Wood Pellets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913415

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

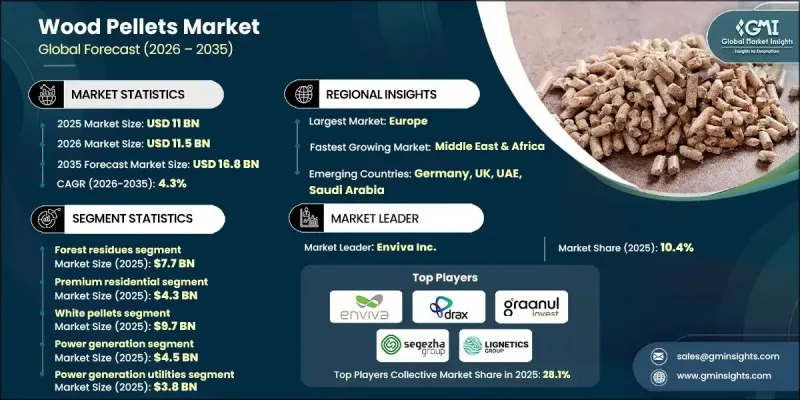

세계의 목재 펠릿 시장은 2025년 110억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 4.3%로 성장하여 168억 달러에 이를 것으로 예측됩니다.

시장의 발전은 발전 및 대규모 난방 용도에서 바이오매스 기반 에너지 솔루션의 채택 확대와 밀접한 관련이 있습니다. 유틸리티 및 산업 운영자는 배출량 감소 및 환경 규제 준수 목표 달성을 위해 기존 화석 연료의 대안으로 목재 펠릿으로의 전환을 가속화하고 있습니다. 고에너지 소비산업에서도 안정된 성능과 저배출 특성을 갖춘 표준화 연료의 필요성으로 펠릿 기반 시스템이 도입되고 있습니다. 신재생에너지 이용을 촉진하는 정책 틀과 규제 요건은 여전히 강력한 성장 요인으로 작용하고 있습니다. 정부의 인센티브, 신재생에너지 의무, 지속가능성 목표가 바이오매스의 보급 확대를 지원하고 목질 펠릿의 비용 경쟁력을 향상시키는 동시에 세계 에너지 전환에서의 역할을 강화하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 규모

110억 달러

예측 금액

168억 달러

CAGR

4.3%

산림 잔류물 기반 펠렛 부문은 2025년 77억 달러를 차지했으며, 원료 구성의 대부분을 차지했습니다. 이 부문은 안정적인 공급과 대규모 펠렛 제조에 대한 적합성을 강조합니다. 재료 특성과 에너지 출력의 일관성은 효율적인 가공과 비용 효율적인 생산을 지원합니다. 첨단 지역에 설립된 임업 공급망은 산업 및 유틸리티 조달 기준을 충족하는 추적성과 지속가능성을 보장하는 조달을 보장함으로써 이 부문을 더욱 강화하고 있습니다.

고급 주택용 펠렛 부문은 2025년 43억 달러 규모였습니다. 이 등급은 가정용 난방 요구 사항과 품질 규제에 엄격하게 적합하며 효율적인 연소, 최소 잔사 및 안정적인 시스템 성능을 제공합니다. 선진국 경제권의 에너지 절약형 주택 난방 솔루션에 대한 지속적인 투자와 청정 에너지 정책의 지원이 수요를 지속하고 있습니다.

북미의 목재 펠릿 시장은 2025년에 16.4%의 점유율을 차지했습니다. 이 지역은 강력한 생산 능력과 대규모 수출 활동(주로 미국이 보조)의 혜택을 받고 있습니다. 풍부한 산림 자원, 확립된 펠렛 제조 인프라, 첨단 물류 능력으로 이 지역은 국제 시장에 효율적으로 공급할 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 요인

식품 및 음료 업계에서 수요 증가

친환경 소재를 촉진하는 정부 규제

소매업 및 소비재(FMCG) 분야에서 채용 확대

업계의 잠재적 위험 및 과제

원재료 가격의 변동성

산림 벌채와 관련된 환경 문제

시장 기회

재생에너지 및 탄소 중립 솔루션에 대한 수요 증가

산업 용도의 확대와 석탄과의 혼합 연소

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

원료

미래 시장 동향

기술과 혁신 동향

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산에서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추계 및 예측 : 원료별, 2022-2035년

산림 잔여물

침엽수

활엽수

통나무 및 펄프재

농업 잔류물

재생 목재

제6장 시장 추계 및 예측 : 등급별, 2022-2035년

프리미엄(A1)

스탠다드(A2)

공업용 등급(B)

기타

제7장 시장 추계 및 예측 : 펠릿 유형별, 2022-2035년

백색 펠릿

흑색 펠릿

제8장 시장 추계 및 예측 : 용도별, 2022-2035년

난방

발전

열병합 발전(CHP)

기타

제9장 시장 추계 및 예측 : 최종 용도별, 2022-2035년

주택 및 가정용

상업시설

발전사업자

산업 제조

지역 열 공급 사업자

농업 및 축산업

외식산업 및 숙박시설

제10장 시장 추계 및 예측 : 지역별, 2022-2035년

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제11장 기업 프로파일

Enviva Inc

Drax Group PLC

Graanul Invest

Lignetics Group

Segezha Group

Fram Fuels

Viridis Energy Inc.

Rentech Inc.

Wood &Energy

Buhler

Energex

Highland Pellets LLC

Pfeifer Group

JHS

영문 목차

영문목차

The Global Wood Pellets Market was valued at USD 11 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 16.8 billion by 2035.

Market development is closely tied to the rising adoption of biomass-based energy solutions across power generation and large-scale heating applications. Utilities and industrial operators are increasingly turning to wood pellets as a substitute for conventional fossil fuels to reduce emissions and meet environmental compliance targets. High energy-consuming industries are also incorporating pellet-based systems due to their need for standardized fuel with consistent performance and lower emission output. Policy frameworks and regulatory mandates promoting renewable energy usage continue to act as strong growth enablers. Government incentives, renewable energy obligations, and sustainability targets are supporting wider biomass adoption, improving the cost competitiveness of wood pellets and reinforcing their role within the global energy transition.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$11 Billion

Forecast Value

$16.8 Billion

CAGR

4.3%

The forest residue-based pellets segment accounted for USD 7.7 billion in 2025, representing a major share of the feedstock mix. This segment benefits from reliable availability and suitability for large-scale pellet manufacturing. The consistency in material characteristics and energy output supports efficient processing and cost-effective production. Established forestry supply chains across developed regions further strengthen this segment by ensuring traceable and sustainable sourcing that meets industrial and utility procurement standards.

The premium residential pellets segment held USD 4.3 billion in 2025. This grade aligns closely with household heating requirements and quality regulations, offering efficient combustion, minimal residue, and stable system performance. Ongoing investment in energy-efficient residential heating solutions and supportive clean energy policies across developed economies continue to sustain demand.

North America Wood Pellets Market accounted for 16.4% share in 2025. The region benefits from strong production capacity and significant export activity, largely supported by the United States. Abundant forest resources, established pellet manufacturing infrastructure, and advanced logistics capabilities enable the region to serve international markets efficiently.

Key companies operating in the Global Wood Pellets Market include Drax Group PLC, Enviva Inc., Lignetics Group, Graanul Invest, Segezha Group, Highland Pellets LLC, Fram Fuels, Rentech Inc., Viridis Energy Inc., Energex, Buhler, Wood & Energy, and Pfeifer Group. Companies active in the Global Wood Pellets Market are reinforcing their market position through capacity expansion, supply chain integration, and long-term offtake agreements. Leading producers are investing in efficient processing technologies to improve yield consistency and reduce operational costs. Strategic partnerships with utilities and industrial buyers are helping secure stable demand and revenue visibility. Firms are also expanding export infrastructure and logistics capabilities to strengthen access to international markets.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Feedstock

2.2.3 Pellet type

2.2.4 Grade

2.2.5 Application

2.2.6 End Use

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing demand from food and beverage industry

3.2.1.2 Government regulations promoting eco-friendly materials

3.2.1.3 Increasing adoption in the retail and FMCG sectors

3.2.2 Industry pitfalls and challenges

3.2.2.1 Volatility in raw material prices

3.2.2.2 Environmental concerns related to deforestation

3.2.3 Market opportunities

3.2.3.1 Rising demand for renewable energy and carbon-neutral solutions

3.2.3.2 Expansion in industrial applications and co-firing with coal

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 Feedstock

3.8 Future market trends

3.9 Technology and Innovation Landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Feedstock, 2022 - 2035 (USD billion) (Kilo Tons)

5.1 Key trends

5.2 Forest residues

5.2.1 Softwood

5.2.2 Hardwood

5.2.3 Roundwood & pulpwood

5.3 Agricultural residues

5.4 Recycled wood

Chapter 6 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD billion) (Kilo Tons)

6.1 Key trends

6.2 Premium (A1)

6.3 Standard (A2)

6.4 Industrial grade (B)

6.5 Others

Chapter 7 Market Estimates and Forecast, By Pellet Types, 2022 - 2035 (USD billion) (Kilo Tons)

7.1 Key trends

7.2 White pellets

7.3 Black pellets

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD billion) (Kilo Tons)

8.1 Key trends

8.2 Heating

8.3 Power generation

8.4 Combined Heat & Power (CHP)

8.5 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD billion) (Kilo Tons)

9.1 Key trends

9.2 Residential / Household

9.3 Commercial establishments

9.4 Power generation utilities

9.5 Industrial manufacturing

9.6 District heating operators

9.7 Agriculture & Livestock

9.8 Food Service & Hospitality

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD billion) (Kilo Tons)