Nuclear Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928889

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

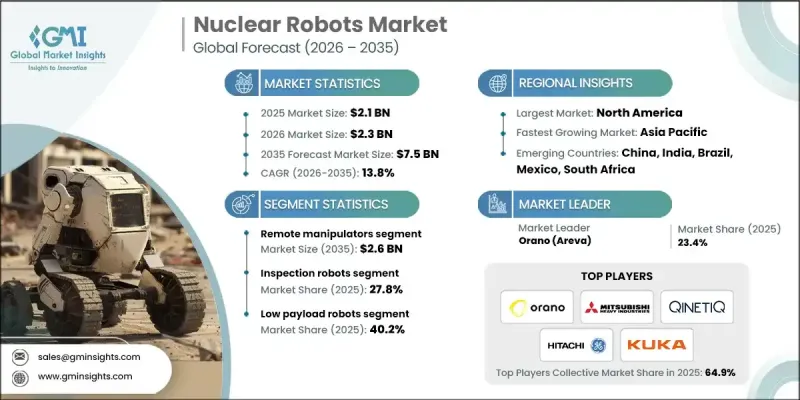

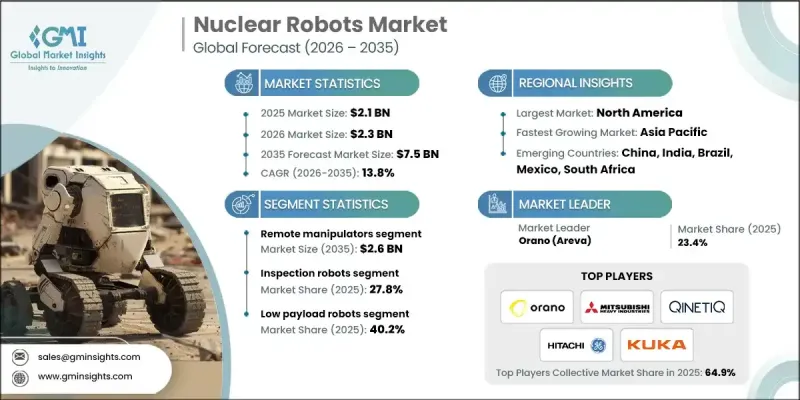

세계의 원자력 로봇 시장은 2025년에 21억 달러로 평가되었으며, 2035년까지 CAGR 13.8%로 성장하여 75억 달러에 달할 것으로 예측됩니다.

시장 성장의 배경에는 전 세계적으로 노후화된 원자력 시설의 증가, 특히 유럽과 북미에서 원자로 및 연료주기 시설이 설계 수명을 초과한 상황이 있습니다. 이들 시설의 폐로 작업은 고방사선, 고위험 환경에서의 작업이 수반되기 때문에 작업자의 안전 확보와 규제 준수 측면에서 원격 조작, 점검, 폐기물 관리가 매우 중요합니다. 정부 자금과 공공 부문의 원자력 안전 및 현대화 프로그램에 대한 투자는 첨단 로봇 기술에 대한 수요를 더욱 촉진하고 있습니다. 원자력 로봇은 검사, 유지보수, 해체, 방사성 폐기물 관리를 위해 특별히 설계되어 정확성과 운영 효율을 향상시키고 인명피폭을 최소화할 수 있습니다. 인공지능과 자율기술의 통합을 통해 이 기계들은 까다로운 방사능 환경에서도 자율적으로 작동할 수 있어 전문 인력의 필요성을 줄이면서 성능과 안전성을 향상시킬 수 있습니다. 폐기 및 현장 복구 프로그램은 이러한 첨단 솔루션에 대한 안정적인 수요를 지속적으로 견인하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035

개시시 가치

21억 달러

예측 금액

75억 달러

CAGR

13.8%

원격 조작 조작기 분야는 2035년까지 26억 달러에 달할 것으로 예상됩니다. 원격 조작 조작기는 방사선량이 많은 지역에서 원자력 부품의 조립, 유지보수 및 취급을 안전하게 수행할 수 있는 능력으로 인해 널리 채택되고 있습니다. 촉각 피드백 및 직관적인 제어 인터페이스의 혁신으로 피폭 위험을 낮추면서 작업자의 정확성을 향상시켰습니다.

검사 로봇 부문은 2025년 27.8%의 점유율을 차지했습니다. 이 로봇들은 AI 기반 내비게이션과 센서 기반 이상 감지 기능을 탑재해 원자로, 파이프라인, 저장시설의 자율 점검을 실현하고 있습니다. 지속적인 모니터링을 보장하면서 인력 작업, 가동 중단 시간, 방사선 피폭을 줄입니다.

북미 원자력 로봇 시장은 2025년 38.9%의 점유율을 차지했습니다. 이 지역의 성장은 광범위한 원자력 인프라, 대규모 폐로 활동, 안전과 자동화를 강조하는 강력한 규제 정책에 의해 주도되고 있습니다. AI 기반 점검, 유지보수, 폐기물 관리 로봇의 도입 확대와 정부 지원 R&D 이니셔티브가 맞물려 시장 확대를 촉진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계의 부가가치

밸류체인에 영향을 미치는 요인

디스럽션

업계에 대한 영향요인

성장 촉진요인

사고 예방과 긴급 대응 준비에 대한 주력 강화

노후화한 원자력 시설 해체 증가

원자력 사업의 노동력 부족과 스킬 격차

원자력 안전 인프라에의 정부 자금 및 공공 부문 투자

업계의 잠재적 리스크와 과제

높은 자본 비용과 수명주기 비용

원자력 시설간의 표준화와 상호운용성의 부족

시장 기회

해체 프로젝트용 RaaS(robotics-as-a-service) 모델 확대

복수 사이트에서의 적용성을 고려한 모듈형·재구성 가능 로봇 개발

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porters 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

신흥 비즈니스 모델

컴플라이언스 요건

특허 및 지적재산 분석

지정학적·무역 동향

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 기업의 경쟁 벤치마킹

재무 실적 비교

매출

이익률

연구개발

제품 포트폴리오 비교

제품 라인 폭

기술

혁신

지역별 전개 비교

세계 전개 분석

서비스 네트워크 커버율

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더 기업

과제자

팔로어

틈새 플레이어

전략적 전망 매트릭스

주요 발전, 2021-2024

인수합병

제휴 및 합작투자

기술적 진보

확대와 투자전략

디지털 전환의 대처

신흥/스타트업 경쟁 동향

제5장 시장 추정 및 예측 : 유형별, 2022-2035

원격조작 매니퓰레이터

크롤러

공중 드론

수중 로봇(ROV)

휴머노이드 로봇

제6장 시장 추정 및 예측 : 로봇 종류별, 2022-2035

검사 로봇

제염 로봇

보수·수리 로봇

폐기물 처리 로봇

긴급 대응 로봇

제7장 시장 추정 및 예측 : 적재 능력별, 2022-2035

저적재량 로봇

중적재량 로봇

고적재량 로봇

제8장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035

핵폐기물 처리

원자력 시설 해체

방사선 제염

원자력발전소

조사·탐사

기타

제9장 시장 추정 및 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제10장 기업 개요

세계의 주요 기업

Orano

Mitsubishi Heavy Industries

Hitachi-GE Nuclear Energy

Westinghouse Electric Company

지역별 주요 기업

북미

Amentum Services

Mirion Technologies

GE Inspection Robotics

유럽

QinetiQ Group

Framatome

Babcock International Group

아시아태평양

KUKA AG

ABB

Cybernetix(TechnipFMC)

틈새 플레이어/디스럽터

Boston Dynamics

James Fisher & Sons

Veolia Environnement

Nuvia Group

Oceaneering International

Honeybee Robotics

Inuktun Services

KSM

영문 목차

영문목차

The Global Nuclear Robots Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 13.8% to reach USD 7.5 billion by 2035.

Market growth is driven by the rising number of aging nuclear facilities worldwide, particularly in Europe and North America, where reactors and fuel cycle plants are exceeding their operational lifespans. Decommissioning these facilities involves working in highly radioactive and hazardous environments, which makes remote handling, inspection, and waste management critical for worker safety and regulatory compliance. Government funding and public sector investment in nuclear safety and modernization programs are further propelling demand for advanced robotics. Nuclear robots are specifically engineered for inspection, maintenance, deconstruction, and radioactive waste management, offering enhanced accuracy, operational efficiency, and minimized human exposure. The integration of artificial intelligence and autonomous technologies allows these machines to operate independently in challenging radioactive environments, reducing the need for expert personnel while increasing performance and safety. Decommissioning and site remediation programs continue to drive steady demand for these advanced solutions.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$2.1 Billion

Forecast Value

$7.5 Billion

CAGR

13.8%

The remote manipulators segment is projected to reach USD 2.6 billion by 2035. Remote manipulators are widely adopted in radiation-heavy zones due to their capability to assemble, maintain, and handle nuclear components safely. Innovations in haptic feedback and intuitive control interfaces have improved operator precision while keeping exposure risks low.

The inspection robots segment accounted for 27.8% share in 2025. These robots are evolving with AI-powered navigation and sensor-based anomaly detection, enabling autonomous inspection of reactors, pipelines, and storage facilities. They reduce manual labor, operational downtime, and radiation exposure for personnel while ensuring continuous monitoring.

North America Nuclear Robots Market held a 38.9% share in 2025. Growth in the region is driven by extensive nuclear infrastructure, large-scale decommissioning activities, and strong regulatory policies emphasizing safety and automation. Increasing adoption of AI-driven inspection, maintenance, and waste management robots, combined with government-funded R&D initiatives, is bolstering market expansion.

Leading players in the Global Nuclear Robots Market include Hitachi-GE Nuclear Energy, Ltd., KUKA AG, ABB Ltd., Honeybee Robotics, Ltd., Boston Dynamics, Inc., Inuktun Services Ltd., Babcock International Group plc, QinetiQ Group plc, Orano, Framatome, Westinghouse Electric Company LLC, Nuvia Group, Amentum Services, Inc., GE Inspection Robotics, Mitsubishi Heavy Industries, Ltd., Veolia Environnement S.A., Oceaneering International, Inc., Cybernetix (TechnipFMC), James Fisher & Sons plc, and Mirion Technologies, Inc. Companies in the Global Nuclear Robots Market are strengthening their positions through continuous R&D investments to develop autonomous, AI-enabled systems capable of operating in extreme radiation environments. They are forming strategic partnerships with nuclear operators and government agencies to expand adoption. Geographic expansion into regions with aging nuclear infrastructure and decommissioning requirements is another key strategy.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Type trends

2.2.2 Robot type trends

2.2.3 Payload capacity trends

2.2.4 End-use industry trends

2.2.5 Regional trends

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increased focus on accident prevention and emergency response preparedness

3.2.1.2 Increasing decommissioning of aging nuclear facilities

3.2.1.3 Labor shortages and skill gaps in nuclear operations

3.2.1.4 Government funding and public sector investment in nuclear safety infrastructure

3.2.2 Industry pitfalls and challenges

3.2.2.1 High capital and lifecycle costs

3.2.2.2 Limited standardization and interoperability across nuclear sites

3.2.3 Market opportunities

3.2.3.1 Expansion of robotics-as-a-service models for decommissioning projects

3.2.3.2 Development of modular, reconfigurable robots for multi-site applicability

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter';s analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Emerging business models

3.9 Compliance requirements

3.10 Patent and IP analysis

3.11 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn & Units)

5.1 Key trends

5.2 Remote manipulators

5.3 Crawlers

5.4 Aerial drones

5.5 Underwater robots (ROVs)

5.6 Humanoid robots

Chapter 6 Market Estimates and Forecast, By Robot Type, 2022 - 2035 ($ Mn & Units)

6.1 Key trends

6.2 Inspection robots

6.3 Decontamination robots

6.4 Maintenance & repair robots

6.5 Waste handling robots

6.6 Emergency response robots

Chapter 7 Market Estimates and Forecast, By Payload Capacity, 2022 - 2035 ($ Mn & Units)

7.1 Key trends

7.2 Low payload robots

7.3 Medium payload robots

7.4 High payload robots

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 ($ Mn & Units)

8.1 Key trends

8.2 Nuclear waste handling

8.3 Nuclear decommissioning

8.4 Radiation cleanup

8.5 Nuclear power plants

8.6 Research & exploration

8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Units)