ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

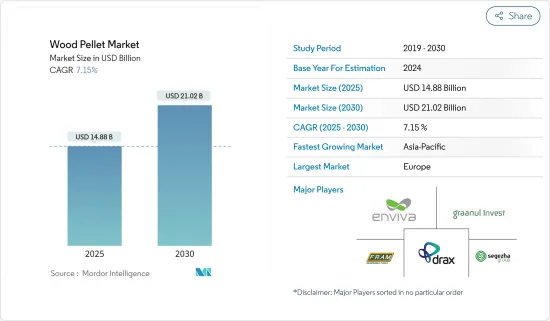

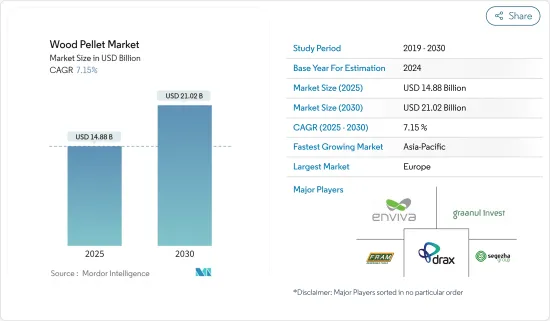

목재 펠릿 시장 규모는 2025년에 148억 8,000만 달러에 이를 것으로 추정됩니다. 예측 기간 중(2025-2030년) CAGR은 7.15%를 나타내고, 2030년에는 210억 2,000만 달러에 달할 것으로 전망됩니다.

중기 시장 성장 촉진요인은 특히 유럽의 청정 에너지 발전에서 목재 펠릿 수요 증가를 포함합니다.

한편, 세계 각지에서 태양광발전, 풍력발전, 지열발전 등 대체재생가능에너지의 채용과 도입 증가는 예측기간 중 시장 성장을 방해할 가능성이 높습니다.

하지만 세계 바이오에너지 협회에 따르면, 목재 펠릿은 발전 시설에서 석탄을 대체할 가능성을 가지고 있습니다. 최근의 기술 개발로 목재 펠릿은 열분해, 수열 탄화, 수증기 폭발 등 다양한 공정을 통해 열이 개선되었습니다. 열 개선으로 목재 펠릿은 석탄의 성질을 가진 연료로 작동합니다. 석탄 발전소의 수가 세계에서 가장 많은 아시아태평양은 향후 시장이 성장할 기회가 될 것으로 예상됩니다.

2022년 동안 목재 펠릿 생산량이 크게 증가한 유럽은 예측 기간 동안 시장에서 큰 점유율을 차지할 것으로 예상됩니다.

목재 펠릿 시장 동향

난방용도가 시장을 독점할 전망

펠릿은 고체 바이오 매스 연료이며 주로 목재 잔류 물과 밀짚과 같은 농업 제품별로 생산됩니다. 익지않는 바이오매스와 비교할 때 펠릿 특유의 이점은 표준화된 특성, 높은 에너지 함량 및 높은 밀도를 포함합니다.

난방 용도의 목재 펠릿은 주로 주택 및 상업 부문에서 식품, 요리, 그릴 및 가정에 열을 공급하는 데 사용됩니다. 샷 비용이 다른 연료보다 싼 상태가 오랫동안 지속되었기 때문에 보다 경제적인 선택이 되어 주택 및 상업 부문의 주요 우려에 대처하고 있습니다.

목재 펠릿은 태우면 고밀도화된 바이오매스 연료로 전력과 열을 생성할 수 있습니다. 목재 펠릿의 생산, 소비 및 상업은 2000년대 후반에 여러 국가에서 현저하게 증가했습니다. 보통 목질 펠릿은 석탄과 섞이거나 석탄으로 대체되는 산업용 발전소가 소비 확대의 원인입니다.

독일·에너지 목재·펠릿 협회에 의하면, 2022년의 독일 국내의 펠릿 난방 시스템은 64만 8,000대로, 2021년의 57만대에 비해 증가했습니다.

게다가 신재생에너지원으로서 목질펠릿은 많은 나라에서 정부로부터 보조금과 장려금을 받고 있으며, 최근 많은 나라가 난방용도의 목질펠릿과 관련된 정책과 제도를 시작하거나 갱신하고 있습니다.

영국 정부는 2022년 11월 23일에 시행된 펠릿 전용 연료 품질 정지 조치를 최장 1년간 실시했습니다. 즉, 정지 조치가 유효한 동안에는 바이오매스 보일러나 소유자가 OFGEM으로부터 재생 가능 열 장려금을 지불받는 공장에서 사용되는 목재 펠릿의 연료 품질 기준은 요구되지 않습니다. 정부는 2022년 2월에 규제를 개정했고, 바이오매스 공급업체 목록(BSL) 번호를 가진 목질 연료는 관련 품질 기준도 충족할 것을 의무화했습니다.

따라서 위의 점에서 예측 기간 동안 난방 용도가 목재 펠릿을 지배할 것으로 예상됩니다.

시장을 독점하는 유럽

유럽의 목재 펠릿 수요는 2022년부터 2028년까지 30-40% 증가할 것으로 예상됩니다. 유럽은 세계 펠릿 수요의 50% 이상을 차지합니다. 게다가 펠릿은 학교나 사무실 등의 지방자치단체나 행정기관 건물의 석탄전환 프로젝트에도 진출하고 있습니다.

미국 농무부 대외농업서비스 보고서에 따르면 2022년 EU 펠릿 소비량은 전년 대비 1.2% 증가한 2,480만 톤에 달했습니다. 유럽의 펠릿 소비량의 약 66%는 가정·상업 부문이, 34%는 산업 부문이 소비하고 있습니다. 상황은 국가마다 다릅니다. 네덜란드와 덴마크의 주요 원동력은 산업용(전력 및 CHP용)입니다. 이탈리아, 독일, 프랑스에서는 주택 난방이 목재 펠릿 사용의 대부분을 차지합니다.

이 지역의 대부분의 국가는 혼소 발전소의 폐쇄 및 전환을 계획하고 있으며, 일부 국가는 연료를 100% 목재 펠릿으로 전환하고 있습니다. 예를 들어 발메트는 2023년 5월 핀란드의 헬싱키에 있는 Salmisaari'A' 발전소에서 Helen사의 석탄 모래 지역 열 보일러와 기포 유동층(BFB) 연소를 목재 펠릿 모닥으로 전환한다고 발표했습니다. 이 전환은 탈석탄이라는 회사의 목표를 추진하는 동시에 지속 가능한 에너지 시스템의 구축을 강화하는 것입니다.

한편, EU는 2022년 7월 우크라이나 전쟁을 받고 발전에 사용되는 러시아 목재 바이오매스의 수입을 금지했습니다. 보도에 따르면 EU는 미국과 동유럽에서 러시아산 목재 바이오 매스 공급을 대체하는 목재 펠릿을 수입하고 있습니다. 엠비바는 전쟁이 시작된 이래 EU로의 출하량을 늘리고 2027년까지 연간 80만 톤의 펠릿을 공급한다는 무명의 유럽 고객과의 10년 계약을 발표했습니다.

또한, 이 지역 시장에서 기술의 진보는 조사 기간 동안 목재 펠릿 수요를 증가시킬 가능성이 높습니다.

따라서 위의 점에서 예측 기간 동안 유럽이 시장을 독점할 것으로 예상됩니다.

목재 펠릿 산업 개요

목재 펠릿 시장은 적당히 통합되어 있습니다. 시장의 주요 기업으로는 Enviva Partners LP, AS Graanul Invest, Drax Group Plc, Fram Renewable Fuels LLC, Segezha Group JSC 등을 들 수 있습니다(특별한 순서 없음).

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

시장 규모 및 수요 예측(단위 : 달러, -2029년)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

청정 에너지 생성에 있어서 목재 펠릿 수요 증가

목질 펠릿 제조 인프라의 성장

성장 억제요인

대체 재생 가능 에너지의 채용과 도입 증가

공급망 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

용도

난방

전력 생산

지역

북미

미국

캐나다

기타 북미

유럽

프랑스

이탈리아

독일

영국

스페인

북유럽 국가

터키

러시아

기타 유럽

아시아태평양

중국

인도

인도네시아

일본

한국

말레이시아

태국

베트남

기타 아시아태평양

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

나이지리아

카타르

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Enviva Partners LP

AS Graanul Invest

Drax Group PLC

Fram Renewable Fuels LLC

Segezha Group JSC

Lignetics Inc.

Biopower Sustainable Energy Corp.

Asia Biomass Public Company Limited

PT South Pacific

Market Ranking/Share Analysis

제7장 시장 기회와 앞으로의 동향

기술 개발에 의한 목재 펠릿의 열적 업그레이드

KTH

영문 목차

영문목차

The Wood Pellet Market size is estimated at USD 14.88 billion in 2025, and is expected to reach USD 21.02 billion by 2030, at a CAGR of 7.15% during the forecast period (2025-2030).

Over the medium period, the primary drivers for the market include increasing demand for wood pellets in clean energy generation, especially in the European region.

On the other hand, the adoption and increasing deployment of alternative renewable energy sources such as solar photovoltaic, wind energy, and geothermal in various parts of the world is likely to hinder market growth during the forecast period.

Nevertheless, as per the World Bioenergy Association, wood pellets have the potential to replace coal in power generation facilities. With technology development in recent years, wood pellets have undergone thermal upgrading through various processes like torrefaction, hydrothermal carbonization, and steam explosion. The thermal upgrading enables wood pellets to act as a fuel with coal properties. The Asia-Pacific region, with the world's highest number of coal power plants, is expected to be an opportunity for the market to grow in the future.

With a significant production of wood pellets during 2022, Europe was expected to have a significant share of the market during the forecast period.

Wood Pellet Market Trends

Heating Application Expected to Dominate the Market

Pellets are a solid biomass fuel, primarily produced from wood residues and agricultural by-products like straw. Specific advantages of pellets as compared to unprocessed biomass include standardized properties, high energy content, and high density.

Wood pellets for heating applications are primarily used in residential and commercial sectors for food, cooking and grilling, and supplying heat to homes. Since the cost of shots remained cheaper than other fuels for a long time, it has become a more economical option, addressing the primary concern of the residential and commercial sectors.

When burned, utility wood pellets (wood pellets) are a densified biomass fuel that can create power or heat. Wood pellet production, consumption, and commerce significantly increased in a few nations during the late 2000s. Industrial power plants, where wood pellets are usually co-fired with or replaced by coal, are the source of consumption growth.

According to the German Energy Wood and Pellet Association, in 2022, there were 648 thousand pellet heating systems in Germany, an increase compared to 570 thousand in 2021.

Moreover, as a renewable energy source, wood pellets have received subsidies and incentives from governments in many countries, and many countries either launched or updated their policies and schemes related to wood pellets for heating applications in recent years.

The UK government has implemented a suspension of fuel quality for pellets exclusively, which went into effect on November 23, 2022, for up to one year. This means that while the rest is in effect, the fuel quality criteria for wood pellets used in biomass boilers and plants where the owner receives Renewable Heat Incentive payments from OFGEM are not required. The government revised regulations in February 2022 to require that any wood fuel having a Biomass Suppliers List (BSL) number also meet the relevant quality criteria.

Therefore, owing to the above points, the heating application is expected to dominate the wood pellet during the forecast period.

Europe to Dominate the Market

Europe's demand for wood pellets is expected to increase by 30-40% between 2022 and 2028. Europe represents more than 50% of global pellet demand. Moreover, pellets have also made their way into coal conversion projects in local authority or public administration buildings such as schools and offices.

According to the USDA Foreign Agricultural Service Report, in 2022, the EU's pellet consumption reached 24.8 million tonnes, up 1.2% from the previous year. The household and commercial sectors consumed around 66% of European pellets, while the industry consumed 34%. The situation varies from one country to the next. The main driver for the Netherlands and Denmark is industrial use (for electricity and CHP). Residential heating accounts for most wood pellet use in Italy, Germany, and France.

Most countries in the region plan to close or convert co-firing power stations, with several moving to 100% wood pellets for fuel. For instance, in May 2023, Valmet announced the convert Helen Ltd's coal-fired district heat boiler and bubbling fluidized bed (BFB) combustion to enable wood pellet firing at the Salmisaari 'A' power plant in Helsinki, Finland. The conversion promotes the company's goal of phasing out coal and simultaneously strengthens the construction of a sustainable energy system.

On the other hand, in July 2022, the European Union banned importing Russian woody biomass used to generate energy in response to the war in Ukraine. According to reports, the EU has imported wood pellets from the United States and Eastern Europe to replace the Russian woody biomass supply. Enviva has increased EU shipments since the war began and announced a 10-year contract with an unnamed European customer to provide 800,000 metric tons of pellets yearly by 2027.

Further, technological advancements in the market in the region are also likely to increase the demand for wood pellets during the studied period.

Hence, owing to the above points, Europe is expected to dominate the market during the forecast period.

Wood Pellet Industry Overview

The wood pellet market is moderately consolidated. Some of the key players in the market include (in no particular order) Enviva Partners LP, AS Graanul Invest, Drax Group Plc, Fram Renewable Fuels LLC, and Segezha Group JSC, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecasts in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Demand for Wood Pellets in Clean Energy Generation