자동차용 패스너 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)

Automotive Fastener Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928957

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 245 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

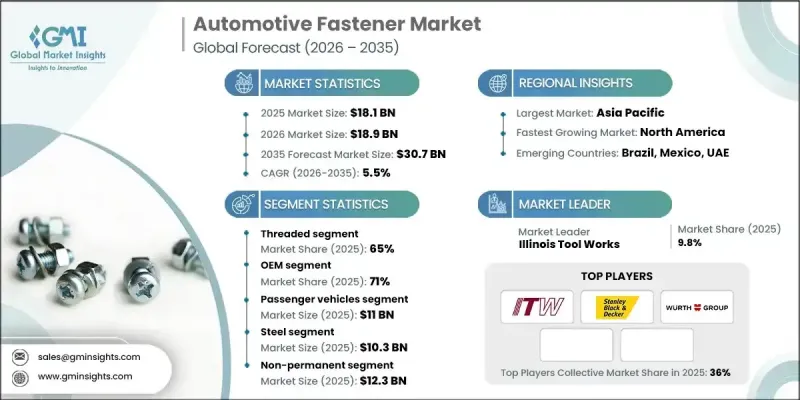

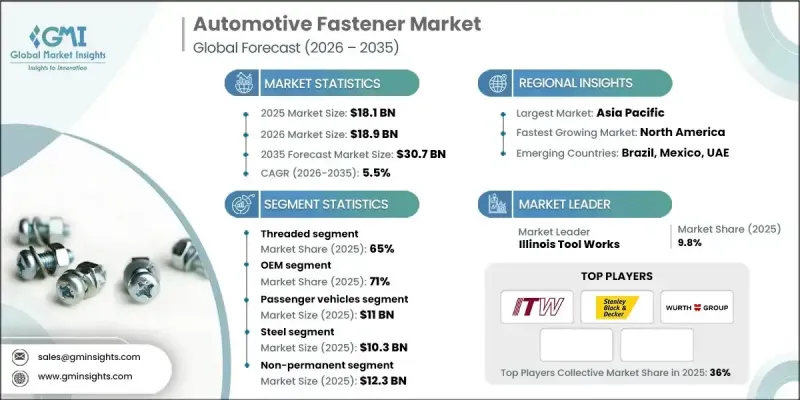

세계의 자동차용 패스너 시장은 2025년에 181억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR)5.5%로 성장하여 307억 달러에 이를 것으로 예측됩니다.

시장 성장은 전 세계 자동차 생산의 급속한 확대, 전기 및 하이브리드 자동차의 보급 확대, 안전성, 내구성 및 성능 향상에 대한 소비자 수요 증가에 힘입어 성장세를 보이고 있습니다. 제조업체, OEM 및 애프터마켓 공급업체들은 효율적인 차량 조립과 라이프사이클 비용 절감을 최우선 과제로 삼고 있으며, 이에 따라 기술적으로 진보된 패스너 솔루션의 중요성이 더욱 커지고 있습니다. 고강도 소재, 경량 부품, 스마트 체결 기술의 혁신은 시장을 재편하고 있으며, 자동차 제조업체가 하중 지지력을 최적화하고, 구조적 무결성을 유지하며, 조립 응력을 실시간으로 모니터링할 수 있게 해줍니다. 시장의 진화는 디지털 토크 모니터링, 예지보전, AI 기반 조립 최적화를 통해 승용차, 상용차, 전기차 부문 전반에 걸쳐 차량 성능 향상, 부품 수명 연장, 생산 공정 효율화에 기여하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

181억 달러

예측 금액

307억 달러

CAGR

5.5%

나사식 체결 부품은 2025년 65%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.9%의 성장률을 보일 것으로 예측됩니다. 이러한 장점은 차량 어셈블리 전체에 걸쳐 안전하고 재사용 가능한 고강도 연결이 요구되는 데서 비롯됩니다. 이러한 체결 부품에 대한 수요는 승용차, 소형 상용차, 전기자동차에 이르기까지 다양하며, 안전, 정확성, 비용 효율적인 유지보수를 보장합니다.

OEM 부문은 2025년 71%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.2%의 성장률을 보일 것으로 전망됩니다. OEM 제조업체는 구조적 신뢰성과 조립 효율성을 유지하면서 대량 생산을 지원하기 위해 자동 잠금 너트 및 EV 최적화 시스템을 포함한 첨단 체결 솔루션에 의존하고 있습니다.

중국 자동차 패스너 시장은 2025년 14억 6,000만 달러 규모에 달할 것으로 예측됩니다. 세계 자동차 제조 기지로서의 지위, 전기자동차 및 하이브리드 자동차 생산의 급속한 확대, 첨단 체결 기술의 채택이 강력한 시장 수요를 견인하고 있습니다. 중국 동부와 남부의 주요 자동차 클러스터에서 고성능 패스너의 도입이 가속화되고 있으며, 이 지역의 리더십을 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

비용 구조

각 공정 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

미국 연방 자동차 안전기준(FMVSS)

캐나다 자동차 안전기준(CMVSS)

유럽

독일 TUV 및 BaFin에의 준거

프랑스 DGITM 가이드라인

영국 차량 인증 기관(VCA) 규제

이탈리아 국토 교통성 규제 대응

아시아태평양

중국 공업 정보화부(MIIT) 가이드라인

국토 교통성 기준

한국 국토 교통성(MOLIT) 규제

인도 도로 운송 성(MoRTH) 및 인도 규격 협회(BIS) 가이드라인

라틴아메리카

브라질 DENATRAN 및 ANFAVEA 규제

멕시코 SCT(연방 통신성) 및 NOM(멕시코 국가 규격) 기준

중동 및 아프리카

아랍에미리트 도로 교통국(RTA) 가이드라인

사우디아라비아 운송 총국(GAT) 규제

Porter의 Five Forces 분석

PESTEL 분석

기술 및 혁신 전망

현재 기술 동향

신기술

가격 동향

지역별

제품별

생산 통계

생산 거점

소비 거점

수출과 수입

비용 내역 분석

특허 분석

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

환경 배려형 구상

탄소발자국에 관한 고려사항

이용 사례 시나리오

EV특유 체결 요건

배터리 팩 및 케이스 고정

열팽창과 진동에 관한 과제

고전압 절연·격리용 패스너

EV와 내연기관차 체결 부품 수요 변화

경량화와 재료 치환 동향

강철, 알루미늄, 복합재료, 플라스틱

트레이드 오프 : 강도 vs중량 vs 비용

자동차 제조업체 경량화 목표

차량 1대당 체결 부품 수량에 대한 영향

차량 시스템별 체결 기술

스마트 패스너와 인더스트리 4.0통합

OEM 조달 및 공급업체 선정 기준

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획과 자금조달

제5장 시장 추산·예측 : 용량별, 2022-2035

나사 잘라

너트

볼트

와셔

기타

비군요글자 잘라

제6장 시장 추산·예측 : 차량별, 2022-2035

승용차

해치백차

세단

SUV

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

제7장 시장 추산·예측 : 재료별, 2022-2035

강

플라스틱

기타

제8장 시장 추산·예측 : 특성별, 2022-2035

비항구

항구

제9장 시장 추산·예측 : 유통 채널별, 2022-2035

OEM

애프터마켓

제10장 시장 추산·예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

싱가포르

한국

베트남

인도네시아

말레이시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

아랍에미리트

남아프리카공화국

사우디아라비아

제11장 기업 개요

Global Player

ARaymond

Bossard

Bulten

Illinois Tool Works(ITW)

KAMAX

LISI Automotive

Nedschroef

Pentair Automotive Fasteners

Stanley Black &Decker

Wurth

Regional Player

Al Ameen Fasteners

Anchors Fasteners

Clavos y Tornillos

Fastenright

Gunther Fasteners

Jorfast

SAE Fasteners

Sundaram Fasteners

Topfast Fasteners

Yuyama Manufacturing

신규 기업

EcoFast Automotive

EVFast Fastening Solutions

GreenBolt Solutions

NextGen Fasteners

Titan Fasteners

LSH

영문 목차

영문목차

The Global Automotive Fastener Market was valued at USD 18.1 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 30.7 billion by 2035.

Market growth is fueled by the rapid expansion of global vehicle production, the increasing adoption of electric and hybrid vehicles, and growing consumer demand for enhanced safety, durability, and performance. Manufacturers, OEMs, and aftermarket providers are prioritizing efficient vehicle assembly and lifecycle cost reduction, which has increased the importance of technologically advanced fastener solutions. Innovations in high-strength materials, lightweight components, and smart fastening technologies are reshaping the market, enabling automakers to optimize load-bearing capacity, maintain structural integrity, and monitor assembly stress in real time. The evolution of the market is also supported by digital torque monitoring, predictive maintenance, and AI-driven assembly optimization, all of which contribute to improved vehicle performance, extended component life, and more efficient production processes across passenger, commercial, and electric vehicle segments.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$18.1 Billion

Forecast Value

$30.7 Billion

CAGR

5.5%

The threaded fasteners accounted for 65% share in 2025 and are expected to grow at a CAGR of 5.9% through 2035. Their dominance is driven by the need for secure, reusable, and high-strength connections across vehicle assemblies. Demand for these fasteners spans passenger vehicles, light and heavy commercial vehicles, and electric vehicles, ensuring safety, precision, and cost-efficient maintenance.

The OEM segment held 71% share in 2025 and is forecasted to grow at a CAGR of 5.2% through 2035. OEMs rely on advanced fastening solutions, including self-locking nuts and EV-optimized systems, to support high production volumes while maintaining structural reliability and assembly efficiency.

China Automotive Fastener Market generated USD 1.46 billion in 2025. Its status as a global automotive manufacturing hub, rapid expansion in electric and hybrid vehicle production, and adoption of advanced fastening technologies contribute to strong market demand. Major automotive clusters across eastern and southern China are increasingly implementing high-performance fasteners, reinforcing the nation's leadership within the region.

Key players in the Global Automotive Fastener Market include Bossard, Wurth, Illinois Tool Works (ITW), ARaymond, Nedschroef, Bulten, Pentair Automotive Fasteners, Stanley Black & Decker, KAMAX, and LISI Automotive. Companies in the Global Automotive Fastener Market are employing multiple strategies to strengthen their position and expand their footprint. They are investing heavily in research and development to create lightweight, corrosion-resistant, and smart fastening solutions. Strategic partnerships with OEMs and aftermarket providers help secure long-term contracts and broaden market access. Firms are also focusing on regional expansion to tap into emerging automotive hubs, particularly in Asia-Pacific. Adoption of digital and AI-based assembly monitoring tools enhances product differentiation.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Capacity

2.2.3 Vehicle

2.2.4 Material

2.2.5 Characteristics

2.2.6 Distribution Channel

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising global vehicle production

3.2.1.2 Adoption of electric and hybrid vehicles (EVs/HEVs)

3.2.1.3 Focus on vehicle safety and durability

3.2.1.4 Technological advancements

3.2.2 Industry pitfalls and challenges

3.2.2.1 Volatility in raw material prices

3.2.2.2 High competition from regional and low-cost manufacturers

3.2.3 Market opportunities

3.2.3.1 Growth in electric vehicles and lightweight vehicle segment

3.2.3.2 Integration of smart and connected fastening solutions

3.2.3.3 Digitalization and smart assembly

3.2.3.4 Lightweight and modular vehicle platforms

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S. Federal Motor Vehicle Safety Standards (FMVSS)

3.4.1.2 Canada Motor Vehicle Safety Standards (CMVSS)

3.4.2 Europe

3.4.2.1 Germany TUV & BaFin Compliance

3.4.2.2 France DGITM Guidelines

3.4.2.3 UK Vehicle Certification Agency (VCA) Regulations

3.4.2.4 Italy Ministry of Infrastructure & Transport Compliance

3.4.3 Asia Pacific

3.4.3.1 China MIIT Guidelines

3.4.3.2 Japan MLIT Standards

3.4.3.3 South Korea MOLIT Regulations

3.4.3.4 India Ministry of MoRTH & BIS Guidelines

3.4.4 Latin America

3.4.4.1 Brazil DENATRAN & ANFAVEA Regulations

3.4.4.2 Mexico SCT & NOM Standards

3.4.5 Middle East and Africa

3.4.5.1 UAE Roads & Transport Authority (RTA) Guidelines

3.4.5.2 Saudi Arabia General Authority for Transport (GAT) Regulations