 이해관계자들은 차량이 각기 다른 시장의 안전, 성능, 규정 준수 요건을 충족할 수 있도록 전 세계적으로 표준과 통신 프로토콜의 통일을 추진하고 있습니다. 기존 네트워크에서 고속 이더넷 기반 시스템으로의 전환과 존 아키텍처의 채택은 현대 차량에 증가하는 센서, 카메라, 컨트롤러의 관리를 돕습니다. 차량 운영사 및 자동차 제조업체들은 텔레매틱스와 실시간 데이터를 활용하여 유지보수 최적화, 효율성 향상, 운영 비용 절감 및 커넥티드 기술의 가치를 강화하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035

개시시 가치

217억 달러

예측 금액

668억 달러

CAGR

12.4%

하드웨어 부문은 2025년 65.5%의 점유율을 차지했습니다. 하드웨어는 ECU, 트랜시버, 와이어링 하니스, 게이트웨이, 센서, 커넥터 등 자동차 통신에서 여전히 중요한 역할을 하고 있습니다. 차량에 ADAS, 인포테인먼트, 파워트레인 관리를 위한 첨단 전자 시스템이 탑재됨에 따라 강력한 통신 하드웨어의 필요성이 증가하고 있습니다. 이러한 구성요소는 소프트웨어로 대체할 수 없으며, 신뢰할 수 있는 차량 내 네트워크와 데이터 흐름에 필수적입니다.

승용차 부문은 2025년 78.2%의 점유율을 차지했으며, 2035년까지 495억 달러에 달할 것으로 전망됩니다. 이 부문이 주도적인 이유는 승용차가 대량 생산되고 새로운 통신 기술을 빠르게 채택하기 때문입니다. V2X, 텔레매틱스, 첨단 차량 내 네트워크 등의 기능이 표준 또는 중급 옵션으로 장착되고 있으며, 대중 시장용 차량 전반에 걸쳐 안전, 인포테인먼트, 운전 보조 기능이 향상되고 있습니다.

미국 자동차 통신 기술 시장은 2025년 55억 달러에 달했습니다. 미국의 주요 동향은 차량과 모든 사물(V2X) 간의 통신 도입 증가입니다. 이를 통해 차량은 인프라, 다른 차량, 네트워크와 정보를 교환할 수 있습니다. 이 기술은 안전과 교통 관리 개선을 목적으로 추진되고 있으며, 스마트 시티 구상 및 시범 프로그램을 통해 지원되고 있습니다. 자동차 제조업체와 기술 기업들은 CAN, LIN과 같은 기존 차량용 프로토콜과 새로운 이더넷 기반 시스템을 유지하면서 V2X를 추진하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

비용 구조

각 단계의 부가가치

밸류체인에 영향을 미치는 요인

디스럽션

업계에 대한 영향요인

성장 촉진요인

차량 전동화와 소프트웨어 정의 차량 진전

ADAS(첨단 운전자 보조 시스템)의 통합 확대

차량용 인포테인먼트 및 커넥티비티에 대한 수요 증가

자율주행차 및 준 자율주행차로의 전환

업계의 잠재적 리스크와 과제

네트워크 통합과 상호운용성 복잡성

사이버 보안과 데이터 프라이버시에 관한 우려

시장 기회

V2X(Vehicle-to-Everything) 통신 성장

5G 대응 자동차 네트워크 보급 확대

전기 상용차 및 자율주행 상용차 확대

AI 기반 차량용 데이터 처리의 통합

성장 가능성 분석

규제 상황

북미

자동차 기술회(SAE) J2735

전기 전자 기술자 협회(IEEE)

전용 단거리 통신(DSRC) 프로토콜

유럽

유럽 통신 표준화 기구(ETSI)

셀룰러 V2X(C-V2X) 통신규격

아시아태평양

차량 네트워크 통신 프로토콜(중국)

자동차 산업 표준 140(AIS 140, 인도)

라틴아메리카

국제 통신 연합 권고

ISO 21217

중동 및 아프리카

SHC 801-자율주행차 요건

국가 전기자동차 정책

Porters 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

비용 내역 분석

지속가능성과 환경에 대한 영향

환경 영향 평가

사회적 영향과 지역사회에 대한 기여

거버넌스와 기업 사회적 책임

지속가능한 금융과 투자 동향

사례 연구

향후 전망과 기회

자동차용 E/E 아키텍처의 진화

분산형, 도메인별, 존별 아키텍처

차량용 네트워크 프로토콜에 대한 영향

ECU 및 와이어 하니스의 복잡성 절감

OEM 로드맵 타임라인(2025-2035)

통신 프로토콜 성능 벤치마킹

소프트웨어 정의 차량(SDV) 실현 가능성 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴·협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 구성요소별, 2022-2035

하드웨어

트랜시버

커넥터 및 케이블

게이트웨이 및 도메인 컨트롤러

소프트웨어

서비스

제6장 시장 추정 및 예측 : 버스 모듈별, 2022-2035

로컬 인터커넥트 네트워크(LIN)

컨트롤러 에어리어 네트워크(CAN)

FlexRay

미디어 지향 시스템 운송(MOST)

이더넷

제7장 시장 추정 및 예측 : 접속 방식별, 2022-2035

차량용/내부 통신 기술

외부 통신 기술

제8장 시장 추정 및 예측 : 차량별, 2022-2035

승용차

해치백

SUV

세단

상용차

소형 상용차(LCV)

MCV

대형 상용차(HCV)

제9장 시장 추정 및 예측 : 차종별, 2022-2035

이코노미

중형차

고급

제10장 시장 추정 및 예측 : 추진력별, 2022-2035

내연기관(ICE)

전기자동차(EV)

하이브리드

제11장 시장 추정 및 예측 : 용도별, 2022-2035

파워트레인 및 섀시

바디 컨트롤과 쾌적성

인포테인먼트 및 텔레매틱스

안전·ADAS

기타

제12장 시장 추정 및 예측 : 판매 채널별, 2022-2035

OEM

애프터마켓

제13장 시장 추정 및 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

베네룩스

아시아태평양

중국

인도

일본

한국

ANZ

싱가포르

말레이시아

인도네시아

베트남

태국

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제14장 기업 개요

세계 기업

Robert Bosch

Continental

NXP Semiconductors

Infineon

Denso

Qualcomm

STMicroelectronics

Texas Instruments

Renesas Electronics

Intel

Harman International

Broadcom

ON Semiconductor

ZF Friedrichshafen

Valeo

Magna

Mitsubishi Electric

Aptiv

Yazaki

Autoliv

지역 기업

Vector Informatik

Melexis

TTTech Auto

Autotalks

Cohda Wireless

LG Electronics

Lear Corporation

Delphi Technologies

신흥 기업

iWave Systems

Marben Products

Danlaw

Ficosa Internacional

KSM

영문 목차

영문목차

The Global Automotive Communication Technology Market was valued at USD 21.7 billion in 2025 and is estimated to grow at a CAGR of 12.4% to reach USD 66.8 billion by 2035.

The market's expansion is driven by the shift toward connected and data-intensive vehicles. Automakers and suppliers are increasingly adopting technologies that enable vehicles to communicate with each other, infrastructure, and cloud-based services. This includes both physical components, such as telematics control units and network modules, and software platforms that support connected services. Next-generation connectivity solutions are being developed to handle growing data requirements and enhance in-vehicle experiences. Industry stakeholders are aligning standards and communication protocols globally to ensure vehicles meet safety, performance, and compliance requirements across different markets. The move from legacy networks to high-speed Ethernet-based systems, along with zonal architectures, helps manage the increasing number of sensors, cameras, and controllers in modern vehicles. Fleet operators and automakers are leveraging telematics and real-time data to optimize maintenance, improve efficiency, and reduce operating costs, reinforcing the value of connected technologies.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$21.7 Billion

Forecast Value

$66.8 Billion

CAGR

12.4%

The hardware segment held a 65.5% share in 2025. Hardware remains critical to automotive communication, encompassing ECUs, transceivers, wiring harnesses, gateways, sensors, and connectors. As vehicles incorporate advanced electronic systems for ADAS, infotainment, and powertrain management, the need for robust communication hardware has intensified. These components cannot be replaced by software and are essential for reliable in-vehicle networking and data flow.

The passenger cars segment accounted for 78.2% share in 2025 and is expected to reach USD 49.5 billion by 2035. The segment leads because passenger vehicles are produced in large volumes and rapidly adopt new communication technologies. Features like V2X, telematics, and advanced in-vehicle networking are becoming standard or mid-range options, enhancing safety, infotainment, and driver assistance across mass-market vehicles.

U.S. Automotive Communication Technology Market reached USD 5.5 billion in 2025. A key trend in the U.S. is the increasing deployment of vehicle-to-everything (V2X) communication, allowing vehicles to exchange information with infrastructure, other vehicles, and networks. This technology is being promoted to enhance safety and traffic management, supported by smart city initiatives and pilot programs. Automakers and tech companies are advancing V2X while still maintaining traditional in-vehicle protocols such as CAN, LIN, and newer Ethernet-based systems.

Major companies in the Global Automotive Communication Technology Market include Mitsubishi Electric, Yazaki, Aptiv, Harman International, Lear, ZF Friedrichshafen, Magna, Valeo, Denso, and Autoliv. To strengthen presence, companies in the Automotive Communication Technology Market are focusing on innovation in high-speed connectivity, telematics, and in-vehicle networking solutions. They are investing heavily in R&D to improve system reliability, data handling, and integration with ADAS and infotainment systems. Strategic partnerships with automakers and semiconductor providers help accelerate adoption and expand global reach. Firms are standardizing protocols, offering modular platforms, and aligning with regulatory requirements to enhance cross-market compatibility. Additionally, companies are leveraging software updates, predictive maintenance, and real-time data analytics to increase client retention, optimize vehicle performance, and ensure long-term competitiveness in a rapidly evolving connected vehicle landscape.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Bus Module

2.2.4 Connectivity

2.2.5 Vehicle

2.2.6 Vehicle Class

2.2.7 Propulsion

2.2.8 Application

2.2.9 Sales Channel

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising vehicle electrification and software-defined vehicles

3.2.1.2 Growing integration of advanced driver assistance systems (ADAS)

3.2.1.3 Increasing demand for in-vehicle infotainment and connectivity

3.2.1.4 Shift toward autonomous and semi-autonomous vehicles

3.2.2 Industry pitfalls and challenges

3.2.2.1 Complexity of network integration and interoperability

3.2.2.2 Cybersecurity and data privacy concerns

3.2.3 Market opportunities

3.2.3.1 Growth of vehicle-to-everything (V2X) communication

3.2.3.2 Increasing adoption of 5G-enabled automotive networks

3.2.3.3 Expansion of electric and autonomous commercial vehicles

3.2.3.4 Integration of AI-driven in-vehicle data processing

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 Society of Automotive Engineers (SAE) J2735

3.4.1.2 Institute of Electrical and Electronics Engineers (IEEE)

3.4.1.3 Dedicated Short Range Communications (DSRC) Protocol

3.4.2 Europe

3.4.2.1 European Telecommunications Standards Institute (ETSI)

3.4.2.2 Cellular Vehicle-to-Everything (C-V2X) Communication Standard

3.4.3 Asia Pacific

3.4.3.1 Vehicle Network Communication Protocol (China)

3.4.3.2 Automotive Industry Standard 140 (AIS 140, India)

3.4.4 Latin America

3.4.4.1 International Telecommunication Union Recommendation