Road Safety Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913301

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 240 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

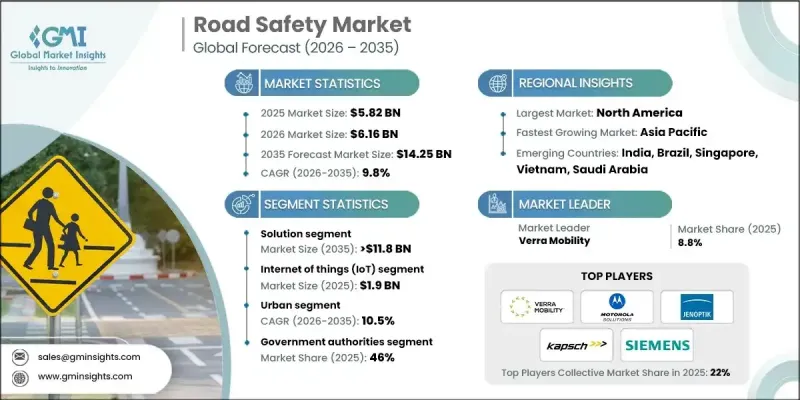

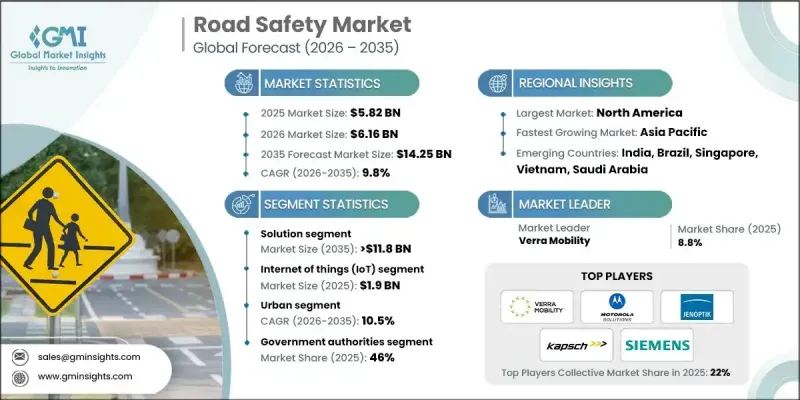

세계 교통안전 시장은 2025년 58억 2,000만 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 9.8%로 성장하여 142억 5,000만 달러에 이를 것으로 예측됩니다.

시장 성장은 세계 각국의 정부가 도입한 보다 강력한 규제 프레임워크에 의해 지원되고 있으며, 도로 네트워크 전체의 엄격한 컴플라이언스 기준, 집행력 강화, 장기적인 안전 목표에 중점화가 진행되고 있습니다. 공공기관은 광범위한 교통현대화 프로그램의 일환으로 첨단 교통안전시스템에 대한 지속적인 투자를 선호합니다. 급속한 도시 확대, 자동차 소유 대수 증가, 도로의 혼잡 악화로 안전면에 대한 우려가 높아지고, 지능적인 감시 및 데이터 구동 리스크 관리 솔루션에 대한 수요가 증가하고 있습니다. 교통 환경이 복잡해짐에 따라 충돌 위험을 줄이면서 교통 흐름을 개선하는 실시간 시각화 기술, 자동 응답 기능 및 예측형 안전 기술에 대한 요구가 커지고 있습니다. 인공지능, 커넥티드 센싱 기술, 클라우드 기반 플랫폼의 지속적인 발전으로 현대 도로 안전 시스템의 정확성, 확장성 및 합리적인 가격이 향상되었습니다. 안전 의식 증가, 도시 인프라 확대, 일관된 안전 기준을 유지하면서 증가하는 교통량을 효율적으로 관리할 필요성이 시장 발전을 더욱 강화하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 금액

58억 2,000만 달러

예측 금액

142억 5,000만 달러

CAGR

9.8%

2025년 솔루션 분야는 79%의 점유율을 차지했고, 2035년까지 118억 달러에 달할 것으로 예측됩니다. 도로 안전 솔루션은 모니터링, 단속 지원 및 분석을 통합하는 플랫폼을 통해 제공되는 사례가 증가하고 있습니다. 이러한 플랫폼을 통해 당국은 상호 운용성과 확장성을 갖춘 기술을 도입할 수 있어 지속적인 모니터링, 예측 리스크 평가, 광범위한 스마트 모빌리티 구상과의 연계를 지원하고 있습니다.

사물인터넷(IoT) 부문은 2025년 33%의 점유율을 차지했고 19억 달러로 평가되었습니다. IoT 기반 도로 안전 시스템은 교통 네트워크 전반에 걸쳐 확장되어 지속적인 데이터 획득, 연결된 인프라 통신, 향상된 상황 인식을 가능하게 하며 운영 효율성과 도로 안전 향상에 기여하고 있습니다.

미국 교통안전 시장은 2025년 17억 5,000만 달러로 평가되었으며, 2026년부터 2035년까지 강력한 성장이 예상됩니다. 시장 확대는 전국 안전 프로그램, 공적 자금 증가, 도시 간 도로 및 도시 도로의 기술을 활용한 안전성 향상을 중시하는 장기적인 이동성 전략에 의해 지원됩니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 현황

수익률 분석

비용 구조

단계별 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

규제집행 확대

증가하는 도로 교통 사고로 인한 사망자 수

도시화와 차량 대수 증가

AI 및 IoT의 기술적 진보

스마트 시티 개발 이니셔티브

업계의 잠재적 위험 및 과제

높은 초기 투자 비용

데이터 프라이버시와 감시에 대한 우려

시장 기회

신흥 시장에서의 인프라 개발

민관협력 모델

자율주행차 및 커넥티드카 통합

고급 분석 및 빅데이터 활용

성장 가능성 분석

규제 상황

북미

미국 : SAE J328 액슬 및 드라이브 라인 부품 성능 요건

캐나다 : SAE J328 액슬 및 드라이브 라인 부품 성능 요건

유럽

영국 : 유엔 유럽 경제위원회 규칙 제13호 차량 제동 및 안정성 시스템

독일 : ISO 26262 도로 차량의 전기 전자 시스템의 기능 안전

프랑스 : UNECE 규정 제79호 ? 조향 및 차량 제어 시스템

이탈리아 : ISO 9001 ? 차동장치 제조 품질경영시스템

스페인 : ISO 14001 ? 차동장치 제조 환경경영시스템

아시아태평양

중국 : GB/T ? 자동차 차동장치 및 드라이브라인 성능 기준

일본 : ISO 26262 도로 차량의 전기 전자 시스템의 기능 안전

인도 : AIS 자동차 산업 규격(차축 및 차동 장치)

라틴아메리카

브라질 : ABNT NBR 자동차 구동계 성능 기준

멕시코 : 자동차 부품 성능 및 안전 기준(NOM)

아르헨티나 : ISO 9001 ? 자동차 부품 품질경영시스템

중동 및 아프리카

아랍에미리트(UAE) : UNECE 규정 제13호 ? 차량 제동 및 안정성 시스템

남아프리카 : ISO 26262 도로 차량의 전기 전자 시스템의 기능 안전

사우디아라비아 : 구동계 시스템에 관한 SASO 자동차 기술 규제

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

신규 기술

코스트 내역 분석

특허 분석

지속가능성과 환경적 측면

지속가능한 실천

폐기물 감축 전략

생산에 있어서의 에너지 효율

친환경 이니셔티브

장래 시장 전망과 기회

이용 사례

도로 안전 시스템의 아키텍처와 도입 모델

고정형 vs 이동형 vs 임시 배치

On-Premise형과 클라우드 기반의 아키텍처

집중형과 분산형 지령센터

기존 ITS 인프라와의 상호 운용성

조달 및 계약 모델

기존 설비투자(CAPEX) 조달

성과 연동 / 결과 연동 계약

수익 분배 및 위반 기반 수익화 모델

건설-운영-양도 및 컨세션 모델

경제적 영향과 투자 수익률(ROI) 평가

데이터 거버넌스, 프라이버시 및 사이버 보안의 틀

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 컴포넌트별, 2022-2035

솔루션

단속

신호위반 단속

과속 단속

버스 전용차로 단속

구간 단속

자동 번호판 인식(ALPR/ANPR)

사고 감지

백오피스

지능형 도로 교통 시스템

교통 관리 시스템

기타

서비스

컨설팅

지원 및 유지 보수

통합

도입 상황

제6장 시장 추정 및 예측 : 기술별, 2022-2035

인공지능 및 머신러닝

사물인터넷(IoT)

컴퓨터 비전

레이더 및 LiDAR

GPS 및 GNSS

클라우드 및 엣지 컴퓨팅 플랫폼

제7장 시장 추정 및 예측 : 용도별, 2022-2035

도시

고속도로

지방

공사 구간 안전 대책

기타

제8장 시장 추정 및 예측 : 최종 용도별, 2022-2035

정부기관

법 집행 기관

민간 사업자

제9장 시장추정 및 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

포르투갈

크로아티아

베네룩스

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

튀르키예

제10장 기업 프로파일

세계 기업

Motorola Solutions

Siemens

Verra Mobility

Cubic

Jenoptik

Sensys Gatso

Conduent

FLIR Systems/Teledyne FLIR

SWARCO

VITRONIC

Kapsch TrafficCom

지역 기업

Redflex

Clearview Intelligence

Traffic Management Technologies

Kria

Truvelo Manufacturers

Optotraffic

Laser Technology

Syntell

Dahua Technology

Saferoad

Emerging/Disruptor Players

IDEMIA

INRIX

Acusensus

Nexar

Samsara

Clearpath Robotics/AMAG

Mobileye

Waycare Technologies

CARMERA

SHW

영문 목차

영문목차

The Global Road Safety Market was valued at USD 5.82 billion in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 14.25 billion by 2035.

Market growth is supported by stronger regulatory frameworks introduced by governments worldwide, with an increasing emphasis on stricter compliance standards, improved enforcement, and long-term safety targets across road networks. Public authorities are prioritizing sustained investment in advanced road safety systems as part of broader transportation modernization programs. Rapid urban expansion, rising vehicle ownership, and increasingly congested roadways have intensified safety concerns, leading to higher demand for intelligent monitoring and data-driven risk management solutions. The growing complexity of traffic environments has increased the need for real-time visibility, automated response capabilities, and predictive safety technologies that improve traffic flow while reducing collision risks. Continuous progress in artificial intelligence, connected sensing technologies, and cloud-based platforms is enhancing the precision, scalability, and affordability of modern road safety systems. Market development is further reinforced by rising public awareness of safety, expanding urban infrastructure, and the need to manage higher traffic volumes efficiently while maintaining consistent safety standards.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$5.82 Billion

Forecast Value

$14.25 Billion

CAGR

9.8%

In 2025, the solutions segment accounted for 79% share and is projected to reach USD 11.8 billion by 2035. Road safety solutions are increasingly delivered through integrated platforms that combine monitoring, enforcement support, and analytics into cohesive systems. These platforms are enabling authorities to deploy interoperable and scalable technologies that support continuous monitoring, predictive risk evaluation, and alignment with broader smart mobility initiatives.

The internet of things segment held 33% share in 2025 and was valued at USD 1.9 billion. IoT-based road safety systems are expanding across transportation networks, enabling continuous data acquisition, connected infrastructure communication, and enhanced situational awareness to improve operational efficiency and roadway safety.

U.S. Road Safety Market was valued at USD 1.75 billion in 2025 and is expected to demonstrate strong growth between 2026 and 2035. Market expansion is supported by nationwide safety programs, increased public funding, and long-term mobility strategies that emphasize technology-enabled safety improvements across urban and intercity roads.

Key participants operating in the Global Road Safety Market include Siemens, Motorola Solutions, Kapsch TrafficCom, Verra Mobility, Conduent, Sensys Gatso, Cubic, IDEMIA, and Jenoptik. Companies active in the Road Safety Market are strengthening their competitive position by focusing on integrated technology development, large-scale deployment capability, and long-term partnerships with public authorities. Many players are investing in advanced analytics, connected platforms, and automation to deliver more accurate and proactive safety solutions. Emphasis is being placed on scalable system architectures that support expanding urban infrastructure. Firms are also pursuing geographic expansion and tailored solutions to meet regional regulatory requirements. Strategic collaborations, recurring service models, and strong post-deployment support are being used to build long-term client relationships. In addition, companies are prioritizing data security, system reliability, and compliance readiness to reinforce trust and sustain market leadership.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Technology

2.2.4 Application

2.2.5 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook & strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Regulatory enforcement expansion

3.2.1.3 Increasing road traffic fatalities

3.2.1.4 Urbanization and vehicle population growth

3.2.1.5 Technological advancements in AI and IoT

3.2.1.6 Smart city development initiatives

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment requirements

3.2.2.2 Data privacy and surveillance concerns

3.2.3 Market opportunities

3.2.3.1 Emerging Market Infrastructure Development

3.2.3.2 Public-Private Partnership Models

3.2.3.3 Integration with Autonomous and Connected Vehicles

3.2.3.4 Advanced Analytics and Big Data Utilization

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 United States: SAE J328 Axle and Driveline Component Performance Requirements

3.4.1.2 Canada: SAE J328 Axle and Driveline Component Performance Requirements

3.4.2 Europe

3.4.2.1 United Kingdom: UNECE Regulation No. 13 Vehicle Braking and Stability Systems

3.4.2.2 Germany: ISO 26262 Functional Safety of Electrical and Electronic Systems in Road Vehicles

3.4.2.3 France: UNECE Regulation No. 79 Steering and Vehicle Control Systems

3.4.2.4 Italy: ISO 9001 Quality Management Systems for Differential Manufacturing

3.4.2.5 Spain: ISO 14001 Environmental Management Systems for Differential Production

3.4.3 Asia Pacific

3.4.3.1 China: GB/T Driveline and Axle Performance Standards for Automotive Differentials

3.4.3.2 Japan: ISO 26262 Functional Safety of Electrical and Electronic Systems in Road Vehicles

3.4.3.3 India: AIS Automotive Industry Standards for Axles and Differentials